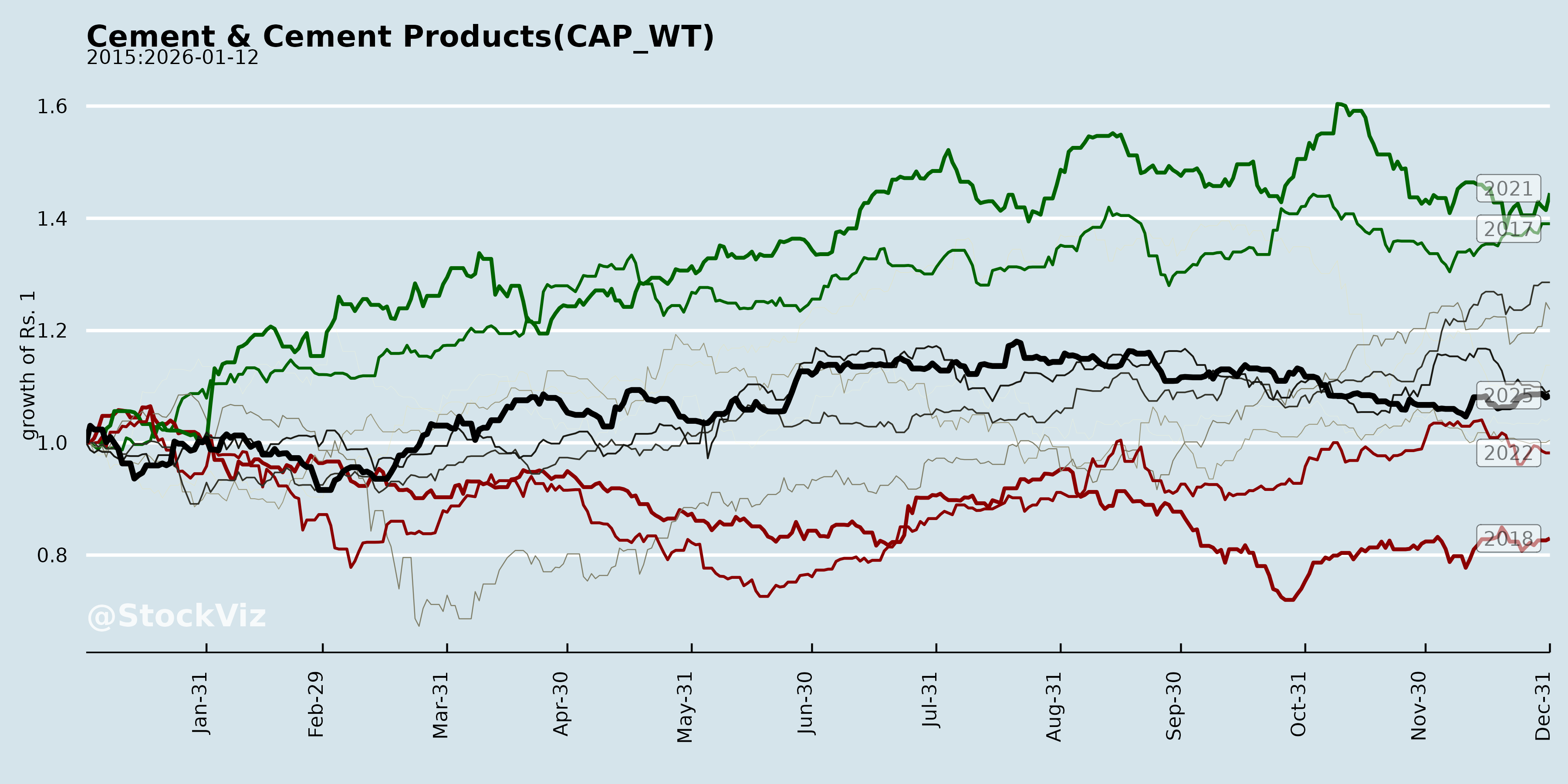

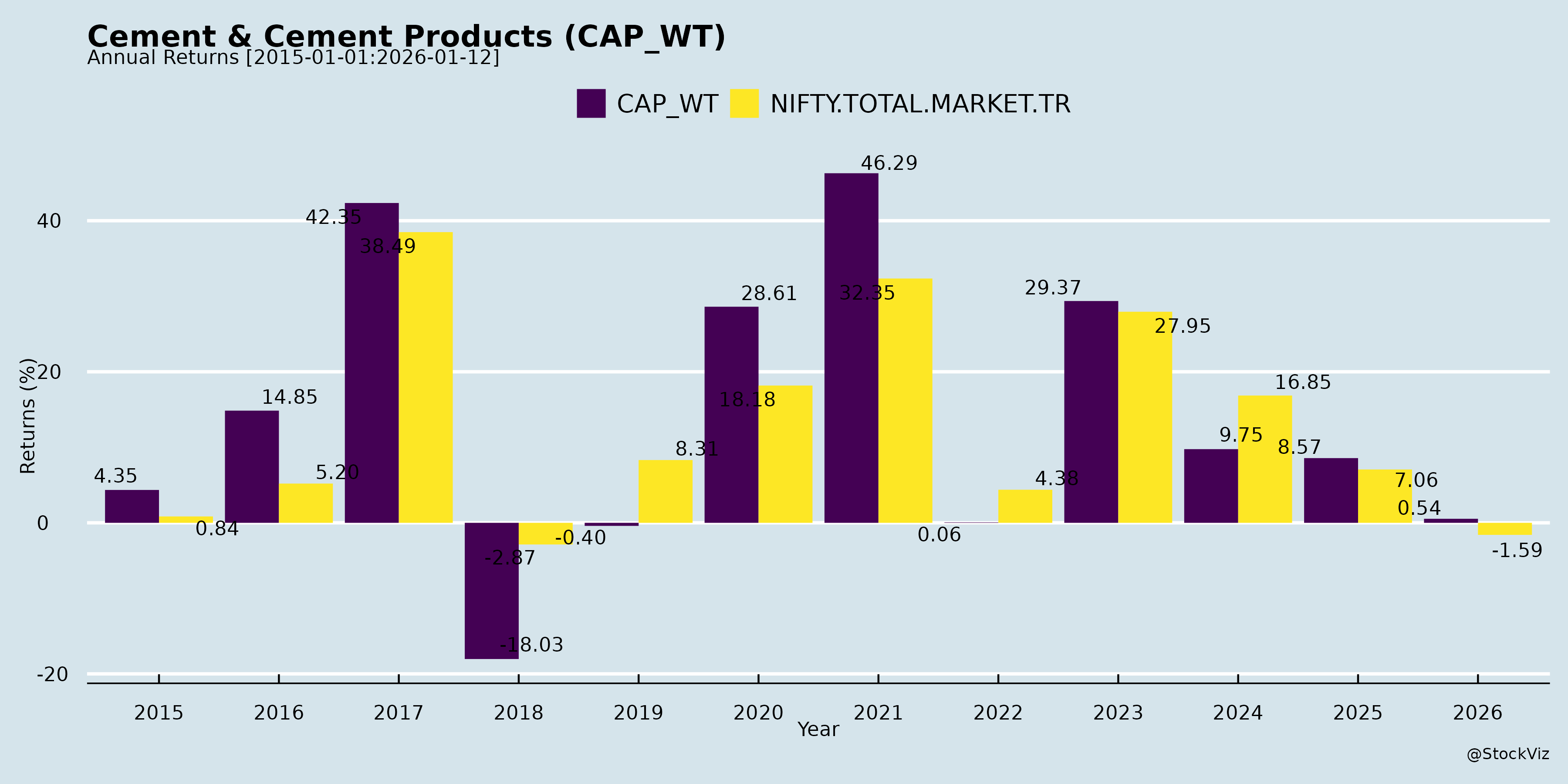

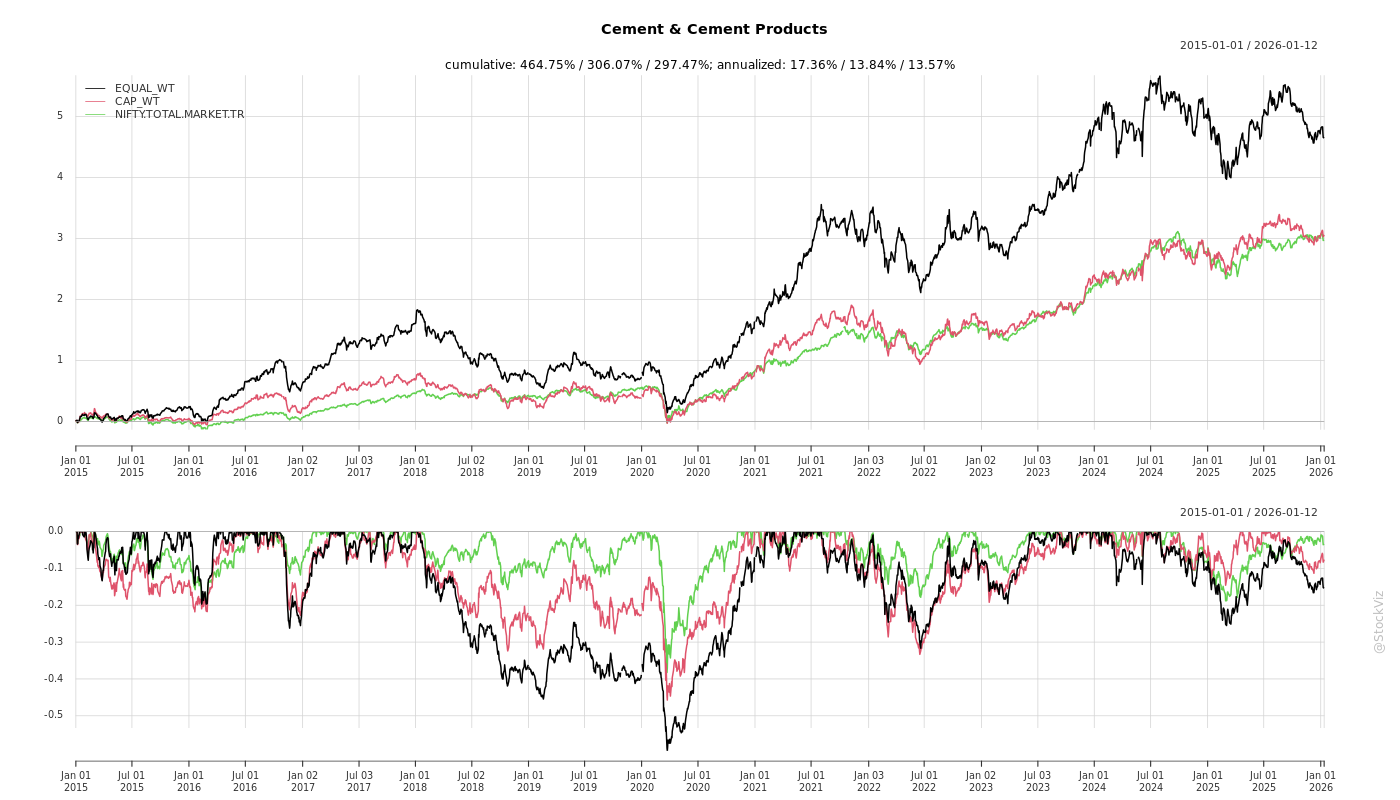

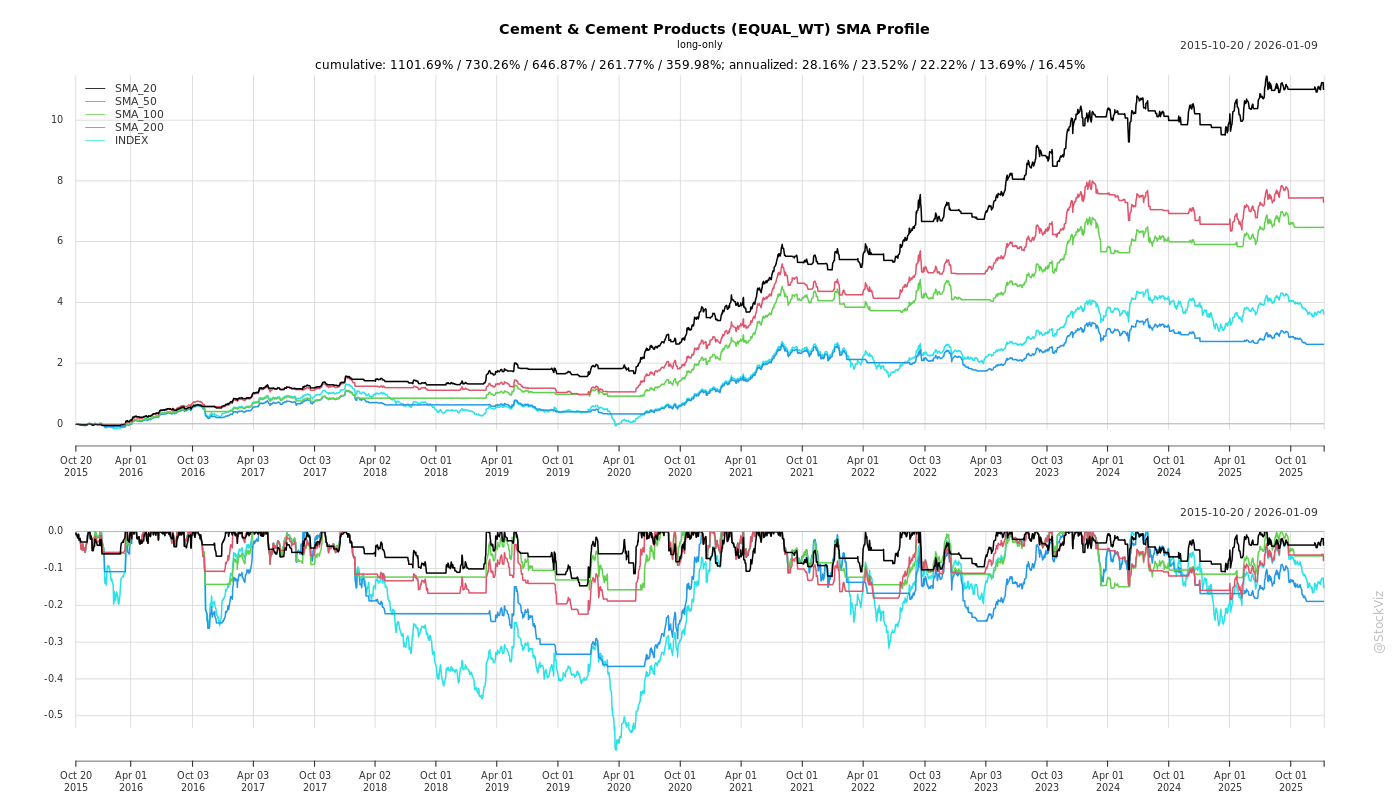

Cement & Cement Products

Industry Metrics

May 8, 2026

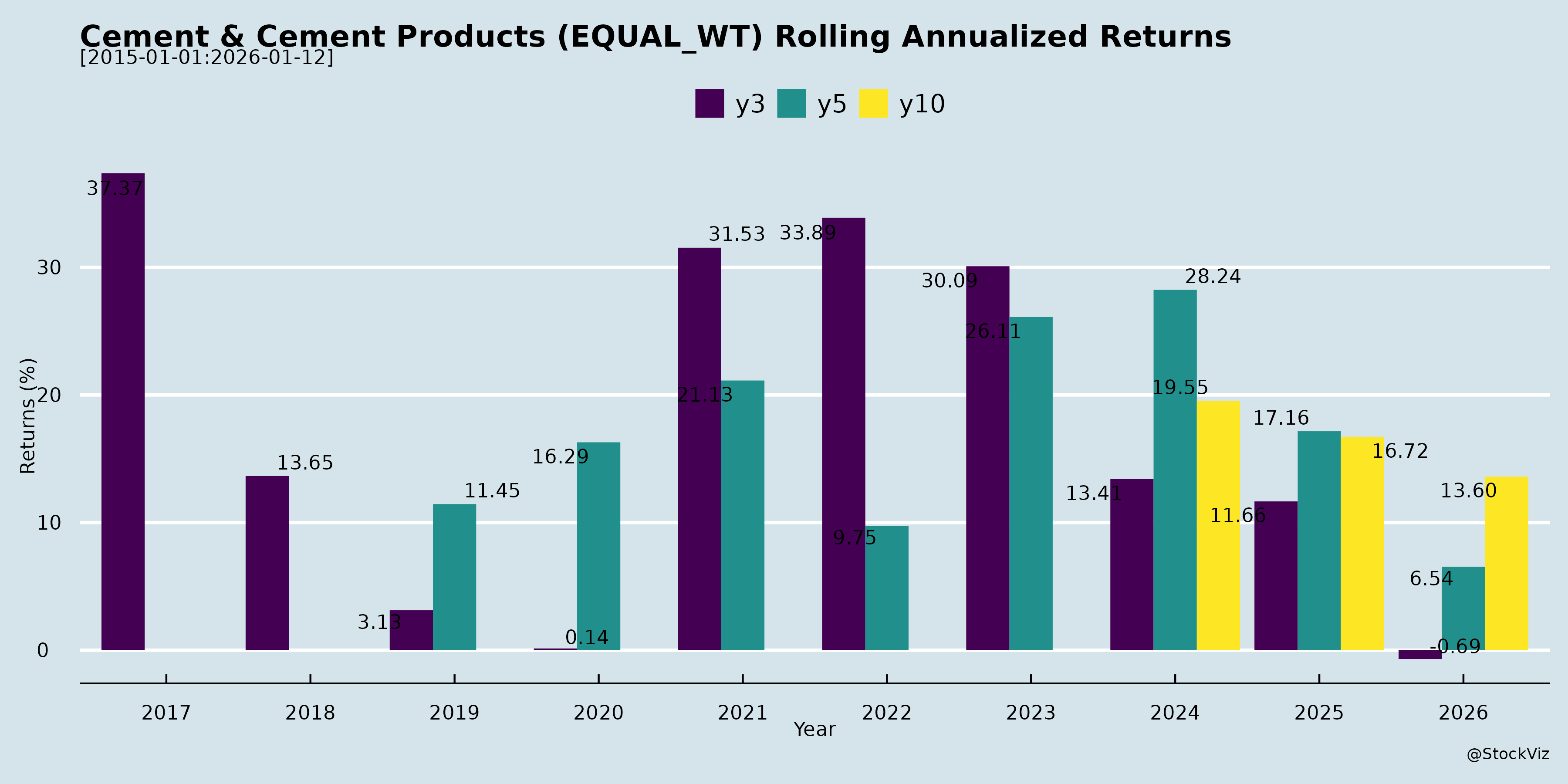

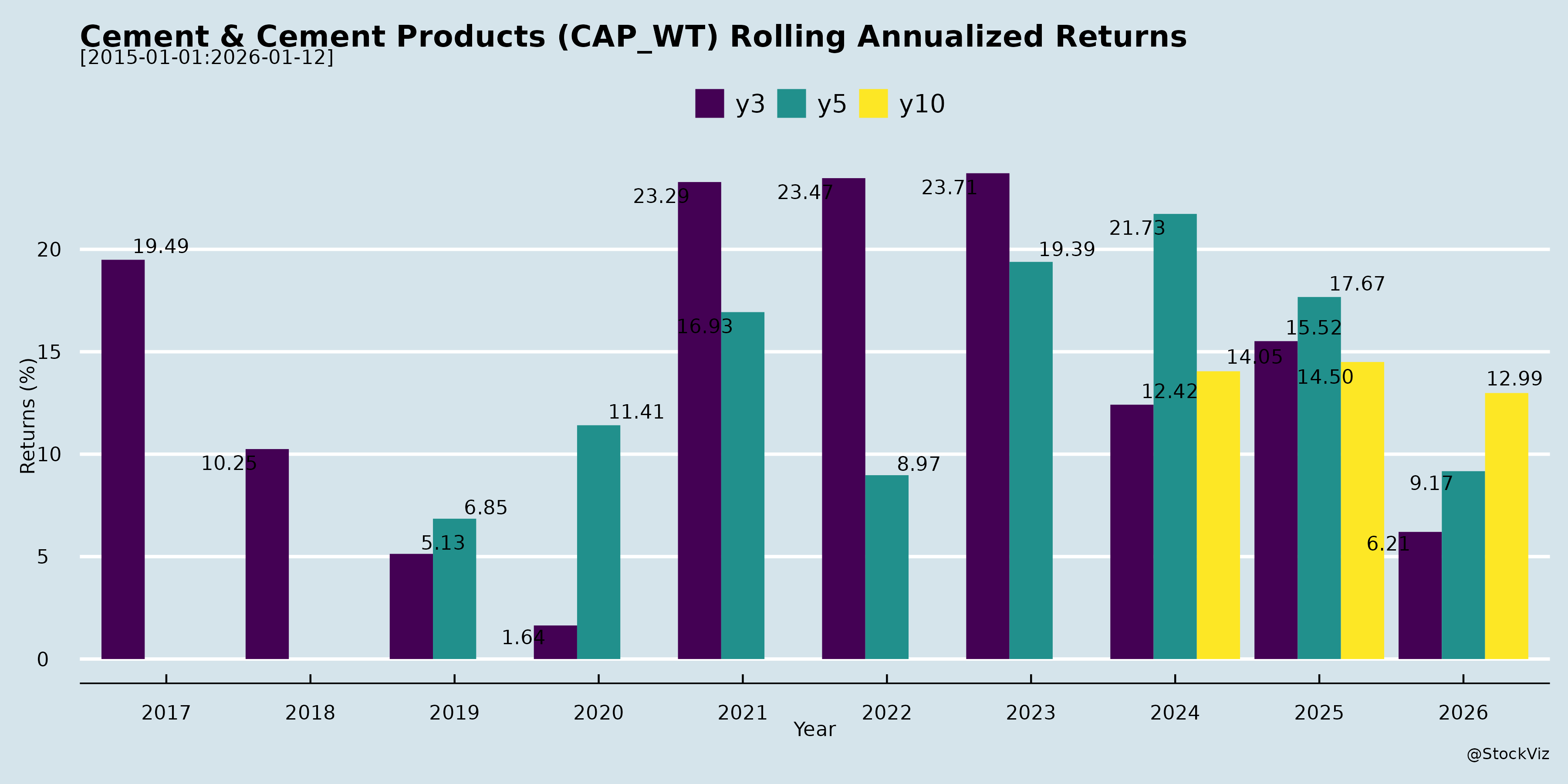

Annual Returns

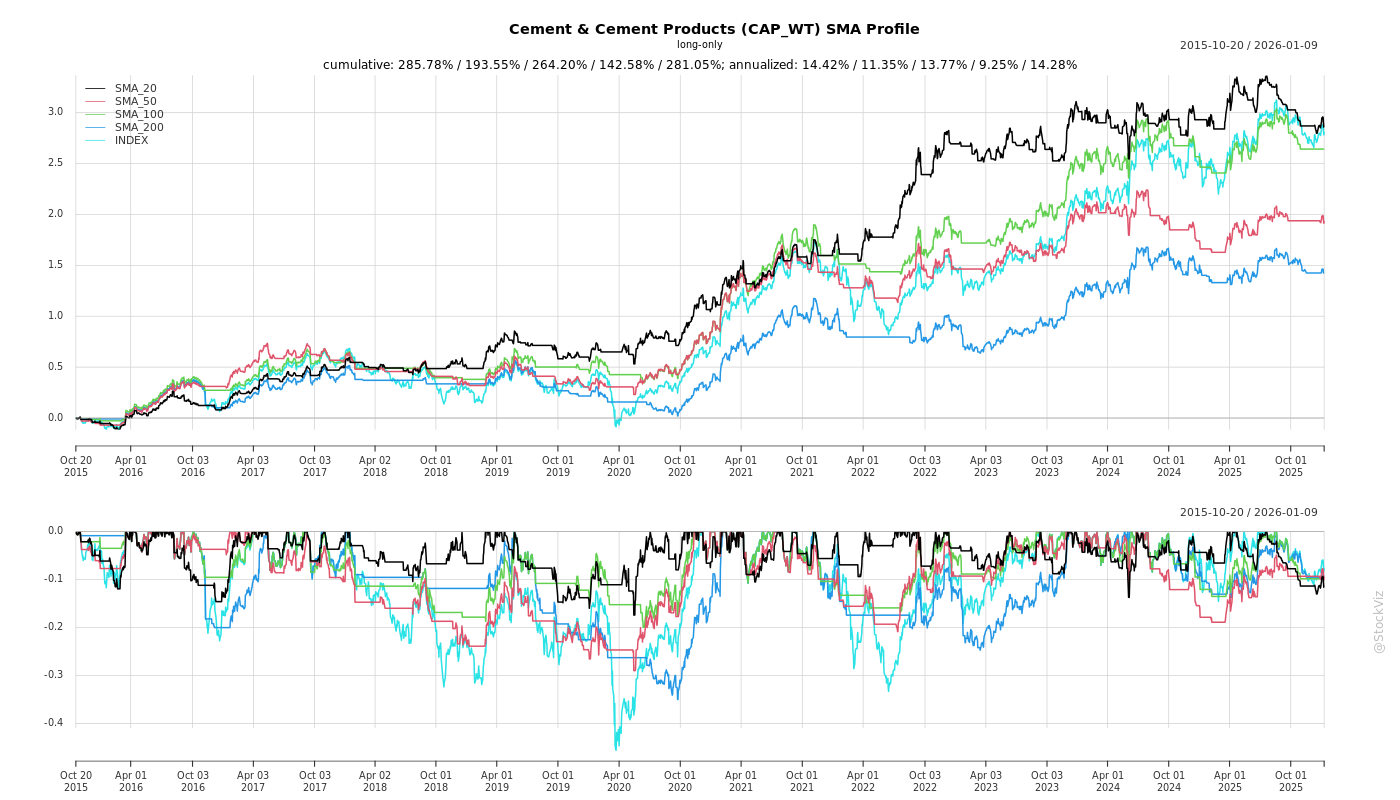

Cumulative Returns and Drawdowns

