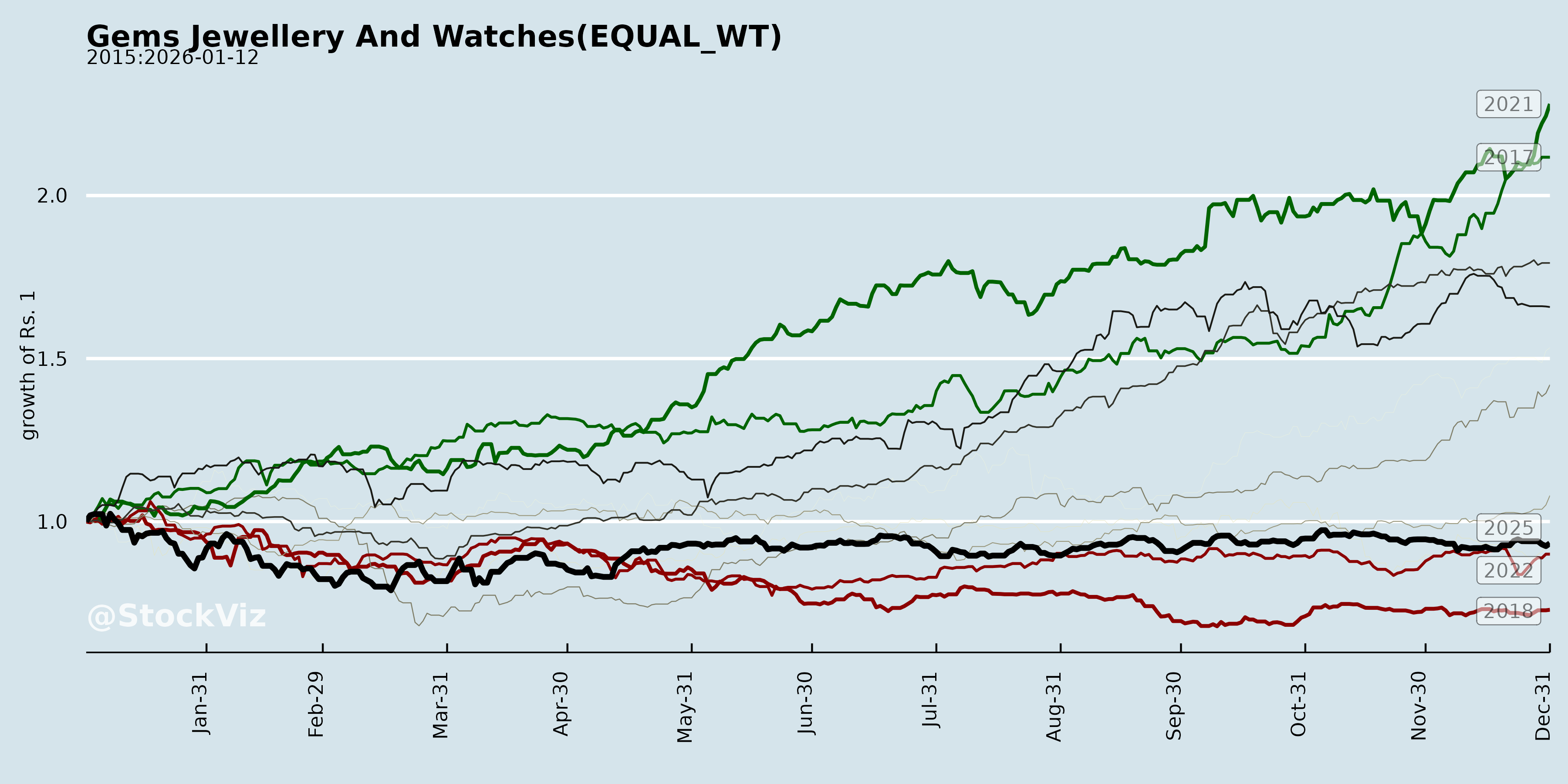

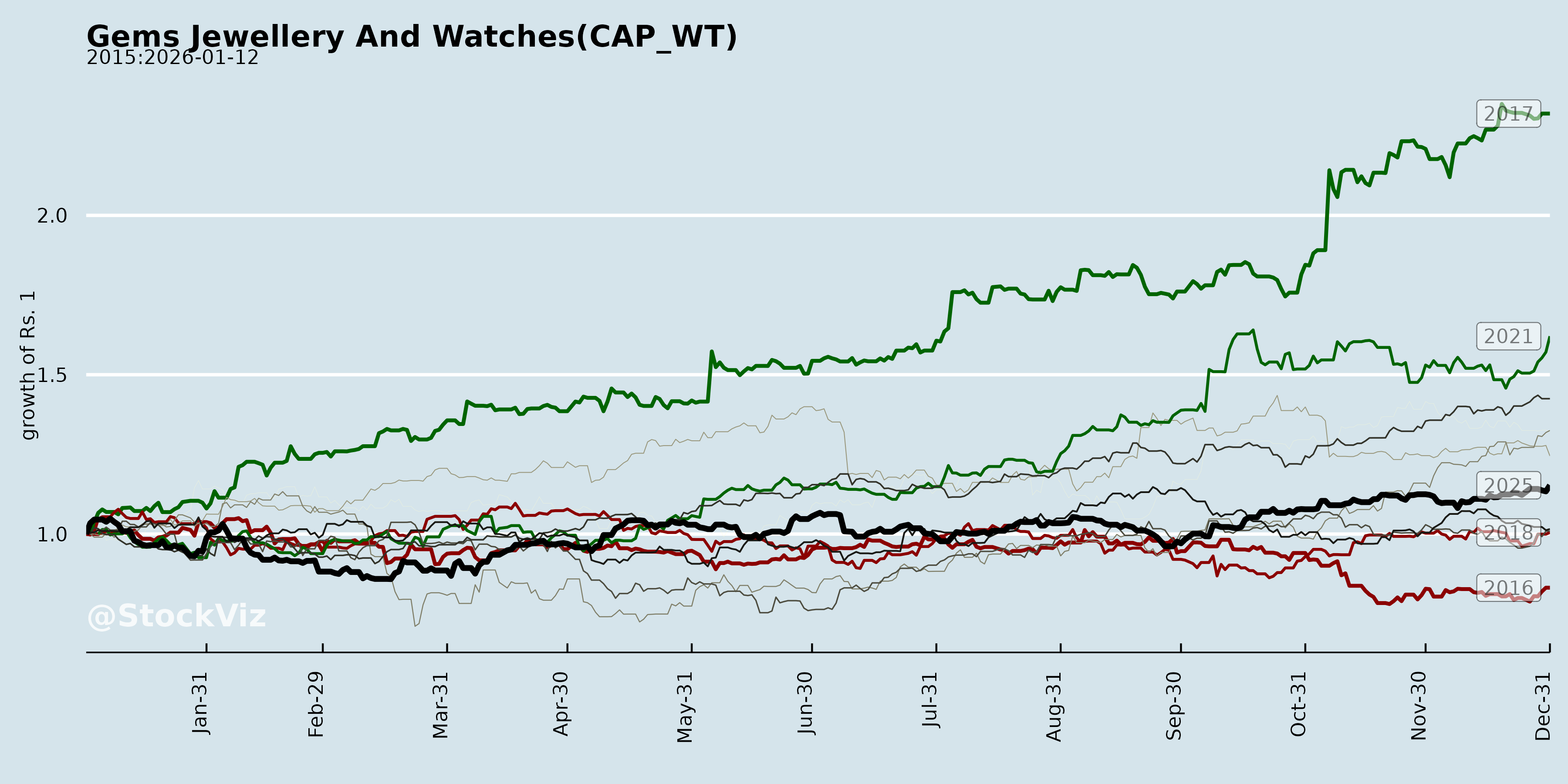

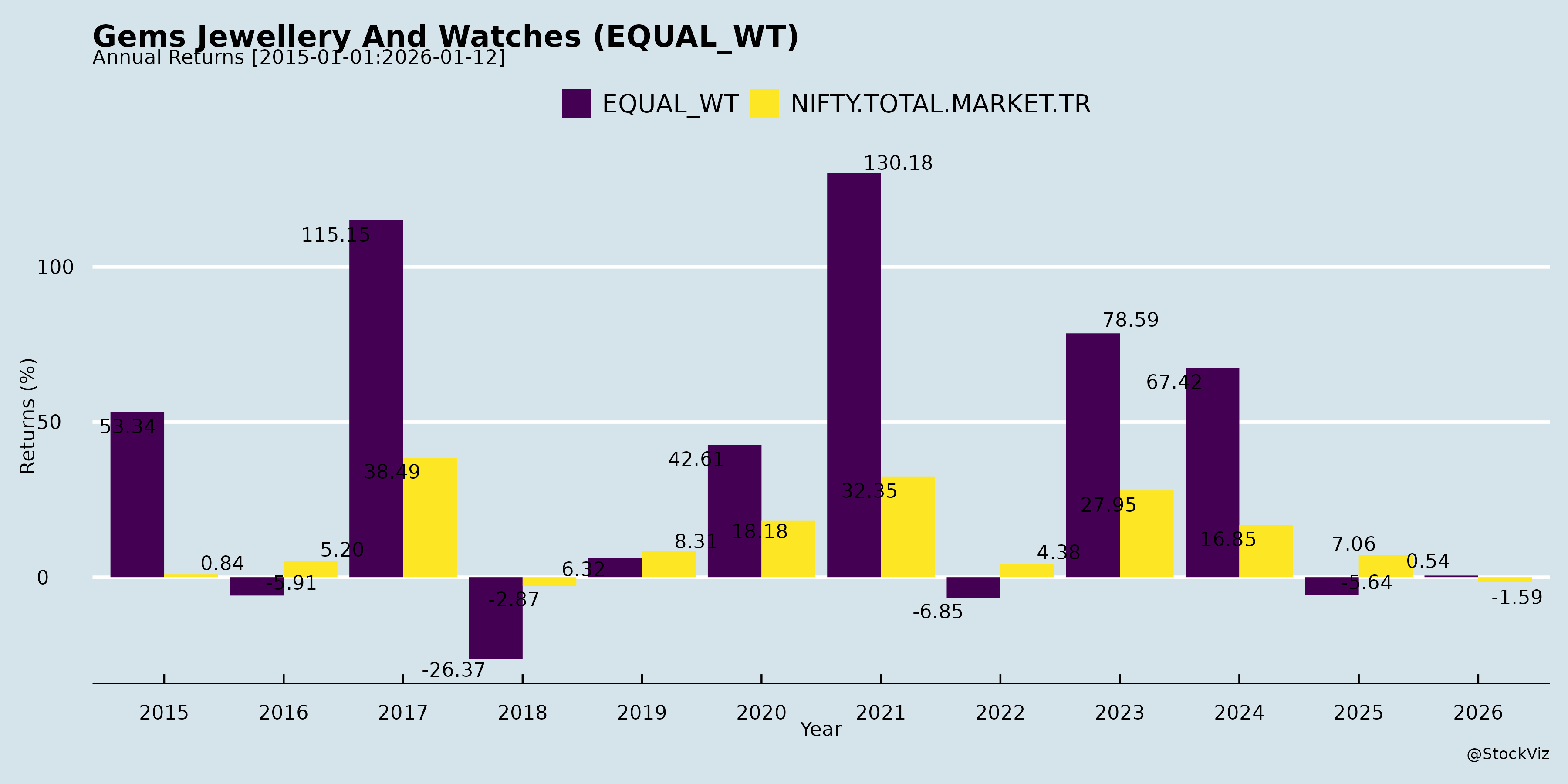

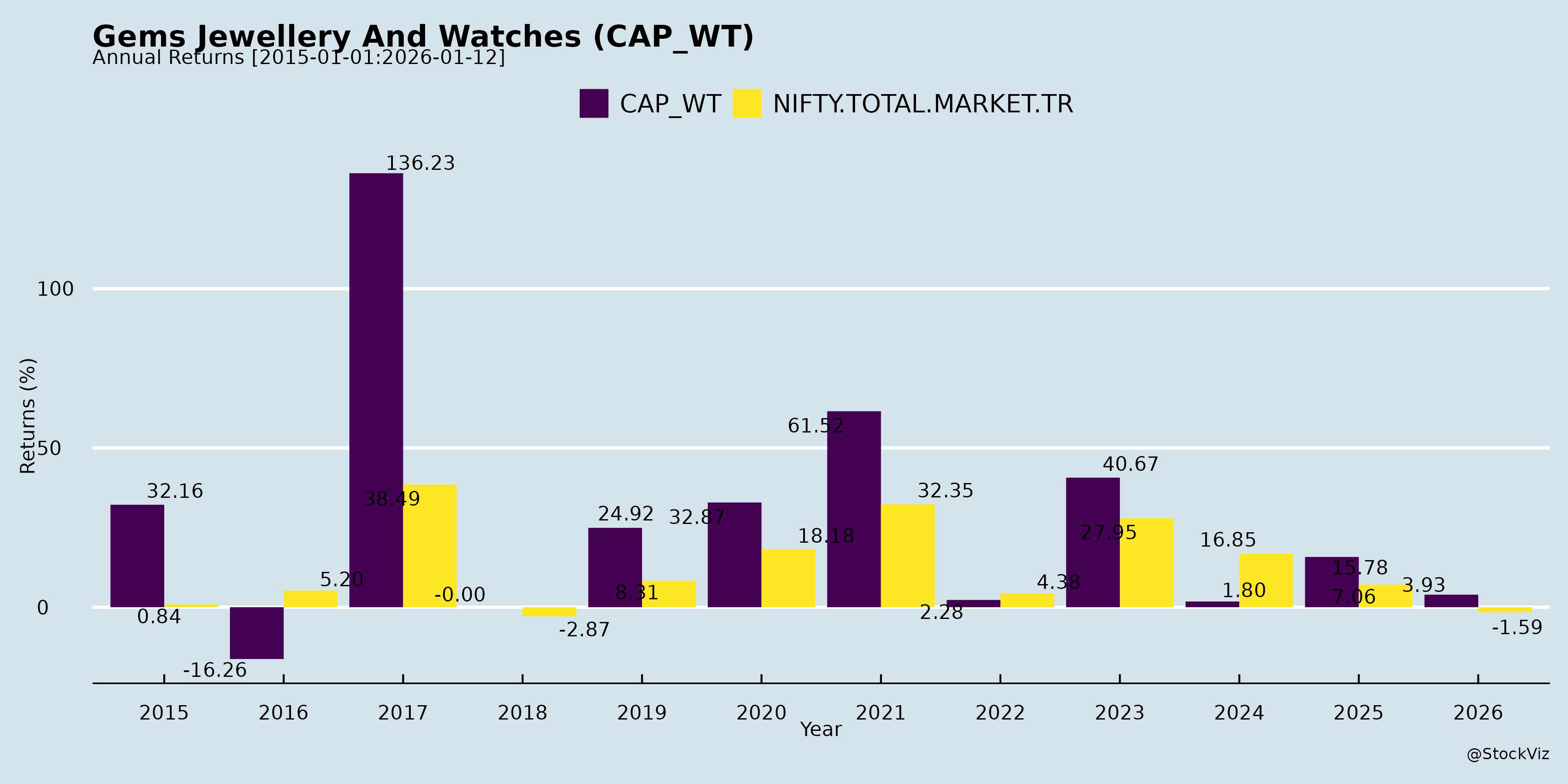

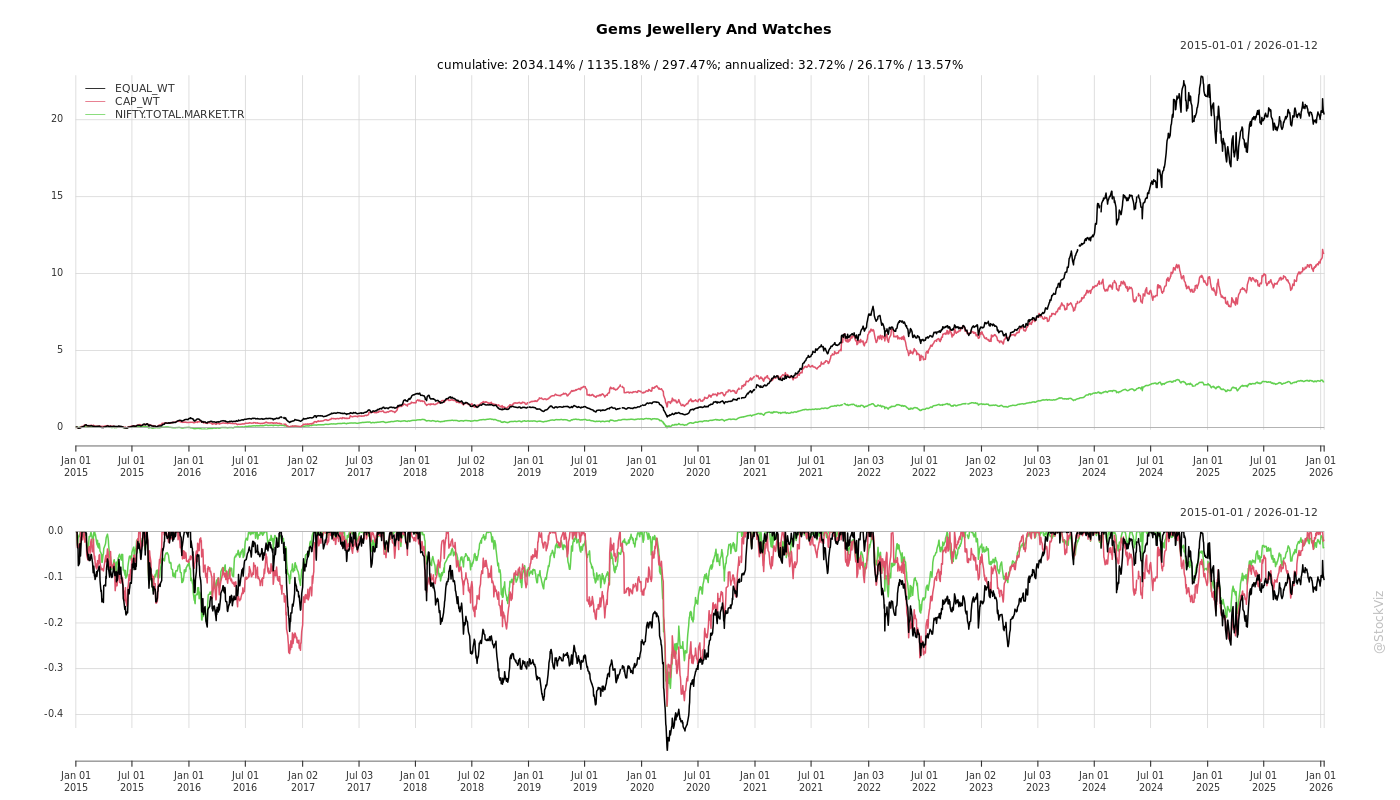

Gems Jewellery And Watches

Industry Metrics

May 8, 2026

Annual Returns

Cumulative Returns and Drawdowns

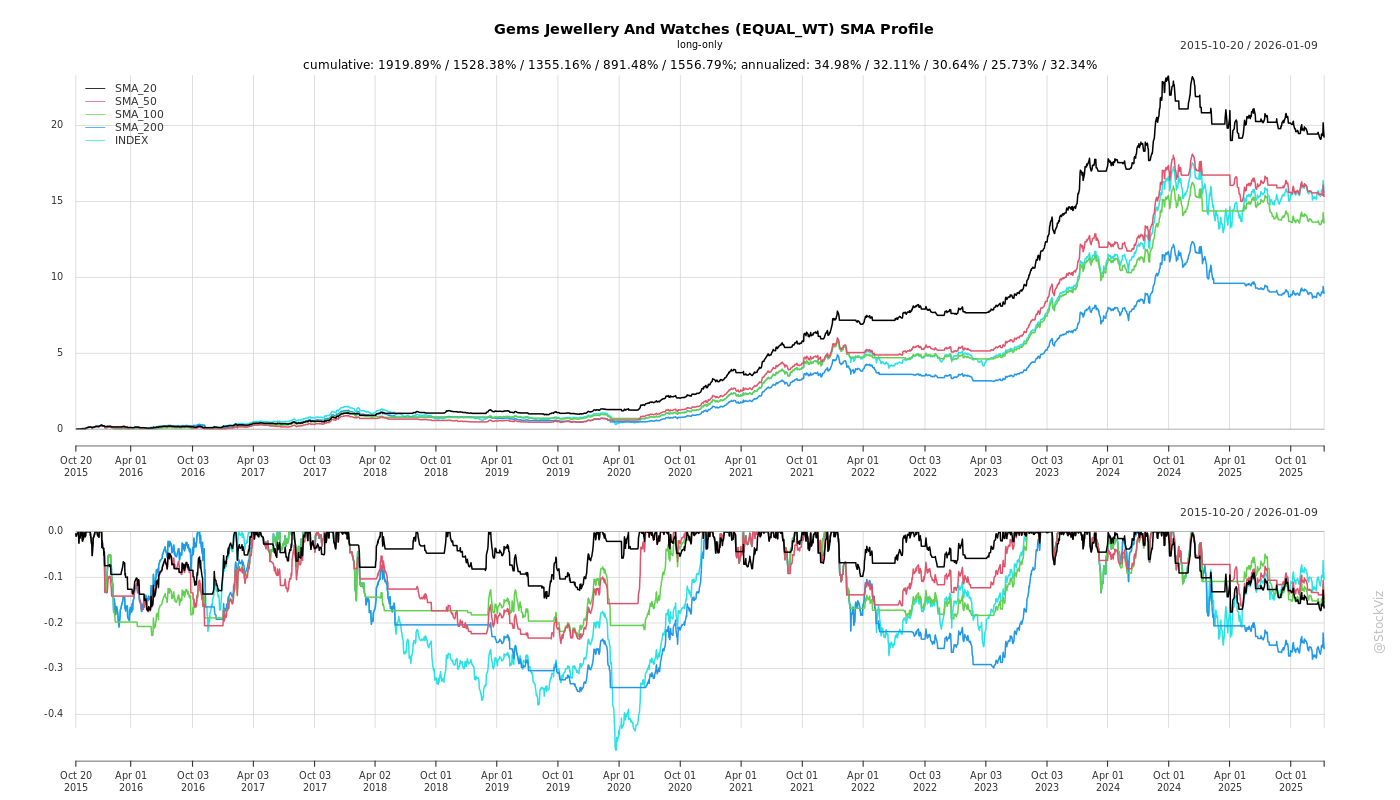

SMA Scenarios

Current Distance from SMA

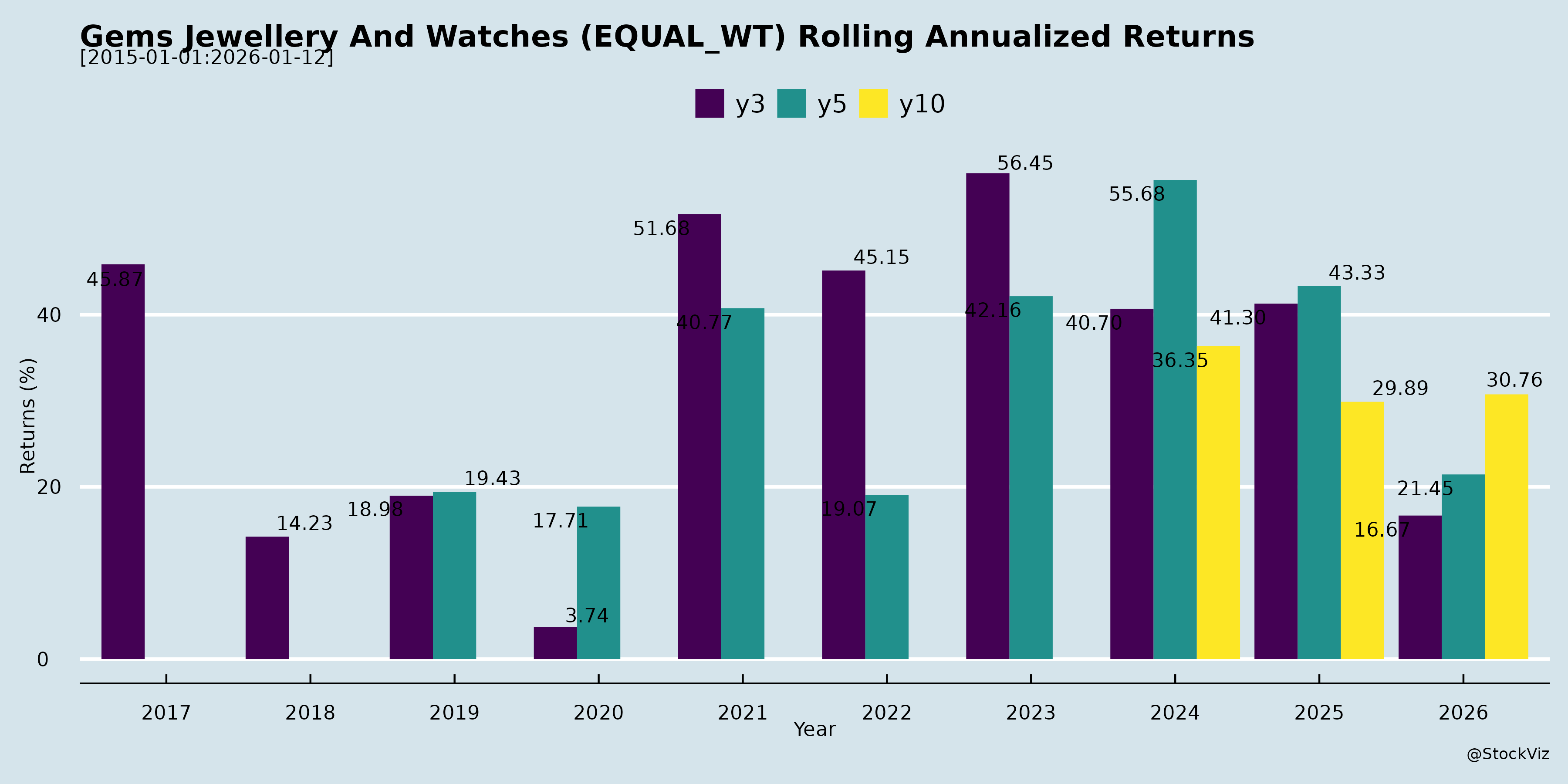

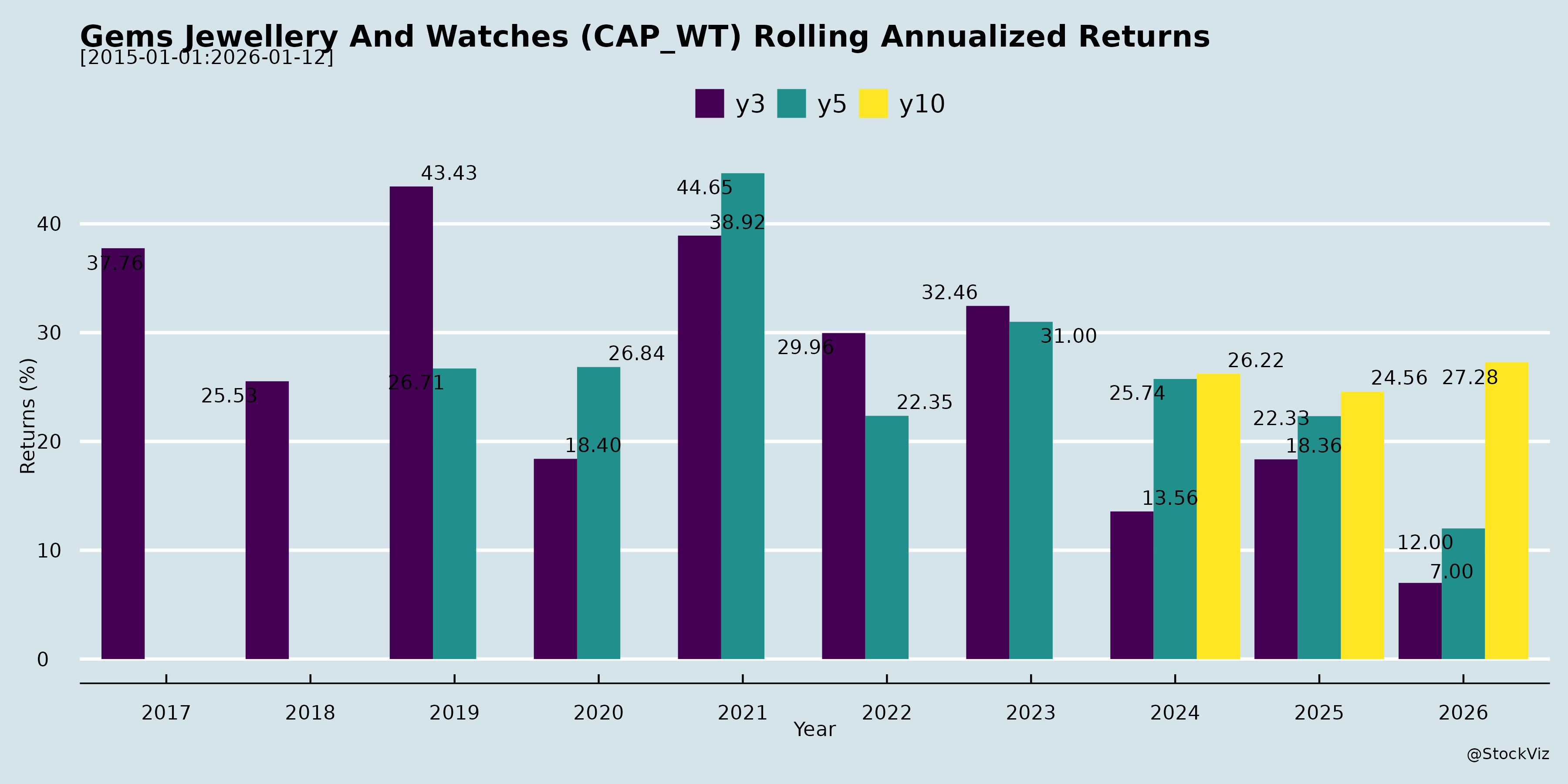

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-16

