SANDESH

Equity Metrics

May 8, 2026

The Sandesh Limited

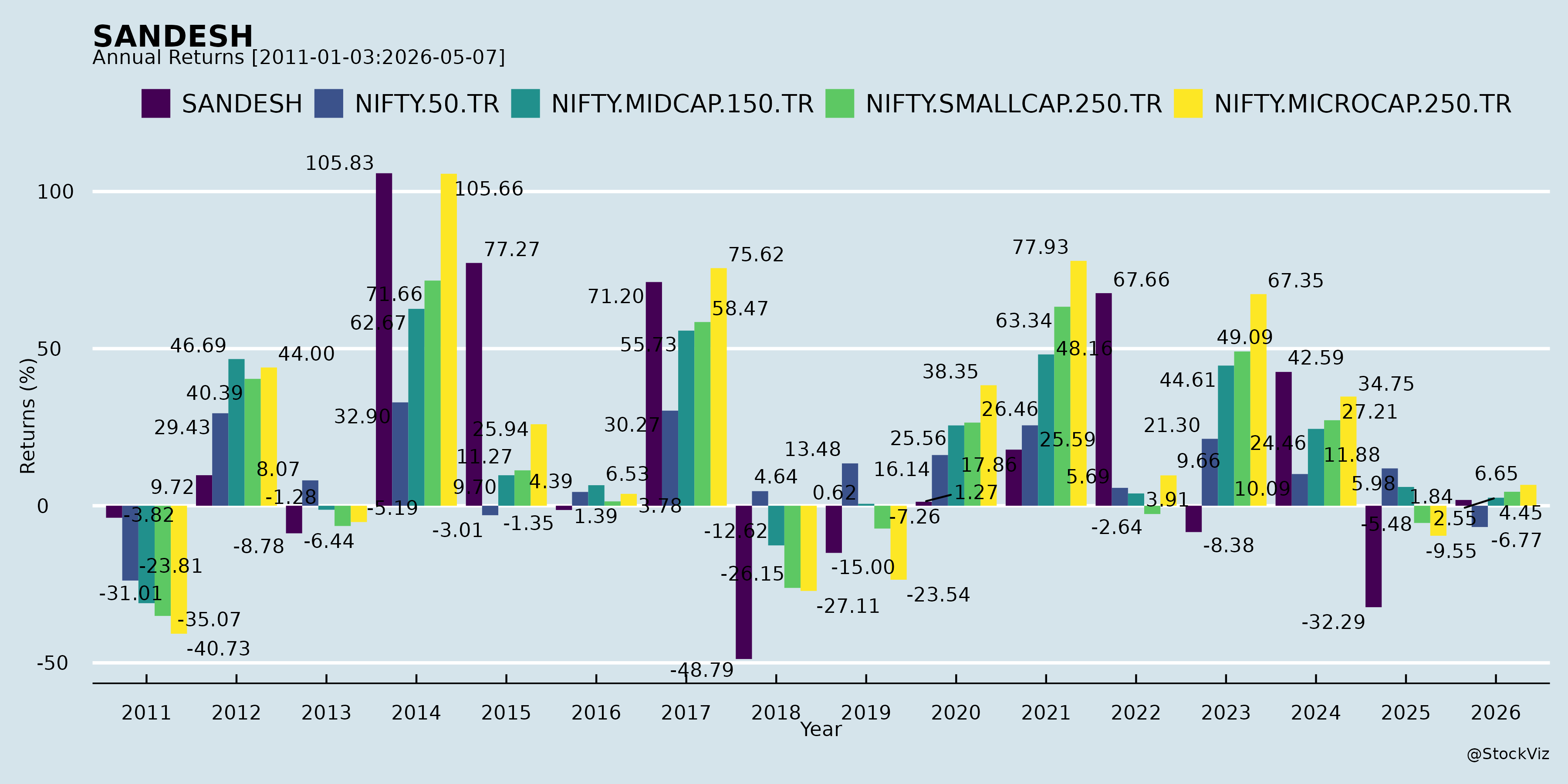

Annual Returns

