KAKATCEM

Equity Metrics

May 8, 2026

Kakatiya Cement Sugar & Industries Limited

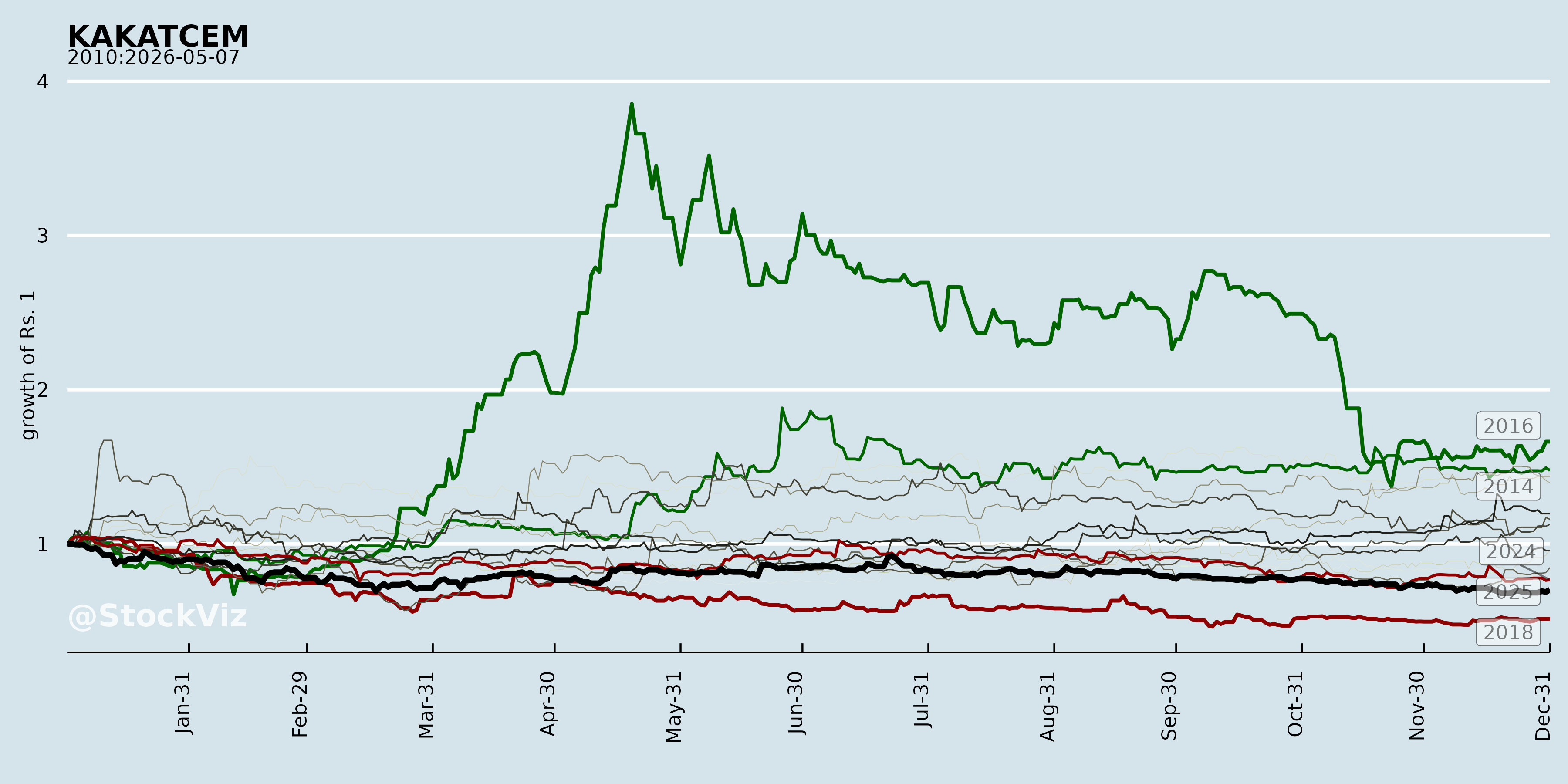

