MOTILALOFS

Equity Metrics

May 8, 2026

Motilal Oswal Financial Services Limited

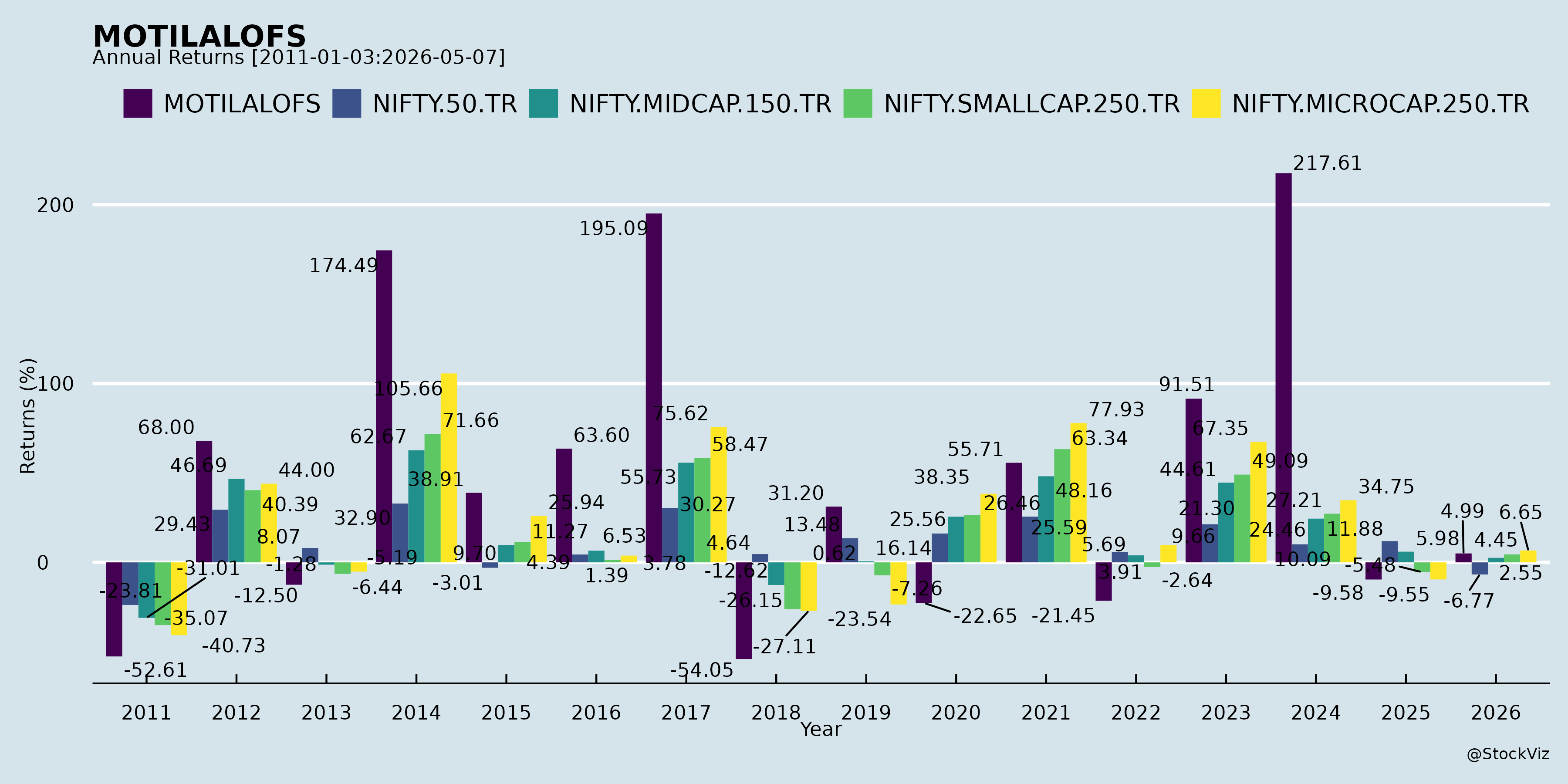

Annual Returns

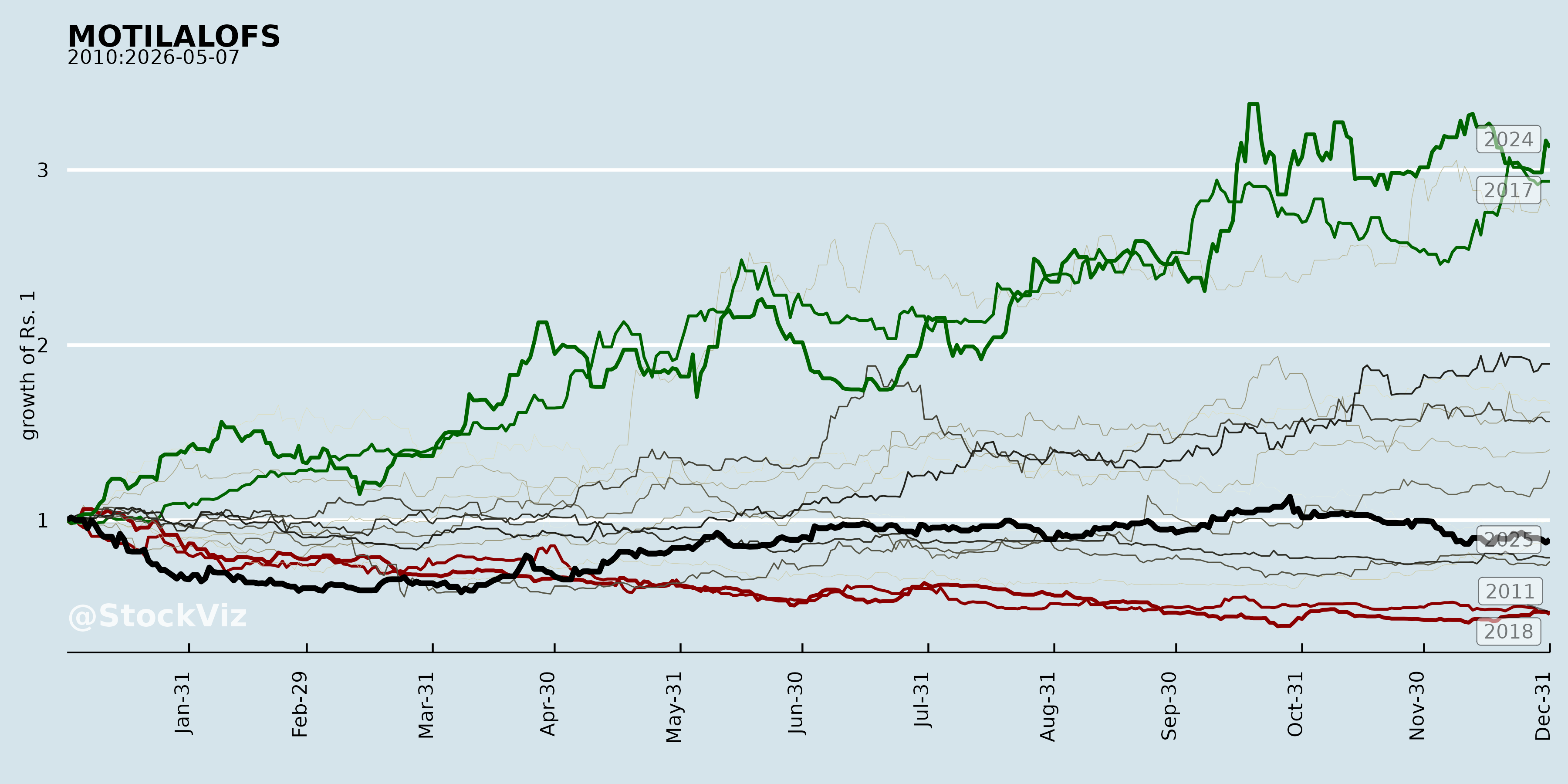

