SMARTWORKS

Equity Metrics

May 8, 2026

Smartworks Coworking Spaces Limited

Diversified Commercial Services

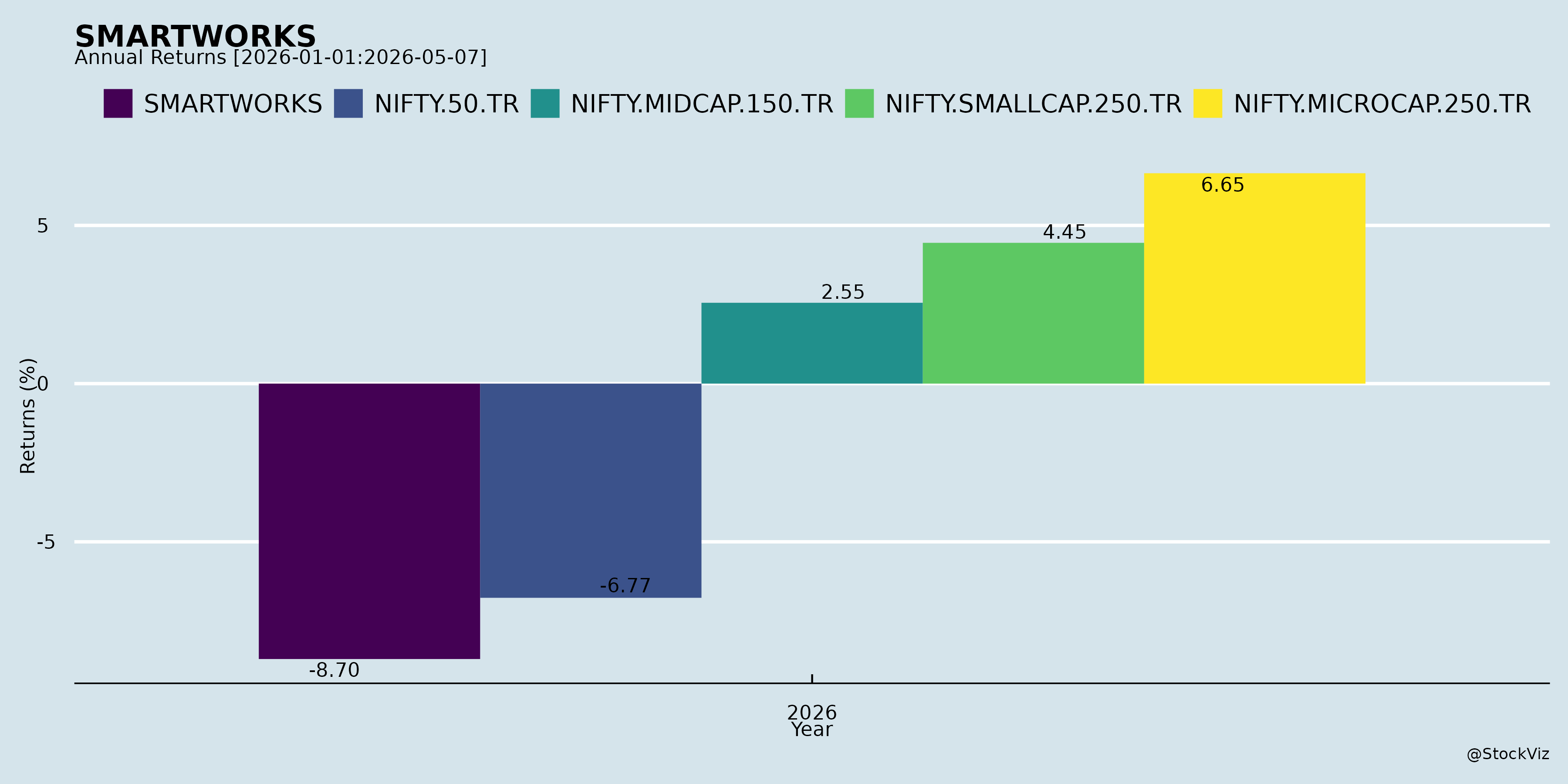

Annual Returns

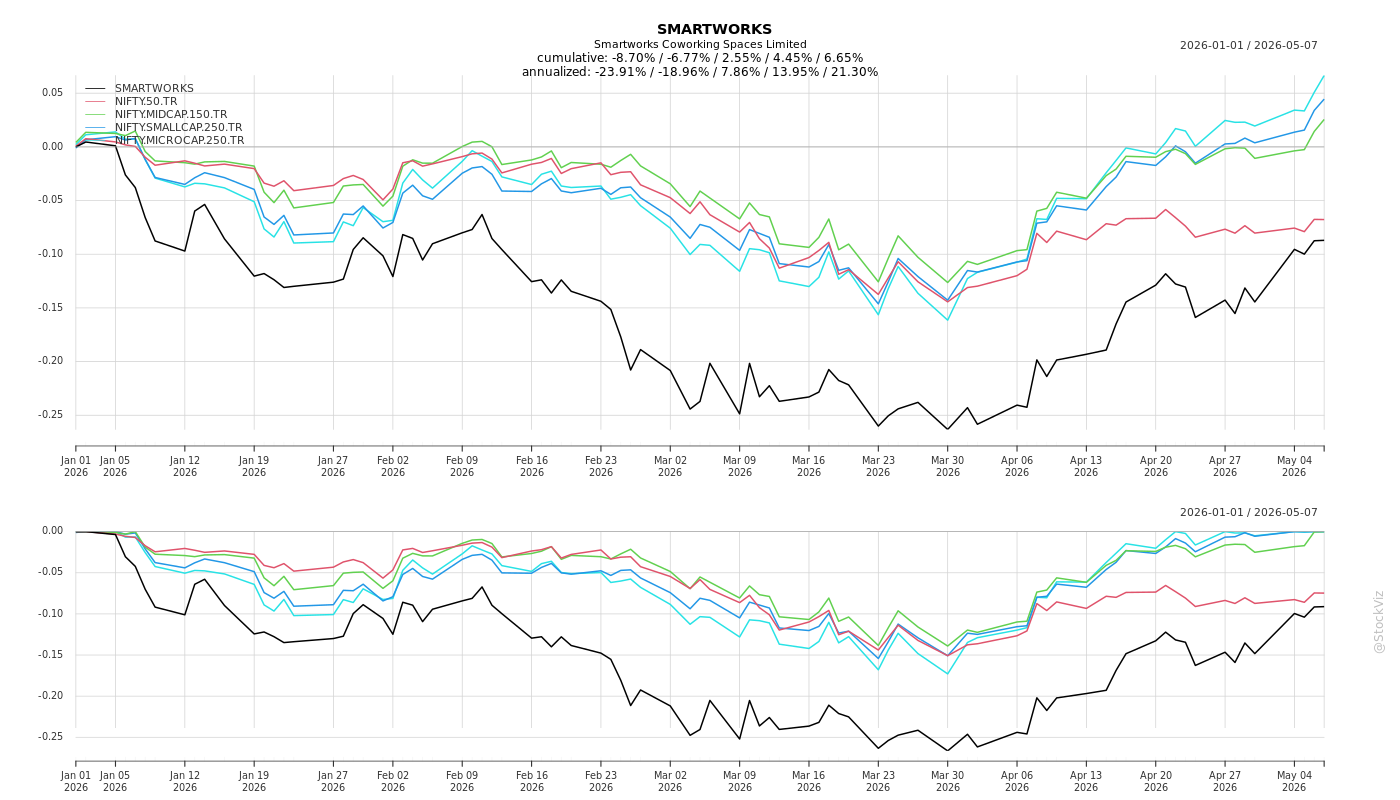

Cumulative Returns and Drawdowns

Fundamentals

Ownership

Margined

AI Summary

asof: 2025-12-08

Smartworks Coworking Spaces Limited (SMARTWORKS) – Investment Thesis & Business Analysis

As of Q2 FY26 Conference Call – November 7, 2025

Company Overview

Smartworks is India’s largest pan-India managed office platform, operating over 12.7 million sq. ft. across 14 cities and serving 760+ enterprise clients. The company operates through a standardized, tech-enabled, campus-style managed workspace model, targeting large enterprises and Global Capability Centers (GCCs). It transitioned to being a publicly listed company in FY26, with strong growth dynamics and self-sustaining operating cash flows.

