Print Media

Industry Metrics

May 8, 2026

Annual Returns

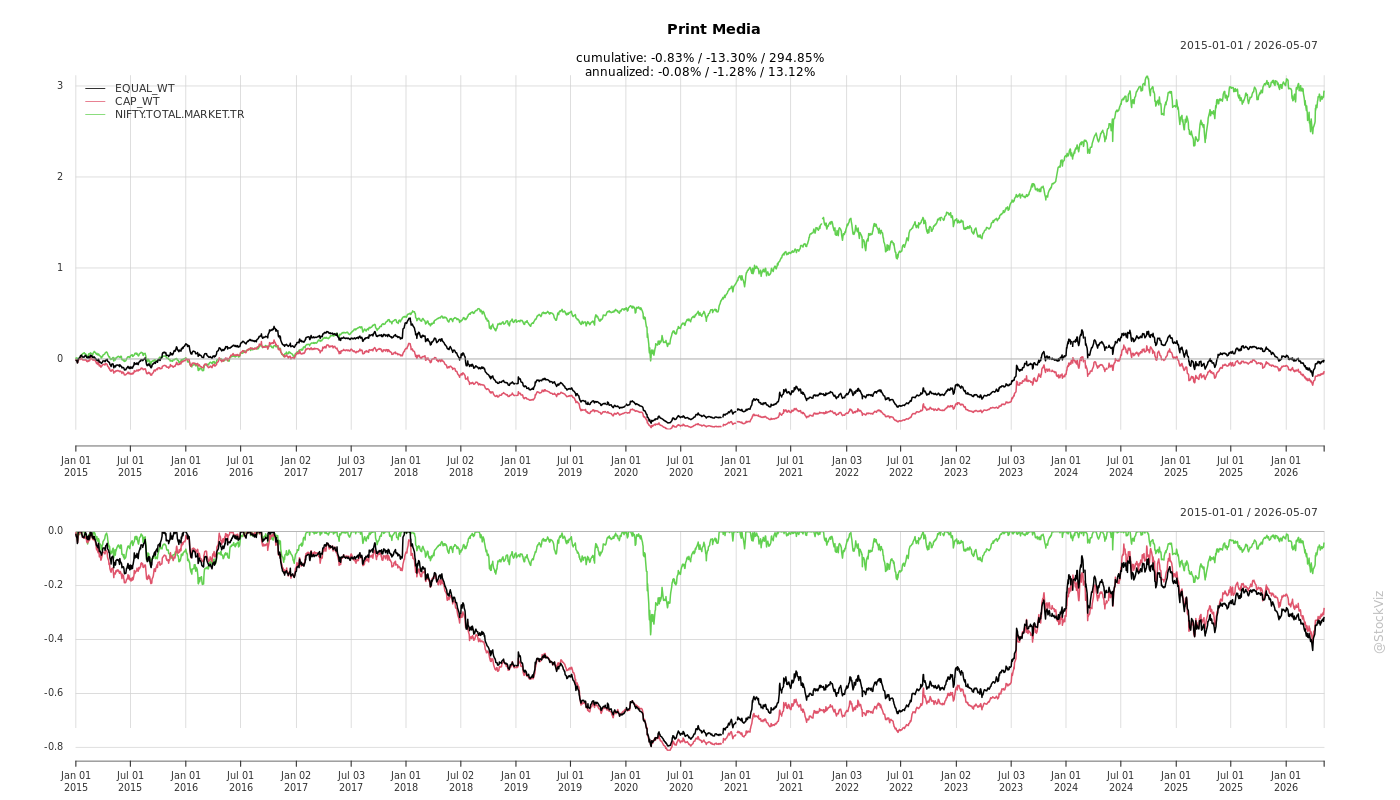

Cumulative Returns and Drawdowns