SMA Scenarios

Current Distance from SMA

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-15

The challenges and opportunities in the Indian cement and building materials industry have evolved significantly over time, shaped by changing macroeconomic conditions, intense competitive dynamics, and a strategic shift towards sustainability and product diversification.

Evolving Opportunities

1. Robust Macroeconomic and Infrastructure Demand Historically dependent on fragmented demand, the industry now benefits from sustained structural tailwinds. India’s GDP growth, forecasted between 6.3% and 6.8%, ensures that domestic consumption and capital expenditure remain the primary engines of growth [1, 2]. The industry is projected to see cement demand cross 620 million tonnes per annum (Mtpa) by FY30, growing at a CAGR of 7% to 8% [3, 4]. * Infrastructure and Housing: Government spending on infrastructure and a rebound in rural and urban housing continue to drive demand [1, 5-7]. * Event-Driven and Regional Tailwinds: Specific regional events, such as the government’s approval of Ahmedabad as the host city for the 2030 Commonwealth Games, are fast-tracking investments in stadiums, transport, and hospitality, creating localized demand surges [8, 9]. Additionally, regions like East India, which historically had low per capita consumption, are showing huge headroom for growth driven by mining and natural resource unlocking [10, 11]. Pre-election government spending in states like Bihar, Assam, and West Bengal has also heavily boosted capital expenditure and infrastructure project pipelines [12, 13].

