Stockbroking & Allied

Industry Metrics

May 8, 2026

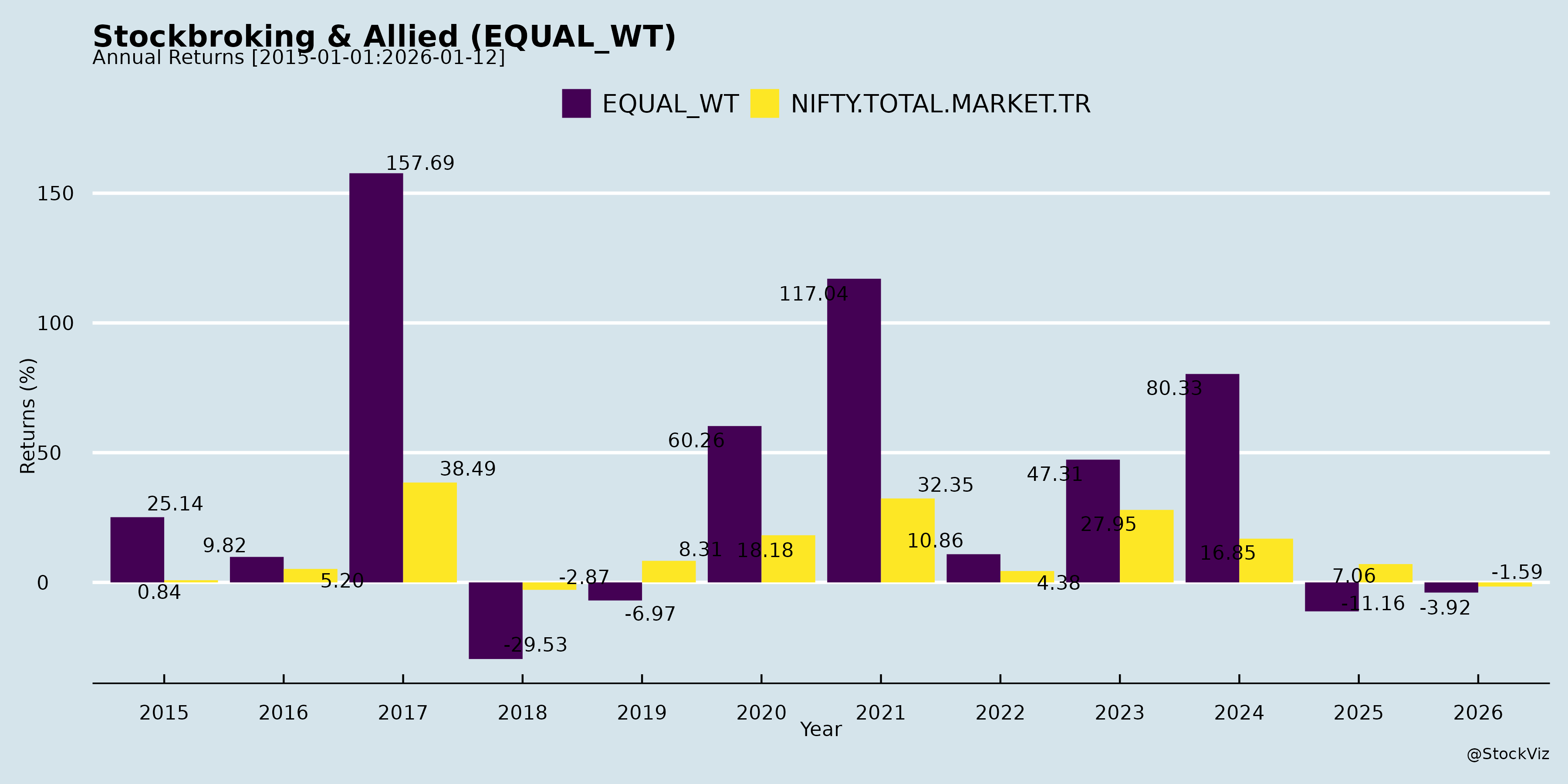

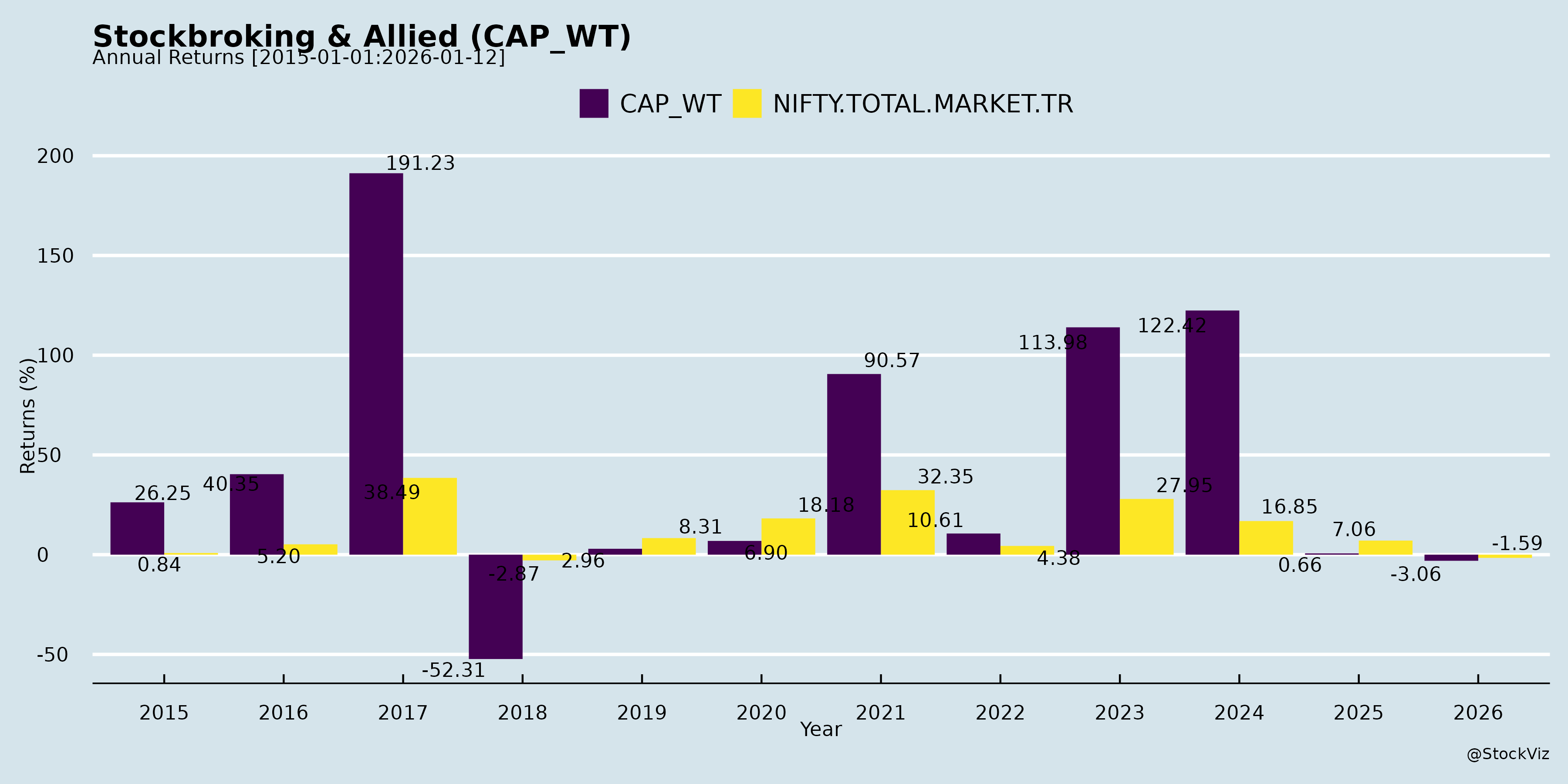

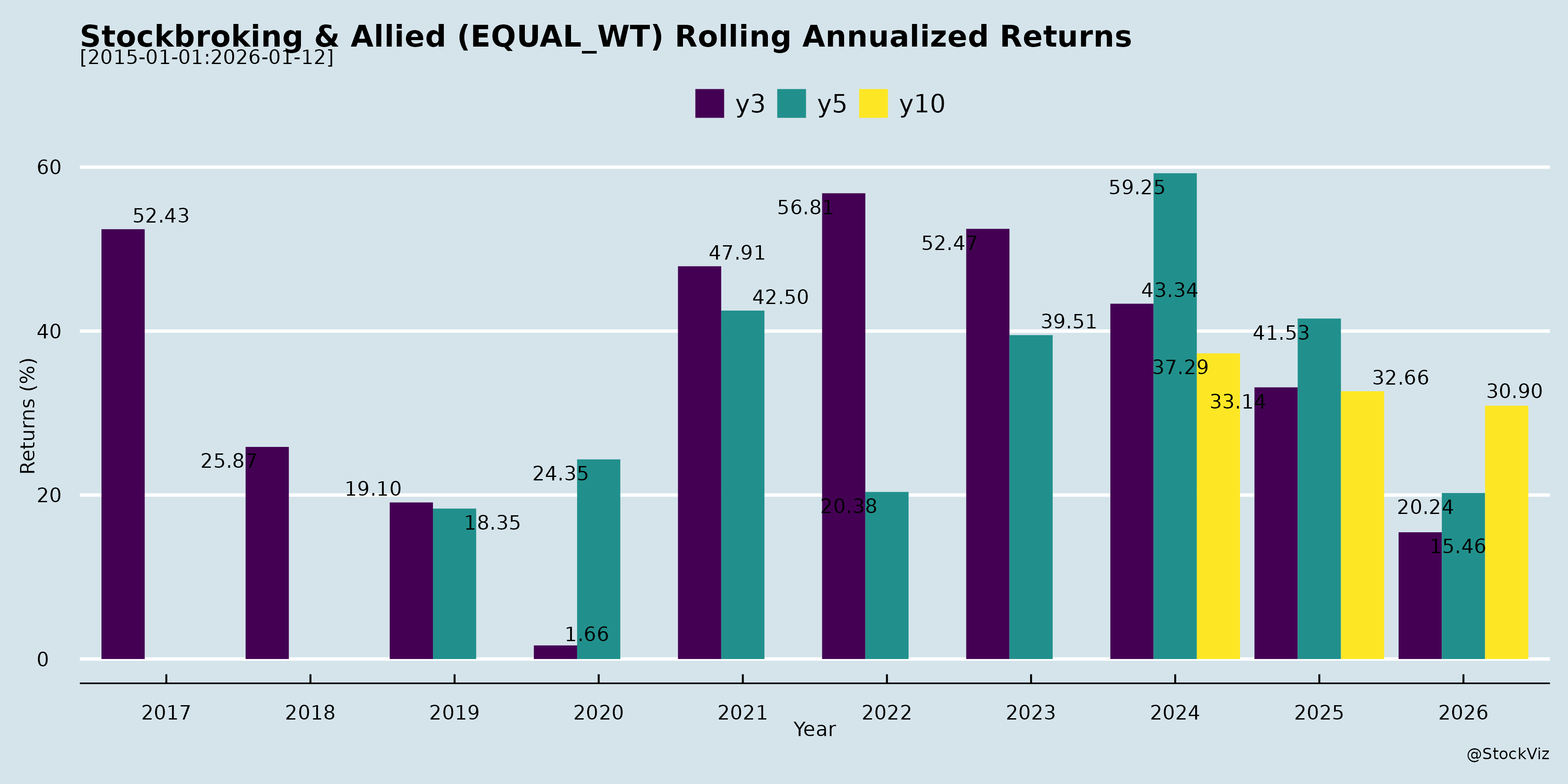

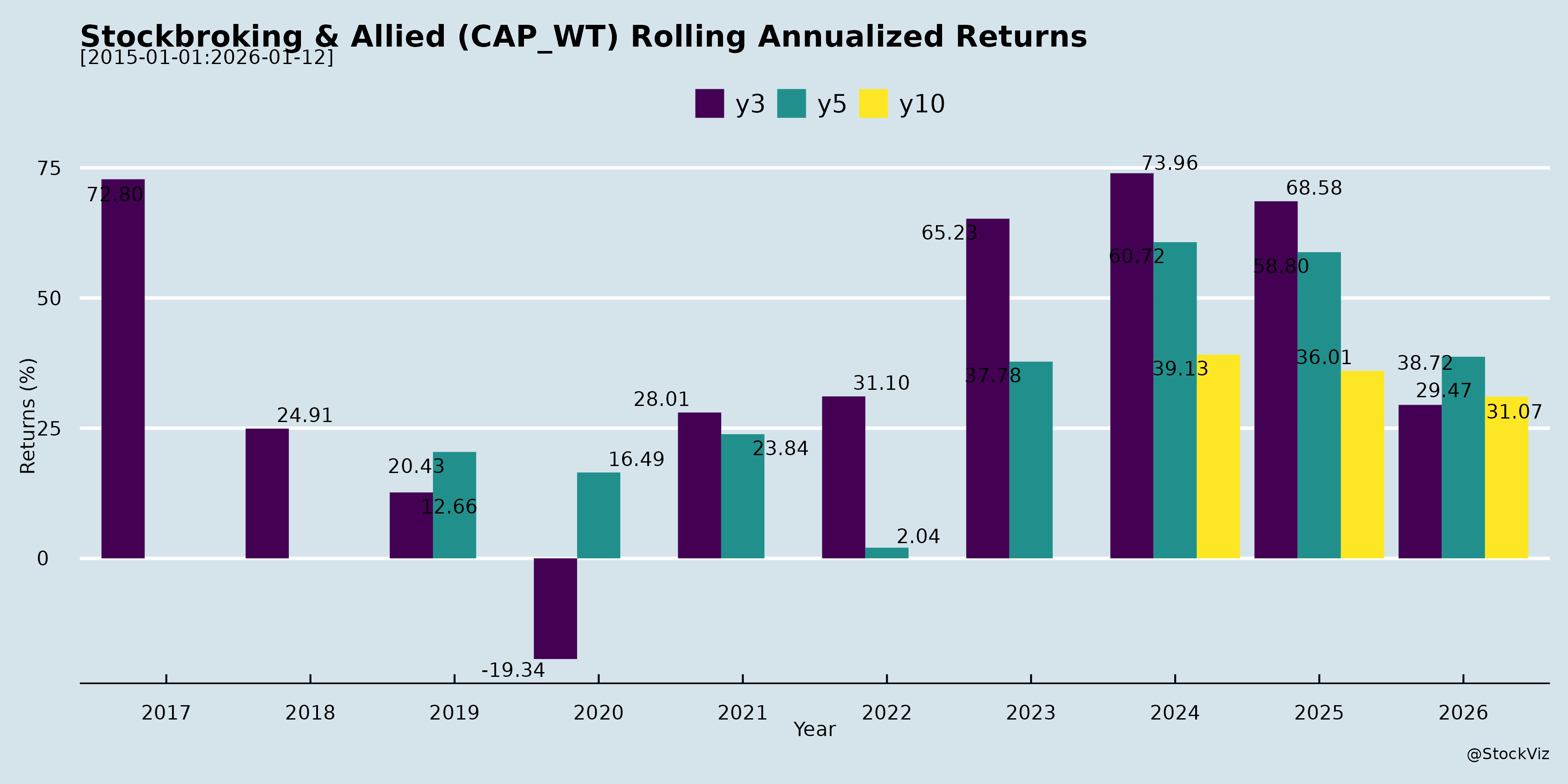

Annual Returns

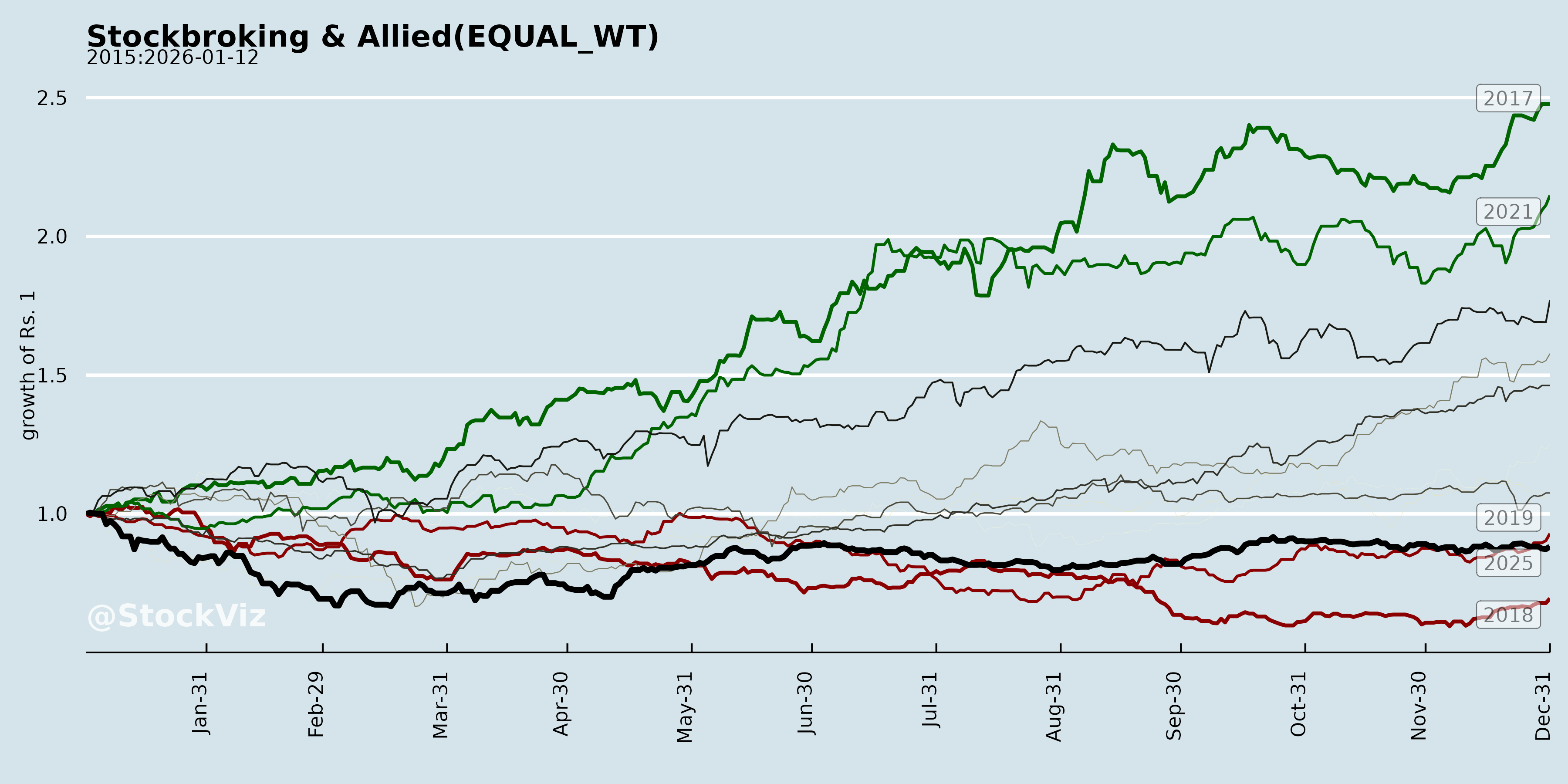

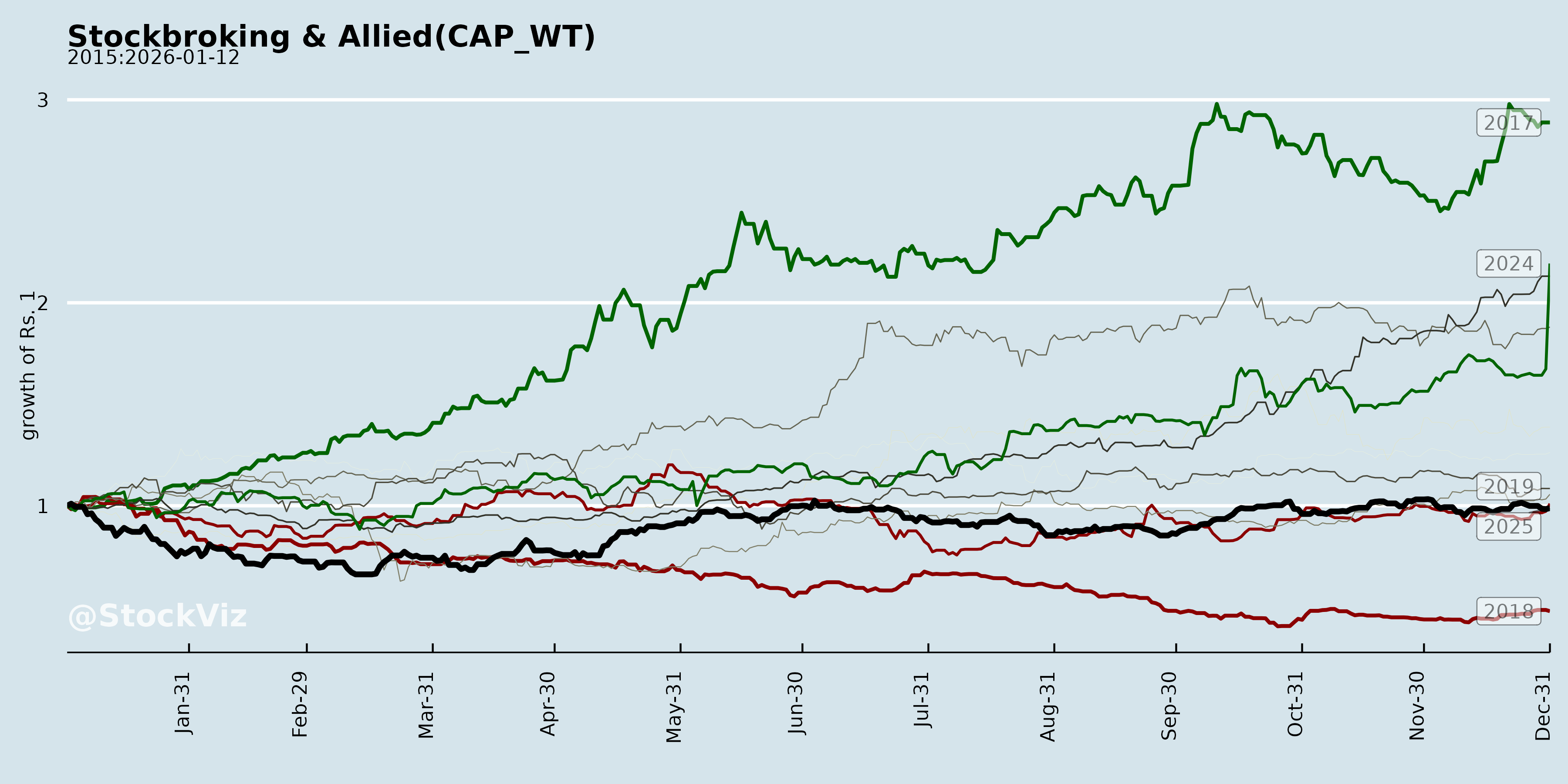

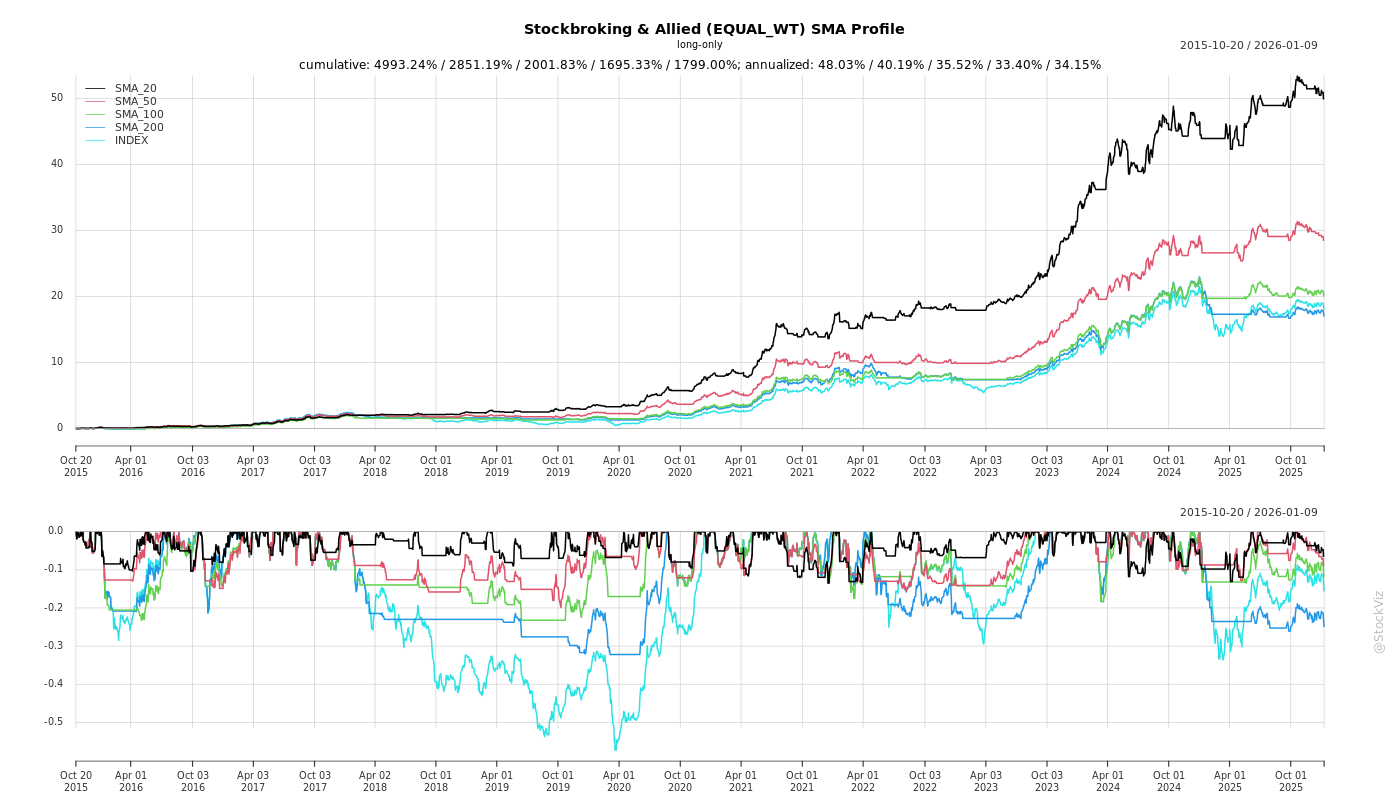

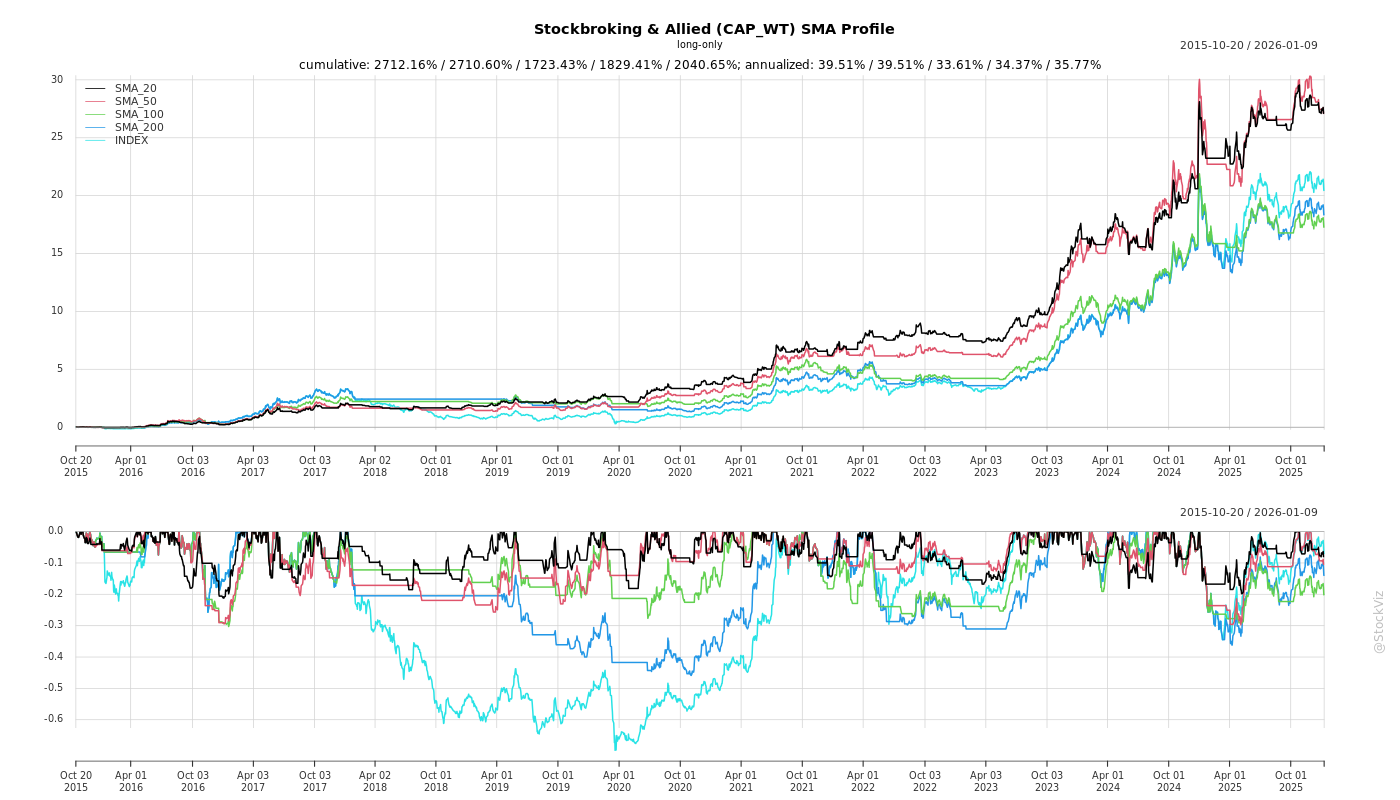

Cumulative Returns and Drawdowns

SMA Scenarios

Current Distance from SMA

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-15

The financial services and broking industry has undergone a profound transformation over time, evolving from traditional, manual operations into highly digitized, technology-driven ecosystems. This evolution has generated significant new opportunities, particularly in wealth management and algorithmic trading, while simultaneously introducing complex challenges in human capital, regulatory compliance, and operational resilience.

Here is a detailed breakdown of how these opportunities and challenges have evolved:

