SHRINGARMS

Equity Metrics

May 8, 2026

Shringar House of Mangalsutra Limited

Annual Returns

Cumulative Returns and Drawdowns

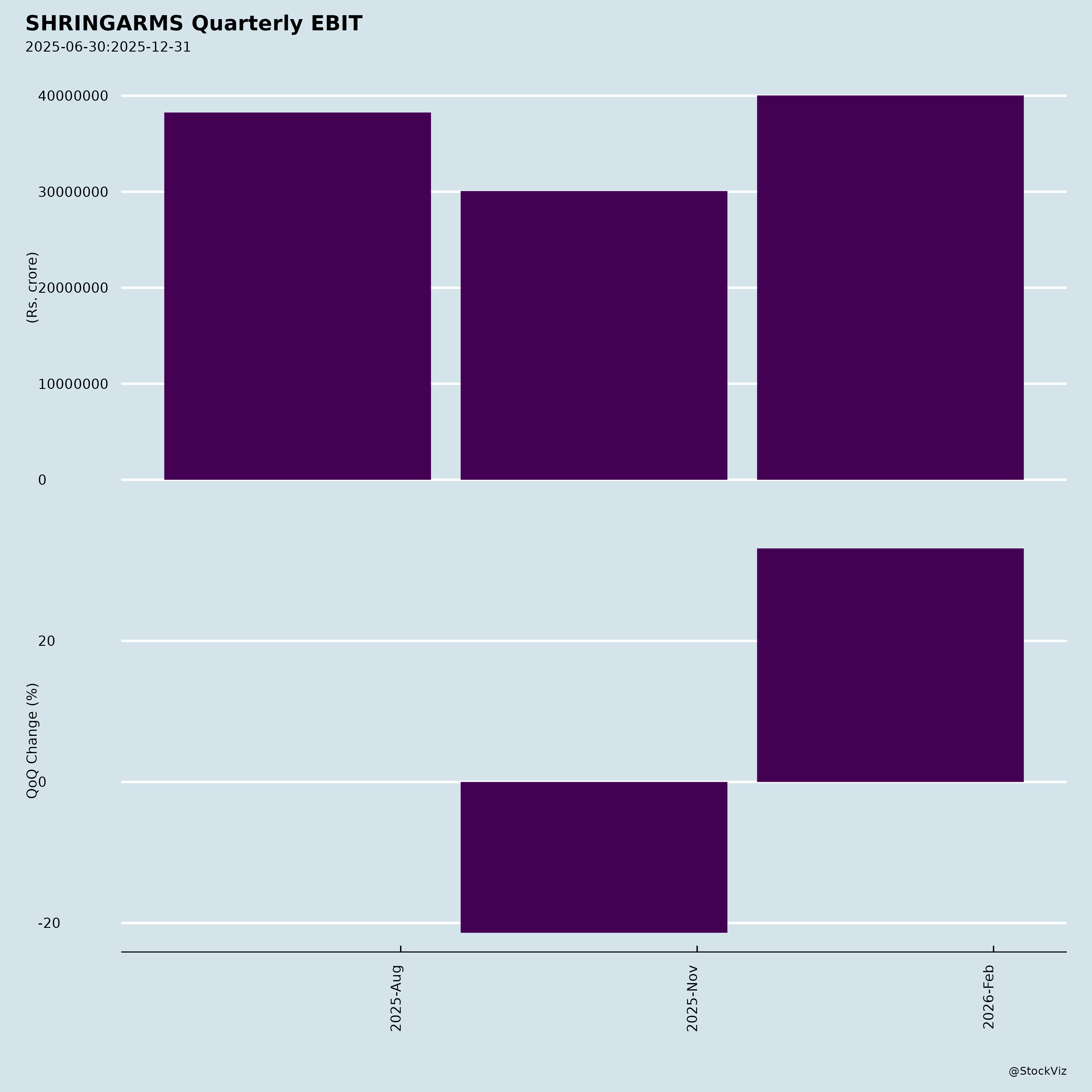

Fundamentals

Ownership

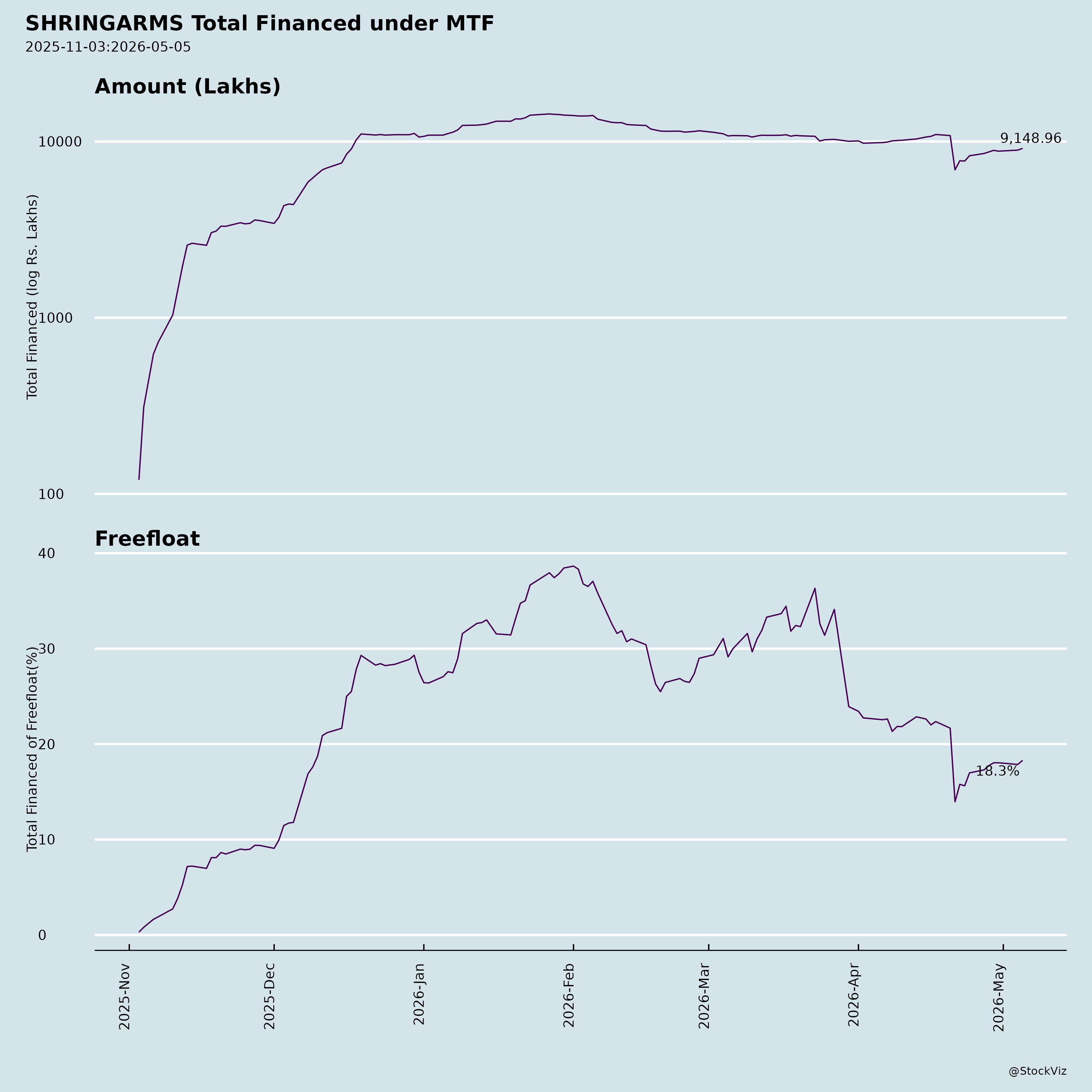

Margined

AI Summary

asof: 2025-12-08

Shringar House of Mangalsutra Limited (SHRINGARMS / BSE: 544512) – Business & Investment Analysis

Company Overview:

Shringar House of Mangalsutra Limited (SHML) is a leading Indian B2B manufacturer and marketer of Mangalsutras, with a 15+ year legacy. It operates in the organized segment of India’s gold jewellery market, specializing in design, manufacturing, and distribution of over 10,000 SKUs across 15+ collections. The company serves marquee corporate clients such as Titan, Malabar Gold, Reliance Retail, and international retailers in UAE, UK, and New Zealand.

It recently became a publicly listed company (IPO in September 2025) and reported its H1 & Q2 FY26 unaudited financial results for the period ended September 30, 2025.