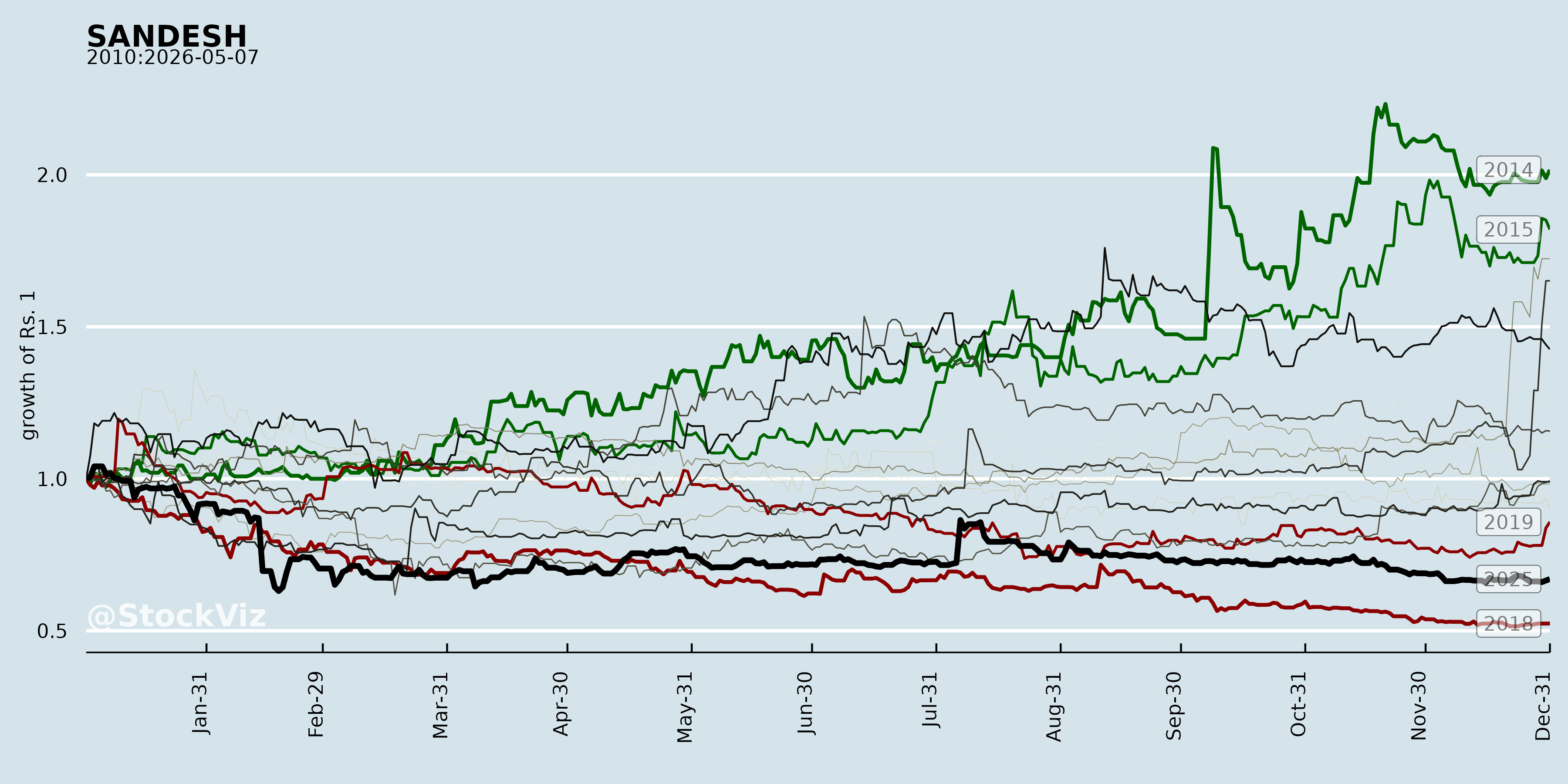

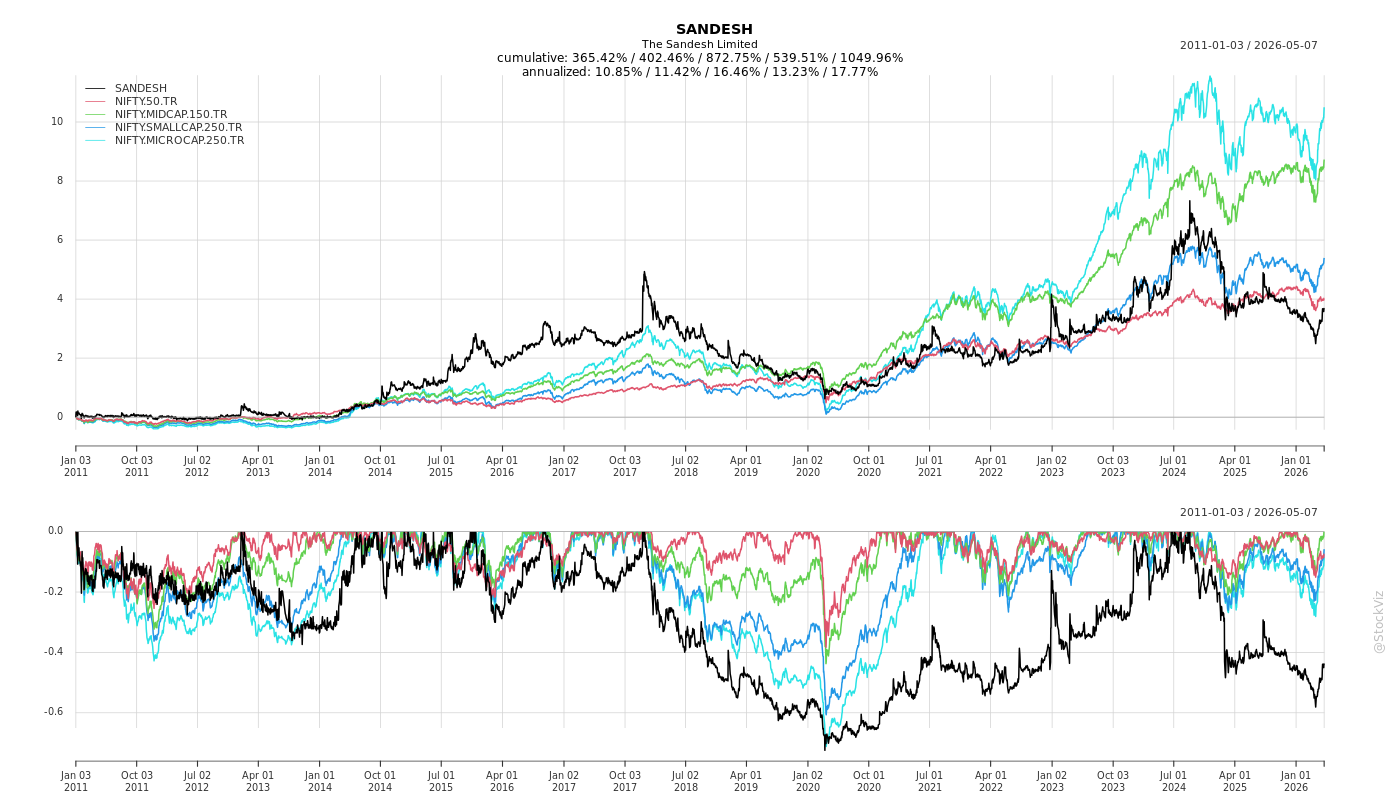

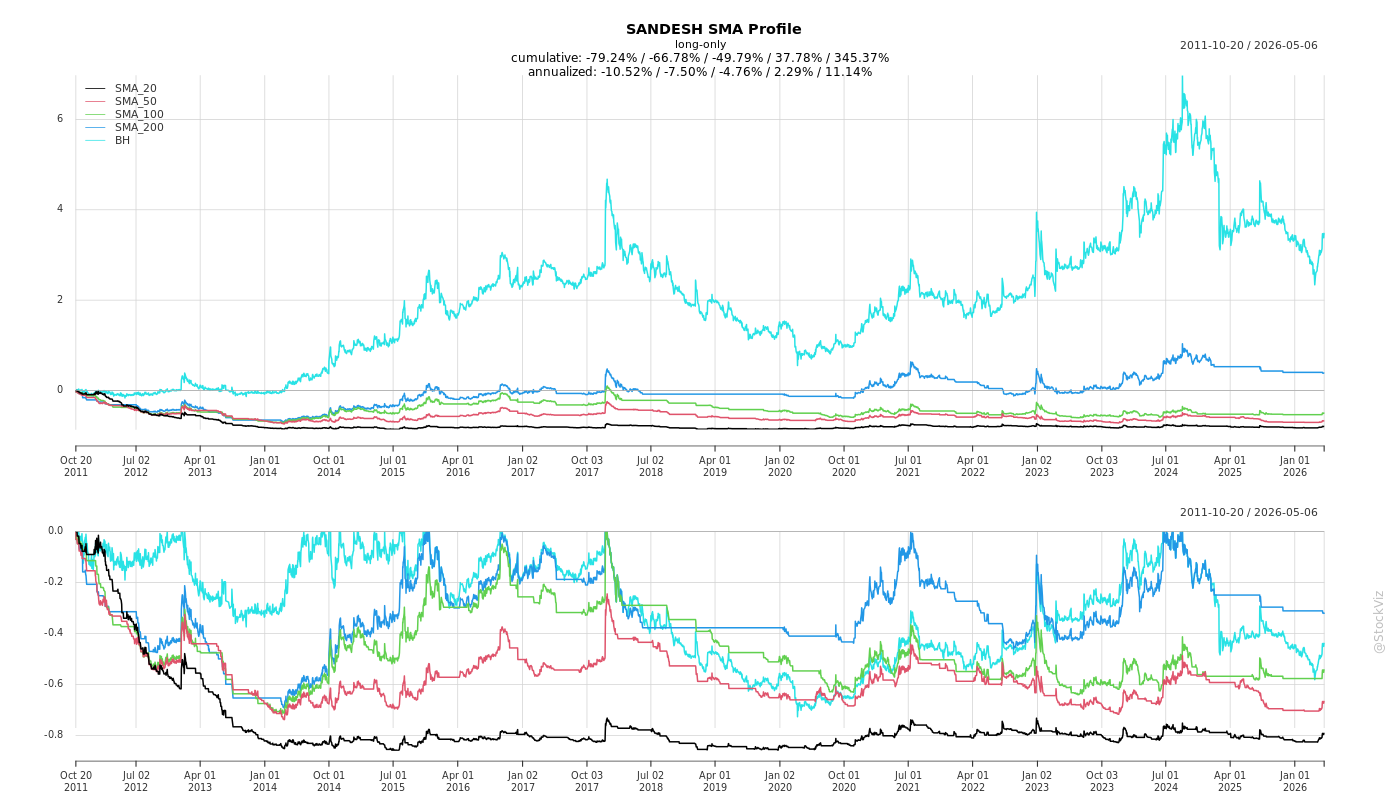