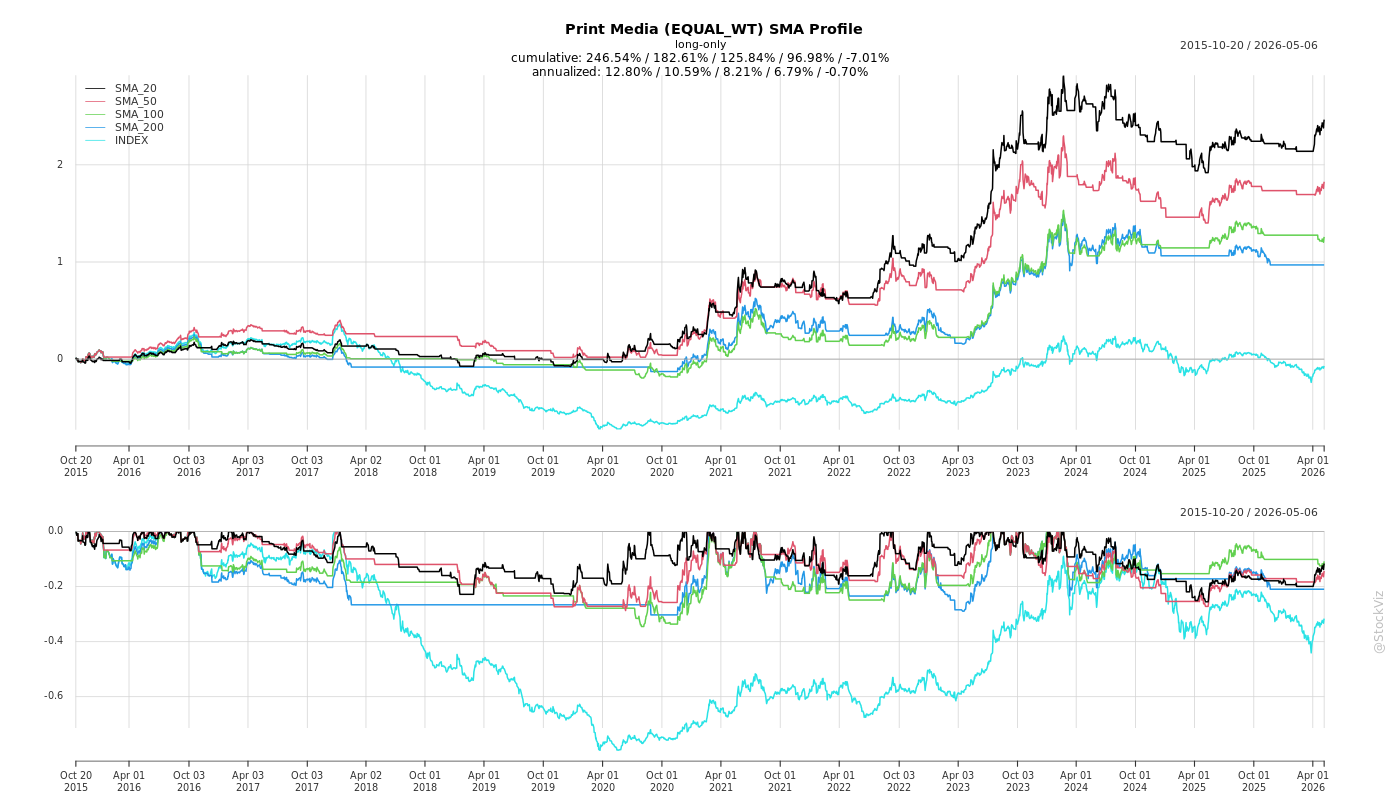

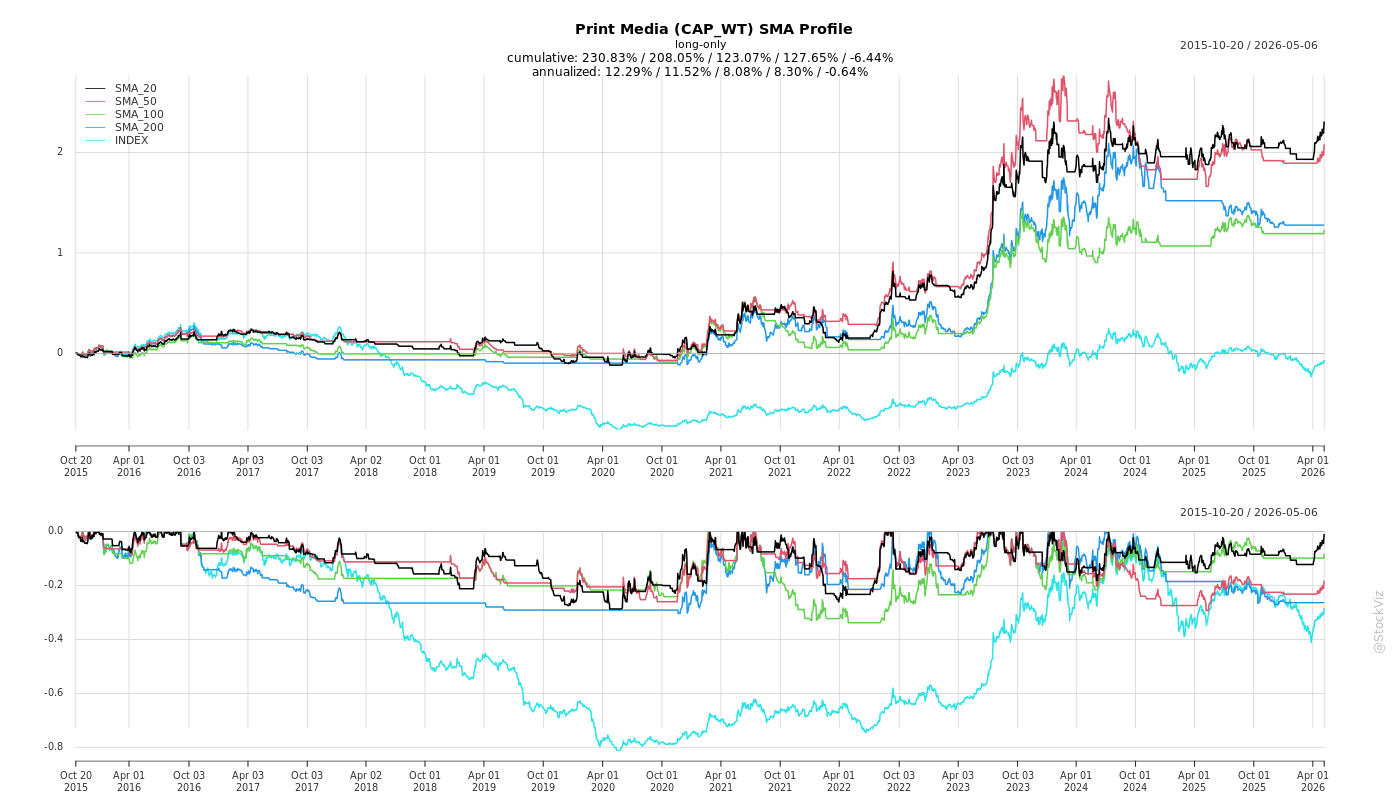

SMA Scenarios

Current Distance from SMA

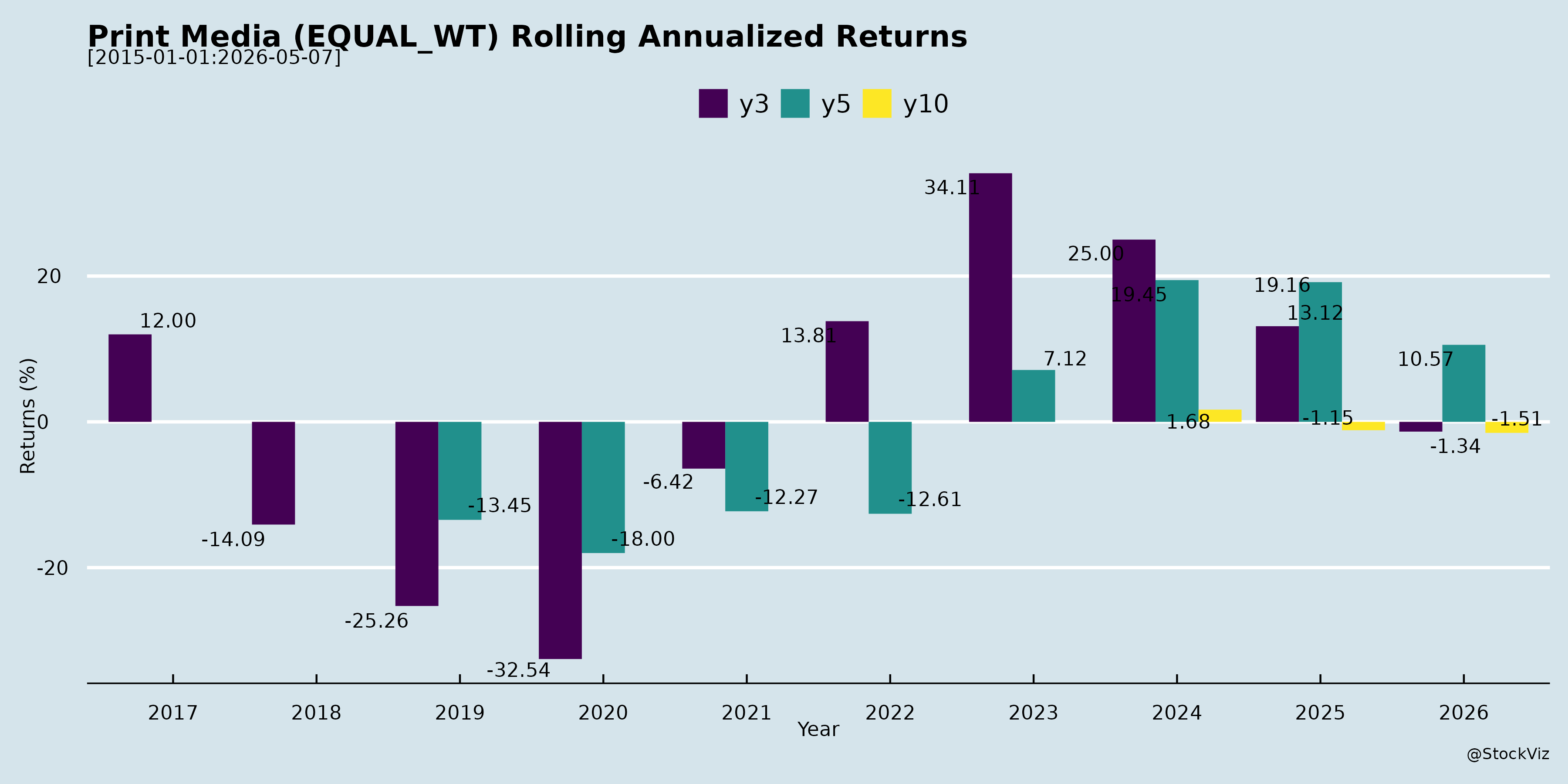