The challenges and opportunities within the jewelry industry have evolved significantly over time, transitioning from standard operational hurdles to complex macroeconomic and technological shifts. As the market has modernized, companies have had to adapt to extreme price volatility, changing consumer demographics, and the rise of new product categories like lab-grown diamonds.

The Evolution of Challenges

- Extreme Gold Price Volatility and Liquidity Pressures: Historically, gold price fluctuations were manageable, but recently, prices have surged dramatically (e.g., up 65% to 79% year-over-year, reaching peaks of USD 5595/Oz or over Rs. 1.5 Lakhs) [1-5]. This unprecedented rise has caused a decline in general walk-ins and window shoppers, as consumer budgets have not increased at the same pace as gold prices [1, 3, 6, 7]. Furthermore, this volatility created severe liquidity pressures for jewelers, who faced unpredictable mark-to-market margin calls on their hedges [8, 9].

- Lab-Grown Diamond (LGD) Pricing Dynamics: In the past, the price of manufacturing lab-grown diamonds fell continuously due to rapid increases in machine capacity and the ubiquity of growing technology [10, 11]. Today, this challenge has stabilized; prices have reached a base and even increased in certain sizes, as the primary cost is now tied to the true labor required to cut and polish the diamond rather than the technological growing process [12, 13].

- Navigating Tariffs and Competition: The industry has had to evolve its supply chain to navigate global trade tariffs. For instance, to combat import duties in the US, companies adopted “dual casting” methods—casting the jewelry in the US and finishing it in India—which successfully evolved into a 0% tariff advantage [14-17]. Meanwhile, domestic competition has intensified with major corporate giants launching their own LGD and traditional jewelry brands, forcing existing players to fiercely defend their market share through competitive pricing and design [18-20].

- Regulatory and Labor Compliance: The Government of India’s consolidation of multiple labor legislations into the “New Labour Codes” has presented an evolving administrative challenge, resulting in one-time financial impacts and increased provisions for employee benefits [21-24].