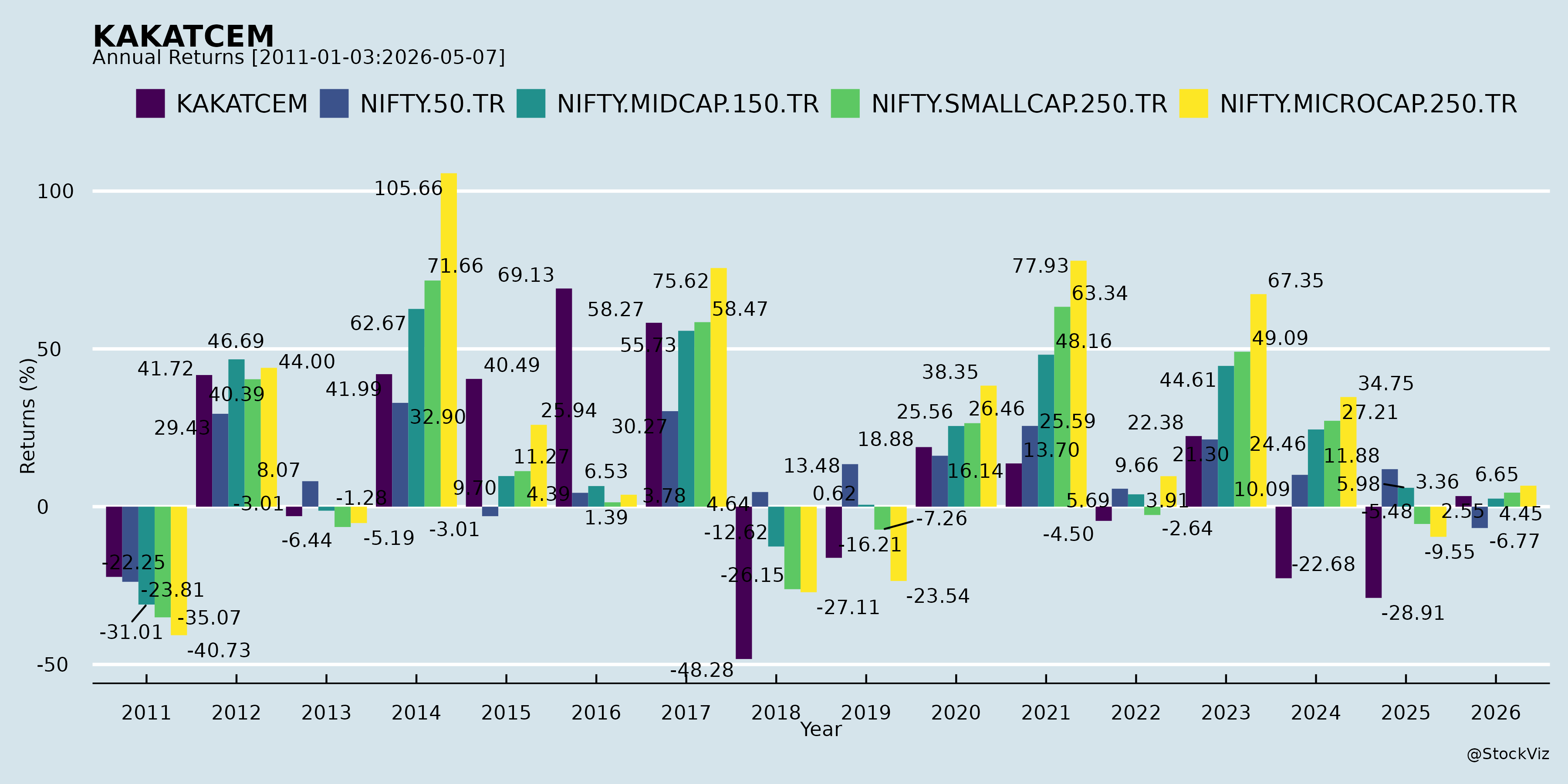

Annual Returns

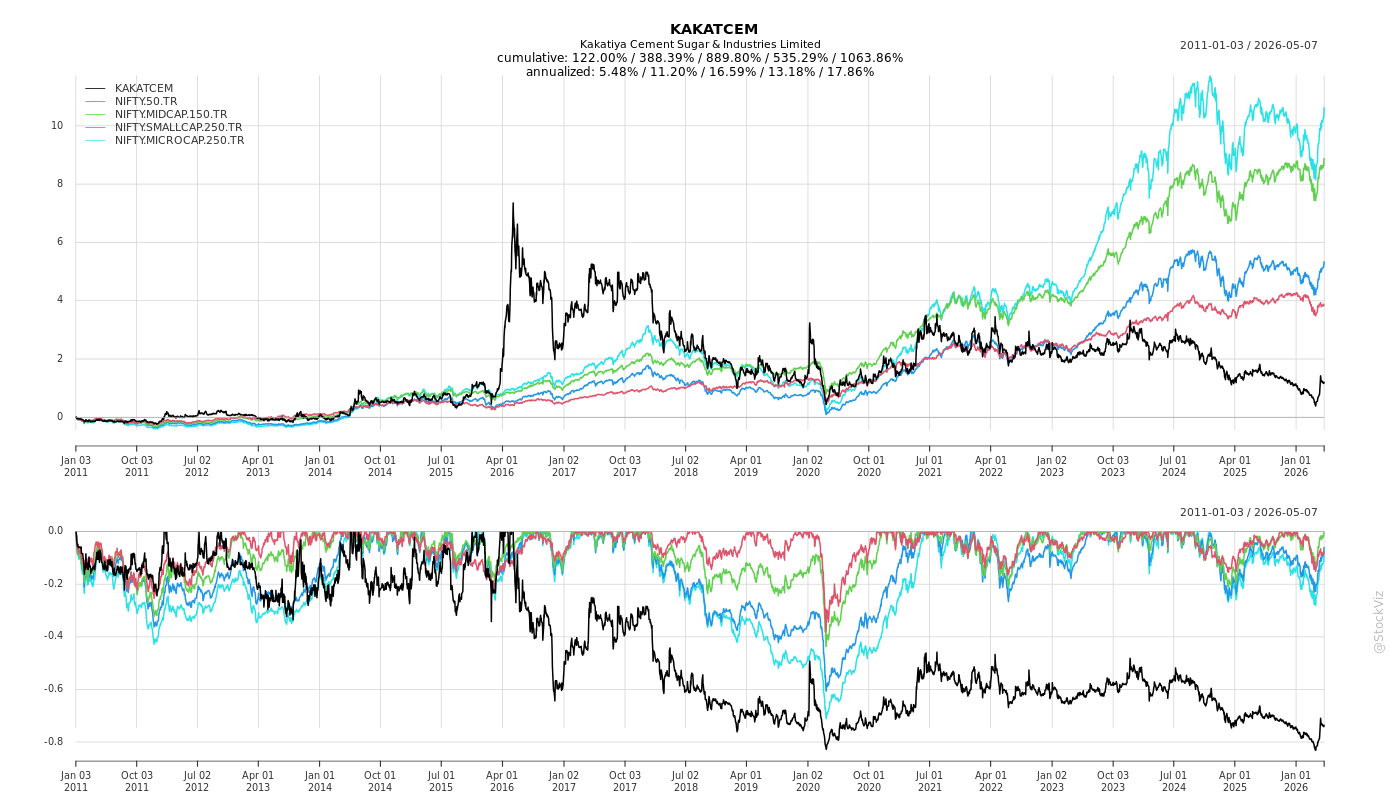

Cumulative Returns and Drawdowns

Fundamentals

Ownership