Cumulative Returns and Drawdowns

Fundamentals

Ownership

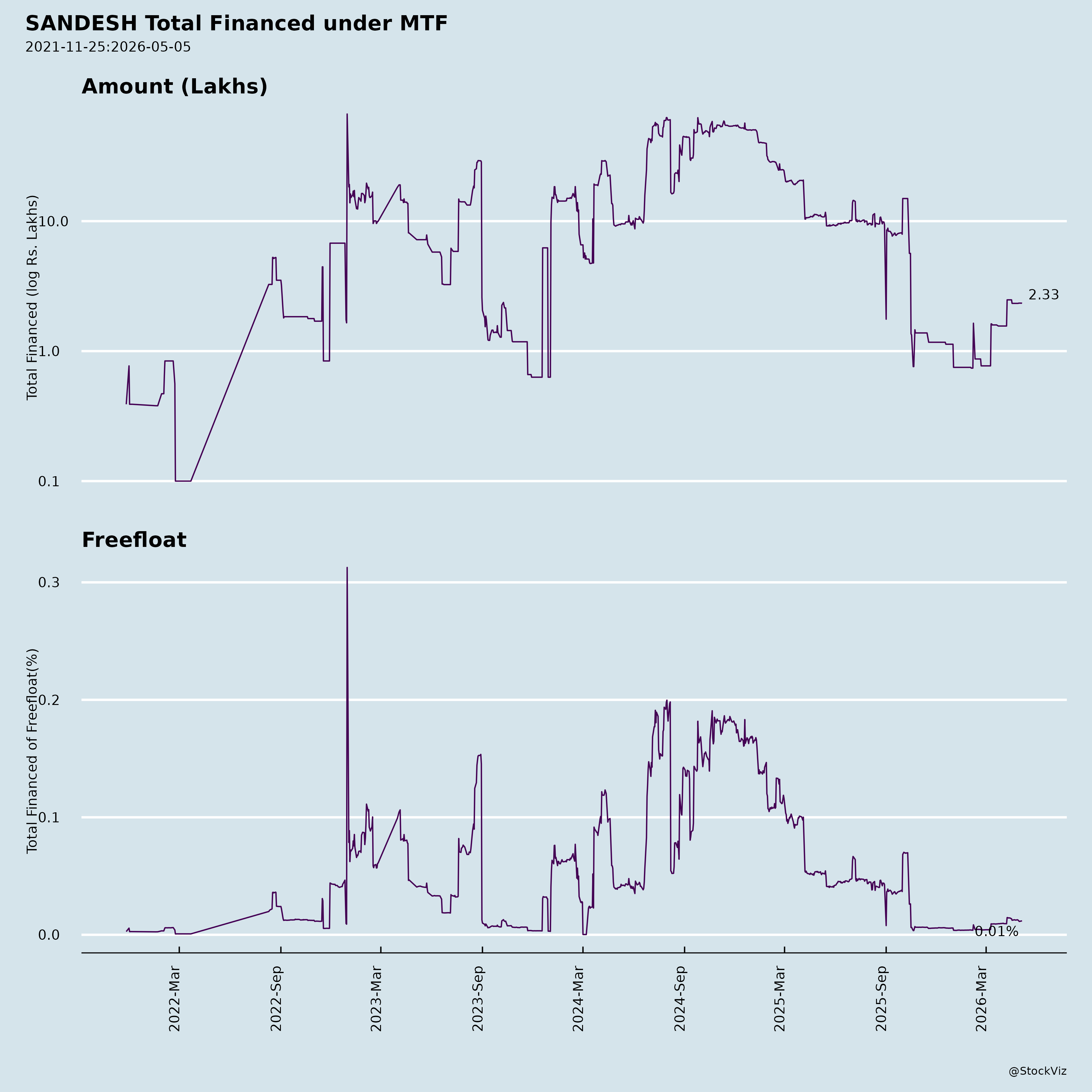

Margined

AI Summary

asof: 2025-11-27

Analysis of The Sandesh Limited (SANDESH) - Headwinds, Tailwinds, Growth Prospects, and Key Risks