I. Key Tailwinds

1. Strong Financial Performance: Revenue and Profit Growth Acceleration

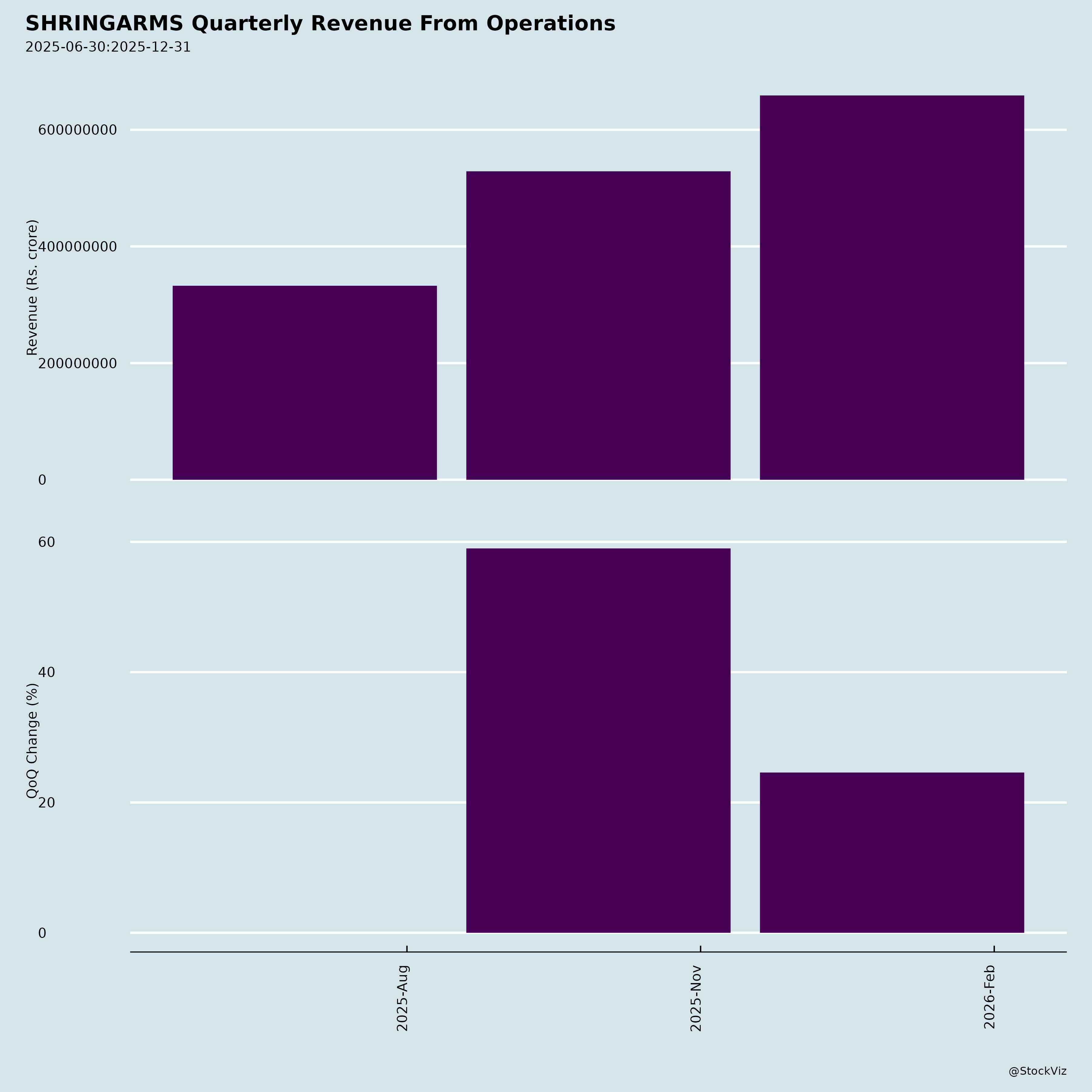

- H1 FY26 Revenue: ₹8,614 million (+25.36% YoY)

- H1 FY26 PAT: ₹513.55 million (+55.46% YoY)

- Q2 FY26 Revenue: ₹5,288 million (+27.09% YoY)

- Q2 FY26 PAT: ₹228.49 million (+42.49% YoY)

- PAT Margin Expansion: from 3.85% (Q2 FY25) to 4.32% (Q2 FY26) — +47 bps

- EBITDA Margin Expansion: 8.63% (H1 FY26) vs 7.24% — +139 bps, indicating operational leverage.