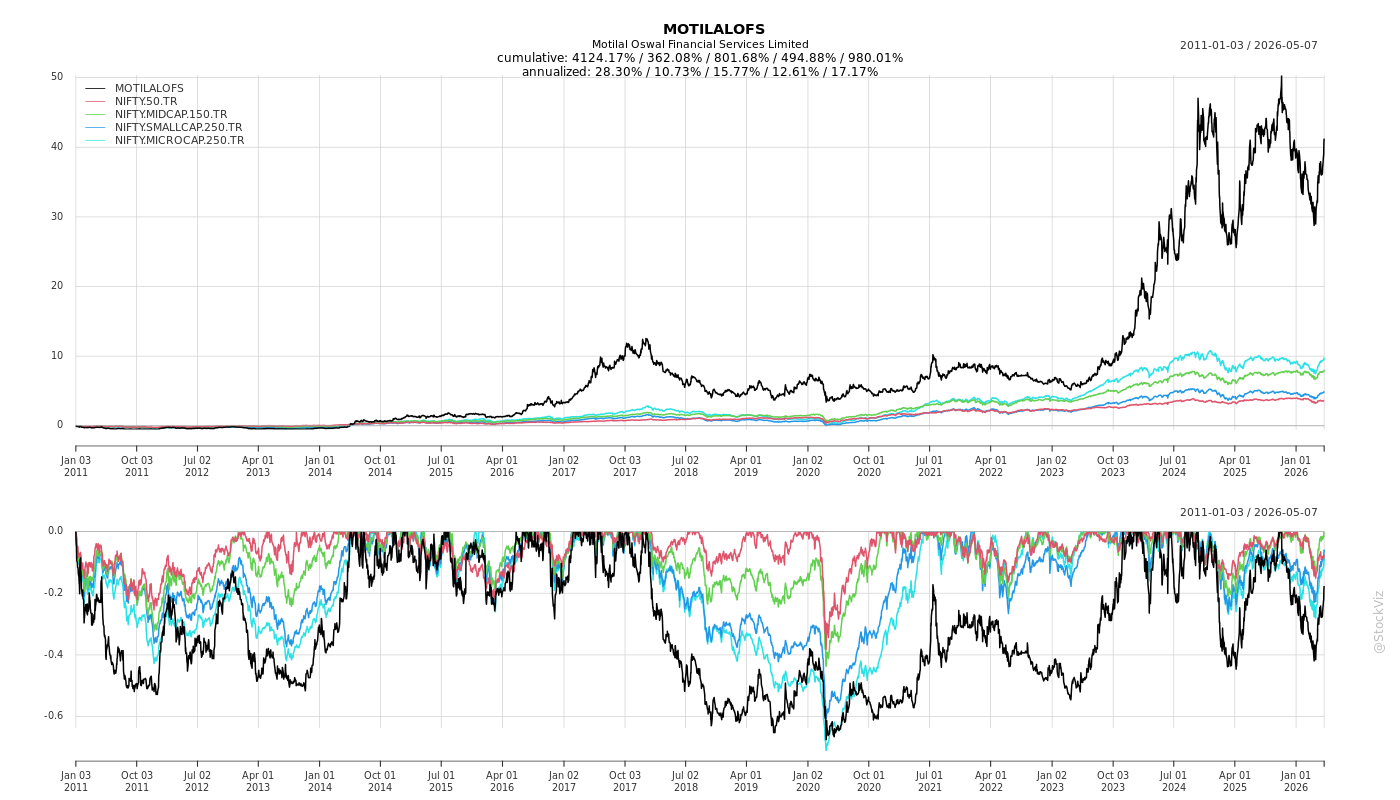

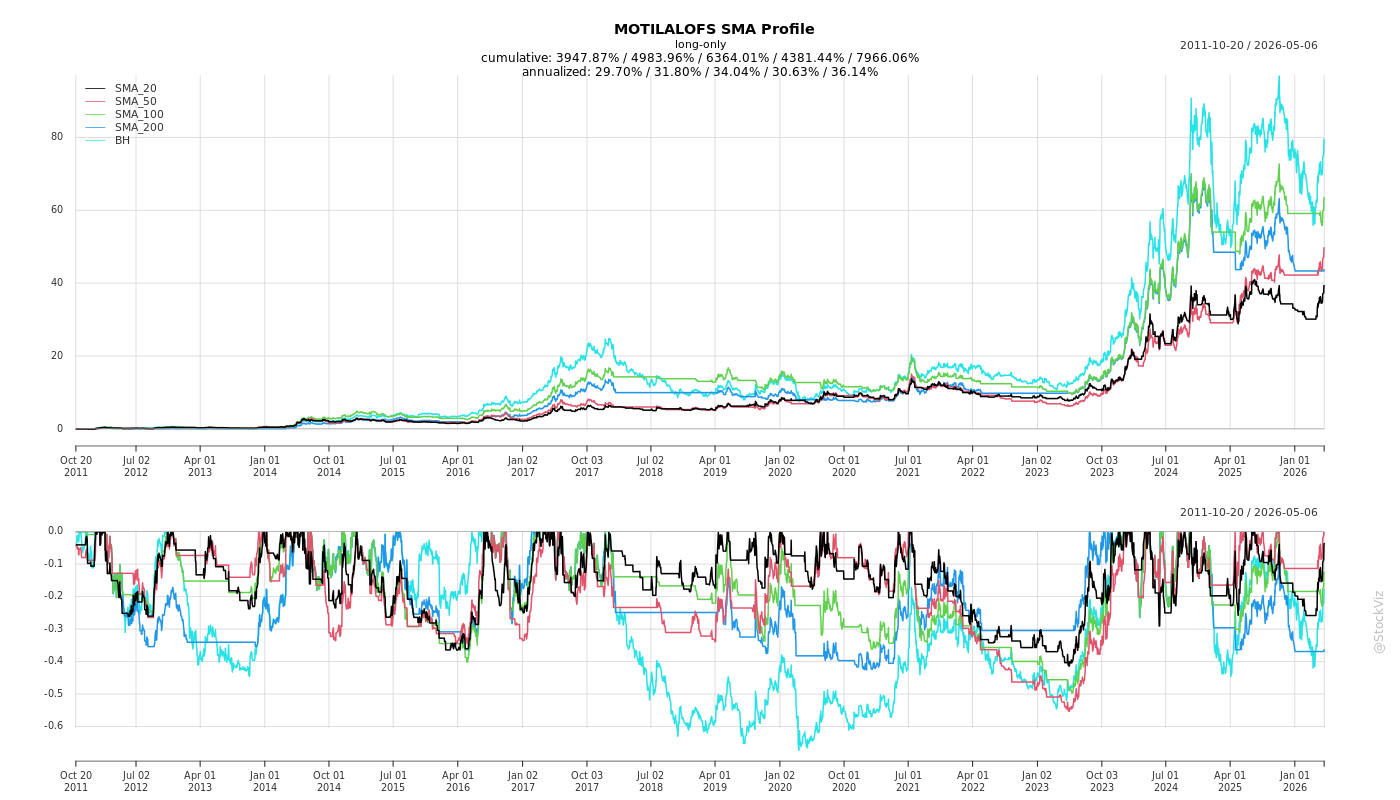