2. Premiumization and Product Diversification Companies have actively evolved their product mixes to escape the commoditized nature of standard cement, shifting focus toward value-added, premium products. * Premium Cement: Brands like Ambuja Kawach, ACC Gold, and Nuvoco’s Concreto have established themselves as high-margin, water-repellent, and superior-strength products [14-16]. For example, Shree Cement successfully increased the share of its premium products from 15% to 22% of its total trade volume, optimizing its product mix to boost profitability [17, 18]. * Ready-Mix Concrete (RMX) and Modern Building Materials (MBM): To capture additional value, companies are aggressively expanding into RMX and construction chemicals. Shree Cement plans to increase its RMX plants from 19 to 45 by late 2026 [19, 20], while players like Nuvoco are driving strong year-over-year growth in tile adhesives, block jointing mortars, and wall putty [21, 22].

3. Industry Consolidation and Synergies The industry is experiencing a massive wave of consolidation, creating powerful pan-India networks that optimize logistics, manufacturing, and capital allocation. Notable examples include the amalgamation of ACC Limited and Orient Cement into Ambuja Cements to create a unified ‘One Cement Platform’ [23-25]. Similarly, Sagar Cements has achieved geographic expansion and access to new limestone reserves through strategic acquisitions like BMM Cement, Satguru Cement, and Jajpur Cement [26, 27]. Mid-sized players are also forming strategic alignments, such as Shree Digvijay Cement acquiring exclusive brand and distribution rights for Hi-Bond Cement to leverage economies of scale and reduce freight costs in Gujarat [28-30].

4. Sustainability and Technological Innovation What was once viewed merely as a regulatory burden has evolved into a core strategic opportunity for cost leadership. * Green Power & Alternative Fuels: Companies are heavily investing in green power, with Shree Cement reaching 61% renewable energy usage [31, 32] and Adani Cement targeting a 60% green power share and 30% alternative fuel use by FY28 [33]. * Decarbonization Technologies: Cutting-edge technologies are being deployed, such as Ambuja Cements pioneering the world’s first commercial deployment of Coolbrook’s RotoDynamic Heater™ (RDH™) technology for electrified kiln heating, and participating in the Indo-Swedish Carbon Capture Utilization (CCU) pilot project [34-36].

Evolving Challenges

1. Intensifying Competition and Pricing Pressures Despite strong demand, the influx of new capacities has severely diluted pricing power over time. * Margin Compression: New capacity expansions by major players (like Shree Cement and UltraTech adding millions of tons in the same geographic clusters) have intensified competition [37, 38]. Consequently, the geographic arbitrage that some companies previously enjoyed has vanished, bringing premiums over competitors down from Rs. 30 to near zero at times, and causing EBITDA margins for some players to drop to decade lows (e.g., Rs. 500 per ton) [39-42]. * Stagnant Long-Term Pricing: The long-term price CAGR in the cement sector over the last 10 years has been dismal—in the low single digits and often below inflation [43, 44]. As new capacity comes online, competitors frequently prioritize market share over margins, leading to volatile and subdued pricing [45, 46].

2. Geopolitical Uncertainty and Volatile Input Costs The industry remains highly sensitive to global supply chain disruptions. * Fuel and Packaging Costs: Conflicts in the Middle East and broader geopolitical tensions have led to spikes in crude oil, international pet coke, and coal prices, alongside currency depreciation [47, 48]. Additionally, the rising cost of granules has directly impacted the cost of packaging bags [49, 50]. These combined inflationary pressures are expected to squeeze margins for at least one to two quarters at a time [51]. * Export and Economic Slowdowns: A softer global economic growth environment threatens to impact India’s exports and broader investment inflows, which indirectly affects large-scale commercial and industrial development [5, 52].

3. Logistical and Labor Constraints While elections stimulate government spending, they also introduce operational bottlenecks. For instance, during the Bihar state elections, railway lines prioritized passenger trains over goods trains, which severely impaired freight movement for companies relying on inter-state cement transport [53, 54]. Additionally, election periods and extended monsoon seasons often cause a severe scarcity of laborers, as workers return to their home states, heavily disrupting on-site construction activities [55, 56].

4. Capital Efficiency and Return on Capital Employed (ROCE) Over time, Return on Capital Employed (ROCE) and Return on Equity (ROE) have trended downwards across the sector [57, 58]. Because the capital cost of setting up new capacity or acquiring existing plants remains quite rich, and entry barriers (like limestone auctions) are rising, extracting a risk-adjusted hurdle rate of return has become increasingly difficult [43, 59, 60]. Companies are often forced to choose between pushing volume at the expense of price, or artificially constraining volumes to maintain price parity and fixed-cost recovery, making capacity utilization a tricky balancing act [58, 61, 62].

What are the headwinds affecting this industry?

asof: 2026-04-15

Cost Inflation and Supply Chain Disruptions The cement industry is highly fuel-intensive, making it particularly vulnerable to supply chain disruptions and rising prices for crude oil, pet coke, and coal [1], [2], [3]. These input cost spikes are largely driven by ongoing geopolitical conflicts and tensions in the Middle East, which create broader market volatility [4], [5], [6], [7]. This burden is further exacerbated by currency depreciation, which increases the landed cost of imported fuels [4], [6], [8]. Companies are also facing increased packaging expenses due to a surge in granule costs [5], [7], as well as higher freight and transportation costs caused by occasional supply chain and transport network disruptions [2], [9], [10]. Because the industry typically operates on low margins, these cost escalations have an immediate and heavy impact on overall profitability [1], [3].