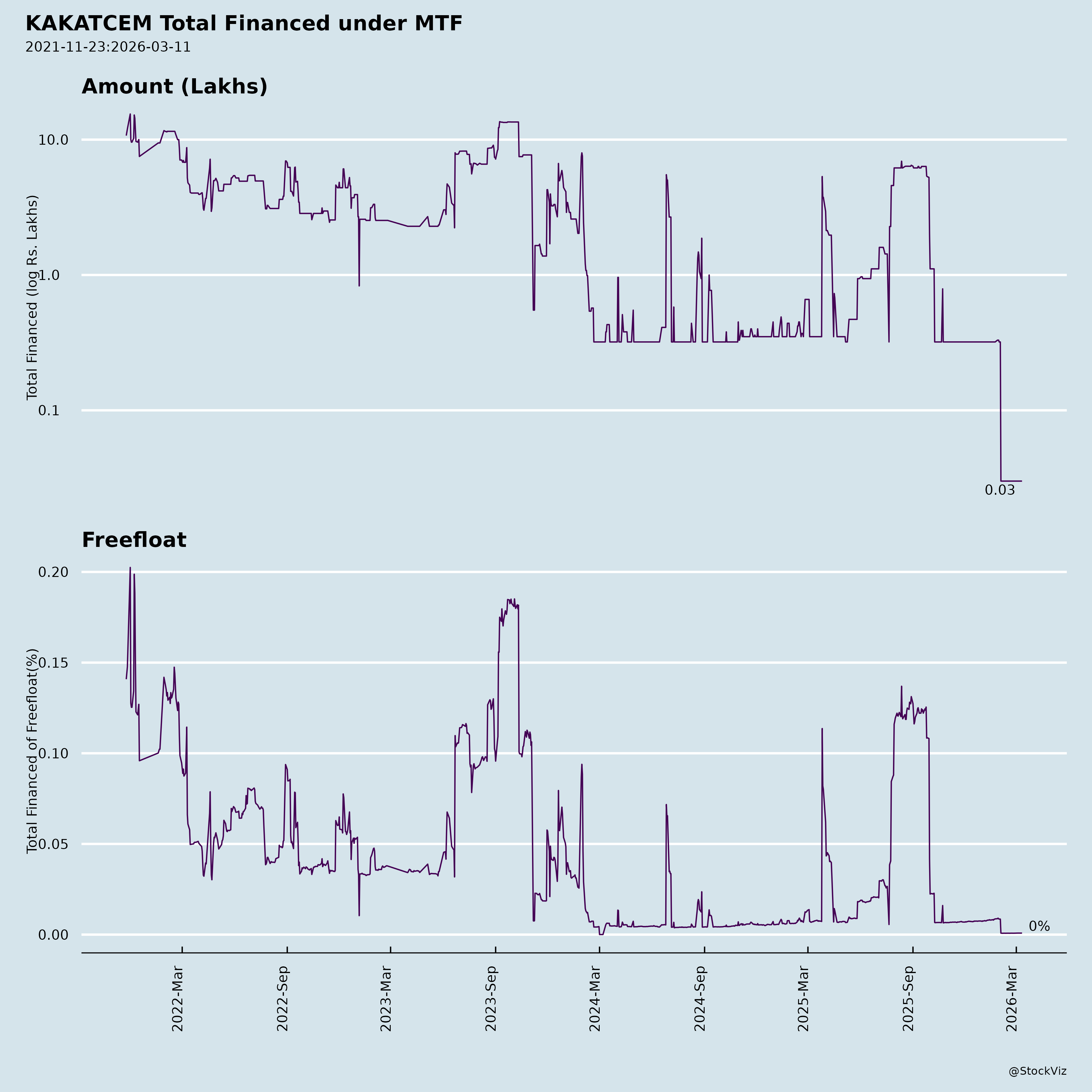

Margined

AI Summary

asof: 2025-12-08

Company Overview

Kakatiya Cement Sugar & Industries Limited (KCSIL)