The Evolution of Opportunities

- The Strategic Pivot to Lightweight and Lower-Caratage Jewelry: As high gold prices squeezed consumer budgets, the greatest evolving opportunity has been the mass introduction of 18-karat, 14-karat, and even 9-karat lightweight jewelry [1, 3, 25-29]. This shift allows consumers to buy more items within a fixed budget [30, 31]. Counterintuitively, this trend is highly profitable for jewelers, as lightweight and highly designed lower-carat pieces carry higher effective making charges and yield stable or improved profit margins compared to traditional heavy 22-carat gold [30, 32-36].

- Surge in Silver and Diamond/Studded Categories: To offset gold price shocks, companies have aggressively expanded their silver and diamond portfolios. Silver jewelry, which boasts workmanship indistinguishable from gold, has seen surging demand and commands significantly higher gross margins of 25% to 30% [37-42]. Similarly, the diamond-studded segment continues to grow rapidly in value, acting as a key focus area for brand premiumization [43-45].

- The Boom in Old Gold Exchange: A few years ago, old gold exchanges accounted for about 25% to 30% of business; today, this has evolved to 45% to 50% [46, 47]. Because consumers lack the liquid cash to afford new gold at peak prices, recycling old household gold has become a vital strategy to drive sales volumes and customer upgrades [48-50].

- Lab-Grown Diamonds as a Dominant Mainstream Category: What started as a niche alternative has evolved into a global phenomenon. LGDs have actively eaten away market share from natural diamonds, and consumer demand has exploded across the US, Middle East, Australia, and India [51-54]. Brands are now scaling B2C retail store networks to offer “full-stack” LGD solutions, ranging from entry-level fashion pieces to flawless high-end bridal rings [55-58].

- Technological Integration and Omnichannel Retailing: The industry has evolved from traditional brick-and-mortar sales to embracing cutting-edge retail technology. Companies are capitalizing on AI-based software for real-time inventory monitoring, digital ring builders, Augmented Reality (AR) in-store scanners, and AI tools like “Shape of You” that recommend jewelry based on a customer’s face shape [59-65].

- Market Consolidation and Demographic Tailwinds: Increased government regulations regarding hallmarking and traceability are structurally forcing the market to shift from unorganized local jewelers to organized, compliant corporate brands [66-69]. Furthermore, India’s middle class is projected to expand to over 60% of the population by 2047, presenting a massive, long-term opportunity for organized brands to scale through franchisee models into Tier-2 and Tier-3 cities [70-73].

What are the headwinds affecting this industry?

asof: 2026-04-16

High and Volatile Gold Prices The most significant headwind facing the jewelry industry is the extreme elevation and volatility of gold prices. Gold prices have surged drastically, with reports indicating year-over-year increases of 65% to 79%, reaching peak levels that force immense pressure on the market [1-3]. This rapid fluctuation—sometimes seeing daily price variations of 2% to 5% and sudden massive drops after reaching record highs—has created a highly uncertain environment for both jewelers and consumers [3-6].

Declining Consumer Footfalls and Volume Offtake The skyrocketing cost of gold has directly impacted consumer behavior, leading to a noticeable decline in physical retail traffic and purchase volumes. While gold prices increased by 65% to 70%, consumer budgets only increased by roughly 20% to 25% [1, 2]. Consequently, consumers are being priced out of the market, resulting in: * Reduced Footfalls: Showrooms have seen a 10% to 15% decrease in footfalls, as window shoppers and casual buyers sit on the sidelines [7-12]. * Lower Grammage/Volume Sold: Overall gold volume sales have degrown, with some jewelers reporting a 10% drop in volume over a 9-month period [13, 14]. Customers are purchasing strictly for need-based events (like weddings) and avoiding casual or luxury shopping, which brings down the average grammage sold per customer [15-20]. * Delayed Purchases: The sudden price shocks cause psychological barriers, prompting some customers to postpone their investments in hopes that prices will correct [11, 12, 21, 22].

Liquidity Constraints and Reliance on Old Gold Exchange Because retail customers do not have the liquid cash to keep up with the inflated cost of new gold, they are increasingly relying on exchanging their existing jewelry [7, 9]. The proportion of old gold exchange has doubled for some jewelers, surging from historical levels of 25%–30% up to 45%–50% of total sales [23-26]. While this helps keep the industry moving, it highlights a severe liquidity crunch among end consumers [7, 9].

Margin Pressures and the Need for Discounting To counter the shock of high prices and dropping footfalls, jewelers are being forced to offer extra discounts and promotional schemes to tempt buyers back into stores, which directly cuts into their gross margins [11, 12, 27, 28]. Additionally, in the B2B segment, manufacturers are facing psychological pressure from their corporate retail clients who are attempting to squeeze supplier margins to offset their own rising costs [29, 30].

Working Capital and Hedging Challenges The elevated price of gold has dramatically inflated the value of inventory, straining working capital and increasing borrowing requirements for businesses [31-33]. Furthermore, extreme price volatility creates turbulence in hedging activities [4, 6]. Jewelers operating on the sell side face heavy mark-to-market hedge calls during sudden price spikes, which heavily pressures their short-term liquidity [5, 34]. The financial uncertainty caused by these price movements has even forced some jewelers to temporarily defer the opening of planned retail outlets [35, 36].

Shifts in B2B Procurement Dynamics The wholesale jewelry sector is facing headwinds as retailers hesitate to procure and hold wholesale inventory at peak market rates [37]. Fearing that gold prices might suddenly drop, many corporate retailers are shifting away from outright wholesale purchases and instead demanding job-work arrangements [37, 38]. Additionally, B2B retailers are facing significant margin calls on their own hedges, which ties up their liquidity and makes it difficult for them to procure the raw gold needed to give job-work orders to manufacturers [39].

Rising Regulatory and Compliance Costs The industry is also navigating increased operational costs due to regulatory changes. The implementation of new labor codes has resulted in higher statutory staff and labor costs, directly impacting the bottom line [33, 40-43]. Furthermore, the government is planning to introduce much stricter regulations, making hallmarking stronger and implementing rigorous traceability requirements [44, 45]. This incoming wave of compliance will require jewelers to heavily invest in systematic data analysis and technological integration to legally operate and grow [44, 45].

What are the key things to understand about this industry?

asof: 2026-04-16

The impact of surging gold prices and market volatility A defining characteristic of the jewellery industry is its sensitivity to the highly volatile pricing of gold. Over recent periods, gold prices have surged dramatically, rising by approximately 65% to 70% year-over-year and hitting peak levels around USD 5,595 per ounce or over INR 1.5 Lakhs per 10 grams before settling [1-4]. Despite these massive price hikes, consumer budgets have only increased by around 20% to 25%, creating a significant affordability gap [1, 3]. To counter this volatility and maintain liquidity, businesses have had to adjust their risk management strategies, such as maintaining hedging ratios at a prudent 55% to 60%, down from historical levels of 80% to 90% [5-8].

