Diversified Commercial Services

Industry Metrics

May 8, 2026

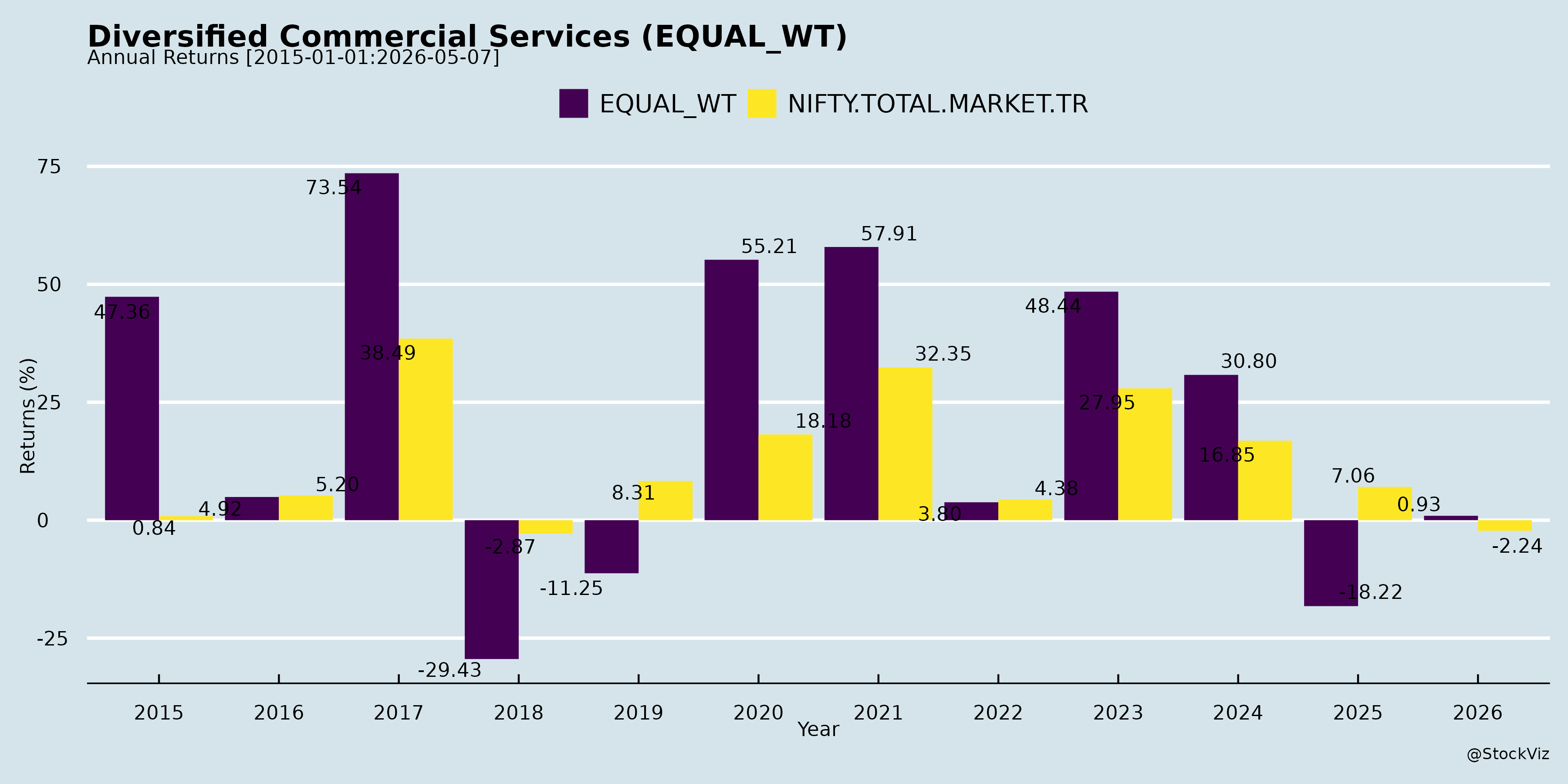

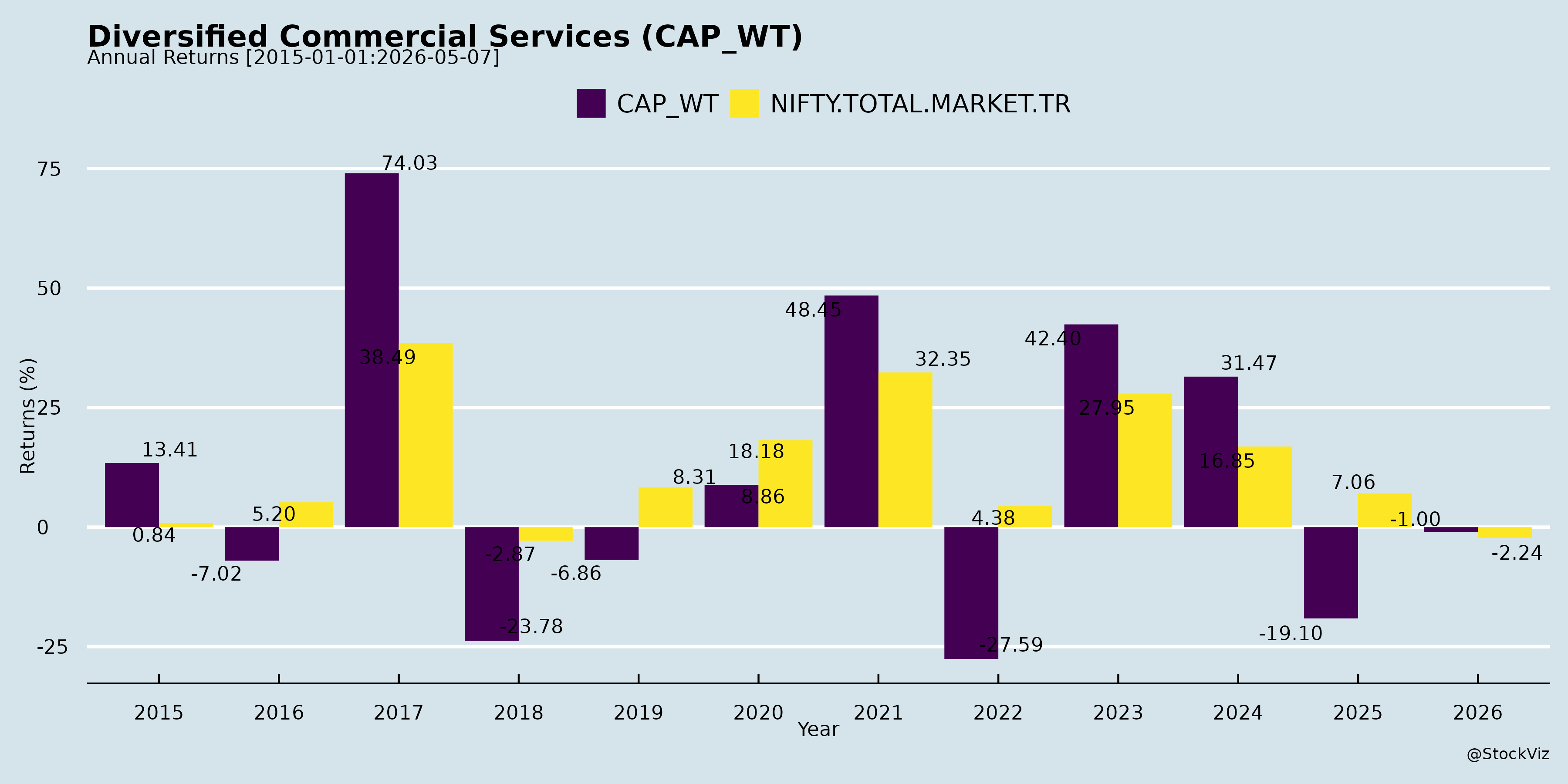

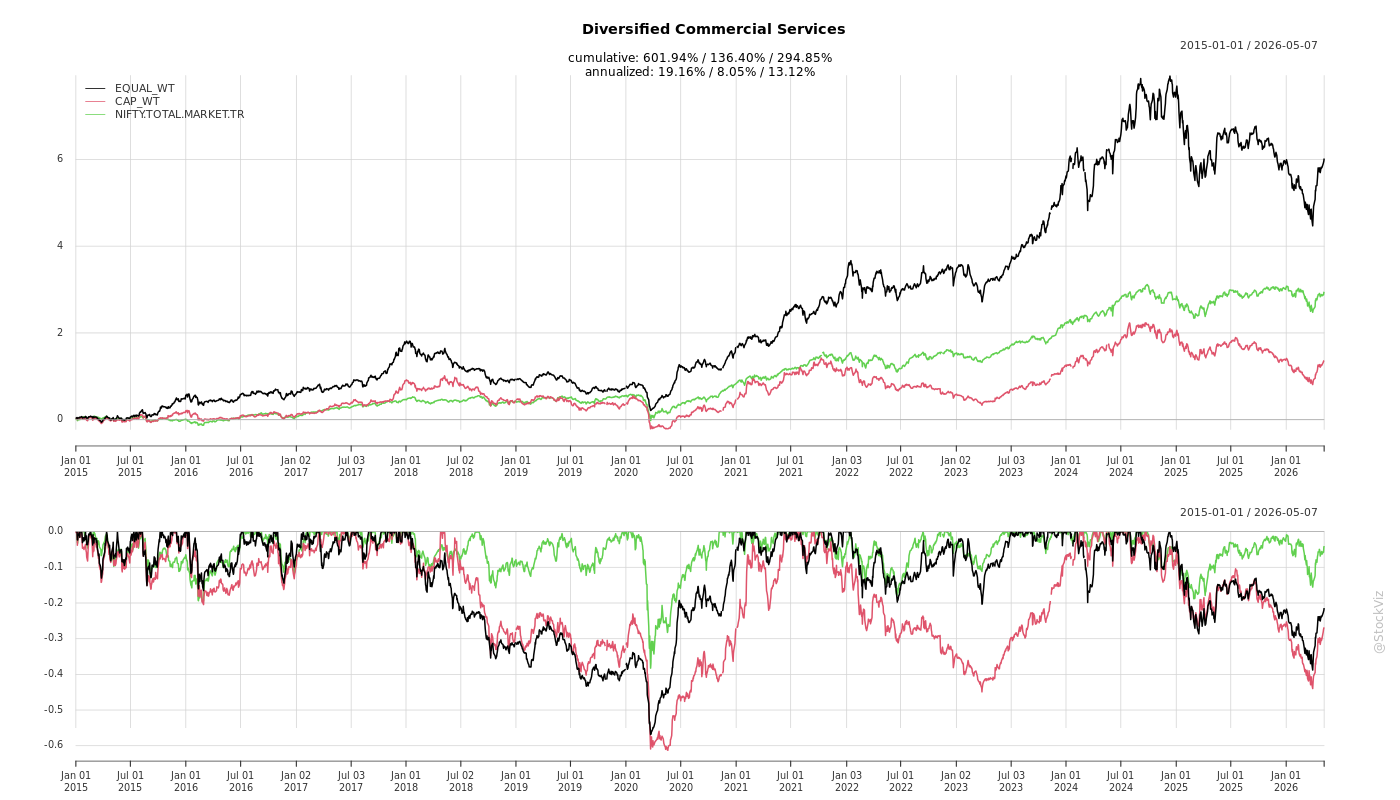

Annual Returns

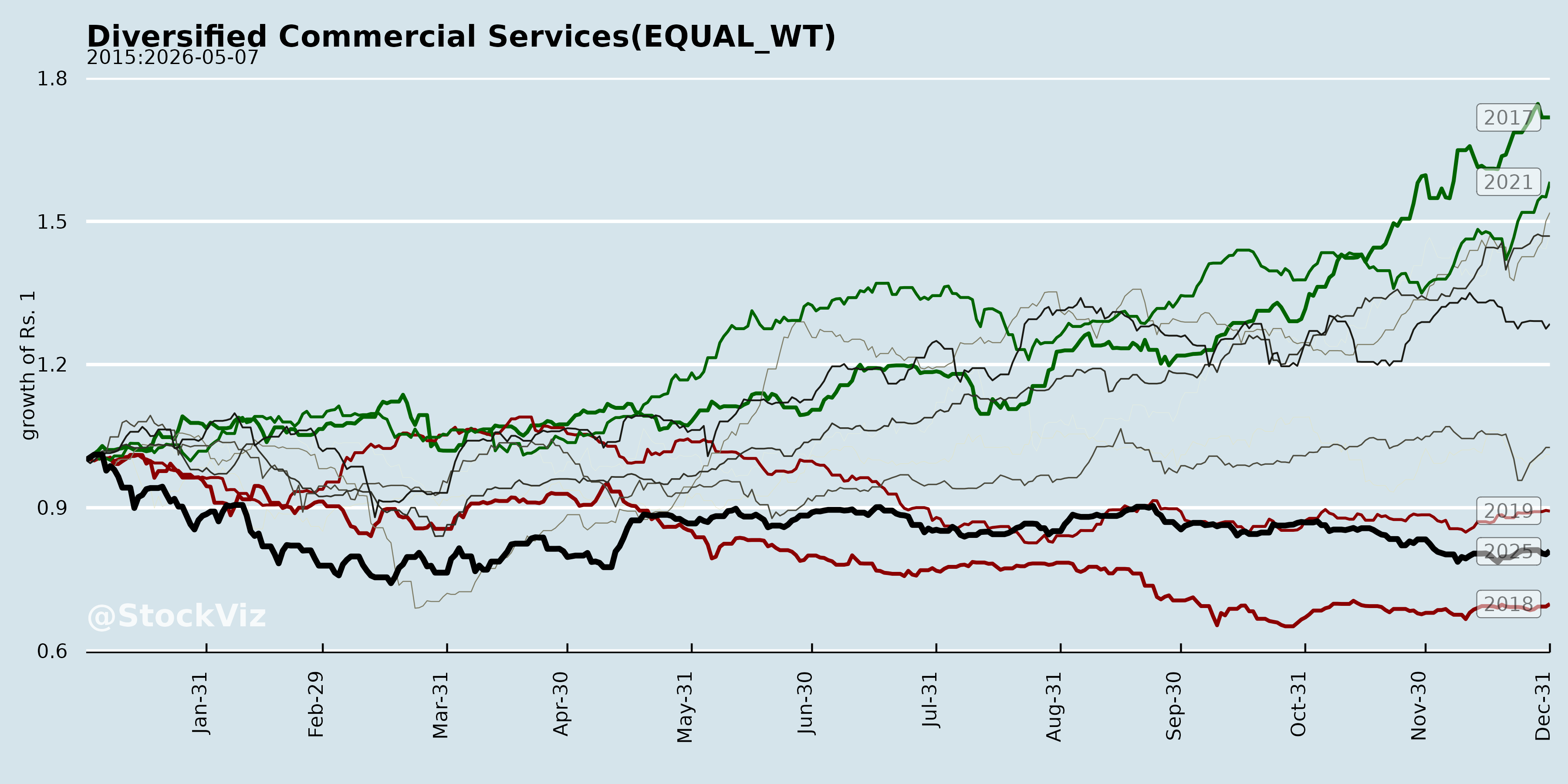

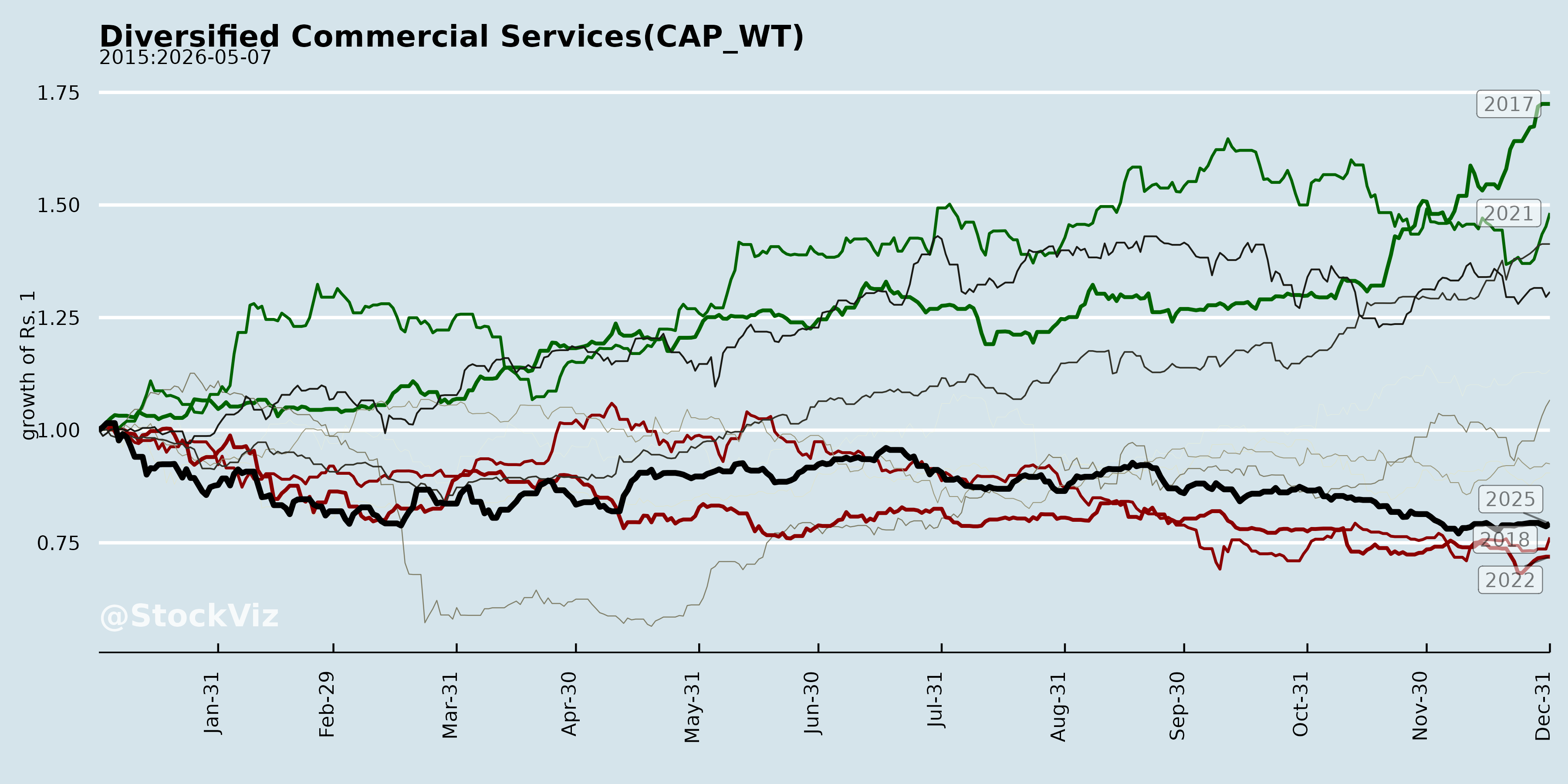

Cumulative Returns and Drawdowns

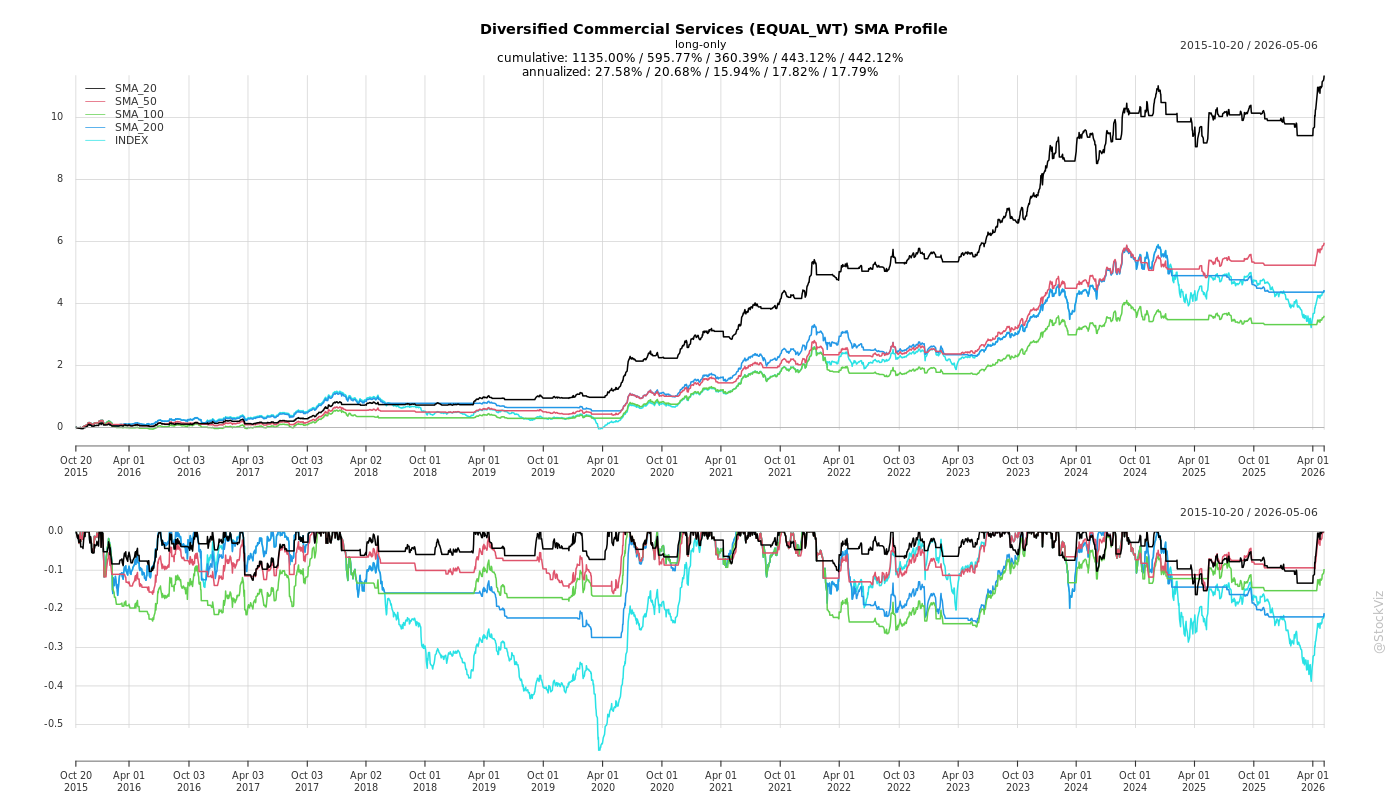

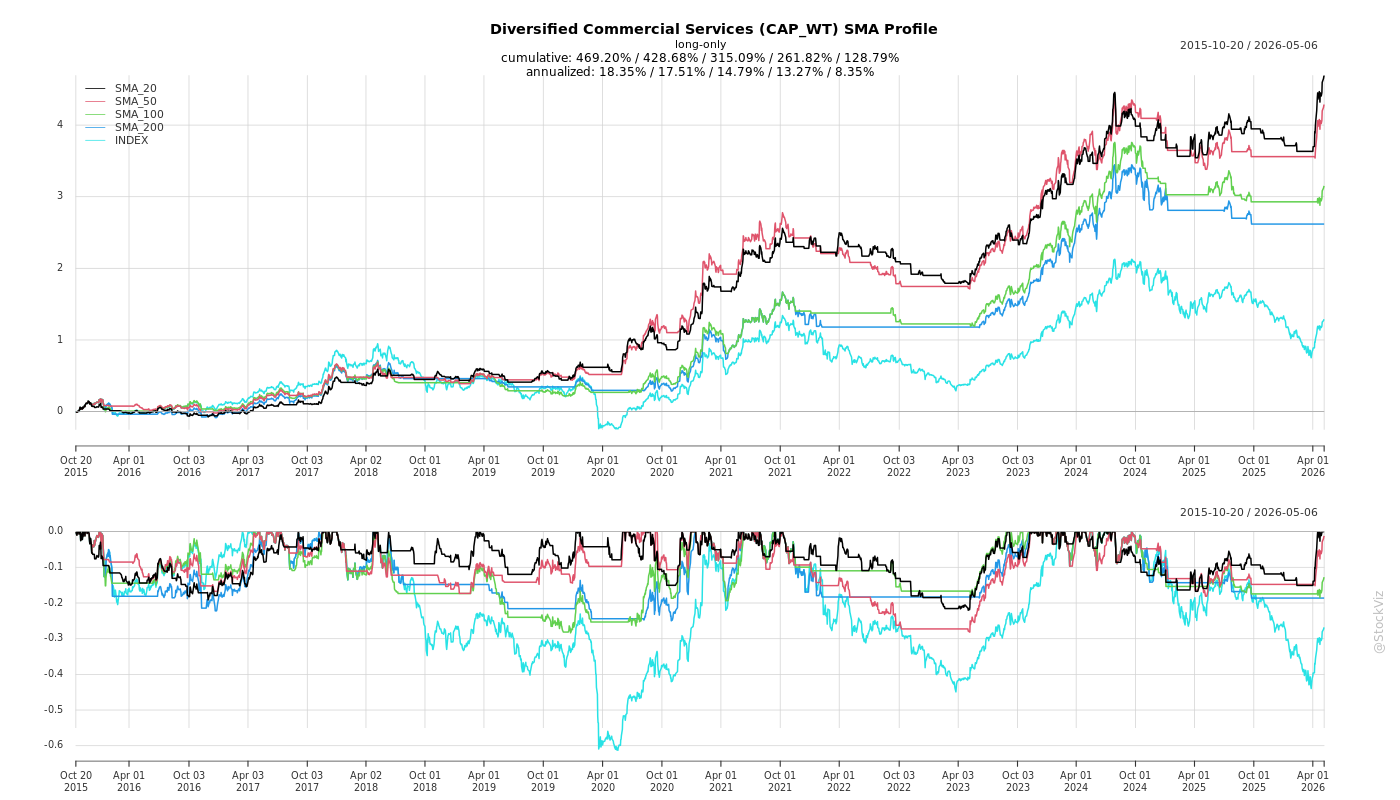

SMA Scenarios