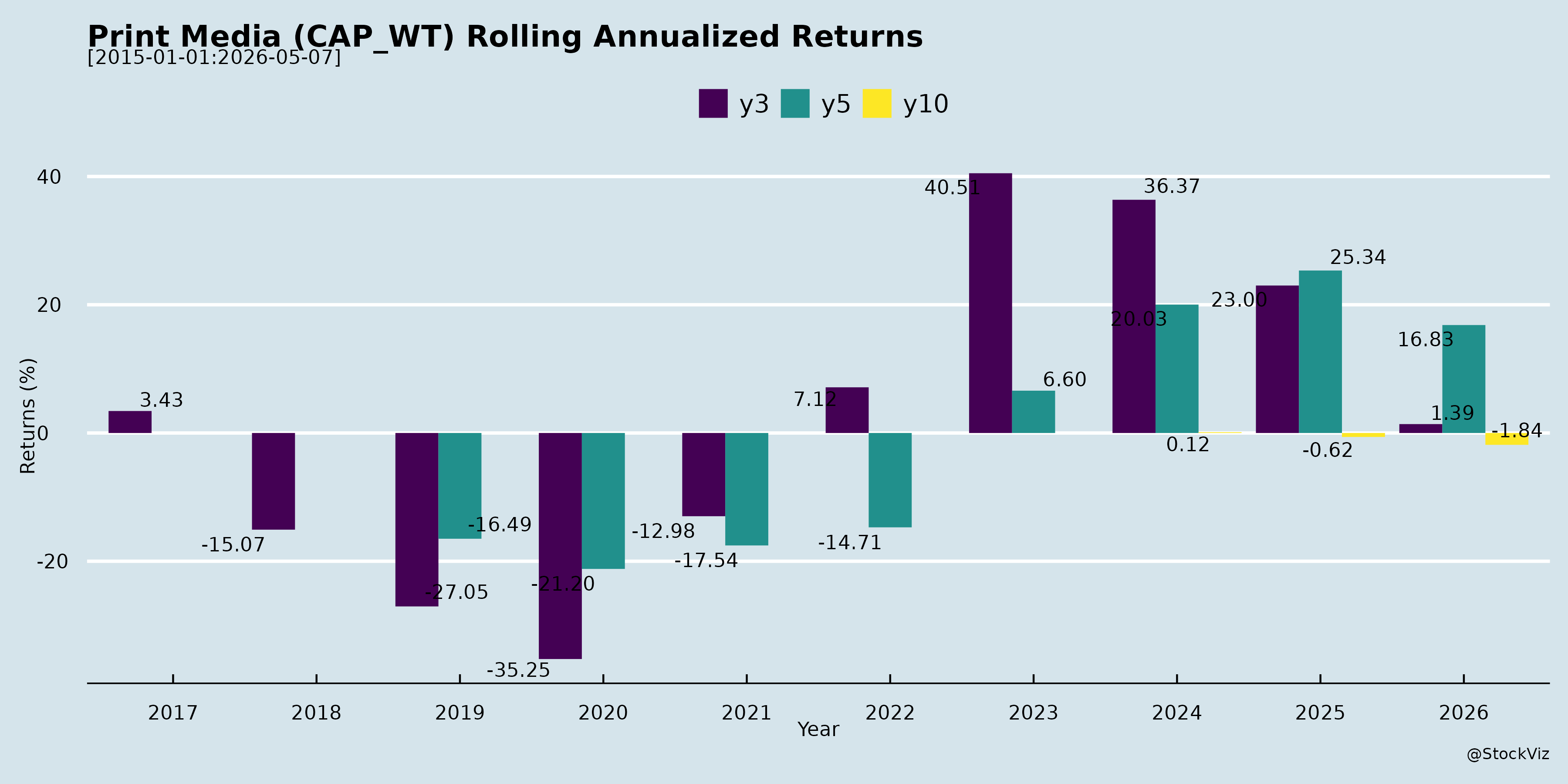

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-15

The Evolution of Challenges

The media and publishing companies have navigated a shifting landscape of challenges, ranging from volatile comparative base effects and commodity cycles to new regulatory frameworks.