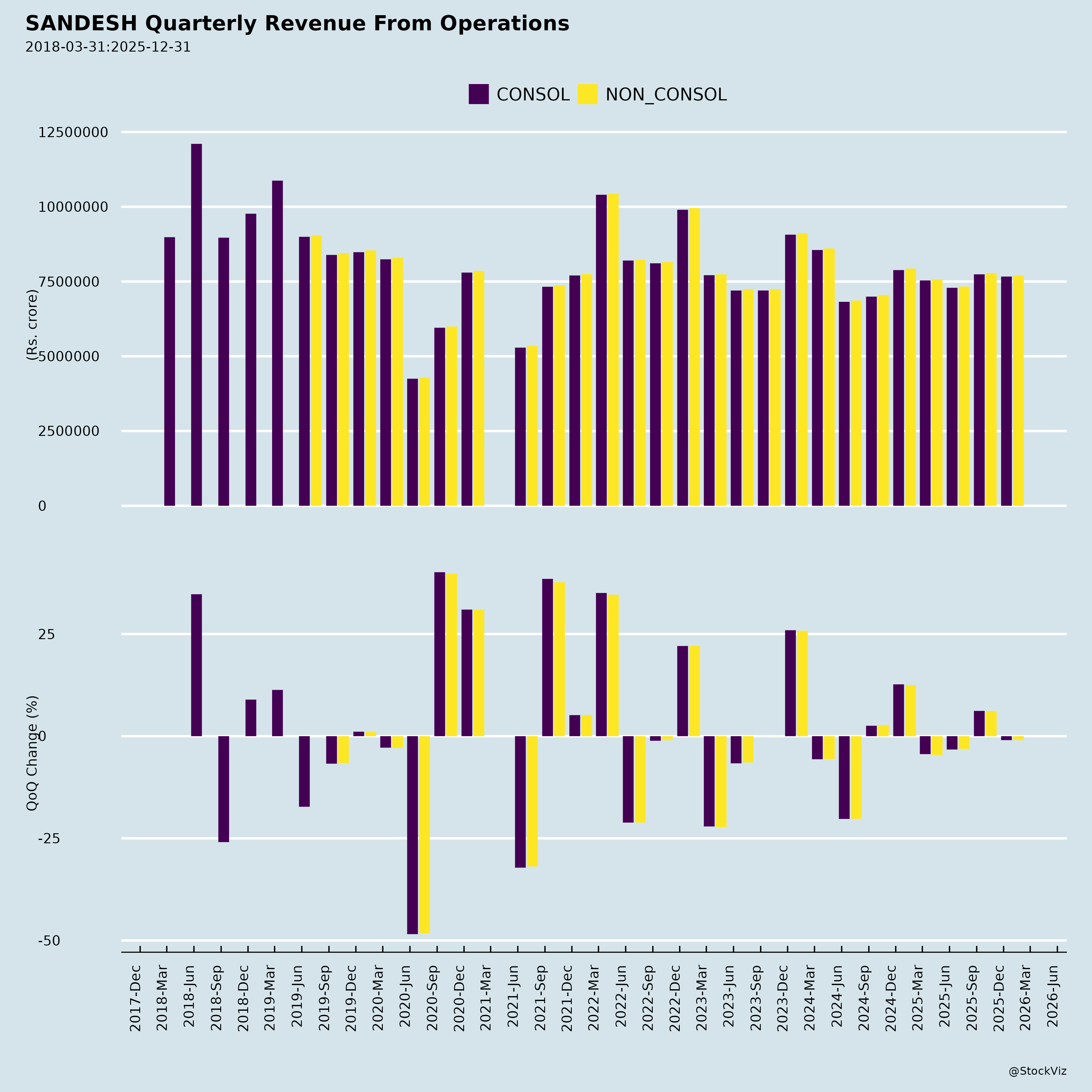

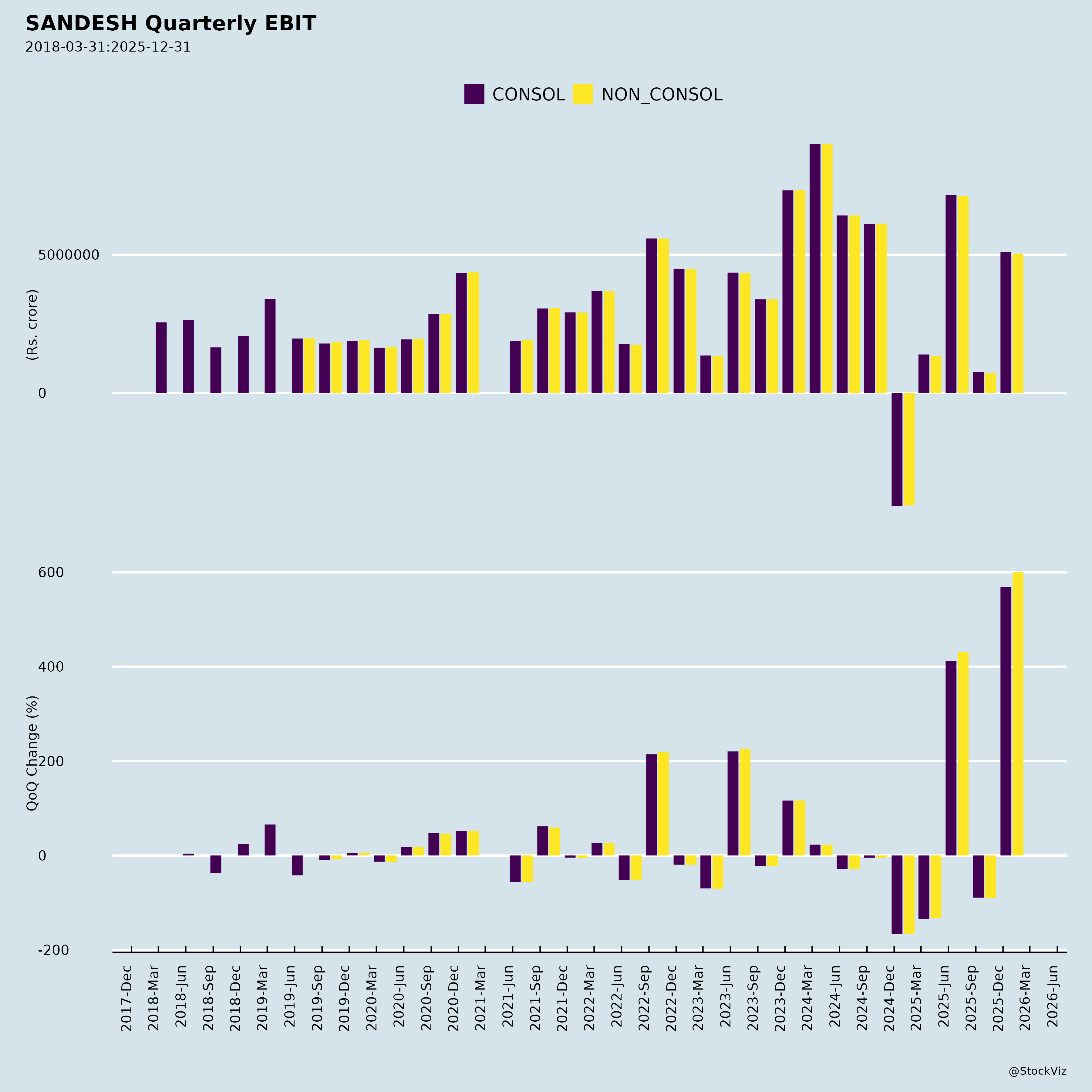

Overview: Sandesh Limited, a Gujarat-based media company (primarily newspapers), reported unaudited H1 FY26 (ended Sep 30, 2025) results. Standalone revenue from operations grew 9% YoY to ₹15,030 lakhs, but PAT declined 29% YoY to ₹6,263 lakhs due to volatile investment gains (Q1: +₹4,923 lakhs gain; Q2: -₹1,827 lakhs loss). Consolidated figures similar (PAT ₹6,190 lakhs). Balance sheet robust with ₹1.5 lakh crore assets (up 5% YoY), driven by investments (₹1.2 lakh crore). Low debt, strong cash flows from ops (₹2,647 lakhs standalone). AGM resolutions passed with ~100% promoter support.

Headwinds (Challenges Pressuring Performance)