The Evolution of Opportunities * Shift from Traditional Broking to Fintech: The industry has structurally shifted from manual, dealer-driven, and transaction-dependent models to API-driven fintech platforms [1]. This evolution has enabled companies to generate more recurring and annuity-based income through proprietary strategies, low-latency execution, and subscriptions [1]. * Rise of Algorithmic Trading: Algorithmic trading has seen massive adoption. Prior to 2010, the Indian equity markets were largely dominated by manual trading [2]. Between 2010 and 2015, institutional investors began adopting execution-focused algorithms [2]. Post-2020, the landscape evolved again with the introduction of plug-and-play platforms utilizing AI and Machine Learning, allowing retail and High Net-Worth Individuals (HNIs) to deploy rule-based, emotion-free strategies at scale [2, 3]. * The “Financialization” of Household Savings: There is a massive structural opportunity as Indian households increasingly move their savings into capital markets. India is projected to become the world’s fourth-largest private wealth market by 2028 [4, 5]. Mutual fund Assets Under Management (AUM) are expected to compound at a 16-18% CAGR, and the total gross savings opportunity in India is projected to grow from USD 13.5 trillion to USD 47 trillion by 2042 [5, 6]. * Growth in Alternate Assets and Insurance: The alternative investment industry is expected to grow fivefold over the next decade, with the HNI share in alternates projected to increase from 15% to 25% [7]. Additionally, India’s underpenetrated insurance market offers significant multi-year premium growth potential as awareness of health, protection, and retirement planning rises [5]. * Geographic Expansion: Expanding distribution networks into non-metro cities has become a major opportunity to unlock large, untapped pools of wealth [5, 8].

The Evolution of Challenges * Human Capital and Retention: As the industry scales, retaining talent and managing costs have become major hurdles. For instance, overall employee attrition hit 47.6% (and 70.9% for frontline staff) in FY2025 at one major firm [9]. The wealth management space, in particular, is facing intense recruitment competition, leading to rising employee costs that can pressure operating profits [10, 11]. There are also ongoing