Intensified Competition and Structural Overcapacity The sector is grappling with persistent overcapacity, with the national capacity utilization hovering only around 70% [11], [12]. As major players continue to execute aggressive capacity expansions, competition has intensified significantly, leading to a scramble for market share rather than margin preservation [13], [14], [11], [15]. This overcapacity creates severe pricing pressures and margin dilution, narrowing the price premium that established brands historically enjoyed over standard offerings [16], [17], [18], [19]. Furthermore, newer plants are frequently able to undercut market prices by leveraging large government incentives and tax sops [17], [20], [19].

Demand Volatility and Seasonal Factors Unpredictable weather patterns, particularly severe, extended, and unseasonal monsoons, have repeatedly dampened construction activities and suppressed cement demand across various quarters [21], [22], [23], [24], [25], [26]. In addition to weather, the industry has faced temporary labor shortages at construction sites during major festive seasons (like Diwali), marriage seasons, and state elections, which stalls project execution and lowers cement off-take [22], [24], [27], [28]. Furthermore, following recent GST reductions, the market experienced short-term confusion and sluggishness, which led to an excessive softening of cement prices, particularly in the non-trade and institutional segments [29], [30], [31], [32].

Regulatory and Tax Burdens Certain operating regions face highly specific regulatory headwinds that inflate variable costs. A primary example is the additional levy of a mineral-bearing land tax (MBIT) in Tamil Nadu. This newly imposed tax of Rs. 160 per ton of limestone acts as a significant structural cost headwind for companies with mining and manufacturing footprints in the state [33], [34], [35].

Macroeconomic and Global Risks On a broader scale, indications of a global economic slowdown present a systemic headwind for the industry [36], [37]. Softer global growth and geopolitical uncertainties threaten to negatively impact India’s exports and foreign investment inflows, which could indirectly slow down the capital expenditure and domestic infrastructure projects that serve as the primary engines of cement demand [36], [37].

What are the key things to understand about this industry?

asof: 2026-04-15

Based on the provided company reports and earnings transcripts, the Indian cement industry is a highly competitive, capital-intensive, and cyclical sector. Here are the key things to understand about its current dynamics:

1. Strong Demand and Growth Drivers * Steady Expansion: The cement market is expanding at a healthy rate of 6% to 8% year-on-year, with total demand expected to cross 620 million tonnes per annum (MTPA) by FY30 [1-3]. * Key Sectors: This growth is primarily fueled by a strong government focus on public infrastructure, urban and semi-urban development, and a rebound in private consumption and capital expenditure [1, 4]. Rural housing, urban housing, and infrastructure remain the dominant consumers of cement [2, 5, 6].

2. Margins, Pricing, and Capacity Utilization * Low Margins and Cost Sensitivity: The cement industry is highly fuel-intensive and typically operates on very low margins, meaning any increase in raw material, fuel, or supply chain costs must generally be passed on directly to the customer [7, 8]. * Overcapacity & Utilization: The national average capacity utilization for the sector is around 70% to 75% [9, 10]. Because capacity additions are expected to grow at 5%-6% per annum against a demand growth of 7%-8%, overcapacity is likely to persist in the foreseeable future, which can lead to pricing volatility when new plants are commissioned [10, 11]. * Cyclical Nature: Cement is inherently cyclical; periods of muted demand and low pricing are often followed by upward trends depending on macroeconomic stability and construction seasons [12, 13].

3. Sales Strategy: Trade vs. Non-Trade and Premiumization * Trade (B2C) Dominance: Companies highly prioritize the “trade” segment (sales directly to consumers through dealer networks) over the “non-trade” or institutional segment (B2B/infrastructure sales) [14, 15]. Trade sales typically offer better pricing stability, higher margins, and better clinker realization [16, 17]. * Premiumization: To combat pricing pressures, manufacturers are increasingly focusing on selling premium cement products and optimizing their product mix [4, 15].

4. Sustainability and “Green” Initiatives (ESG) * Blended Cements: There is a major push toward environment-friendly “blended cements” like Portland Pozzolana Cement (PPC), Portland Slag Cement (PSC), and Composite Cement, which use less clinker and incorporate industrial by-products like fly ash and slag [9, 18-20]. * Green Power and Decarbonization: Companies are heavily investing in green energy, such as Solar, Wind, and Waste Heat Recovery Systems (WHRS), to power their plants and lower their carbon footprint [21-24]. * Resource Stewardship: Leading players are setting science-based net-zero targets (SBTi), adopting frameworks like the Taskforce on Nature-related Financial Disclosures (TNFD), utilizing Alternative Fuels and Raw materials (AFR) to reduce landfill waste, and striving for high “water positivity” indexes [25-28].

5. Consolidation and High Entry Barriers * The industry is undergoing significant consolidation, highlighted by major mergers and acquisitions, such as the amalgamation of ACC Limited and Orient Cement Limited into Ambuja Cements to create a pan-India “One Cement Platform” [29, 30]. * Entry barriers are rising due to strict limestone mine auctions, the capital-heavy nature of building new plants, and the challenging operational discipline required to successfully execute and integrate projects [31, 32].

6. Importance of Logistics and Value-Added Products * Proximity and Freight: Because cement is a bulky commodity, a company’s locational advantage—proximity to raw materials (limestone, coal) and key markets—is critical for efficient distribution and reducing the cost of production [33, 34]. Companies leverage robust multimodal logistics, including dedicated railway fleets and coastal sea routes via captive jetties, to maintain cost leadership [35, 36]. * Diversified Offerings: To capture additional growth and provide end-to-end building solutions, cement companies are aggressively expanding into Ready-Mix Concrete (RMX) and Modern Building Materials (MBM), such as construction chemicals, wall putty, tile adhesives, and AAC blocks [37-40].