Interpretation: Strong top-line growth driven by volume, product mix shift toward premium items, and operating efficiency. Margin improvement signals scaling benefits.

2. Favorable Industry Trends & Market Position

- Indian Mangalsutra Market CAGR: 5.8% (FY24–FY32) → Expected to reach ₹303 billion.

- Gold dominates market share: 52.3%, with 70% of demand from South & West India.

- SHML is niche-focused: Only Mangalsutras, which are culturally essential and less discretionary → consistent demand.

- Growing demand for hallmarking, which SHML already offers via HUID — aligns with 2021 BIS mandate.

Interpretation: SHML operates in a growing, culturally anchored segment with limited cyclicality in demand.

3. First-Mover Innovation: “24K SHUDDH” Collection

- World’s first HUID hallmarked 24-karat Mangalsutra.

- Made of pure 24K gold, which is rare due to softness; SHML’s technological edge (CNC, 3D printing) enables durability.

- Enhances brand differentiation, margin potential, and B2B appeal.

Interpretation: A signature innovation that elevates brand positioning and enables premium pricing — a key USP.

4. Integrated, Tech-Enabled Manufacturing

- 8,300 sq. ft. facility with 2,500 kg annual capacity — already operating at ~69% utilization.

- In-house: 22 designers, 179 karigars, QC with XRF machines and steel pin detectors.

- Technology: CNC para machines, 3D printing, captive casting, end-to-end control.

- Recognized with “Excellence in Self-Certification Level-1” by Titan — rare B2B credibility.

Interpretation: Scalable, quality-driven model with low dependency on external vendors.

5. Diversified & High-Quality Client Portfolio

- 34 B2B corporate clients including:

- Titan (India’s top brand)

- Malabar Gold, Reliance Retail, Joyalukkas, Damas (UAE), etc.

- Clients have 10–15 year relationships — high stickiness and low churn.

- Geographic reach: 24 states + 4 UTs, with exports to UAE, UK, New Zealand, Fiji, USA.

Interpretation: Low client concentration risk, strong relationships, proven scalability.

6. Post-IPO Strategic Expansion Momentum

- Branches opened in Delhi & Pune — expanding supply chain reach.

- IPO proceeds used for working capital, capex, and brand building.

- Focus on reaching underserved markets through third-party partnerships.

Interpretation: Capital structure unlocked for growth; execution clarity post-listing.

II. Key Headwinds & Risks

1. Gold Price Volatility (Major Commodity Risk)

- Cost of raw material = 70–80% of revenue.

- SHML recently purchased 100 kg of gold at ₹11,000/gm, while average inventory cost was ₹8,900/gm — implies mark-to-market inventory risk.

- Operating model does not hedge gold prices → exposure to price swings.

- Although pricing is cost-plus, sudden drops in gold prices can lead to inventory devaluation and margin compression.

Risk: High commodity price sensitivity — major threat to margins and cash flows.

2. Working Capital Intensity

- High inventory & receivables:

- Inventories: ₹3,444 crore (H1 FY26) — 40.6% of total assets.

- Trade Receivables: ₹2,268 crore — up from ₹878 crore (FY25).

- Indicates long cycles, credit dependence on clients, and inventory build-up risk.

Risk: Heavy cash lock-in, liquidity strain, and dependence on borrowings (₹1,818 crore current borrowings).

3. Limited Geographic Diversification in Sales

- While present in 24 states, >70% of Mangalsutra demand is in South and West India.

- Export sales are growing, but still <2% of total volume (H1 FY26) — international market largely underpenetrated.

Risk: Over-reliance on regional demand trends; international expansion lags.

4. Relatively Low Scale vs Market Leaders

- FY25 Revenue: ₹14,300 million — ~$172 million.

- Titan/Tanishq’s FY25 jewellery revenue: ~$3.5 billion.

- SHML’s share in organized gold jewellery wholesale (~19%): still single-digit % — competitive pressure from larger players.

Risk: Faces intense competition and limited pricing power in commoditized SKUs.

5. Dependence on Few Key Clients

- While client relationships are long-standing, Malabar, Titan, Reliance Retail, GRT likely represent major revenue shares.