1. Tailwinds (Growth Drivers)

1.1 Structural Shift in Office Demand Toward Flexibility

- Flexible workspace penetration in Grade-A offices has increased from 10% → 25% (Cushman & Wakefield), indicating a structural behavioral shift.

- Enterprises are prioritizing flexibility, speed-to-market, experience, and technology-enabled solutions over traditional long-term leases.

- Smartworks is positioned at the gold standard of managed campuses, blending design, tech, and scale.

1.2 Surge in GCC (Global Capability Center) Demand

- GCCs to drive ~40–45 million sq. ft. of new office demand in FY26–FY27.

- Smartworks sees 15% of rental revenue from GCCs today, with expectations of doubling this in 2–3 years.

- Launched SmartVantage, a dedicated platform offering workspace + staffing, compliance, legal, tax, and onboarding—making it a one-stop partner for GCCs.

1.3 High Retention of Enterprise Clients & Scaling Client Sizes

- 35% of rental revenue now comes from clients with >1,000 seats, up from 12% three years ago.

- Average tenure for large clients > 50 months, showing high client stickiness.

- Enterprises view Smartworks as a Pan-India infrastructure partner—not just a short-term office provider.

1.4 Strong Pre-fill Demand & Client-Led Expansion

- Over 30% of new capacity is pre-filled by existing clients.

- Expansion decisions are often driven by demand signals from existing clients, reducing market risk.

- Example: Vikhroli campus (815,000 sq. ft.) has 30–35% demand visibility even before handover.

1.5 Improving Unit Economics and Scalability

- Blended center-level EBITDA margin: ~23–24% (excluding corporate costs).

- Normalized EBITDA margin (after corporate): 16.4%, up from 13.4% YoY.

- CAPEX is kept low (~₹1,300/sq. ft.) due to asset-light, build-outs on demand.

- Operating leverage increasing as mature centers (>7.5M sq. ft. at 88% occupancy) become profitability engines.

1.6 Favorable Landlord Dynamics

- 24% of portfolio now from institutional landlords (DLF, Hiranandani, Tata, Panchsheel), up from 18%.

- Strong brand recognition enables securing entire buildings rather than fragmented floors, improving campus integrity and pricing power.

1.7 Net Debt Negative & Strong Cash Generation

- Net debt negative ₹59 crores, reducing gross debt by ~45% post-IPO.

- Normalized operating cash flow: ₹62 crores, OCF/EBITDA ~1x.

- Security deposit arbitrage: Clients pay deposits upfront, offsetting landlord deposits and funding CAPEX.

1.8 Capacity Visibility and Long-Term Supply Pipeline

- 14 million sq. ft. signed and in pipeline, with 100% FY26/FY27 supply visibility.

- FY28 sourcing already underway.

- 1M sq. ft. of new supply + 1.4M sq. ft. of existing centers maturing in H2 FY26, driving revenue growth and margin expansion.

2. Headwinds (Challenges & Near-Term Concerns)

2.1 Decline in Retention Rate (from 94.5% → 74%)

- Due to expiration of low-rent, long-term contracts signed during 2020–21 (COVID phase).

- Management calls this “healthy churn” – exiting below-market deals and re-leasing at higher rates.

- However, such churn could persist over next 2–3 quarters as more legacy contracts expire, potentially pressuring reported retention.

- Commitment occupancy (88%) remains strong, mitigating revenue risk.

2.2 Blended Occupancy Below Mature Centers

- Blended occupancy: ~81%, vs. mature centers: 88%.

- Expansion into new and under-construction centers has diluted the overall figure.

- The gap is temporary but will drag center-level margins until ramp-up completes (~12–14 months typical maturity cycle).