The surge in “Old Gold” exchange Because consumers lack the liquid cash to keep up with skyrocketing gold prices, the recycling and exchange of old gold has become a critical industry driver [9, 10]. Historically, old gold exchange accounted for 25% to 30% of sales, but it has now surged to 45% to 50% [5-8]. This strategy not only aids consumers in upgrading their jewellery without feeling the pinch of high prices, but it also helps the industry sustain sales volumes and manage inventory in a volatile market [9-11].

A strategic pivot toward lightweight and lower-caratage jewellery To fit into the constrained budgets of consumers, jewellers are aggressively pushing lightweight products and lower-purity gold [12-14]. There is a clear industry shift from traditional 22-carat heavy jewellery toward 18-carat, 14-carat, and even 9-carat gold collections [15-19]. Because lightweight pieces are more affordable, customers tend to purchase a higher number of items within the same budget, allowing retailers to maintain overall bill values while slightly improving profit margins due to the refined manufacturing processes required for lighter pieces [20-22]. However, the acceptance of lower caratage varies by region; for instance, North Indian markets are adopting 18-carat jewellery much faster than South Indian markets, which traditionally favor 22-carat gold [23, 24].

Premiumization through diamonds and silver To protect and structurally improve gross margins, the industry is increasingly focusing on value-added categories like diamonds, studded jewellery, and silver [25-28]. Silver jewellery is experiencing strong demand and offers significantly higher profit margins—around 25% to 30% compared to just 12% to 13% for plain gold [29, 30]. Similarly, diamond and studded jewellery attract higher making charges and have seen robust value growth, making them a pivotal factor in driving retail profitability [26, 28, 31, 32].

The rise of Lab-Grown Diamonds (LGDs) Lab-grown diamonds are rapidly capturing market share from natural diamonds, particularly in export markets like the United States, which has aggressively adopted them [33-36]. Historically, the prices of LGDs fell continuously due to increasing manufacturing capacity and ubiquitous technology, but LGD prices have now stabilized because the true labor costs to cut and polish the stones represent a firm price floor [37-40]. The entrance of major traditional retailers, such as Titan with its “beYon” brand, into the LGD space is expected to boost customer education, build trust, and significantly increase the overall market size for this category [41-45]. Furthermore, specific trade structures—such as casting LGD jewellery in the US while finishing it in India—allow companies to navigate international tariffs effectively, securing 0% import duties for “Made in America” labelled products [46-49].

Shift from unorganized to organized retail The Indian jewellery market is undergoing a structural shift from the unorganized sector (local mom-and-pop shops) toward organized corporate retail [50, 51]. Organized players accounted for 35% to 40% of the market in FY24, and this share is expected to rise to 45% to 50% by FY30 [52]. This transition is heavily driven by increasing regulatory pressures (such as mandatory hallmarking and traceability), a growing demand for brand assurance, and the expansion of the middle class [52-55]. Organized brands also benefit from a multigenerational clientele, where trust and legacy lead to steady, repeat business [56].

Innovative business models: Job work and Franchising On the operational side, jewellers utilize specific business models to optimize capital. “Job work” is a highly lucrative B2B segment where large national retailers provide the raw gold, and the manufacturer simply charges for the design and processing [57, 58]. Because the manufacturer does not have to invest in the raw material, this segment boasts high gross margins and protects them from gold price volatility [57, 59]. Additionally, retail expansion is increasingly achieved through asset-efficient, franchise-led routes (FOFO/FOCO models), which allow brands to penetrate Tier-2 and Tier-3 markets without heavy capital expenditure [4, 60, 61].

Data, AI, and Hyperlocal Strategies The industry relies heavily on a “hyperlocal” strategy, customizing designs to match specific regional tastes across India’s diverse demographics [14, 62-64]. To manage this complex inventory, companies are adopting advanced technologies, including AI-based software for real-time inventory monitoring to keep inventory days range-bound [63, 65]. Customer experience is also being digitized, with innovations like the AI-based “Shape of You” tool, which recommends jewellery based on a customer’s face shape, and augmented reality (AR) scanners [66-68].

The anchor of weddings and festivals Finally, despite any economic headwinds, the industry is fundamentally sustained by “compulsion buying” for weddings and traditional festivals [69]. Wedding-related purchases are largely need-based and account for a massive portion of revenue—often up to 60% or 65% of a jeweller’s sales—ensuring robust, cyclical demand during auspicious periods like Dhanteras, Akshaya Tritiya, and the broader wedding seasons [69-71].

What are the tailwinds affecting this industry?

asof: 2026-04-16

A structural shift from the unorganized to the organized sector is one of the most prominent tailwinds in the jewellery industry. The market share of organized players is projected to rise from 35%–40% in FY24 to 45%–50% by FY30 [1]. This transition is being accelerated by a strong regulatory push from the government—such as stricter hallmarking rules and a focus on traceability—which forces systemic compliance and data analysis [1-3]. Furthermore, consumers are increasingly gravitating toward organized brands that offer brand assurance, standardization, access to financing, and transparent exchange offers [1]. Even unorganized manufacturing players are increasingly shifting to the organized sector to take advantage of formal systems like Gold Metal Loans (GML) [4].

Favorable demographic shifts and rising disposable incomes are significantly expanding the consumer base. India’s middle class is projected to double from approximately 30% of the population in 2021 to over 60% by 2047 [5]. This surge in purchasing power translates to higher disposable incomes directed toward luxury items and high-quality, branded jewellery [5]. Accompanying this is a robust growth trajectory in Tier 2, Tier 3, and Tier 4 markets, presenting vast opportunities for geographic expansion [6-9].

Deep-rooted cultural significance and occasion-based demand provide a constant, reliable baseline for sales. Gold is deeply integral to Indian culture and ceremonies, symbolizing wealth and prosperity [5]. Because of this, wedding-related purchases are considered “need-based” and remain steady, continually supporting overall market demand regardless of broader economic fluctuations [10, 11]. Additionally, festive and auspicious occasions—such as Dhanteras, Diwali, Akshaya Tritiya, and Navratri—generate massive, concentrated spikes in consumer purchasing [12-18].