- CIN: L26942TG1979PLC002485

- GSTIN: 36AABCK1868J1ZB

- Stock Codes:

- BSE: 500234

- NSE: KAKATCEM

- Sectors: Cement, Sugar, and Power Generation

- Registered Office: Hyderabad, Telangana

- Key Operations:

- Cement: Dondapadu, Suryapet (Telangana)

- Sugar & Power: Peruvancha, Khammam (Telangana)

📊 Financial & Operational Analysis: Headwinds, Tailwinds, Growth Prospects & Key Risks (as of Q2 FY26 - Sept 30, 2025)

✅ Tailwinds (Favorable Factors)

1. Operational Diversification

- Multi-Product Portfolio: Presence in three capital-intensive but synergistic industries — cement, sugar, and captive power (co-generation).

- Sugar mills produce bagasse-based power, which can offset energy costs in both sugar and cement operations.

- This integration provides cost advantages and resilience during sector-specific downturns.

2. Strong Asset Base

- Total Assets (as of 30-Sep-2025): ₹22,938.99 Crores (Unaudited)

- Equity Base: ₹19,188.88 Crores (₹777.39 Cr equity share capital + ₹18,411.49 Cr reserves)

- Despite losses, the company maintains a robust net worth, giving it financial staying power during restructuring or recovery phases.

3. Recovery in Power and Sugar Segments (YoY improvement expected?)

- While Q2 FY26 shows losses, compare with Q2 FY25:

- Cement Segment: Loss widened from ₹88.78 Cr to ₹193.83 Cr.

- Sugar Segment: Loss of ₹164.03 Cr vs. profit of ₹142.97 Cr in Q2 FY25 — indicating adverse seasonal or price-driven cycle, likely to rebound.

- Power Segment: Loss of ₹40.91 Cr vs. ₹22.61 Cr profit — linked to sugar seasonality.

- This suggests that sugar and power profitability is cyclical, and recovery possible in next quarters depending on sugarcane availability and sugar prices.

4. Settlement of Long-Pending Litigation (Positive One-Time Event)

- Paid ₹737.31 Lakhs (₹73.73 Cr) to TGTRANSCO for disputed transmission charges (2004–2022).

- This removes long-standing contingent liability and regulatory risk.

- Allows the company to focus on operations without overhang of litigation.

5. High Net Debt Reduction

- Borrowings (as of 30-Sep-2025): ₹932.10 Crores (down from ₹1,842.24 Cr on 31-Mar-2025).

- Cash Flow from Financing Activities (H1): Net outflow of ₹1,152.37 Crores — primarily due to repayment of borrowings.

- Shows conscious de-leveraging strategy, which could improve credit profile and reduce future finance cost burden.

6. Strong Cash Generation from Core Operations (H1 FY26)

- Cash flow from operating activities: ₹370.37 Crores (before tax payment).

- This occurred despite net loss of ₹1,470.92 Cr, due to:

- High depreciation (₹131.5 Cr)

- Inventory drawdown (₹1,444.66 Cr decrease — likely liquidation of stock)

- Stable trade payables and receivables

- Indicates operational cash resilience.

❌ Headwinds (Challenges & Negative Trends)

1. Massive Net Losses in Q2 FY26

- Net Loss: ₹1,148.64 Crores (vs. profit of ₹69.07 Cr in Q2 FY25).

- Loss Before Tax: ₹1,140.18 Crores.