- High Base Effects and Seasonal Shifts: A significant recent challenge for revenue growth has been the year-over-year comparison anomalies caused by shifting festive seasons and election cycles. For instance, DB Corp’s advertising revenue in Q3 FY26 declined by 7.8% year-over-year largely because festive advertising spends shifted heavily into Q2, whereas in the previous year, they were concentrated in Q3 [1-3]. Furthermore, the absence of state elections (such as those in Haryana and Jharkhand) that boosted ad revenues in the previous year created a high base effect that was difficult to match [1, 3]. HT Media faced a similar challenge in its Radio business, where revenue contracted sharply due to the high base effect of a major event held in the previous year [4-6].

- Regulatory and Compliance Burdens: The Government of India’s notification to consolidate multiple existing labour laws into four new Labour Codes has created immediate financial friction across the industry [7-9]. Companies including DB Corp, Sandesh Limited, and Jagran Prakashan have had to reassess their employee benefit obligations—such as gratuity—based on the revised definition of wages [7, 9, 10]. This regulatory evolution resulted in companies booking one-time incremental provisions and exceptional items in their financial statements [9-12]. Additionally, Jagran Prakashan faced scrutiny from the Income Tax Department, receiving a Notice of Demand for Rs. 1.19 crores and an accompanying penalty notice, which the company intends to appeal [13-15].

- Commodity Cycles and Geopolitical Risks: The cost of newsprint, a massive operational expense for publishers, moves in distinct cycles. While companies have recently benefited from being at the bottom of the price cycle, market indicators and the current geopolitical scenario suggest that newsprint prices will see a gradual increase in the coming quarters [16, 17]. To mitigate this evolving challenge, companies are forced to continuously optimize their buying, adjust their newsprint mix, and control consumption [18, 19].

- Competitive Circulation Pressures: In previous years, intense competitive pressure in certain markets led to an over-distribution of print copies, which negatively impacted pricing power [20, 21]. Although this has recently stabilized to more reasonable levels, maintaining circulation revenue requires constant vigilance against market-to-market copy wars [20, 21].

The Evolution of Opportunities

To counteract traditional publishing headwinds, companies have aggressively evolved their business models, capitalizing on digital transformation, technological innovation, and macro-economic tailwinds.

- Scaling Digital-First and “Phygital” Offerings: The most significant evolution is the transition toward robust digital platforms that complement traditional print. DB Corp has successfully maintained a dominant position in the News App space, growing its Monthly Active Users (MAUs) to approximately 21 million by utilizing a three-dimensional digital strategy focused on high-quality original content, superior user experience, and strong technology [22-24]. HT Media’s digital business has similarly validated its digital-first commitment, delivering a 30% year-over-year revenue growth while significantly improving its margins and maintaining a clear path to profitability [25, 26]. Jagran Prakashan’s digital properties also rank among the top 15 in the news category, boasting around 51 million unique visitors [27]. Emphasizing this digital shift, Sandesh Limited recently appointed a Senior Digital Content Head to drive SEO-driven growth, data-centric content planning, and the management of a modern digital newsroom at scale [28, 29].

- Artificial Intelligence (AI) and Content Monetization: AI is evolving from a basic tool for cost efficiency into a core driver of engagement and potential revenue. DB Corp successfully deployed an AI election chatbot alongside interactive digital features during the Bihar elections, driving record engagement of 21 million MAUs and 21 minutes of average time spent on their app [30]. HT Media utilizes AI as a powerful tool for its editorial setup and anticipates that the proliferation of AI will place a higher premium on the credibility and trustworthiness of traditional news sources [31, 32]. Furthermore, proposed government regulatory frameworks may soon require AI platforms to compensate original content creators for the data they use, opening up a highly lucrative future revenue stream for established publishers [33, 34].

- Macro-Economic Tailwinds: Companies are strategically positioning themselves to benefit from broader economic developments. The industry expects that upcoming events, such as the Union Budget and anticipated revisions in government pay and allowances, will spur consumer spending and subsequently boost advertising budgets in the fourth quarter and beyond [35].