Current Distance from SMA

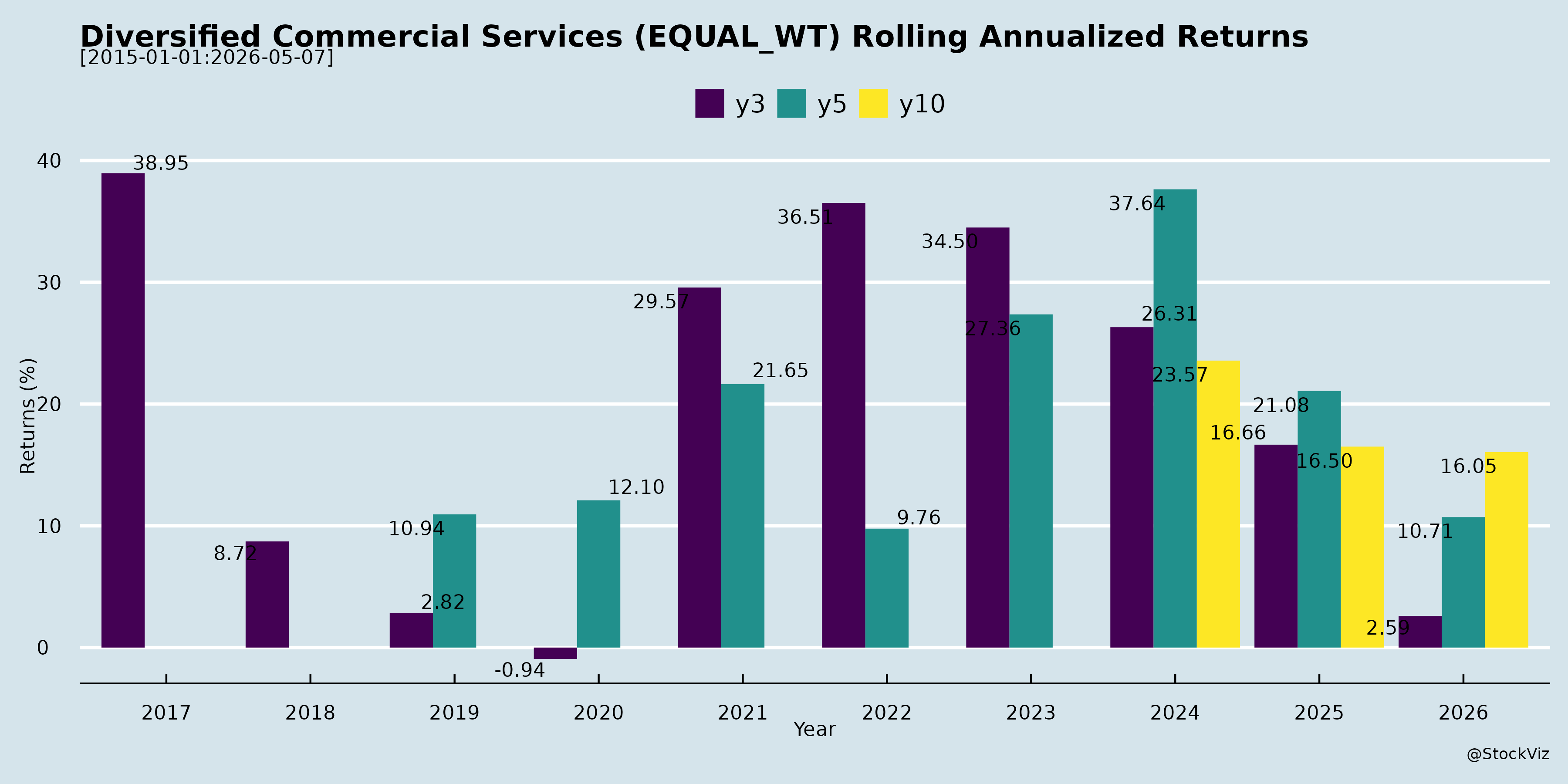

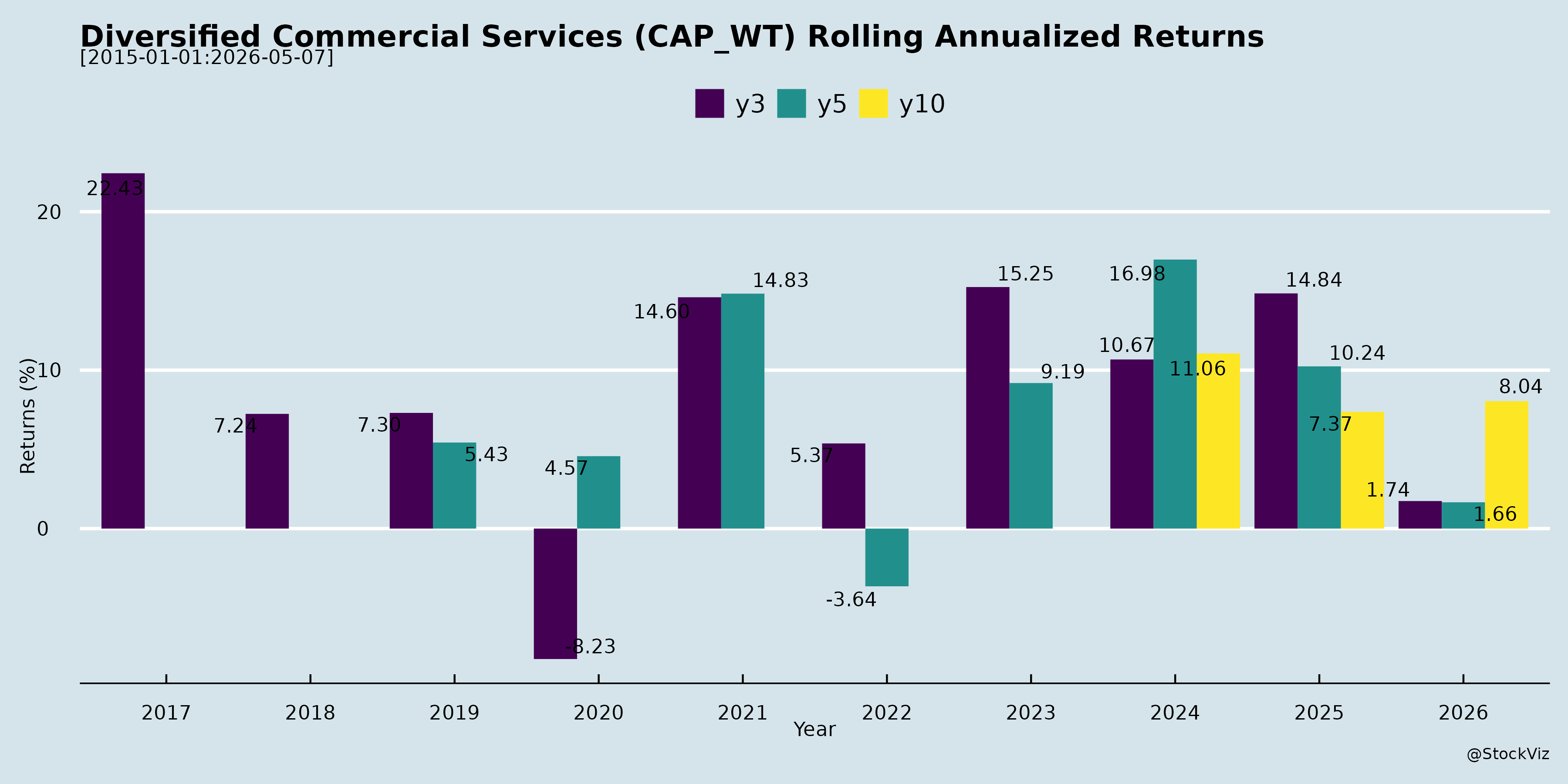

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-15

Based on the sources, companies across various sectors have experienced a dynamic evolution of challenges and opportunities over time. Many have had to adapt to regulatory shifts, technological disruptions, and pricing pressures by pivoting their business models, expanding geographically, and diversifying their portfolios.

Here is a detailed breakdown of how challenges and opportunities have evolved across key industries:

1. Human Resources, Staffing, and Facility Management

Evolving Challenges: * Client Insourcing and Competition: Quess Corp faced a significant one-time event where a large BFSI customer chose to in-source a massive volume of roles, highlighting the risk of relying heavily on single, volume-based clients [1, 2]. Similarly, Krystal Integrated Services has grappled with high competition and the heavy expenditure required to open new business offices [3]. * Industry-Specific Disruptions: ACE Integrated Solutions faced severe liabilities in the examination management sector. Escalating incidents of organized cheating, question paper leaks, data breaches, and high litigation exposure made the sector increasingly unviable [4]. Furthermore, rising operational costs and the rapid disruption of Artificial Intelligence and automation reduced the long-term need for large-scale traditional examinations [4]. * Talent Acquisition: Across the board, changing market dynamics and the emergence of new skills have made attracting and retaining top talent a persistent challenge [5].