Evolving consumer adaptations to high gold prices have created new, highly profitable avenues for jewellers. Rather than being discouraged by soaring gold prices, consumer faith in gold as an investment has actually strengthened, bringing new buyers into the market [10, 11, 19-22]. To adapt to budget constraints, the industry is benefiting from several consumer shifts: * Embrace of Lower Caratage and Lightweight Jewellery: Consumers are widely accepting 18-carat, 14-carat, and even 9-carat gold, allowing them to purchase beautiful, lightweight designs without exceeding their budgets [19, 20, 23-30]. This is highly advantageous for jewellers, as lightweight and lower-carat products often carry much higher, more profitable making charges [31-34]. * Surge in Old Gold Exchange: Because consumers lack the liquid cash to buy expensive gold outright, they are increasingly utilizing old gold exchange programs. For some jewellers, old gold exchange has jumped from a historical average of 25%–30% up to 45%–50% of revenue, keeping the industry moving and ensuring customers can still upgrade their jewellery [23, 25, 35-38]. * Silver as an Alternative: Silver is emerging as an increasingly important and high-margin category. Due to elevated gold prices, silver is viewed as a relatively affordable alternative, driving both strong investment demand and fashion purchases [21, 22, 39].

The rapid expansion of the Lab-Grown Diamond (LGD) market is unlocking an entirely new consumer segment. Global demand for lab-grown diamonds has increased dramatically across the US, the Middle East, Australia, and India [40, 41]. The category is receiving a massive credibility boost as marquee, renowned retail brands enter the LGD space, which is expected to significantly increase the overall consumption pie [42-47]. Furthermore, the historical risk of falling LGD prices has stabilized, with prices for certain sizes even trending upward, making it a safer and more lucrative category for retailers to stock [48-51].

Favorable international trade policies are acting as a major catalyst for B2B exporters. Recent trade agreements with the United States have removed import duties on loose gems (bringing them to 0%) and slashed tariffs on imported jewellery from 50% to 18% [52-57]. This has been a massive sentimental booster, improving relations and giving international retailers the confidence to freely place larger orders with Indian manufacturers [58-61].

Increasing digitalization and omnichannel growth are modernizing the purchasing pipeline. The rising penetration of the internet and smartphones is expanding e-commerce, allowing jewellery brands to reach wider audiences and granting consumers easy access to a vast array of designs and digital purchasing options [1, 62].

What is the general outlook of this industry?

asof: 2026-04-16

The overall outlook for the gems and jewellery industry is highly positive, characterized by robust market expansion, a structural shift toward formalization, and evolving consumer preferences in response to macroeconomic factors.

Market Size and Structural Growth The Indian gems and jewellery market is a major economic driver, contributing approximately 7.5% to the nation’s GDP and 14% to its total merchandise exports [1]. The market was valued at $78.50 billion in 2021 and is projected to reach $119.80 billion by 2027, growing at a steady Compound Annual Growth Rate (CAGR) of 8.34% [2]. Over the last decade alone, the market size has increased almost threefold, from INR 30 billion to INR 120 billion [3, 4].

A defining trend in the industry’s outlook is the rapid shift from the unorganized to the organized sector [5, 6]. Organized players accounted for 35%–40% of the retail jewellery market in FY24, and this share is expected to surge to 45%–50% by FY30 [7]. This formalization is being accelerated by regulatory pushes from the government—such as stricter hallmarking and traceability requirements—as well as increasing consumer demand for brand assurance, transparent pricing, and digital/omnichannel retail experiences [7-9]. Furthermore, the rapid growth of the Indian middle class, projected to expand from roughly 30% of the population in 2021 to over 60% by 2047, is expected to drastically increase disposable incomes and spending on luxury branded jewellery [1].

Impact of Gold Prices and Shifting Consumer Behavior The industry is currently navigating an environment of highly volatile and elevated gold prices, which have surged dramatically to levels around USD 4,700 to USD 5,595 per ounce, with long-term projections potentially reaching USD 6,000 to USD 6,500 [10-12]. Despite these steep price hikes, consumer faith in gold as a symbol of wealth, prosperity, and emotional value remains unshaken [1, 13, 14]. However, because consumer budgets have not increased at the same 65%–70% rate as gold prices, buying patterns are significantly changing [15, 16]: * Lightweight and Lower Karatage: To fit into fixed budgets, consumers are shifting heavily towards lightweight, everyday-wear jewellery [17-20]. There is a surging acceptance of lower-purity gold, with retailers actively introducing and promoting 18-carat, 14-carat, and even 9-carat jewellery collections [17, 18, 21-23]. * Surge in Old Gold Exchange: Because liquidity is tight, consumers are increasingly using their existing assets to fund new purchases. The share of old gold exchange has jumped from historical levels of 25%–30% to account for 45%–50% of total revenues for major retailers [24-28]. * Resilience of Wedding Demand: The wedding segment remains a massive, steadfast driver for the industry. Wedding jewellery is considered a “compulsion buy,” meaning customers maintain stable, fixed-budget purchases for these committed events regardless of economic fluctuations [21, 22, 29].

Emerging Product Categories and Trends To sustain growth and improve profit margins, the industry is pivoting toward high-value and high-margin product categories: * Lab-Grown Diamonds (LGD): The demand for lab-grown diamond jewellery is increasing dramatically across the globe, including in the US, the Middle East, Australia, and India [30, 31]. Prices for lab-grown diamonds, which were previously falling due to increased manufacturing capacity, have now stabilized and even trended upwards, removing the risk of inventory price declines [32-35]. The entry of major corporate players into the Indian LGD retail space is expected to expand the overall market size for this nascent category [36-39]. * Silver and Fashion Jewellery: Silver is emerging as a highly popular and affordable alternative to gold, boasting robust investment demand and strong aesthetic appeal [40-43]. Silver jewellery is highly lucrative for businesses, yielding gross margins of 25%–30% compared to the 12%–13% margins seen in gold jewellery [44, 45]. Additionally, younger Gen-Z consumers are driving significant growth in the fashion and costume jewellery segments, seeking stylish, versatile, and affordable pieces [2, 46]. * Diamond and Studded Jewellery: There is strong organic growth in diamond and studded jewellery, fueled by digital marketing, social media campaigns, and younger demographics conducting research before purchasing [47, 48].

Global and Export Opportunities On the international front, the B2B jewellery export outlook is highly bullish. Recent trade deals, such as the implementation of a 0% import duty on loose gems into the United States, have significantly boosted market sentiment and freed up retailer purchasing power [49-54]. Exporters are also successfully diversifying their client bases beyond the US, capturing new growth in Europe, Israel, Australia, and the Middle East [55-58]. The GCC region (including the UAE, Saudi Arabia, Qatar, Oman, Kuwait, and Bahrain) is exhibiting particularly robust economic growth, creating a lucrative market for high-quality, culturally resonant jewellery offerings [59].

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.