- Print Resilience and Margin Expansion: Despite the digital pivot, the core print business has evolved to yield higher profitability through strict cost discipline and pricing power. Favorable newsprint prices, combined with a tight grip on discretionary marketing and administrative spends, have allowed companies to expand their EBITDA margins significantly [4, 36, 37]. HT Media reported sequential and year-over-year upticks in advertising pricing, proving that established print mastheads still retain strong monetization capabilities [36, 38].

What are the headwinds affecting this industry?

asof: 2026-04-15

High Base Effects from Shifts in Festive and Election Spending A significant headwind currently limiting year-over-year revenue growth across the print and media industry is the high base effect from the previous year [1-3]. For example, D.B. Corp Limited reported a 7.8% decline in year-over-year advertising revenue and a 4% decline in total revenue for Q3, which was heavily impacted by a shift in the festive calendar [3]. While festive spending was highly concentrated in Q3 during the previous year, a portion of it shifted to Q2 in the current financial year [1, 3, 4]. Additionally, the previous year benefited from a surge in political advertising due to state elections in Haryana and Jharkhand, an influx of revenue that was absent in the current period [3]. HT Media also experienced this high base effect in its Hindi print advertising revenues [2, 5-7], and its Radio business saw a sharp revenue drop due to a massive event-led revenue base in the prior year [2, 5, 8, 9].

Financial Impact of the New Consolidated Labour Codes Regulatory changes have introduced sudden, one-time financial burdens across the industry. The Government of India’s notification of four consolidated Labour Codes has forced companies to reassess their employee benefit obligations, particularly regarding the revised definition of wages and its impact on gratuity and past service costs [10-13]. This has forced multiple media entities to book significant provisions and exceptional expenses: * HT Media booked an exceptional item of approximately INR 41.4 crores to true-up its carrying liabilities under the new laws [14-17]. * The Sandesh Limited recognized an incremental statutory impact of Rs. 241.13 Lakhs under exceptional items to account for retirement and gratuity benefits [11, 12, 18, 19]. * Jagran Prakashan Limited saw its operating profits directly impacted by Rs. 5.76 crores (standalone) and Rs. 6.89 crores (consolidated) due to provisions made to effect the new labour codes [20-22]. * D.B. Corp Limited reported a one-time estimated increase in employee benefit provisions of Rs. 15.17 million [10, 23].

Challenging Environment for the Radio Segment The radio broadcasting segment is actively struggling against a “challenging market environment where revenues and margins remain under pressure” [8, 9, 24, 25]. Companies are having to proactively recalibrate their radio operations to better align with current, difficult industry dynamics [8, 9, 24, 25]. The severity of these challenges is highlighted by past financial periods; for instance, Jagran Prakashan noted that its radio cash-generating unit previously required a massive impairment loss of Rs. 12,089.42 Lakhs [26].

Looming Newsprint Cost Increases and Pricing Limitations While the industry has recently benefited from being at the bottom of the newsprint pricing cycle, market indicators suggest a gradual upward shift in newsprint commodity prices is approaching [27-30]. This poses a future headwind because passing these increased costs onto consumers is highly challenging. Management at HT Media noted that mitigating higher paper costs by increasing cover prices will be “a tougher part when priced in the Hindi markets for sure,” and historical trends show that advertising pricing does not easily move in tandem to offset these spikes [31-34]. Furthermore, the print industry occasionally battles competitive pressures where publications try to increase copy volumes in certain markets, which subsequently suppresses pricing power [35-38].

What are the key things to understand about this industry?

asof: 2026-04-15

The media and publishing industry operates across a diverse portfolio of business segments, primarily relying on print publications (such as daily newspapers in multiple languages like English, Hindi, Gujarati, and Marathi), FM radio broadcasting, and rapidly expanding digital platforms [1-7]. Additionally, several companies maintain presence in outdoor advertising, promotional marketing, and event management [5, 6].

To thoroughly understand this industry, one must look at the specific dynamics driving its revenues, costs, technological evolution, and regulatory environment:

1. Revenue Streams and Seasonality The industry’s financial health is heavily dependent on two main pillars: advertising and circulation. * Advertising Revenue: This is the most significant revenue driver across print, radio, and digital platforms. However, advertising spend is highly cyclical and vulnerable to base effects from seasonal shifts [8-12]. For example, corporate financial performance heavily fluctuates based on the timing of major festive seasons (which can shift between different financial quarters) and large-scale regional or national elections that temporarily boost ad spending [12-16]. * Circulation Revenue: This is generated by the sale of physical newspaper copies. Companies must carefully navigate competitive pressures by balancing the number of copies printed with cover pricing strategies to ensure circulation revenues remain steady [8-11, 17-20]. * Other Operating Income: Companies also supplement their income through outside printing jobs, scrap sales, and forfeitures related to standard operating business arrangements [21-24].