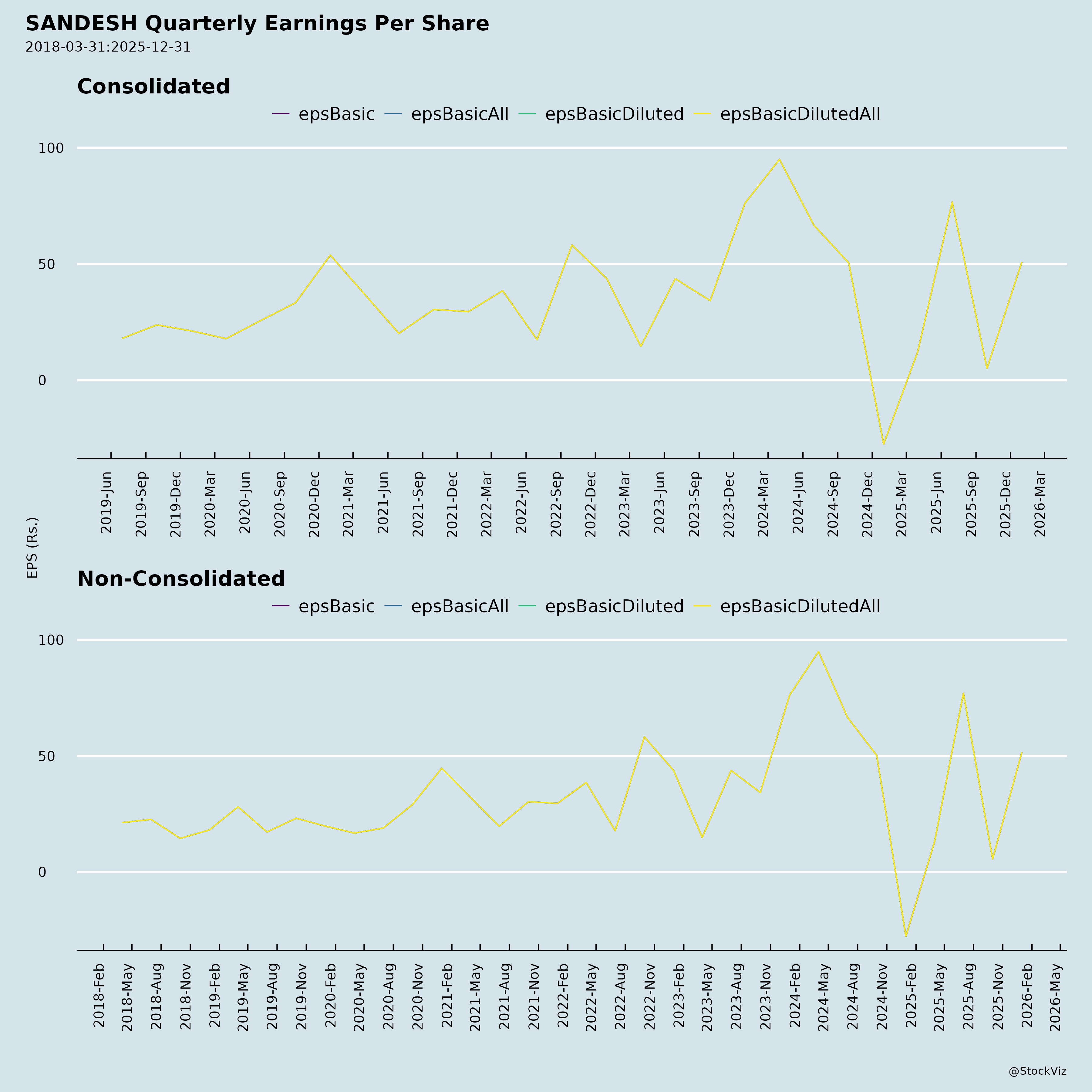

- Investment Volatility: ~25-40% of total income from FVTPL gains/losses on equity/MFs; Q2 swing from Q1 gains crushed profitability (PAT Q2: ₹429 lakhs vs. Q1: ₹5,834 lakhs).

- Declining Core Profitability: H1 PAT down 29% YoY despite revenue growth; high “other expenses” (₹4,269 lakhs, up due to investment losses) signals cost pressures.

- Media Sector Pressures: Ad revenue cyclical (Q2 ops revenue flat QoQ); digital shift evident in loss-making subsidiary (Sandesh Digital: ₹73 lakhs H1 loss).

- Cash Burn: Net cash down ₹852 lakhs H1 due to capex/investments; dividend payout (₹189 lakhs) adds minor pressure.

Tailwinds (Supportive Factors)

- Operational Resilience: Core media revenue up 9% YoY (H1: ₹15,030 lakhs); segment results strong (Media: ₹2,095 lakhs Q2 profit before interest/tax).

- Robust Balance Sheet: Equity ₹1.41 lakh crore; investments up 3-5% QoQ (₹1.2 lakh crore total); near-zero debt (finance cost <₹7 lakhs H1).

- Positive Cash Generation: Ops cash flow ₹2,647 lakhs (standalone); liquidity strong (cash + equivalents ₹1,160 lakhs).