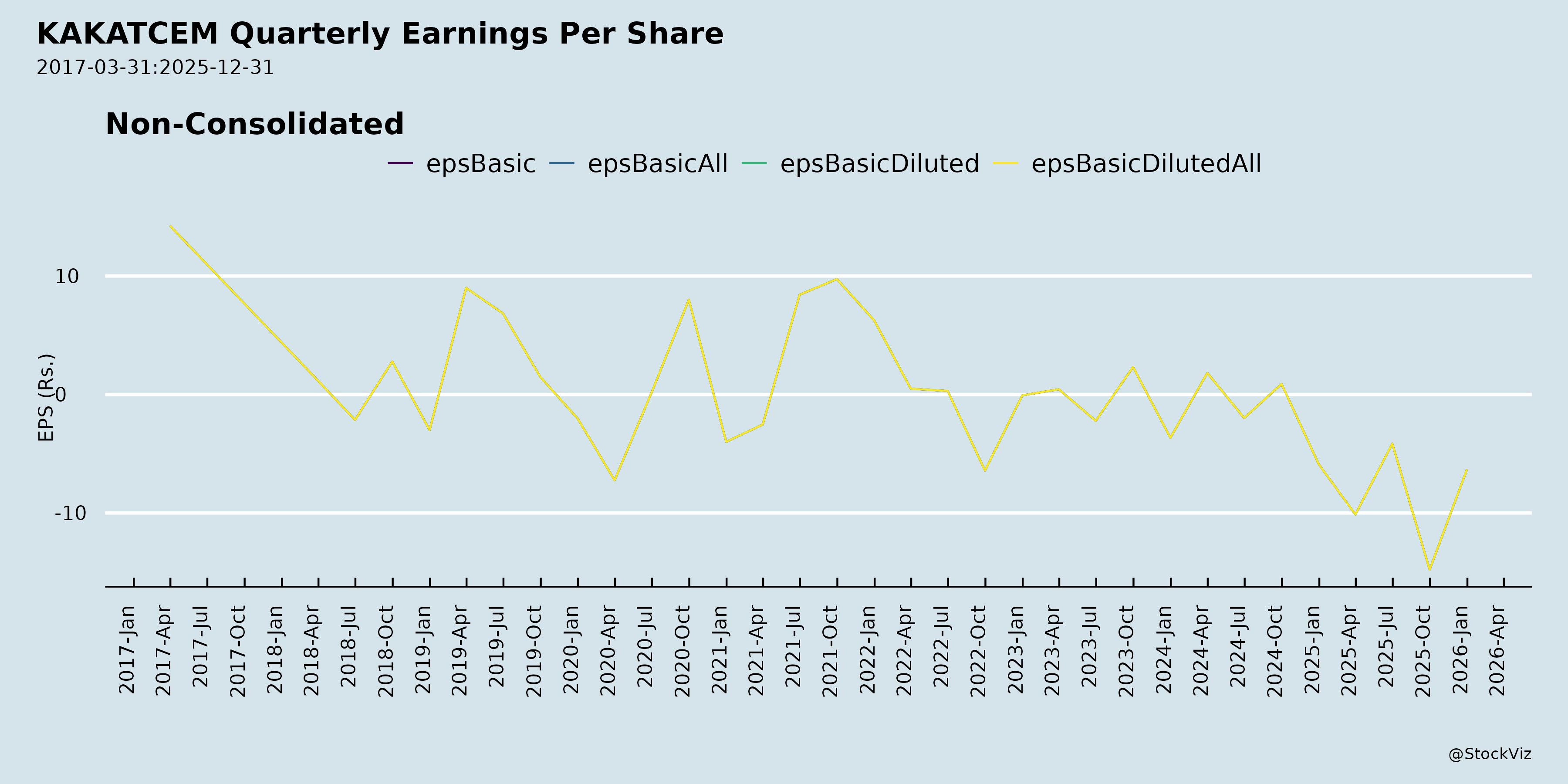

- EPS (Basic): ₹(14.78) — deterioration from ₹0.89 gain YoY.

- Indicates severe operational or one-off distress.

2. Exceptional Items – Massive One-Time Expense

- Transmission charge payment: ₹737.31 Crores under “Exceptional Items”.

- Though settled, this heavily skewed the losses.

- Even excluding exceptional item:

- Pre-exceptional loss: ₹402.88 Cr vs. profit of ₹67.71 Cr in Q2 FY25 → core business performance still deteriorated significantly.