Cumulative Returns and Drawdowns

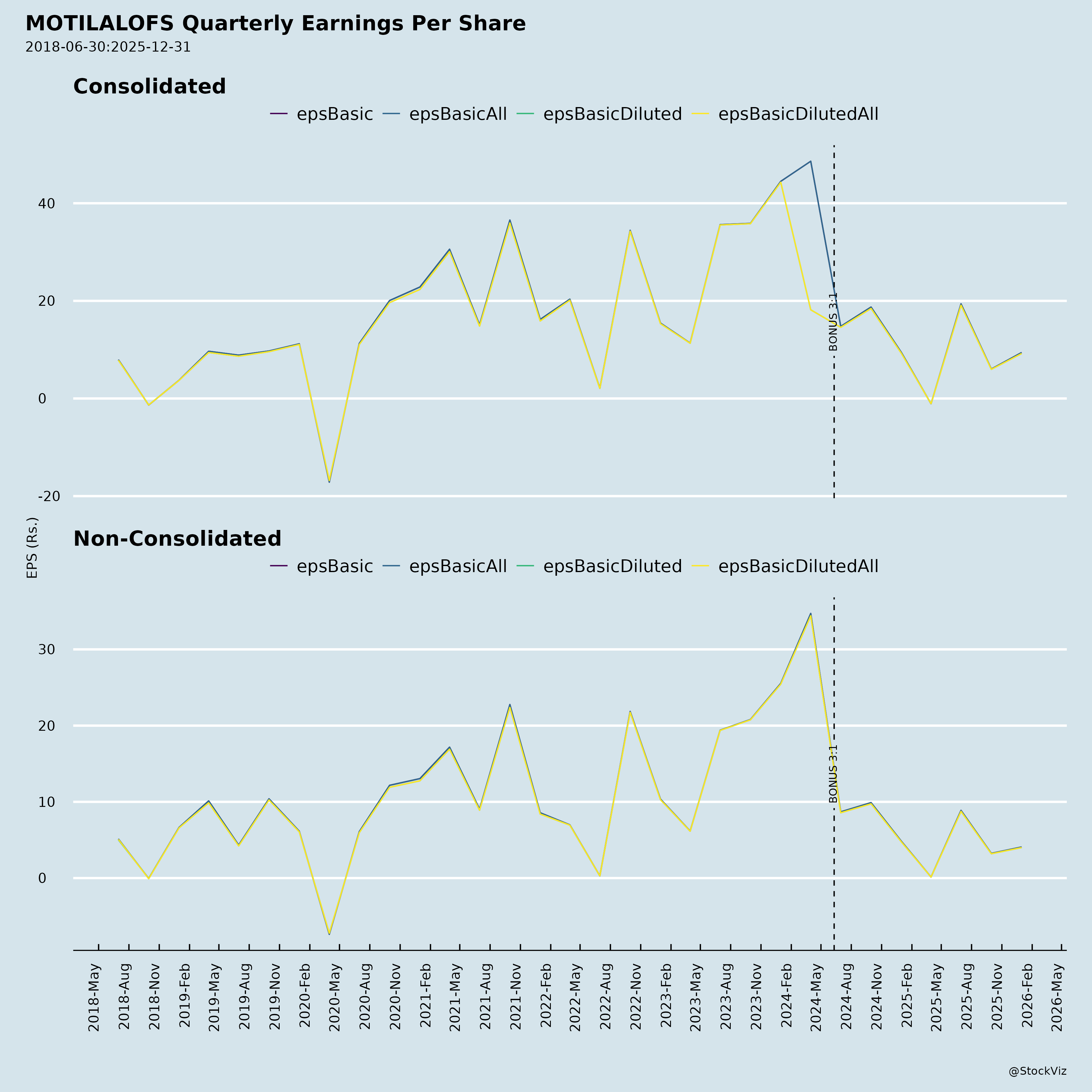

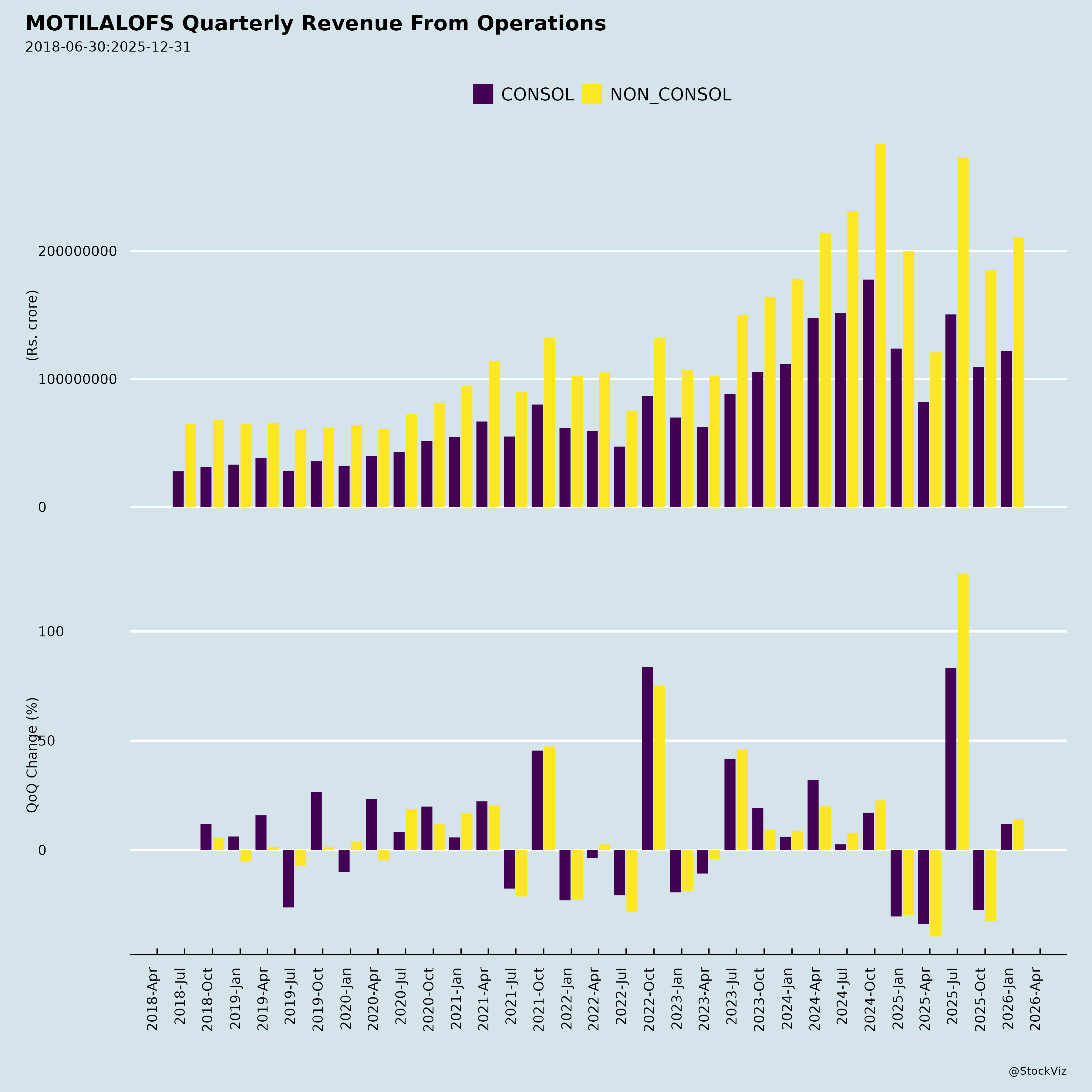