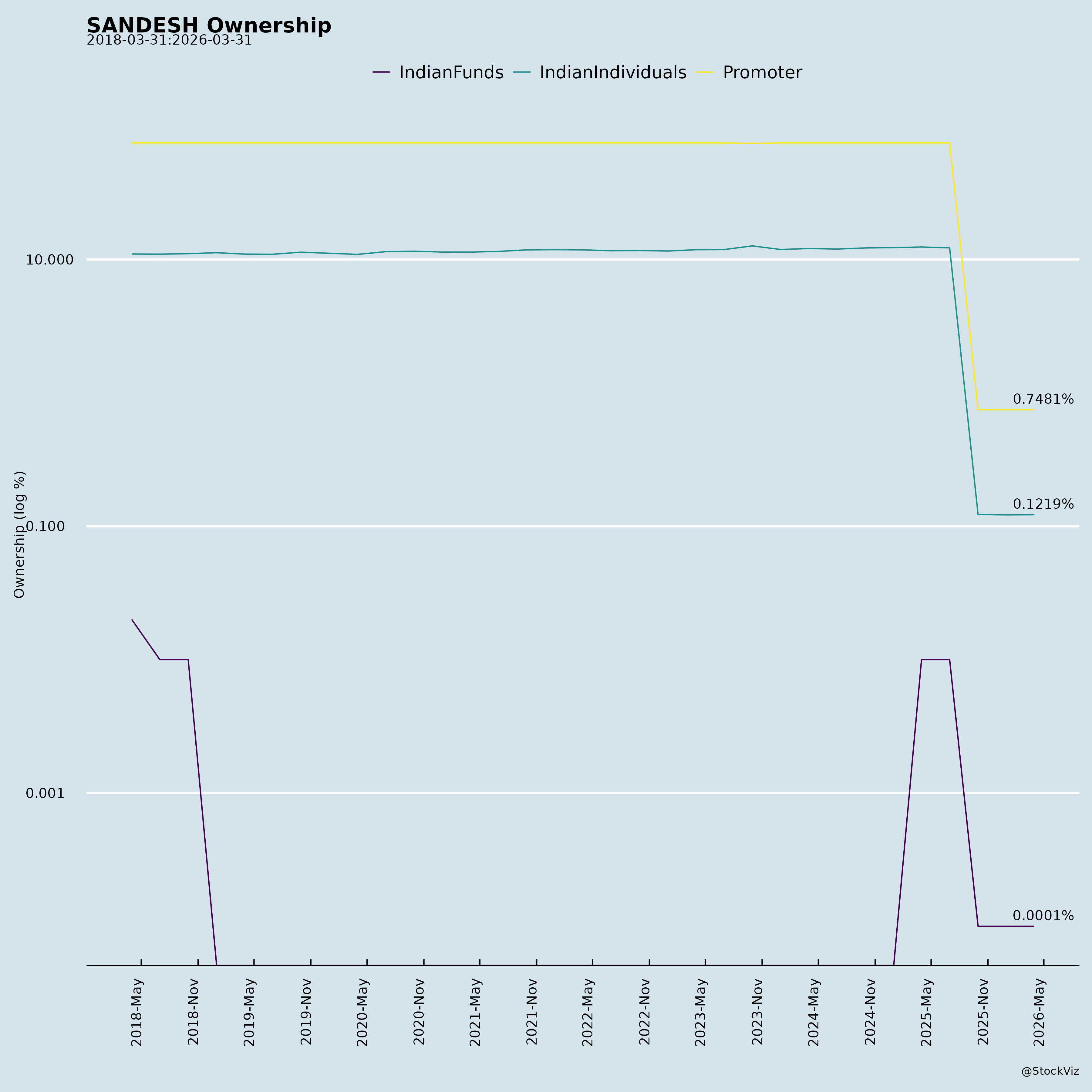

- Governance: Clean audit reviews; AGM approvals (e.g., MD continuation) with 99.99% favor; promoter holding ~75%.

Growth Prospects

- Media Expansion: Regional dominance in Gujarat; potential ad recovery (H1 growth); digital pivot via subsidiary (revenue ₹106 lakhs H1).

- Treasury Yield: Large investment corpus (65% current assets) could drive 10-15% returns in bull markets; historical FY25 gains ₹2,497 lakhs.

- Capex Momentum: PPE up 3% QoQ (₹5,940 lakhs); finance segment stable (₹209 lakhs H1 revenue).

- Outlook: FY26 revenue growth 8-10% possible if markets stabilize; EPS H1 at ₹82.74 (annualized ~₹165, premium to FY25 ₹102).

Key Risks

| Risk Category | Description | Mitigation |

|---|---|---|

| Market/Investment Risk (High) | 30-40% profit reliance on volatile FVTPL; equity/mkt corrections could erase gains (e.g., Q2 loss). | Diversified portfolio; but no hedge visible. |

| Operational Risk (Medium) | Media ad cyclicality; newsprint costs up (22% of expenses); digital losses. | Regional moat; cost controls (employee/depn stable). |

| Liquidity/Interest Rate Risk (Low) | Investing cash burn; rising rates on deposits. | Strong ops cash; low leverage. |

| Regulatory/Competition Risk (Medium) | SEBI/media regs; digital competition (e.g., online news). | Compliant (clean audits); promoter stability. |

| Execution Risk (Low) | Subsidiary drag; capex delays. | Wholly-owned; monitored via consol. |

Summary Verdict: Solid core media business with treasury tailwind, but high investment volatility caps rating (headwind dominant). Growth tied to market recovery; monitor Q3 for sustained ops momentum. Target P/E multiple: 8-10x (current implied ~10x annualized EPS). Positive AGM signals stability.

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.