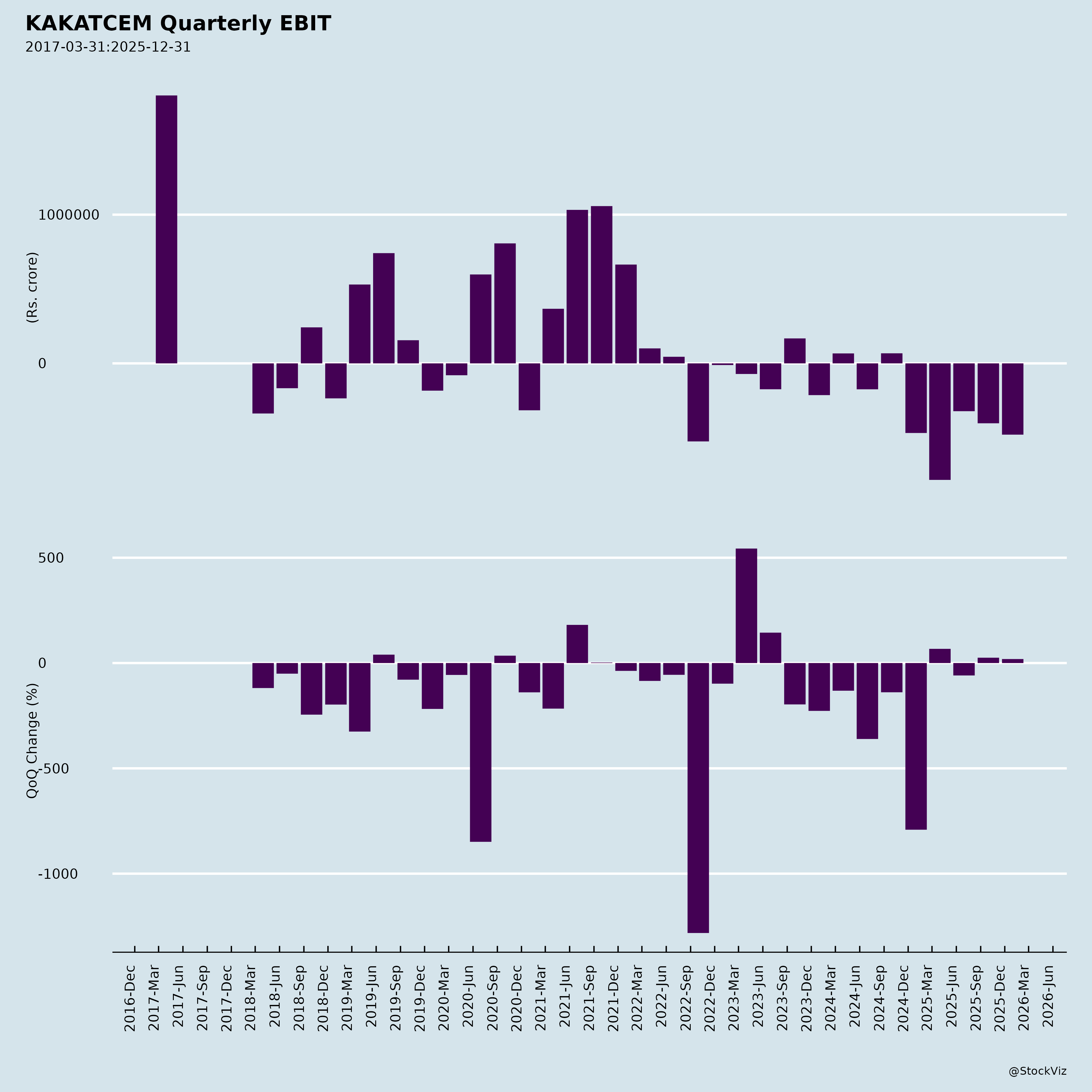

3. Deepening Losses in Cement Segment

- Cement Segment Result:

- Q2 FY26: ₹(193.83) Cr loss

- Q1 FY26: ₹(88.78) Cr loss

- Loss doubled sequentially.