Evolving Opportunities: * Portfolio Diversification: To navigate headwinds, Quess Corp doubled down on a multi-vertical strategy, shifting focus from entry-level roles to high-skill, niche, and digital technology areas [6-9]. They also expanded into the Middle East, identifying “blue ocean” opportunities in retail, e-commerce, and banking [10, 11]. * Strategic Pivots: Recognizing the structural decline in the examination industry, ACE Integrated Solutions pivoted toward private training, architecture, turnkey construction projects, Building Information Modelling (BIM), and defense applications [4, 12]. Kapston is strategically entering the Business-to-Consumer (B2C) marketplace to offer integrated home services like cleaning, EPC (electrical, plumbing, carpentry), and beauty services [13]. * Compliance as a Tailwind: For formalized players like Bluspring Enterprises, the introduction of stringent compliance codes has become a massive opportunity. Because it is becoming difficult for clients to work with non-compliant vendors, highly compliant and safety-first operators expect their bargaining power and market share to increase [14, 15]. Bluspring is also transitioning from traditional manpower supply to SLA-based operations and maintenance (O&M) [16, 17].

2. Infrastructure, Heavy-Lift, and Energy Exploration

Evolving Challenges: * Policy Shifts and Market Contraction: Sanghvi Movers Limited experienced a “perfect storm” around 2017 when the wind energy sector shifted from Feed-in Tariffs to reverse auctions [18-21]. Aggressive bidding led to unviable tariffs and industry-wide margin compression [19, 21]. Combined with OEM consolidation and peak debt burdens from heavy fleet capital expenditures, crane utilization collapsed [18, 20]. * On-Ground Execution Issues: Inox Green and Inox Wind face routine, quarter-to-quarter infrastructure challenges, including acquiring land, establishing grid connectivity, and preparing 220 kV substations [22-25].

Evolving Opportunities: * Geographic and Sector Expansion: Sanghvi Movers evolved from being a “Nation Builder” to a “Global Builder” by expanding its heavy-lifting solutions to the GCC region and capitalizing on the untapped white space in the broader renewables sector [26-31]. * Broader Renewable Adoption: The wind sector in India is expanding beyond traditional strongholds (Gujarat, Maharashtra, Karnataka) into new states like Rajasthan, Andhra Pradesh, and Madhya Pradesh, aided by growing PGCIL grid connectivities [32, 33]. * Global Mining Supercycle: South West Pinnacle is capitalizing on a global mineral exploration supercycle fueled by the transition to clean energy and reindustrialization [34]. They are expanding into Oman—where the government is diversifying away from oil into mining—and targeting emerging opportunities in Africa, the Middle East, and Central Asia [35, 36].

3. Real Estate and Flexible Workspaces

Evolving Challenges: * Client Concentration and Customized Assets: Awfis Space Solutions faces risks when building massive, dedicated centers (500 to 1,000+ seats) customized for single large clients. If these clients leave after their 36 to 60-month lock-in periods, the resulting drop in occupancy and high refurbishment costs can negatively impact the P&L [37-40]. Awfis also faced short-term revenue dips due to environmental (GRAP) restrictions in North India [41, 42].

Evolving Opportunities: * Shift to Flexible Solutions: The way companies consume real estate has fundamentally evolved. Flexible workspaces are transitioning from tactical, interim solutions to core components of enterprise real estate strategies [43-45]. * GCCs and Tier-2 Growth: There is rising demand from Global Capability Centers (GCCs), bolstered by measures in the Union Budget 2026 that offer long-term tax holidays for foreign companies using India-based infrastructure [46-49]. Furthermore, Awfis notes a 16% year-on-year growth in Tier-2 seat capacity, showing the adoption of flexible models beyond major metropolitan areas [50, 51]. * Infrastructure Corridors: Nesco is expanding its real estate footprint beyond urban centers by developing “Wayside Amenities” across express highways, capturing a new market of fuel and non-fuel services for travelers [52, 53].

4. Financial and Cash Management

Evolving Challenges: * Pricing Pressures and Cost Increases: Radiant Cash Management Services is facing pricing pressures from clients, particularly concerning low-volume collection points [54, 55]. While the overall volume of cash handled has remained stable, the sheer number of physical points has increased, which drives up the cost of cash executives and cash vans [54, 55].

Evolving Opportunities: * Untapped Markets and New Services: The retail cash management industry remains highly under-penetrated, with less than 3% of retail outlets currently utilizing these services [56]. Radiant is evolving by targeting Tier 3+ locations (like UP, West Bengal, Assam, and Odisha) where populations lack access to new-age fintech [57, 58]. They are also turning retail outlets into business correspondents to offer a wider variety of financial services, creating sustained annuity revenue models [57, 58].

5. Jewelry and Diamond Certification

Evolving Opportunities: * The global diamond and jewelry industry is transforming due to rising disposable incomes, an expanding middle class, and the rapid adoption of affordable, sustainable Lab-Grown Diamonds (LGDs) [59]. As consumer demand for independent certification grows globally, companies like IGI are expanding their service delivery formats (such as mobile and in-factory labs) to build trust and capture market share [59, 60].

What are the headwinds affecting this industry?

asof: 2026-04-15

Staffing and Workforce Management Industry * Client Insourcing and De-hiring: The industry has experienced seasonal softness and de-hiring, particularly in the Banking, Financial Services, and Insurance (BFSI) and Consumer, Retail & Telecom (CRT) verticals [1-4]. A significant headwind has been large BFSI customers choosing to in-source large volumes of talent onto their own payrolls, directly impacting headcount growth [5-8]. * Regulatory Changes and Compliance Costs: The transition to the new Labour Code requires a complete reset of wage structures and client budgets [9, 10]. This has created interim friction as clients take time to model and factor these new costs into purchase orders [11-14]. Furthermore, new escrow account processes mandated by the RBI and state governments have unfortunately delayed collections in some instances [15, 16]. * Macro-economic Slowness: General slowness in the economy has presented overarching challenges to headcount additions and growth [17].

Wind Energy and Infrastructure Development * Site Readiness and Execution Delays: A major challenge is the delay at customer sites, which leads to the postponement of wind turbine off-takes [18-21]. Because the infrastructure setup is often out of the equipment supplier’s control and must be provided by the buyers, any mismatch results in project bottlenecks [22-25]. * Ground-Level Logistics: The industry routinely faces on-ground hurdles such as land acquisition issues, delays in substation readiness, and challenges in securing 220 kV line connectivity [26-29].

Crane Rental and Heavy-Lift Industry * Policy Shifts and Margin Compression: Historically, the shift from Feed-in Tariffs to reverse auctions triggered industry-wide margin compression, causing aggressive bidding that rendered many megawatt projects unviable [30, 31]. * OEM Consolidation and Debt: The sector has suffered from OEM consolidation (with wind OEMs dropping from 14 to 4-5) and severe debt servicing stress, as business contractions coincided with peak leverage [30-33]. Current risks also include a 2-3% margin dilution risk and the inherent dangers of a heavily capital-intensive, debt-reliant business model [34, 35].

Cash Management and Logistics Industry * Impact of Digitization: The rapid adoption of digital payments has stunted the growth of cash throughput, particularly in Tier 1 and Tier 2 locations [36, 37]. * Loss of Key Segments: Companies are facing a reduction in collection points within the railways and microfinance subsegments, alongside a degrowth in the e-commerce logistics segment [38-41]. * Rising Costs and Pricing Pressures: While the volume of cash handled has remained stable, the number of collection points has increased, thereby driving up the overall cost of servicing these points [42, 43]. Simultaneously, the industry faces stiff competitive pricing pressures from clients, particularly for low-volume points or highly competitive large-scale deals [42-45].