- No client-wise revenue disclosure — makes revenue concentration risk unclear.

- Loss of any key client could impact earnings materially.

Risk: Hidden concentration risk in B2B model with large customers.

6. IPO Proceeds Utilization & Execution Risk

- As of Sep 2025, ₹2,113 million (over 70%) of IPO proceeds still unutilized.

- Working Capital: ₹784 million used of ₹700 million proposed → overspent

- General Corporate: ₹341 million used of ₹420 million proposed → underspent

- Requires effective capital allocation and disciplined expansion.

Risk: Risk of misallocation, inefficiency, or slow rollout.

III. Growth Prospects

1. Pan-India Supply Chain Expansion

- Targets untapped markets through third-party distribution partnerships.

- New offices in Delhi & Pune are early steps in North & West India presence.

Potential for revenue diversification and volume scale-up.

3. Technology & Manufacturing Scale-Up

- Plans to increase manufacturing capacity further.

- Can automate more to reduce labor dependency and boost margins.

- Backward integration (gold alloying, casting) already in place — scope for further cost control.

Scalability and margin enhancement upside.

4. Export Market Penetration

- Already exports to UAE, UK, NZ, Fiji, USA.

- Indian diaspora (especially in US, Canada, Middle East) offers long-term export potential.

- Can build brand recognition internationally.

High-margin export revenue opportunity underutilized.

5. Brand Building & Trade Show Participation

- Strategy to showcase designs in national and regional B2B exhibitions.

- Focus on marketing & client engagement post-IPO.

Enhances product visibility, new client acquisition.

IV. Summary: Investment Thesis for SHRINGARMS

| Factor | Assessment | Implication |

|---|---|---|

| ✅ Tailwinds | ||

| 1. Strong financial growth | Revenue & PAT growing >25%, with margin expansion | Accelerating profitability |

| 2. Niche, essential product | Mangalsutra demand culturally stable | Low demand cyclicality |

| 3. Innovation leadership | “24K SHUDDH” — first-mover edge | Brand differentiation, higher margins |

| 4. Integrated manufacturing | Control over design-to-delivery | Scale, quality, efficiency |

| 5. Client stickiness | 10–15 years with key partners | Low churn, recurring revenue |

| 6. Post-IPO momentum | Expansion, transparency, capital | Improved governance & growth |

| ⚠️ Headwinds / Risks | ||

| 1. Gold price volatility | No evident hedging | Inventory, margin risk |

| 2. Working capital intensity | High inventory & receivables | Liquidity pressure |

| 3. Client concentration (risk) | No revenue breakdown | Hidden risk |

| 4. Scale limitations | Small vs market leaders | Competitive pressure |

| 5. IPO fund rollout | 70% funds unutilized | Execution risk |

| 6. Regional demand focus | South & West centric | Geographic imbalance |

| 🚀 Growth Drivers | ||

| - Pan-India expansion | Delhi & Pune offices | Volume scale |

| - Premium products | 24K SHUDDH, diamonds | Margin boost |

| - Exports | Diaspora markets | Long-term upside |

| - Brand building | Trade fairs, campaigns | B2B trust & pipeline |

Overall Assessment: Buy with Caution – High Growth, High Sensitivity

✅ Pros:

- Strong execution capabilities and healthy profitability trajectory.

- Unique product innovation in a structurally growing market.

- Solid B2B moat with Tier-1 clients and integrated manufacturing.

⚠️ Caveats:

- Must monitor gold price trends, inventory turnover, and receivables collection.

- IPO fund deployment and expansion execution will be critical upcoming quarters.

- Not a pure hedge against inflation — due to margin risks.

Final Verdict:

SHRINGARMS is a high-growth, niche B2B player in the organized gold jewellery space with innovation, quality, and client trust driving margins. While prone to gold volatility and working capital stress, its growth strategies are sound, and post-IPO investment cycle could unlock meaningful scale.

Recommended for: Growth-focused investors who understand commodity-linked manufacturing cycles and seek exposure to India’s organized jewellery transformation.

Monitor closely: Inventory management, fund utilization, gold prices, and H2 FY26 trends.

Analyst Notes Keywords:

#NichePlayer #B2BJewellery #GoldPriceSensitive #IPOPlay #MarginExpansion #InnovationLead #PanIndiaExpansion #HUIDHallmarking

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.