- Q2 FY26: ₹(193.83) Cr loss

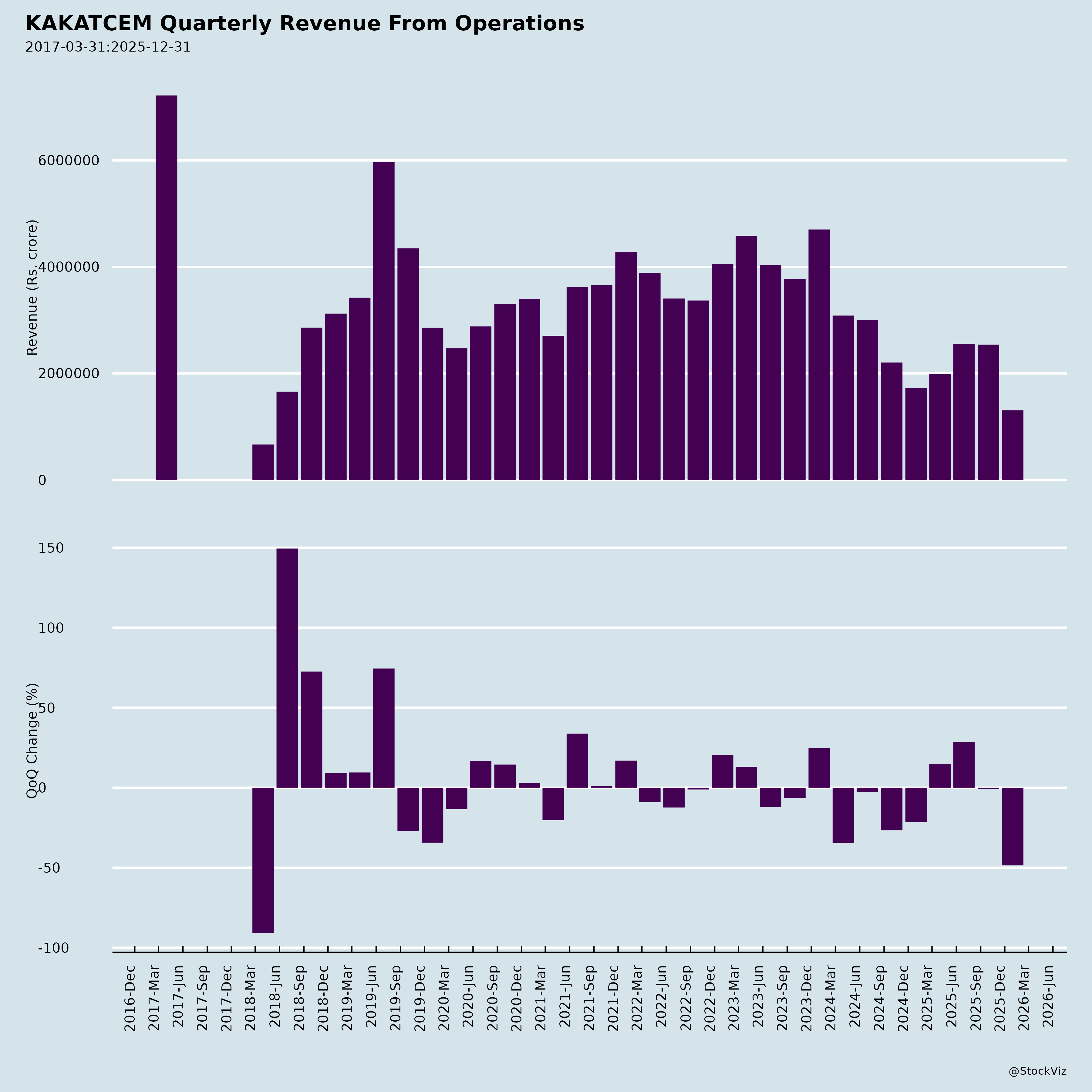

- Revenue: ₹1,790.19 Cr → ₹1,985.72 Cr (QOQ drop), but costs (esp. power & fuel) rising faster.

- High dependency on external power or outdated plant machinery could be increasing input costs.

4. Declining Revenue in Cement

- Cement segment sales:

- Q1 FY26: ₹1,985.72 Cr

- Q2 FY26: ₹1,790.19 Cr (↓ 9.8% QoQ)

- Q1 FY26: ₹1,985.72 Cr

- Suggests volume decline or pricing pressure due to:

- Competition (UltraTech, Shree Cement, etc.)

- Regional demand slowdown in Telangana/AP.

- Rising clinker/input costs.

5. Liquidity Tightening

- Cash & Cash Equivalents: Dropped to ₹18.63 Crores as of 30-Sep-2025 (from ₹3,772.73 Cr in April 2025).

- Despite cash from operations, company used cash to repay debt and/or possibly for litigation settlement.

- Critical liquidity risk: Very low operating buffer.

- Heavy reliance on trade payables and current liabilities (₹2,051.84 Cr current liabilities).

6. Inventories Sharp Decline – Fire Sale?

- Inventories: ₹2,222.15 Cr (Sep 2025) vs. ₹3,726.81 Cr (Mar 2025) → ↓ ₹1,504.66 Cr.

- While this boosted cash flow, such a plunge suggests stock liquidation, which may not be sustainable.

- Could lead to supply constraints next quarter if restocking not funded.

🔮 Growth Prospects

| Segment | Outlook |

|---|---|

| Cement | Challenging short-term due to loss-making operations. Potential upside if company invests in modernization, backward integration (clinker units), or regional consolidation. Telangana infrastructure push may support demand long-term. |

| Sugar | Cyclical rebound possible: Profitable in Q2 FY25, loss in Q2 FY26. Recovery depends on sugarcane supply, sugar realization, export policy, and ethanol blending mandates (govt. pushing 20% ethanol by 2025). |

| Power | Co-gen power from bagasse is low-cost and sustainable. Revenue could improve if surplus power is sold to the grid. Future scope in biomass or solar hybrid models. |

| Overall | Turnaround story in long-term — strong asset base, reduced debt, and settlement of disputes suggest management is cleaning the slate. Growth hinges on operational efficiency and market recovery. |

⚠️ Key Risks

| Risk | Explanation |

|---|---|

| 1. Liquidity Risk | Cash balance at ₹18.63 Cr is critically low. Unable to withstand any delay in collections or spike in input costs. |

| 2. Cement Segment Viability | Consistently loss-making. Raises questions about plant efficiency, technology, or competitiveness. May require asset review or capex. |

| 3. Commodity Price Volatility | Sugar prices, cement demand, and fuel/power tariffs are cyclical and policy-driven. Exposure to agricultural disruption (rainfall, cane crop) adds uncertainty. |

| 4. Regulatory & Tax Risks | Past disputes with TSTRANSCO indicate energy/billing vulnerability. Future audits or tax assessments possible. |

| 5. Debt Servicing Pressure | Though reducing, borrowings still at ₹932 Cr with ongoing interest cost (₹4.11 Cr in Q2). Renewal risk if liquidity not restored. |