Flexible Workspace and Co-working Industry * Pollution Norms and Execution Delays: The construction and fit-out segments of this industry have faced temporary project deferrals and execution delays heavily linked to GRAP-IV pollution restrictions in specific regions [46-49]. * Supply Pipeline Hurdles: Operators have occasionally faced delays by landlords in property handovers, leading to lower-than-expected seat additions in managed aggregation models [46-51].

Examination and Recruitment Services * Security and Reputational Risks: The industry is increasingly plagued by escalating incidents of malpractice, organized cheating, question paper leaks, and data breaches, which create severe reputational and compliance liabilities [52]. * Cost and Technological Disruption: Rising operational costs for manpower, infrastructure, and strict security protocols are rapidly outpacing profit margins [52]. Additionally, rapid technological disruption from Artificial Intelligence and automation is reducing the long-term viability and need for large-scale traditional physical examinations [52].

Telecom Support and Active Infrastructure * Delayed Network Rollouts: The telecom vertical has seen sequential revenue dips due to a noticeable slowdown and weakness in the rollout of new networks by major telecom operators [53, 54]

What are the key things to understand about this industry?

asof: 2026-04-15

Your query asks about “this industry,” but the provided sources actually contain financial and strategic information spanning several distinct industries within the broader business-to-business (B2B) and infrastructure services landscape. Could you please clarify if you are interested in one specific sector?

In the meantime, to provide a comprehensive answer, here are the key things to understand about the major industries covered in the sources:

1. Flexible Workspaces & Managed Offices (Co-Working)

- Structural Demand Shifts: The commercial real estate environment is undergoing a massive structural shift as corporate occupiers increasingly prefer flexibility [1], [2]. Companies are moving away from traditional real estate models to prioritize speed-to-market, capital efficiency, compliance, and scalability [1], [2].

- The GCC Boom: A major catalyst for this sector is the rapid expansion of Global Capability Centers (GCCs) in India, driven by the country’s deep talent pool and structural cost advantages [3], [4]. GCCs are projected to account for nearly 40% of total office space absorption by 2026 [3], [4].

- Evolution of Managed Offices: While traditional co-working spaces continue to cater to startups, freelancers, and small cohorts, “Managed Offices” have decisively emerged as a core growth engine for operators [5], [6], [7]. These bespoke, single-tenant spaces are tailored for large enterprises and GCCs that want to outsource their entire workspace lifecycle while retaining their brand identity and exclusivity [8].

- Asset-Light Strategies & Premium Focus: To improve profitability and return on capital employed (ROCE), flexible workspace operators are increasingly utilizing asset-light “managed aggregation” models rather than taking on heavy traditional leases [9], [10]. Network expansion is heavily focused on premium Grade-A and elite locations, alongside growing traction in Tier-2 cities as distributed workforce models become more popular [11], [12].

2. Staffing, Recruitment & HR Services

- Massive Market Growth: The Indian flexi-staffing market is currently valued at approximately USD 10 billion and is expanding at an extraordinary 28% year-over-year [13]. Customers utilize staffing firms to maintain workforce flexibility, ensure compliance efficiency, and focus on their core business activities [14].

- Risk Mitigation via Multi-Vertical Strategies: To insulate themselves against economic headwinds, large staffing firms are doubling down on multi-vertical strategies [15], [16]. By balancing volume-driven sectors (like BFSI and retail) with value-driven sectors (like manufacturing, IT, and construction), they can successfully navigate cyclical downturns [15], [16].

- Pivoting from High-Risk Segments: The traditional government examination and recruitment sector has become increasingly unviable [17]. Escalating issues such as organized cheating, paper leaks, data breaches, and massive litigation exposures have forced legacy companies to pivot away from these services into private training, architecture, and other specialized tech sectors [17].

3. Facility Management & Security Services

- Compliance as a Tailwind: Facility management companies provide integrated solutions including cleaning, catering, security, and asset management [18], [19]. A major driver for formalized, nationally-scaled players in this space is the introduction of stringent new labor codes [20], [21]. Because these codes enforce strict compliance, it is becoming exceedingly difficult for clients to work with unorganized, non-compliant vendors, directly increasing the bargaining power of established firms [20], [21].

4. Cash Management & Logistics Services

- Impact of Digitization: While the number of cash pick-up and delivery points continues to rise across the country, the volume of cash throughput per point—especially in Tier 1 and Tier 2 cities—is stagnating due to the widespread adoption of digital payments [22], [23].

- Pricing Pressures: The industry faces notable pricing pressures from clients, particularly banks seeking competitive quotes for low-volume retail points where fixed-price contracts become too expensive [24], [25], [26], [27].

- Diversification Efforts: To counter stagnant core revenues, cash management firms are utilizing their existing secure vault and transport infrastructure to diversify into new high-value logistics segments, such as transporting diamonds, bullion, and organized gold jewellery [28], [29], [30], [31].

5. Mineral & Energy Exploration

- Entering a Supercycle: The global mineral and energy exploration industry is entering a supercycle fueled by the clean energy transition, decarbonization, and the urgent race to secure critical raw materials like copper, lithium, and rare earths [32].

- Technological and Regulatory Drivers: A global policy shift toward resource nationalism, combined with strict ESG (Environmental, Social, and Governance) due diligence standards, is driving the need for highly structured, scientific exploration [33]. Companies rely on advanced techniques like 2D/3D seismic mapping to locate resources and precise aquifer mapping to evaluate groundwater for infrastructure [34], [35].

6. Heavy-Lift & Crane Infrastructure

- Demand Centers: Heavy lifting and crane rental services are experiencing significant demand from core nation-building sectors, including upstream oil & gas, wind energy installations, and urban infrastructure [36], [37], [38], [39].

- Strategic Transformation: To mitigate the margin dilution and debt-servicing stress historically associated with asset-heavy models, these companies are shifting toward hybrid capital models, deploying asset-light operations where possible, and replacing traditional promoter-driven leadership with professional CXO management [40], [41].

What are the tailwinds affecting this industry?

asof: 2026-04-15

The sources provided cover several different sectors. Here are the key tailwinds affecting these various industries:

Staffing, Facility Management, and Workforce Solutions * Implementation of New Labour Codes: The upcoming Labour Codes are expected to drive greater formalization, consolidation, and stronger governance within the sector [1, 2]. Because the new codes introduce stringent compliance requirements, it will become increasingly difficult for companies to work with non-compliant, unorganized vendors [3, 4]. This creates a significant structural tailwind for large, organized players who already operate in a highly compliant, safety-first environment [3-6]. * Rise of Contract Work: There is an increasing trend of top talent taking up freelancing or contract-based roles, which boosts the need for staffing firms to facilitate the relationship between these workers and clients [7].