2.3 CAPEX and Cash Flow Mismatch in Near Term

- Heavy security deposit outflows (~2M sq. ft. secured in Q2) for centers that will hand over in FY27.

- This creates negative OCF impact in the short term, though it’s strategic and reversed as client deposits come in.

- Risk: Working capital strain if ramp-up delays occur due to macro or demand shocks.

2.4 Regional Supply Constraints in Mature Markets

- Bombay, Gurgaon, Delhi have limited availability of large-format, stand-alone buildings.

- Demand exists, but execution depends on finding suitable mega-campuses.

- However, management believes their model mitigates this by converting smaller clusters into large centers.

2.5 Decline in City Count (15 → 14)

- Withdrew from Jaipur (49,000 sq. ft.) due to scalability constraints of existing facility.

- Indicates selective exit when asset size doesn’t support long-term growth targets.

- Not a major headwind, but underlines barrier in smaller cities without large assets.

3. Growth Prospects

| Metric | Current | Near-Term Outlook |

|---|---|---|

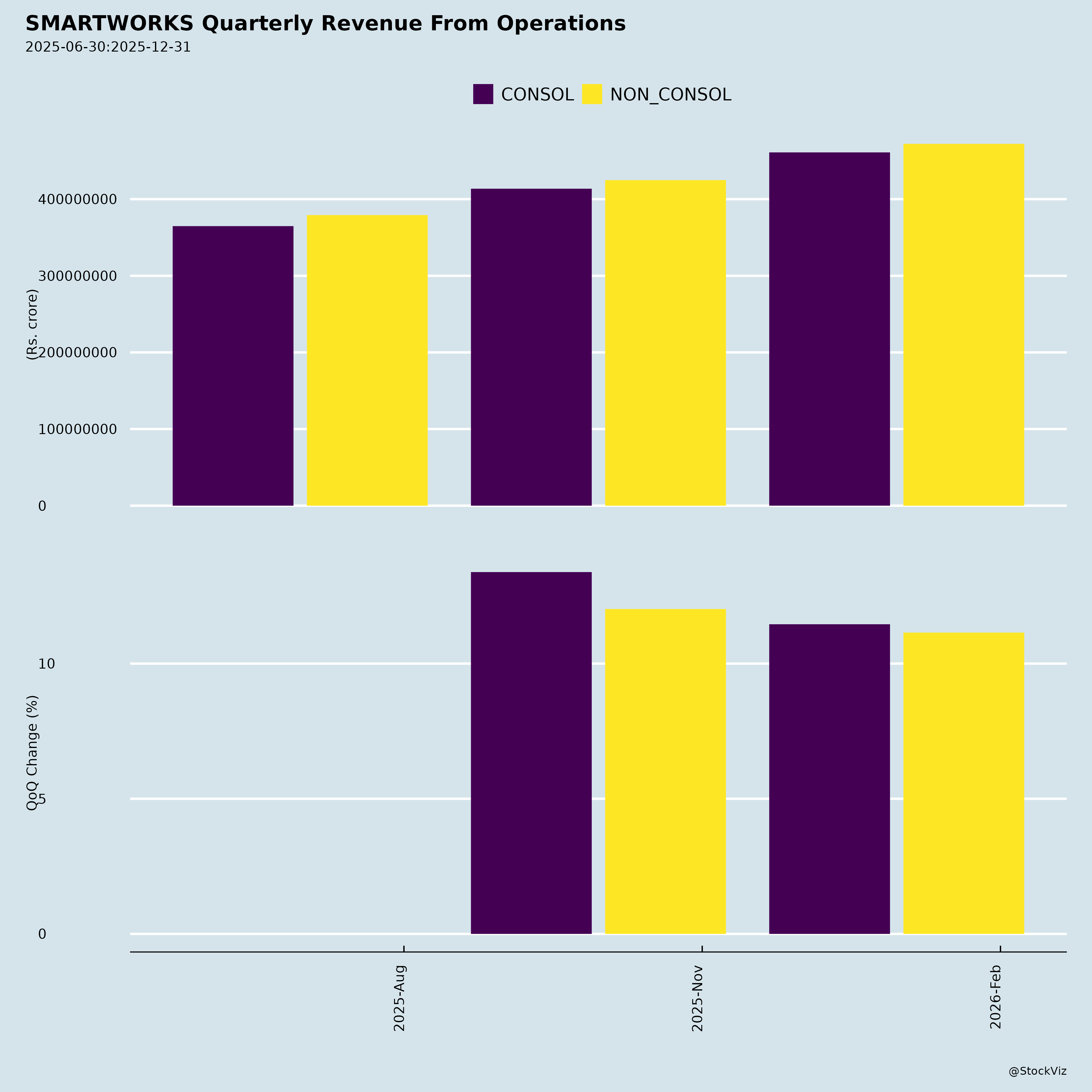

| Revenue Growth | ₹425 crores (Q2 FY26, +21% YoY, +12% QoQ) | Aiming for >30% annual growth; strong tailwinds support acceleration in H2 FY26 |

| Capacity Growth | 12.7M sq. ft. | +2.4M sq. ft. in H2 FY26, with full visibility |

| GCC Revenue | 15% of rental | Expected to double in 2–3 years; SmartVantage to drive this |