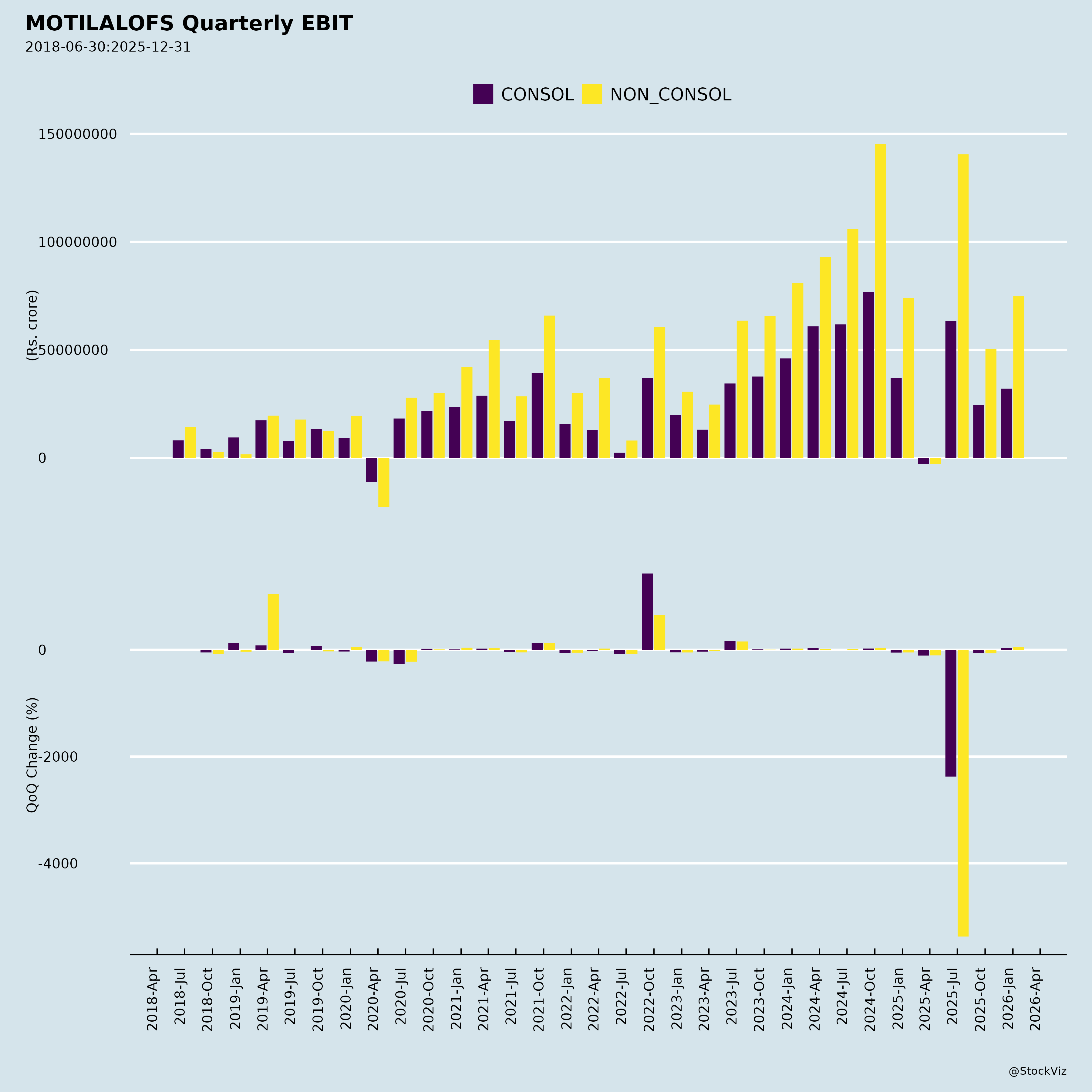

Fundamentals