2. Critical Cost Drivers and Margin Management Profitability in the print sector is highly sensitive to commodity cycles, most notably the cost of newsprint [25-28]. * Newsprint Volatility: Newsprint prices are subject to global commodity cycles, geopolitical developments, and foreign exchange movements [29-33]. To mitigate price hikes, companies employ strategies such as optimizing their buying, adjusting the mix of newsprint used, and strictly controlling consumption [34-37]. Raising the cover price of the newspaper to offset these costs is often challenging, particularly in highly competitive regional markets like the Hindi-speaking belt [34-37]. * Discretionary Spending: To expand their EBITDA margins, companies rely heavily on strict cost discipline, tightly controlling discretionary expenditures such as marketing, administrative, and event costs [8-11, 25-28].

3. The Digital-First Transition Legacy print and radio companies are aggressively scaling their “digital-first” offerings to maintain a path toward future profitability [1-4]. * User Engagement: A major strategic focus is driving the growth of Monthly Active Users (MAUs) on mobile applications and news portals [33]. * Premium Content and Technology: The industry is investing heavily in high-quality, premium journalism in multiple formats, including rich text, visual graphics, and short vertical videos specifically designed for mobile users [38, 39]. Furthermore, companies are leveraging strong technology platforms to personalize news experiences based on user demographics, location, and real-time context, which helps drive long-term retention and loyalty [39, 40].

4. The Integration and Impact of Artificial Intelligence (AI) AI represents both an operational tool and a potential strategic advantage for the industry [41-44]. * Operational Enabler: AI is currently utilized to assist editorial setups and create better, more efficient content offerings, such as AI election chatbots [40-44]. * Credibility and New Revenue: With the proliferation of AI-generated content, there is a growing premium placed on trustworthiness, which positions established, credible news publishers advantageously [41-44]. Furthermore, evolving government regulatory frameworks may soon require AI platforms to financially compensate original content creators for the data they use, which is viewed as a highly positive potential revenue stream for the industry [45-52].

5. Impact of Regulatory Changes: The New Labour Codes A significant, uniform factor currently impacting the financial statements across the Indian media industry is the Government of India’s implementation of the ‘New Labour Codes’ [53-57]. * This regulatory shift consolidates multiple existing labour legislations into a unified framework [57-61]. * Under accounting standards (Ind AS 19), changes to the definition of wages have constituted a plan amendment for employee benefits, requiring companies to immediately recognize past service costs [57, 58]. Consequently, companies have had to book substantial exceptional items and make provisions in their profit and loss statements to account for increased employee benefit expenses, particularly concerning gratuity and retirement benefits [53-58, 62-64].

6. Editorial Influence and Brand Trust At its core, the industry relies on courageous and responsible journalism to build its brand and drive audience engagement [65]. Exclusive investigations, data-driven analysis, and ground-level reporting on civic and political issues not only shape public discourse but frequently compel direct government action and policy changes [65-69]. Maintaining this editorial excellence is what ultimately sustains the loyal user base necessary for both circulation and digital growth [38, 65].

What are the tailwinds affecting this industry?

asof: 2026-04-15

Stable and Softening Newsprint Prices are a major factor driving profitability in the print media industry. Companies are currently benefiting from newsprint commodity cycles remaining at the bottom, with prices consistently lower than the previous year [1]. The market has experienced stable newsprint prices along with some sequential rate corrections, which directly aids in healthy margin expansions [2, 3]. This critical cost relief, paired with a disciplined approach to discretionary spending, has translated into meaningful growth in operational profitability and EBITDA margins [2, 4, 5].

Improving Advertiser Sentiment and Ad Pricing is also contributing to the industry’s positive momentum. There has been a gradual pick-up in advertising demand across markets, reflecting an improving sentiment among advertisers [6]. Media groups are successfully implementing pricing growth in their ad rates, witnessing upticks on both a sequential and year-over-year basis [2, 7]. This resilience is notably strong in English language titles, which have driven sequential and annual growth in advertising revenues despite shifts in festive season timelines [4, 8].

Upcoming Macroeconomic and Policy Catalysts are expected to further bolster the sector. Industry leaders remain optimistic about the overall consumption outlook in India [9]. Specifically, the upcoming Union Budget, anticipated revisions in government pay and allowances, and other supportive policy measures are projected to stimulate consumer spending in the upcoming quarters [9]. This anticipated boost in consumer spending creates a favorable environment for advertisers to increase their marketing budgets.