challenges related to wage gaps and gender diversity at senior decision-making levels [12, 13]. * Operational and IT Risks: Because the modern broking business is highly reliant on real-time, high-volume IT systems, firms are inherently exposed to vulnerabilities like technical glitches and cyber disruptions [13-15]. Companies are forced to make heavy investments in IT infrastructure and cybersecurity to mitigate these systemic risks [15]. * Regulatory Scrutiny and Compliance: The surge in transaction volumes has made the industry more prone to operational penalties, such as margin-related lapses and reporting mismatches [15]. Additionally, regulators are strictly monitoring new technological offerings; for example, SEBI recently examined over 120 stock brokers whose platforms allegedly promised guaranteed returns or consistent profits through algorithmic strategies, leading to a targeted settlement scheme for these violations [16]. * Customer Grievances: The scale of digital adoption has occasionally strained customer service. Firms have experienced significant year-over-year spikes in customer complaints (e.g., a ~46% increase in FY2025), forcing them to shift from detective models to preventive, multi-layered control approaches to protect consumers [14, 17]. * Macroeconomic Volatility: The industry remains vulnerable to global trade uncertainties, geopolitical tensions, and broader market volatility [18, 19]. These macroeconomic factors can lead to FII outflows, moderation in client funding books, and delays in executing robust IPO mandates [19-22].

What are the headwinds affecting this industry?

asof: 2026-04-15

The financial services, broking, and wealth management industry is currently facing several significant headwinds spanning macroeconomic pressures, operational vulnerabilities, regulatory risks, and human resource challenges:

Macroeconomic and Market Volatility The sector has been heavily impacted by a softer macro environment, geopolitical tensions, and shifting global trade dynamics, which have clouded the industry’s external outlook [1-4]. These challenges, compounded by sustained Foreign Institutional Investor (FII) outflows and subdued investor sentiment, have caused a noticeable moderation in cash market shares and client funding books [3, 4]. Unfavorable and volatile market conditions have temporarily slowed business momentum, with the broking industry experiencing a decline of up to 30% in trading volumes during certain periods [5, 6].

Fundraising and Capital Market Delays For merchant banking and institutional equities, the fund-raising environment has become highly selective and challenging due to deep nervousness in the small and midcap segments, alongside overarching domestic and global macroeconomic uncertainties [7]. This inherent market volatility has actively caused delays for several existing IPO and capital market mandates [8].

Operational and IT Vulnerabilities Because the broking and wealth management industry relies heavily on high-volume, real-time IT systems to function, it is inherently exposed to risks associated with IT resilience, technical glitches, and system disruptions [9-11]. Companies are vulnerable to systemic technical breakdowns and face an ongoing threat from a rise in cybersecurity incidents, necessitating continuous, heavy investments in IT infrastructure and cybersecurity controls [11, 12].