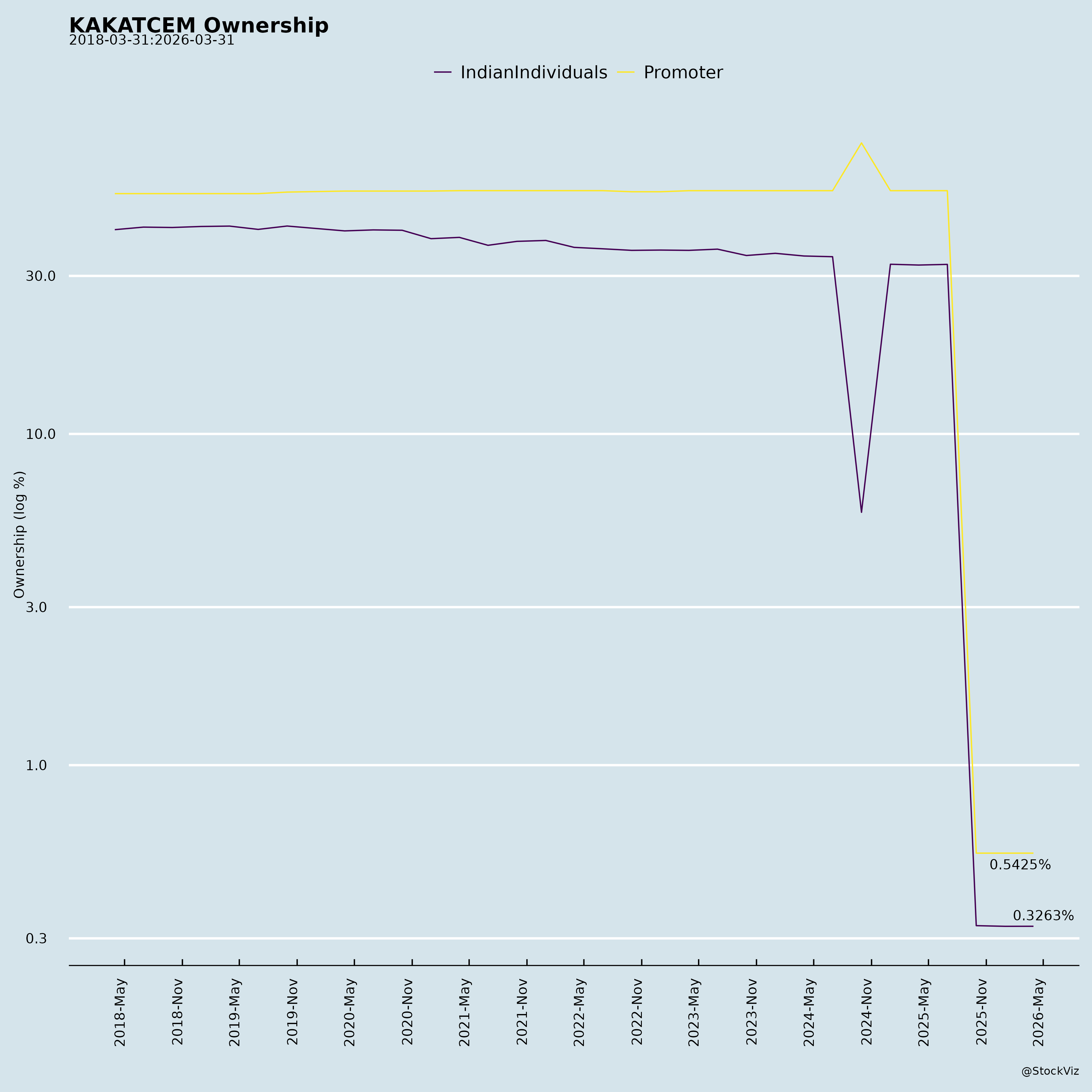

| 6. Shareholder Confidence | Massive Q2 loss and near-zero cash may affect market perception. Re-lodgment of physical shares (zero requests as of Nov 30) shows low retail investor activity or poor transfer infrastructure. |

✅ Summary: Investment Thesis

| Factor | Assessment |

|---|---|

| Financial Health | Poor (Short-Term), Resilient (Long-Term) – Net losses and liquidity squeeze; but strong equity base and de-leveraging. |

| Earnings Trend | Deteriorating – Deep losses in Q2 FY26 across core segments. |

| Catalysts | 1. Sugar season recovery (Q3/Q4). 2. Stable energy costs. 3. New cement contracts or expansion. 4. Strategic sale or joint venture. |

| Valuation Risk | Current EPS (₹-14.78) makes P/E meaningless. Stock may trade on book value or turnaround potential. |

| Outlook | Speculative / Turnaround Play – Not for risk-averse investors. Requires a 2–3 year horizon for potential recovery. |

🔚 Conclusion

Kakatiya Cement Sugar & Industries Limited is navigating a difficult phase, with massive one-time charges and operational losses, especially in cement. However, management is cleaning the balance sheet (debt down, disputes resolved, cash flow positive) and operating a diversified agro-industrial model with long-term sustainability potential.

✅ Recommendation:

Monitor closely for signs of: - Improvement in Q3 cement profitability - Rebuilding of cash balances - Increase in sugar segment revenue - Any capacity expansion or strategic partnerships

Currently a high-risk, potential turnaround stock — suitable only for speculative or contrarian investors with tolerance for volatility and long holding periods.

Key Metric to Track Next Quarter:

- Cash & Cash Equivalents

- Cement Segment Profit/Loss

- Inventory Levels

- Debt Repayment vs. Replenishment of Liquidity

Data Source: Unaudited Financial Results for Q2 FY26 (Quarter ended 30-Sep-2025), SEBI disclosures, and RTA report dated Dec 2025.

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.