| EBITDA Margin | 16.4% | Set to expand due to operating leverage, center maturity, lower corporate costs |

| ROCE | 14.3% | Expected to double in 2 years; industry-leading efficiency |

| City Expansion | 14 cities | Focused on Tier-1 cities with large buildings, with targeted entry into new Tier-2 markets |

Long-Term Vision

- Scale to ~15–16M sq. ft. with 12M+ sq. ft. in mature centers (~80%+ occupancy).

- Self-sustaining CAPEX model: No external funding needed for 25–30% growth.

- Transition from growth phase to sustainable high-margin scale profitability.

4. Key Risks (Forward-Looking)

| Risk | Nature | Mitigation |

|---|---|---|

| Macro demand slowdown | Economic downturn could delay GCC expansions or corporates downsizing real estate | High committed occupancy (88%) provides buffer; clients stick long-term |

| Competition from traditional landlords or other operators | Rivals offering flex services or landlords offering managed spaces | Smartworks’ large campus model, tech, pan-India scale, and GCC partnerships create high entry barriers |

| Ramp-up delays in new centers | Construction delays, slower leasing than expected | Leasing begins pre-handover; 30–35% pre-fill reduces risk |

| Overestimation of GCC growth | If foreign investment into India slows | Diversified across BFSI, IT, healthcare; GCC penetration still early stage |