Regulatory Scrutiny and Compliance Risks Broking operations are highly prone to regulatory fines and operational penalties, such as those stemming from margin-related lapses, reporting mismatches, and other procedural errors tied to managing high transaction volumes [11-13]. Furthermore, the industry faces strict regulatory crackdowns regarding misleading practices. For example, SEBI has recently scrutinized and initiated settlement schemes for stock brokers whose Application Programming Interfaces (APIs) were integrated with algorithmic trading platforms that improperly promised guaranteed returns or consistent profits [14, 15].

Talent Acquisition, Attrition, and Rising Costs The wealth management space is intensely competitive, leading to industry-wide recruitment challenges and severe frontline attrition [16, 17]. Some firms have reported overall attrition rates near 48%, with frontline sales attrition spiking as high as ~71%, which disrupts workforce stability and elevates conduct-risk exposure [18, 19]. Additionally, surging employee costs—driven by increased headcount, higher variable payouts, and one-time labor code provisions—coupled with rising IT and marketing expenses, have heavily impacted operating profitability across various firms [20-22].

ESG and Governance Constraints Certain industry players are navigating Environmental, Social, and Governance (ESG) headwinds. Key issues include an absence of time-bound environmental targets, a lack of renewable energy infrastructure, and significant wage disparities [23, 24]. For example, audits have noted female-to-male wage gaps, high ratios between executive and median employee pay, and an ongoing need to deepen gender diversity at senior, decision-making levels [10, 24].

What are the key things to understand about this industry?

asof: 2026-04-15

Comprehensive Ecosystem Beyond Traditional Broking The financial services and broking industry has evolved far beyond simple stock execution. Firms now operate as integrated conglomerates offering a vast spectrum of services under one roof, including wealth management, asset management, investment banking (such as IPOs, QIPs, and M&A advisory), portfolio management services (PMS), alternate investment funds (AIF), margin trading facilities (MTF), and even e-governance solutions like PAN and NPS facilitation [1-5]. To combat the cyclicality of transaction-dependent revenues, companies are shifting toward platform-based, subscription-led, and interest-led revenue models, which provide higher recurring and annuity income [6, 7].

Technological Transformation and the Dominance of Algo-Trading Technology is arguably the most critical differentiator in the modern capital markets. There is a massive shift toward Application Programming Interfaces (APIs) and algorithmic trading, with automated, systematic execution accounting for approximately 70% of executed volumes [8]. Firms are heavily investing in low-latency infrastructure, AI-powered robo-advisory platforms, and quantitative strategy development to offer clients emotion-free, data-driven trading [3, 8-10]. Digital platforms have also streamlined client onboarding through paperless KYC, significantly lowering customer acquisition costs and allowing firms to scale rapidly [3, 11].

Inherent IT Vulnerabilities and Cybersecurity Risks Because the industry is highly reliant on IT systems to handle high-volume, real-time transactions, it is inherently exposed to IT resilience risks [12]. Firms and their clients are frequently vulnerable to technical glitches and disruptions [12, 13]. To mitigate these risks, companies must maintain scalable hardware across global standard data centers, conduct regular cyber security audits, and adhere to regulatory cyber resilience frameworks [12, 14, 15].

Demographic Shifts: Retail Boom and Wealth Creation The industry is benefiting from major demographic tailwinds. There is rising retail investor participation driven by the “financialization of household savings” and increased demand for multi-asset trading [11]. Simultaneously, the private wealth segment is expanding rapidly. India is projected to become the 4th largest private wealth market globally by 2028, with the Total Addressable Market (TAM) for Wealth Management expected to grow at a mid-teen CAGR [16]. Firms are building dedicated networks of relationship managers to cater to High Net-worth Individuals (HNIs) and Ultra-HNIs [16, 17].

Stringent Regulatory Oversight and Risk Management Operating in this space requires navigating a complex and strict regulatory environment governed by bodies like SEBI and various stock exchanges [18, 19]. Key regulatory and risk factors include: * Real-time Risk Monitoring: Brokerages must deploy robust Pre-Trade and Post-Trade Risk Management Systems (RMS) to automatically validate margins and block trades that exceed exposure limits [20, 21]. * Surveillance and AML: Automated transaction monitoring is required to track suspicious activities related to Anti-Money Laundering (AML), market abuse, and insider trading [22]. * Penalties and Fraud: The industry is prone to operational lapses (e.g., margin-related errors or reporting mismatches), which frequently result in regulatory fines and penalties [13, 15]. Brokerages must also protect against severe financial crimes, such as fraudulent off-market transfers of shares from client Demat accounts [23, 24]. * Mis-selling Crackdowns: Regulators actively penalize non-compliance, such as the recent SEBI actions against stock brokers associated with algorithmic platforms that falsely promised guaranteed returns or consistent profits [25, 26].

Vulnerability to Market Cyclicality Despite technological advancements, the industry remains highly sensitive to macroeconomic conditions. Global trade uncertainties, shifting market sentiments, and financial market volatility directly impact operations [27, 28]. For instance, during market slowdowns, broking industries can experience trading volume declines of up to 30%, which underscores the importance of having a diversified business model (like wealth advisory and debt operations) to maintain stable revenues [29].

Research as a Core Value Driver Finally, deep fundamental and quantitative research acts as the backbone of client engagement. Firms differentiate themselves by offering bottom-up organizational analyses, macroeconomic perspective research, and quantitative studies on volatility and options data [30]. This in-house intellectual capital is vital for servicing diverse institutional client bases—ranging from mutual funds to foreign portfolio investors—and successfully executing investment banking mandates [31-33].

What are the tailwinds affecting this industry?

asof: 2026-04-15

The Indian financial services, wealth management, and capital markets industry is currently benefiting from a confluence of powerful structural, macroeconomic, and technological tailwinds. These growth drivers are reshaping how both retail and institutional investors participate in the markets.