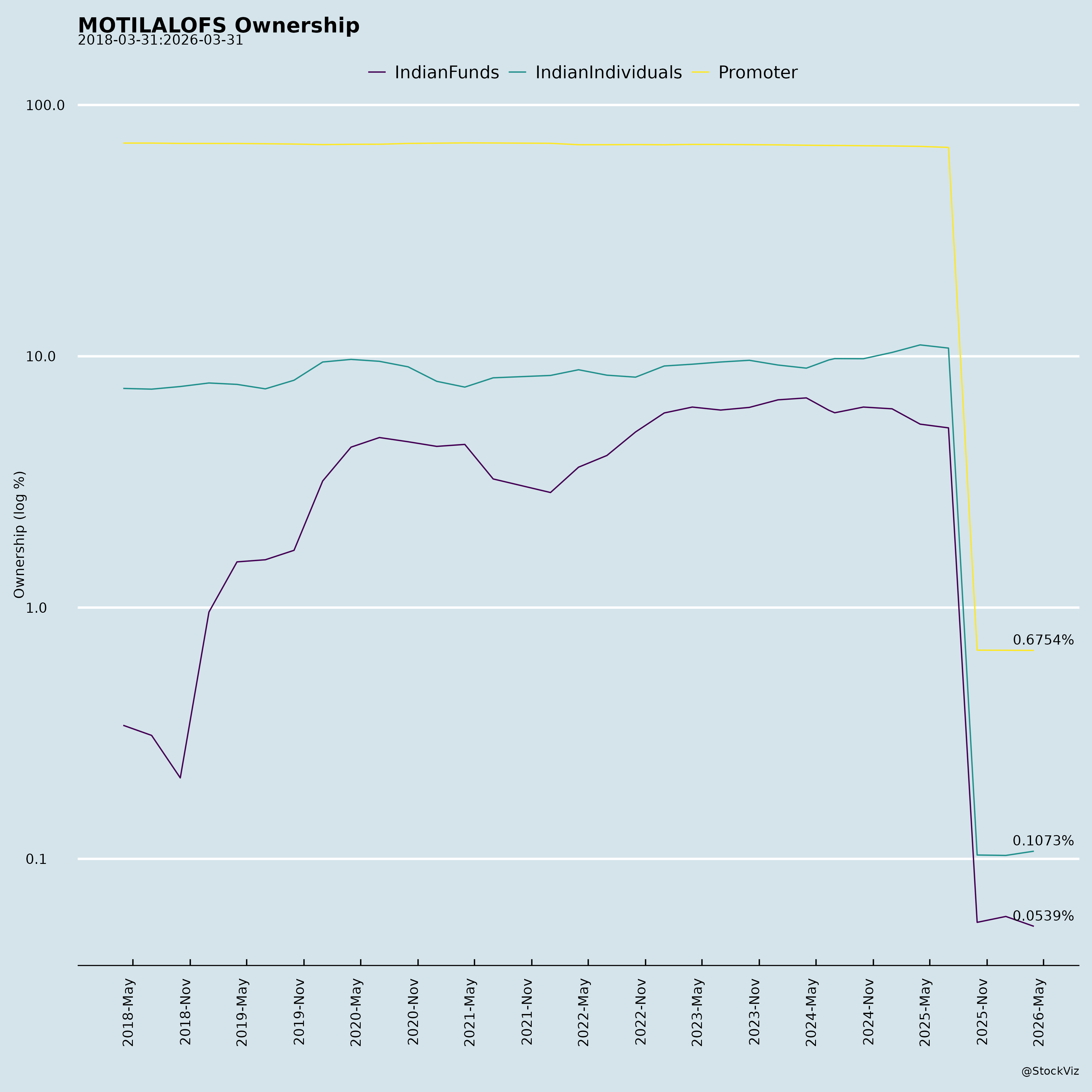

Ownership

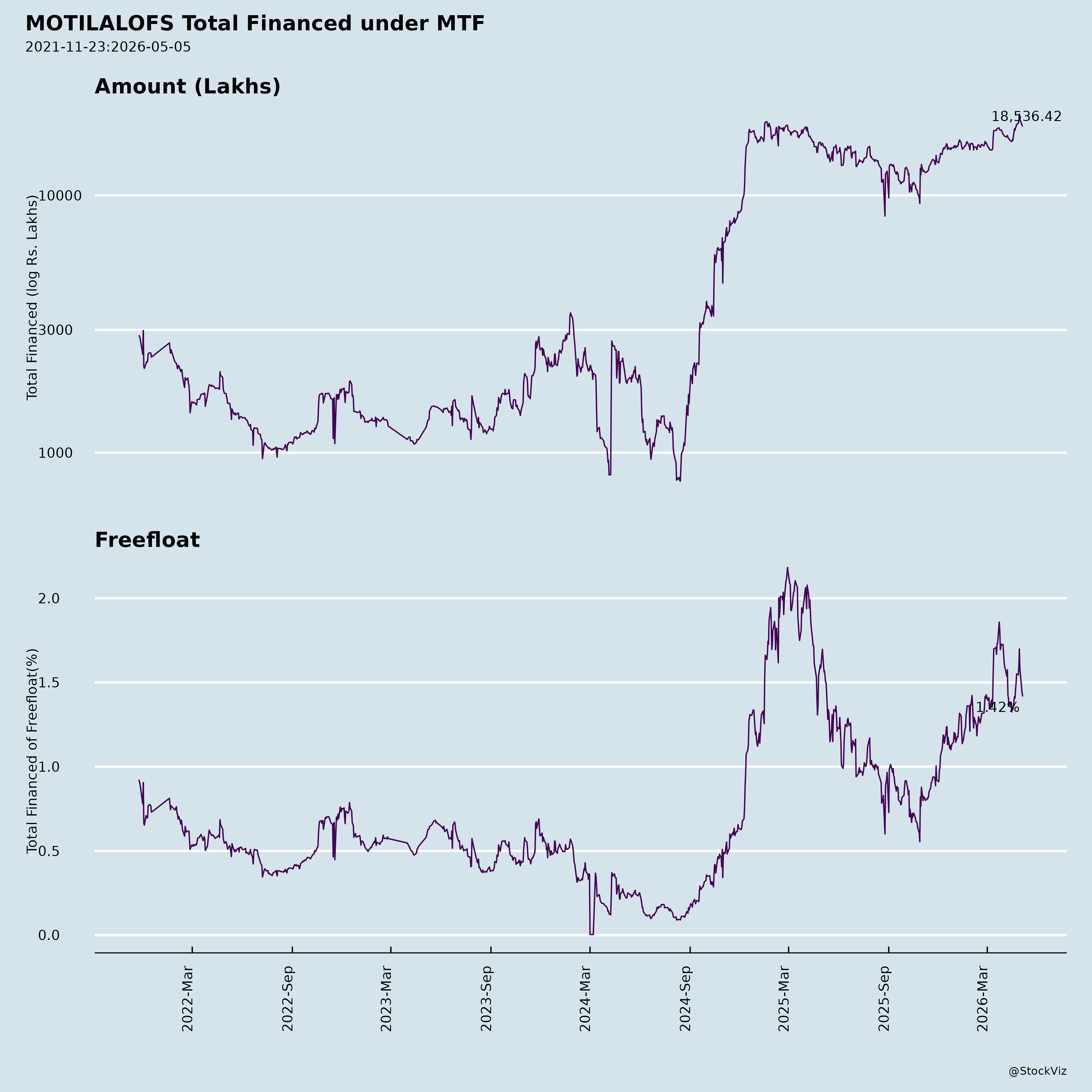

Margined

AI Summary

asof: 2025-12-03

Analysis of Motilal Oswal Financial Services Ltd. (MOTILALOFS)