Rapid Digital Transformation and Audience Growth represent a robust structural tailwind. The industry is successfully scaling its digital-first offerings, with digital business segments delivering significant year-over-year revenue growth and improving margins [10-12]. For instance, news applications have seen massive traction, with platforms like Dainik Bhaskar growing their user base almost tenfold since 2020 to reach approximately 21 million Monthly Active Users (MAUs) [3, 13]. By leveraging strong technology platforms, personalized news experiences, and high-quality original content across formats like hyper-local news and short videos, publishers are driving deep user engagement, loyalty, and long-term retention [13-15].

Emerging AI Monetization and Favorable Regulatory Frameworks are providing a highly promising avenue for future revenue. As artificial intelligence integration becomes more prevalent, the premium placed on the credibility and trustworthiness of established news publishers puts them in a highly advantageous position [16, 17]. Furthermore, proposed government regulations suggest that AI platforms will be required to compensate original content creators for the data they utilize to train and operate their models [18-20]. This evolving regulatory environment is viewed as a significant positive enabler, potentially transforming AI from a mere operational efficiency tool into a material and viable revenue opportunity for original news publishers [18, 20, 21].

What is the general outlook of this industry?

asof: 2026-04-15

The print and media industry is demonstrating strong resilience, characterized by stable topline performance, steady circulation revenues, and meaningful growth in overall profitability. [1-4] Media companies are reporting positive momentum primarily driven by upticks in advertising revenue across established print mastheads and a highly disciplined approach to cost management. [2, 5-7] For instance, the industry has seen consistent advertiser sentiment and pricing growth, which has directly translated to expanded operating margins and increased profit after tax (PAT). [8-12] Even in the face of fluctuating seasonal billing and high base effects from previous election cycles, operational efficiencies and cost control measures have allowed the core print segment to maintain healthy margins. [12-14]

Favorable raw material costs are currently supporting profitability, though companies remain cautious about future commodity cycles. [8, 15-17] Newsprint prices, a major direct cost component for the industry, have remained stable and at the bottom of their cycle, with some sequential rate corrections actively contributing to better operating margins. [15, 18] While industry management expects newsprint prices to remain relatively range-bound in the near term, there is an anticipation of potential gradual increases in the future, largely dependent on evolving geopolitical developments and foreign exchange movements. [15, 17-19] To mitigate these cyclical market fluctuations, companies plan to continuously optimize their newsprint buying mix and tightly control overall consumption. [20-22]

Digital transformation and “digital-first” offerings have emerged as critical pillars for future growth and audience retention. [18, 23-25] The digital segment is delivering exceptionally strong performance, marked by significant year-on-year revenue increases, expanding Monthly Active Users (MAUs), and steadily improving margins. [18, 26-28] Companies are heavily investing in technology to deliver personalized, high-quality journalism and hyperlocal coverage across multiple digital formats, including rich text, visual graphics, and short vertical videos. [29, 30] This strategic shift toward a “phygital” (physical plus digital) model is driving deep audience engagement, long-term user loyalty, and an increased willingness from consumers to pay for premium original content. [18, 29, 30]

Artificial Intelligence (AI) is increasingly viewed as a significant operational enabler and a potential new revenue stream. [31-34] Within the industry, AI is currently being utilized as a powerful tool to improve overall productivity and assist editorial setups. [31, 33, 35] Furthermore, the rise of AI places a high premium on content credibility and trustworthiness, which benefits established news sources. [31, 33, 35] With the government proposing regulatory frameworks that would require tech platforms to financially compensate original content creators for the data used by their AI models, trusted news organizations find themselves in an advantageous position to monetize their proprietary content. [36-39]

Macro-economic tailwinds and policy measures are expected to bolster consumer spending, further supporting industry growth. [40] The management outlook on overall consumption in India remains highly positive. [40] Upcoming governmental policies, such as expected revisions in government pay and allowances, as well as broader Union Budget measures, are anticipated to stimulate consumer spending in the upcoming quarters. [40] Combined with strong brand presence, deep editorial connections, and growing digital reach, media organizations believe they are well-positioned to capture these emerging market opportunities. [40]

Conversely, the Radio broadcasting segment is navigating a much more challenging market environment. [2, 4, 41, 42] Unlike the flourishing print and digital sectors, radio revenues and margins have remained under sustained pressure, often struggling to grow against high base effects from previous event-led business cycles. [2, 4, 43, 44] Consequently, media groups are proactively recalibrating their radio operations and offerings to ensure the segment is better aligned with current industry dynamics and to chart a clearer path toward profitability. [2, 4, 23, 24]

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.