Here is a detailed breakdown of the primary tailwinds propelling the industry forward:

Macroeconomic Growth and Regulatory Stability * Rapid Economic Expansion: India is projected to retain its position as the world’s fastest-growing major economy [1]. The macroeconomic environment remains stable with a positive bias, supported by historically low inflation, strengthening external financial buffers, and a fiscally prudent budget focused on capital expenditure (CAPEX) [2]. Furthermore, the RBI has confidently projected real GDP growth at 7.4% [2]. As India advances toward its aspiration of becoming a USD 35 trillion economy by 2047, the rapid economic development is directly expanding the financial sector [3]. * Favorable Regulatory Environment: The industry is benefiting from a constructive and forward-looking regulatory framework implemented by bodies like SEBI. Improved market transparency, well-defined risk controls, and regulatory stability are heavily boosting long-term capital formation and investor confidence [4-6].

The Financialization of Household Savings * Shift to Financial Assets: There is a massive structural shift underway known as the “financialization of savings,” wherein households are moving away from traditional physical assets into equities and mutual funds [1, 4, 7]. Over the long term, the allocation of savings into equities is projected to jump from 5% to 20%, while the Mutual Fund AUM-to-GDP ratio is expected to leap from 10% to 55% [7]. * Mutual Fund and Savings Growth: The household savings rate has the potential to rise to 2.7% by 2030 [3]. Driven by this financialization, Mutual Fund Assets Under Management (AUM) in India are expected to compound at a robust 16-18% CAGR [8].

Surging Wealth Creation and Demographic Expansion * Booming Private Wealth Market: India is on track to become the world’s 4th-largest private wealth market by 2028 [8, 9]. The strong performance of the capital markets is accelerating wealth creation and drastically increasing individual participation in financial assets [8]. * Untapped Non-Metro Markets: Wealth management and broking firms are finding a massive, previously untapped pool of savings by expanding their reach into Tier-2 and other non-metro cities [8, 10]. * Underpenetrated Insurance Sector: Alongside wealth creation, rising awareness of health, protection, and retirement planning within an underpenetrated insurance market offers significant multi-year premium growth opportunities for financial distributors [8].

Digitization and Exponential Retail Participation * Digital Platforms: The rise of digitization has fundamentally transformed client acquisition. Digital platforms and instant onboarding (e.g., Quick EKYC) have drastically lowered the cost of acquiring customers while vastly improving scalability for brokers [4, 11]. * Surging Demat and SIP Accounts: The industry is witnessing an exponential rise in retail participation, evidenced by aggressive additions of Demat accounts and highly consistent Systematic Investment Plan (SIP) flows, which signal a long runway for sustained growth [12]. Furthermore, consistent mass-media and digital outreach—such as the “Mutual Fund Sahi Hai” campaign—have successfully built foundational trust among retail investors [8].

Evolution of Trading Infrastructure and Algorithmic Adoption * Growth in Derivatives & Multi-Asset Trading: There is tremendous growth in equity derivatives, options trading volumes, and demand for multi-asset trading [4]. * Rise of Algorithmic Trading: The rapid volume growth in derivatives demands speed, precision, and systematic execution [5]. Consequently, the industry is seeing a massive shift toward rule-based, emotion-free algorithmic trading [5]. This is being enabled by major technological advances in exchange infrastructure, including low-latency systems, co-location facilities, and robust matching engines [5]. Retail and High Net-Worth Individual (HNI) investors can now easily access these capabilities through “plug-and-play” algorithmic platforms [5].

Explosive Growth in Alternative Assets and Primary Markets * Rise of Alternates (PMS & AIFs): Alternative assets are growing at twice the pace of mutual funds, driven by HNIs and Ultra-HNIs seeking superior returns and customized portfolio diversification [3]. The Portfolio Management Services (PMS) and Alternative Investment Fund (AIF) industry has expanded at a ~33% CAGR over the last decade and is projected to surge past INR 100 trillion by 2030 [3]. Overall, India’s Alternates AUM is expected to grow fivefold, reaching $2 Trillion by 2034 [13]. * Robust IPO Pipeline: A highly active primary market acts as a major catalyst for merchant banking and institutional equities divisions. India’s IPO cycle is exceptionally strong, with hundreds of upcoming filings proposing to raise trillions of rupees, indicating a deep confidence in the market’s capacity to absorb new capital issuances [4, 14].

What is the general outlook of this industry?

asof: 2026-04-15

The general outlook for the financial services and capital markets industry is highly optimistic, underpinned by strong macroeconomic tailwinds, technological advancements, and a structural shift in how wealth is managed and created.

Macroeconomic Growth and Wealth Creation India is currently positioned as the world’s fastest-growing major economy, experiencing an “economic take-off.” The nation’s GDP is projected to grow from USD 3.9 trillion to an estimated USD 17 trillion by 2042 [1]. The Reserve Bank of India (RBI) has signaled confidence in domestic demand by raising its real GDP growth projection to 7.4%, supported by historically low inflation, improving labor markets, and strong fiscal policies [2, 3].

Driven by this economic expansion, India is set to become the world’s 4th-largest private wealth market by 2028 [4, 5]. The Total Addressable Market (TAM) for wealth management features approximately INR 240 trillion in investible wealth and is expected to grow at a mid-teen Compound Annual Growth Rate (CAGR) [6]. The number of High Net-Worth Individuals (HNWIs) in India is projected to grow from 85,698 in CY24 to 93,753 in CY28 [7], while households in the UHNI/HNI segments are expected to jump from 200,000 to 300,000 by FY2027 [5].

Financialization of Savings and Retail Participation A defining trend for the industry’s future is the accelerating financialization of household savings, which is shifting capital away from traditional physical assets and into equities and structured financial products [4, 8-10]. Currently, the market has a massive runway for growth, as only about 5% of savings are allocated to equities and retail participation stands at around 10% [9].

Digitization has radically lowered client acquisition costs and catalyzed exponential retail participation [8, 10]. The industry is witnessing a relentless rise in Systematic Investment Plan (SIP)

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.