Overview: MOTILALOFS reported resilient H1FY26 results (ended Sep 30, 2025) with record operating PAT of ₹1,088 Cr (+11% YoY), driven by annuity segments (Asset Management, Private Wealth). Consolidated total income was ₹4,604 Cr (down 11% YoY due to softer trading volumes), PAT ₹1,518 Cr (+46% adjusted for MTM). AUA/AUM ~₹6.8 lakh Cr, client base 14.5 Mn. Balance sheet strong (net worth ₹12,871 Cr, up ~10x in 10 years), but ops cash flow negative on loan growth. Recent actions include board refresh (next-gen promoters + independents), NCD raise (₹500 Cr), minor SEBI settlement (₹34.85 lakh, no guilt admission).

Tailwinds (Positive Catalysts)

- Annuity Revenue Dominance: 70%+ revenue from recurring streams (Asset Mgmt PAT +46% YoY to ₹180 Cr, AUM +46% to ₹1.77 lakh Cr; Private Wealth +23% PAT, AUM +19%; Housing Finance +27% PAT, disbursals +48%).

- Market Leadership: #1 in IPOs/QIPs/rights (H1); 8% blended ADTO share, 7-9% in cash/F&O premium; SIP inflows +2.2x YoY (₹4,172 Cr).

- Strong Fundamentals: 31% PAT CAGR (decade), 22% avg ROE, 20% payout (3 buybacks, no equity dilution). Treasury XIRR 18.7% (AUM +14% YoY).

- Rating & Capital Access: ICRA upgrade to AA+ (highest for cap markets firm); Crisil/India Ratings AA+/A1+; NCD raise ₹500 Cr fully utilised.

- Governance/Expansion: Board strengthened (Pratik Oswal, Vaibhav Agrawal for next-gen; Conrad D’Souza, Ashok Kothari for expertise). New IFSC subs (e.g., MOAM IFSC); 550+ cities reach.

Headwinds (Challenges)

- Trading Volatility: Wealth Mgmt PAT -24% YoY; Q2 revenue -35% YoY on lower volumes (Capital Markets flat despite ECM lead).

- Margin Pressures: Employee costs +23% YoY; finance costs stable but impairment up (₹52 Cr). Op margin dipped to 34% (H1).

- Cash Flow Strain: Ops cash flow -₹2,345 Cr (H1) on loan book +28% (₹13,539 Cr), working capital drag (receivables down but payables -).

- Regulatory Noise: SEBI settlement on AP lapses (front-running probe); corrective steps taken, but compliance scrutiny in broking.

- Talent Transition: Group CMO resignation (personal reasons); potential short-term marketing impact.

Growth Prospects (High Confidence, Multi-Year)

- Asset/Wealth Scaling: MF net sales share 8.2%; alternates (IBEF V ₹6,900 Cr first close); PMS/alternates AUM ₹10,000 Cr; target 30-40% CAGR via ETFs/index funds, SIPs.

- Housing Finance: AUM +24% YoY (₹5,236 Cr); disbursals +48%; granular retail focus.

- Cap Markets/Distribution: ECM dominance; distribution book +34% CAGR to ₹40,544 Cr; net flows +29%.

- Treasury Leverage: Reinvest op profits (42% CAGR); equity-based, resilient to rates.

- Structural: 13K+ employees, digital push (Fintech exposure via promoters), IFSC/Gift City expansion. AUA +10-15% CAGR feasible; ROE 20%+ sustainable.

Key Risks (Moderate, Mostly Mitigable)

| Risk Category | Description | Mitigation |

|---|---|---|

| Regulatory/Compliance | Front-running probes, AP lapses; SEBI scrutiny on brokers. | Sensitization done; no guilt admission; strong ratings. |

| Market/Cyclical | Volatility in trading vols (80% revenue cyclical); equity MTM swings. | Annuity shift (70% recurring); treasury hedges. |

| Liquidity/Funding | Negative ops CF; debt/equity 1.15x; NCD reliance. | Asset cover 1.2x+; ratings support cheap funding. |

| Concentration | Promoter family (next-gen entry); Wealth/Cap Mkts exposure. | Independent directors added; diversified AUM. |

| Competition/Execution | Intense in AMCs/wealth (HDFC, Zerodha); talent retention. | Niche leadership (ETFs, alternates); board refresh. |

| Macro | Rate hikes (finance cost 25% expenses); equity corrections. | Fixed-rate treasury; granular lending. |

Investment Summary: Bullish Long-Term. Tailwinds from annuity growth, governance outweigh headwinds (volatility, CF). Prospects strong (20%+ PAT CAGR feasible). Risks regulatory/market-driven but low-impact (minor settlement, MTM-adjusted PAT robust). Hold/Buy on dips; target 25-30x FY27 EPS (~₹80-90). Monitor Q3 vols, CF normalization.

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.