Flexible Workspaces and Commercial Real Estate * Expansion of Global Capability Centers (GCCs): The rapid expansion of GCCs in India is a powerful structural demand driver [8, 9]. Global enterprises are scaling their presence to leverage India’s deep talent pool and cost advantages, with GCCs expected to account for roughly 40% of total office absorption by 2026 [8, 9]. This boom in GCCs is also a major driver for the professional staffing industry [10, 11]. * Shift Toward Workspace Flexibility: There is a structural shift in occupier preferences toward speed-to-market, capital efficiency, scalability, and reduced operational complexity [12-14]. Flexible and managed office solutions have transitioned from being temporary arrangements to a core component of corporate real estate strategies [12-14]. * Favorable Government Policies: Measures announced in the Union Budget 2026 have improved long-term tax certainty for multinational corporations [15, 16]. The introduction of a long-term tax holiday for foreign companies delivering global digital and cloud services from India, alongside clearer transfer pricing norms, has strengthened India’s attractiveness as a global operating base [15-18].

Infrastructure, Renewables, and Heavy Engineering * Clean Energy Transition and Supercycle: The global mineral and energy exploration industry is entering a supercycle, driven by the rapid transition to clean energy, reindustrialization, and the race to secure critical raw materials like copper, lithium, and rare earths [19]. * Surge in Capital Expenditure (Capex): There is a massive capex surge in renewables and infrastructure buildouts across India and global markets [20, 21]. The total installed capacity for power generation is expected to more than double by 2029-30 [22], and India will need an estimated INR 235 trillion (USD 3.36 trillion) of investment in infrastructure over the next decade [23]. * Resource Nationalism and ESG Standards: A global policy shift toward localization and resource nationalism has brought early-stage exploration to the forefront [24]. Furthermore, rising Environmental, Social, and Governance (ESG) standards and due diligence requirements are increasing the demand for structured and scientific exploration services [24].

Diamond and Jewelry Industry * Economic and Demographic Growth: The industry is benefiting from rising disposable incomes in India and an expanding middle-class [25]. * Lab-Grown Diamonds (LGDs): A major trend fueling market expansion is the rapid adoption and worldwide acceptance of Lab-Grown Diamonds, which are favored for their affordability and sustainability [25].

What is the general outlook of this industry?

asof: 2026-04-15

Staffing, Human Resources, and Facility Management The Indian staffing market is currently a $10 billion industry and is growing at a rapid 28% year-on-year, with projections indicating it will become one of the largest global staffing markets by 2030 [1]. A major driver of this expansion is the rise in temporary, contract-based, and freelance work, which is making third-party payroll and staffing firms pivotal in managing modern workforce relationships [1]. Furthermore, upcoming Labour Code changes are anticipated to drive greater formalization, consolidation, and stronger governance within the industry [2, 3]. These regulatory shifts will mandate stricter compliance frameworks for statutory and retiral benefits, making it increasingly difficult for businesses to use non-compliant or unorganized vendors [4-7]. This acts as a structural tailwind for organized, nationally scaled players who can absorb these compliances seamlessly [2-4, 6]. Additionally, there is robust demand from Global Capability Centers (GCCs), which are driving the need for higher-value digital, technology, and consulting talent [8, 9].

Flexible Workspaces and Commercial Real Estate The commercial real estate sector is witnessing a major structural shift toward flexible workspaces, transitioning from being viewed as interim tactical solutions to becoming a core component of enterprise real estate strategies [10, 11]. Occupiers heavily favor these models for their speed-to-market, capital efficiency, regulatory compliance readiness, and scalability [10, 11]. Flexible workspaces currently capture roughly one-sixth of total new office leasing in India and are expected to approach one-fifth in the near term [10, 11]. A massive structural demand driver is the rapid expansion of Global Capability Centers (GCCs), which are projected to account for approximately 40% of total office absorption by 2026 [12, 13]. This demand is broadening beyond large multinationals to include mid-market global firms, unicorns, and emerging new-age sectors [12, 13]. This growth is further reinforced by favorable union budget measures—such as long-term tax holidays for digital/cloud services and clearer transfer pricing norms—that significantly enhance tax certainty and operational predictability for multinational corporations establishing bases in India [14-16].

Renewable Energy (Wind Power) The outlook for the wind energy sector is highly positive, underpinned by the country’s ambitious target to reach 100 gigawatts of wind capacity by 2030 [17, 18]. Industry leaders report robust demand, particularly from the Commercial & Industrial (C&I) sector, with new projects rapidly opening up across states like Rajasthan, Andhra Pradesh, Tamil Nadu, and Madhya Pradesh [19-24]. While the sector previously experienced margin compression after a policy shift that replaced feed-in tariffs with reverse auctions, this shakeup has now created a significant “white space” and market opportunity for stable, well-governed players [25-28]. The segment remains underpenetrated and is supported by direct demand from customers seeking trusted, capable renewable partners [26, 28].

Mineral and Energy Exploration The global mineral and energy exploration industry is entering a supercycle, fueled by the rapid transition to clean energy, global reindustrialization, and the urgent strategic race to secure critical raw materials like copper, cobalt, lithium, and rare earths [29]. The global exploration services industry is projected to cross $20.1 billion by 2032 [29]. Key tailwinds include a global policy shift toward resource nationalism, rising ESG (Environmental, Social, and Governance) due diligence standards that boost the demand for structured scientific exploration, and massive advancements in AI-based geological modeling, seismic imaging, and precision drilling [30]. Domestically, the Indian mineral exploration equipment market is expected to reach $13.45 billion by 2033 [30].

Heavy-Lift, Crane Rental & Infrastructure Services The heavy-lift and crane rental industry is directly benefiting from nationwide and global infrastructure buildouts. The crane rental market is expected to see a baseline 14% industry growth rate, largely driven by a surge in capital expenditure for renewables and massive infrastructure projects both domestically and globally, particularly in the Middle East and Saudi Arabia [31, 32].

Diamond and Jewelry Certification The global diamond and jewelry industry is transforming due to evolving consumer preferences, rising disposable incomes, and an expanding middle class [33]. A defining trend shaping the industry’s future is the rapid worldwide adoption of Lab-Grown Diamonds (LGDs), which are favored for their affordability and sustainability [33]. As LGD manufacturing capacities rise and wholesale prices stabilize, the demand for independent certification services is expanding to ensure authenticity, transparency, and trust [33, 34].

Retail Cash Management and Logistics The retail cash management industry is seeing stable cash volumes alongside an increasing number of physical service points [35, 36]. While there is some pricing pressure from clients on low-volume points, the core business remains robust and generates healthy margins heavily tied to economic stability and volume movements [35-40]. The industry is successfully expanding into lucrative niches, such as business-to-consumer home delivery models and dedicated secure logistics for the diamond, bullion, and jewelry sectors [41-44].

Large-Scale Examination Services (Negative Outlook) In stark contrast to the growth in other sectors, the traditional large-scale government examination and recruitment industry is facing severe headwinds and becoming less viable. The sector is exposed to escalating risks, including widespread organized cheating, question paper leaks, data breaches, and exceptionally high litigation exposure where even minor lapses lead to severe financial penalties and reputational damage [45]. Furthermore, rising operational and security costs are outpacing margins, while the rapid technological disruption from Artificial Intelligence is drastically reducing the long-term necessity of traditional large-scale testing [45].

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.