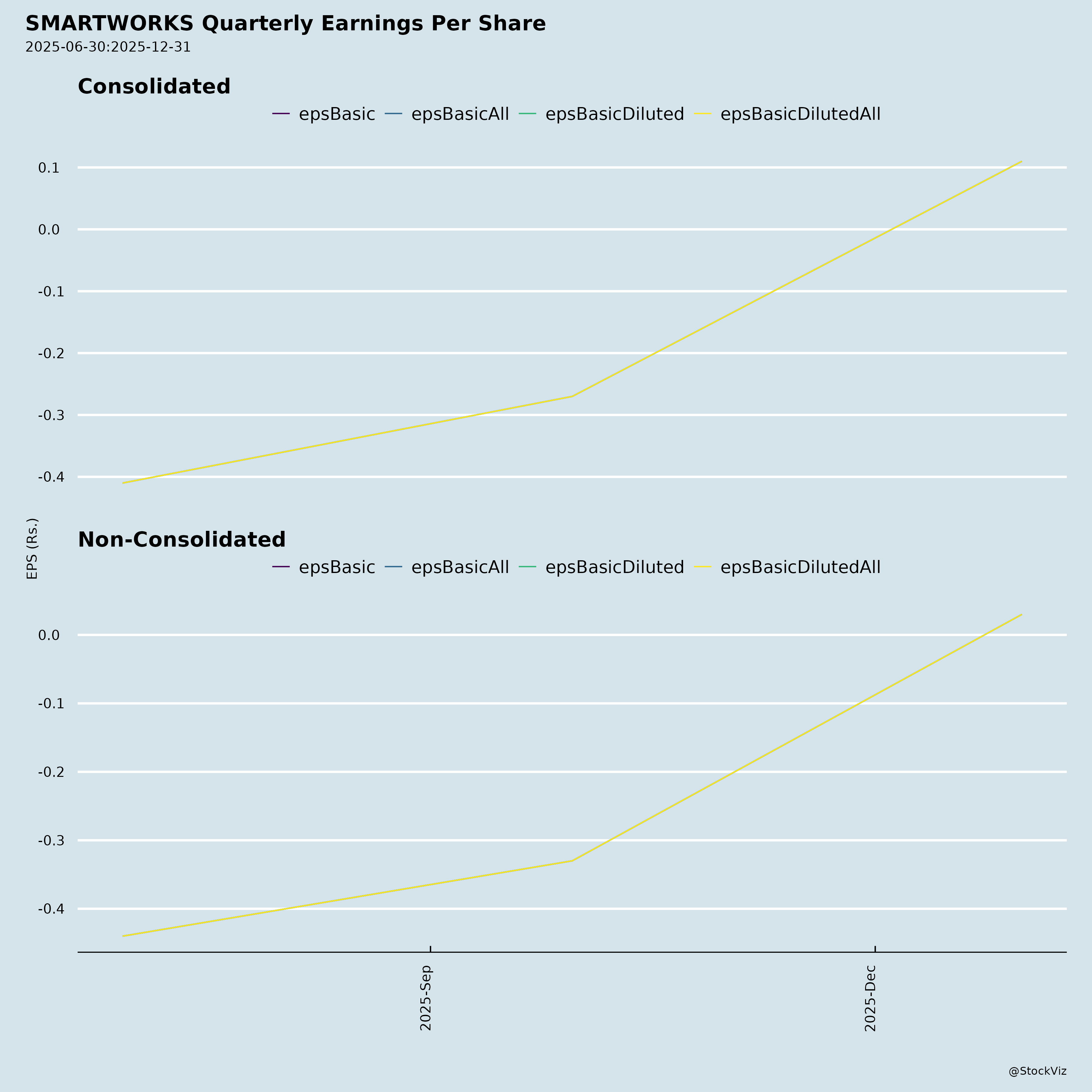

| IND AS 116 accounting impact | Leases create non-cash provisions, depressing reported PBT | Management expects normalized and reported profits to converge over time |

| Dependence on large corporate clients | Concentration risk in top clients | Portfolio diversified across sectors; clients are sticky and long-term |

5. Summary (Investment Perspective)

✅ Strengths & Why Invest

- Market leader in institutional-grade flexible office space with strong ESG and scalability.

- Structural tailwinds: GCC boom, hybrid work, corporates shifting to managed models.

- High predictability: 88% committed occupancy, long leases, enterprise base.

- Asset-light and capital-efficient: High ROCE (14.3%), net debt negative, strong OCF.

- Margin expansion path through operating leverage and scale.

- Strategic product innovation via SmartVantage positions it as a GCC ecosystem enabler.

⚠️ Concerns & Watch-Outs

- Temporary suppression of retention rates and blended occupancy due to legacy contract churn.

- Short-term cash outflows for deposits may pressure net cash, despite being strategic.

- Geographic concentration in Tier-1 cities limits diversification.

- Need to secure large-format buildings consistently to sustain exponential growth.

Final Verdict: Bullish Long-Term, with Near-Term Inflation of Costs and Churn

Rating: BUY

Target Horizon: 2–3 Years

Smartworks is at an inflection point—leveraging its scale, brand, and institutional credibility post-listing to capture the transformation of India’s office ecosystem. While near-term metrics like retention and cash flow may be subdued, the core demand strength, GCC focus, and margin trajectory support a multi-year growth story. The company is well-positioned to become the default Pan-India infrastructure provider for enterprise and GCCs, with a path to sustainable double-digit ROCE and EBITDA margins >20%.

Data Sources: Q2 FY26 Earnings Transcript, Investor Presentation, Shareholder Letter (implied), Management Commentary

Last Updated: November 12, 2025

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.