What are the tailwinds affecting this industry?

asof: 2026-04-15

Continued government investments in infrastructure and capacity building are massive drivers for the cement industry over the medium to long term [1, 2]. The Union Budget 2026–27 has reinforced these growth prospects by raising public capital expenditure to ₹12.2 lakh crore, keeping infrastructure like roads, railways, and urban systems at the core of the country’s development [3]. There is a large pipeline of capital expenditure, including the construction of metros in 9 to 10 cities, bridges, hydropower projects, railway tracks, and extensive highway networks [4-6]. Additionally, specific regional developments, such as the approved Commonwealth Games 2030 in Ahmedabad, are putting allied investments in stadiums, transport, and hospitality on the fast track [7, 8].

Robust demand from the housing sector remains a primary engine of growth for the industry [9, 10]. The sector is experiencing a highly positive phase fueled by sustained government spending on affordable housing and a strong revival in private real estate development and commercial urbanization [11-13]. Rural consumption and steady rural housing demand are also playing a crucial role in maintaining consistent volume growth [14, 15].

Strong macroeconomic stability and GDP growth provide significant structural tailwinds. The Indian economy is expected to continue as one of the fastest-growing globally, with GDP growth forecasts ranging from 6.3% to 6.8% [9, 10], and recent projections by the RBI pointing toward a 7.4% GDP growth rate for FY 26-27 [16, 17]. Because cement demand historically grows at a multiplier of about 1x to 1.1x the national GDP [16, 17], these economic conditions are highly favorable. Furthermore, steady employment conditions, benign inflation within a manageable range, monetary easing, and supportive tax and GST rationalization measures are expected to sustain momentum and boost private consumption [3, 18, 19].

Accelerating industry consolidation and rising barriers to entry are expected to heavily support long-term value creation, pricing power, and margin expansion [20-23]. Barriers to entry are increasing significantly due to the complexities of limestone auctions, the immense challenges of commissioning new greenfield projects, and the difficulties in executing and turning around acquisitions [24-27]. This consolidation—coupled with disciplined capital allocation by major players—is anticipated to drive prices up over the medium to long term, yielding better returns on capital [28-31].

Deeper ESG integration and the adoption of technology-enabled construction practices are shaping how companies compete and profit [6, 32]. There is a structural shift towards sustainable construction practices, creating favorable conditions for environmentally friendly products like AAC blocks, green cement, and blended cement [33-36]. The industry is benefiting from higher trade and premium cement sales, supported by R&D-driven, customized solutions, which deliver superior EBITDA margins and realization advantages over standard products [32, 37, 38].

Collectively, these core drivers are placing the industry on a trajectory for an estimated demand growth of 6% to 8% in the near to medium term [32, 39-44]. Long-term demand remains exceptionally strong, with industry forecasts anticipating that Indian cement demand could cross 620 million metric tonnes per annum (MTPA) by FY30 [45, 46].

What is the general outlook of this industry?

asof: 2026-04-15

The general outlook for the cement industry is highly positive, characterized by robust volume growth, strong macroeconomic tailwinds, and significant structural shifts towards sustainability. The industry is expected to sustain its growth momentum in both the near and long term, driven primarily by India’s economic resilience and heavy investments in infrastructure.

Strong Demand and Volume Growth Projections The cement industry is on track to witness a demand growth of approximately 6% to 8% in the financial year 2025-2026 [1-4]. Following a subdued period impacted by monsoons and elections, demand revived significantly in the third quarter and is expected to continue through the fourth quarter with double-digit growth in some regions [5, 6].

Looking further ahead, the long-term trajectory is remarkably strong. Industry leaders project a 7% to 8% demand growth over the next 10 to 20 years, with overall cement demand in India expected to cross 620 million tonnes per annum (MTPA) by FY30 [7, 8]. Because cement consumption generally grows at 1x to 1.1x the national GDP—which the Reserve Bank of India projects at 7.3% to 7.4%—the sector is well-supported by India’s position as the fastest-growing major economy [9-11].

Primary Growth Drivers The anticipated surge in cement demand is anchored by several core drivers: * Government Infrastructure Spending: The Union Budget 2026–27 has raised public capital expenditure to ₹12.2 lakh crore, keeping infrastructure—such as roads, railways, and urban systems—at the core of development [12]. State and central planned capex is set to rise by 11.5% to 15% in FY27, heavily supporting construction [13]. * Housing and Real Estate: Both rural and urban housing, alongside affordable housing initiatives and a revival in private real estate development, remain primary engines of growth [4, 14-16]. * Private CAPEX and Manufacturing: A broad-based revival in manufacturing and private capital expenditure, alongside commercial urbanization, will continue to fuel long-term consumption [17, 18].

Pricing, Profitability, and Consolidation While the industry faced severe price corrections in the recent past—especially in the non-trade segments following GST adjustments—prices have begun to recover and stabilize [19-21]. Moving forward, trade prices are expected to rise due to improved demand and the necessity to offset rising input costs, such as fuel and pet coke [21, 22].

Over the medium to long term, profitability is expected to improve due to industry consolidation and rising entry barriers. Acquiring new limestone mines through auctions and successfully integrating new capacities require significant capital and disciplined execution, which naturally restricts new entrants [23-25]. Consequently, as the sector consolidates under larger players, pricing power is expected to move upward, securing better risk-adjusted returns [26, 27].

Headwinds and Short-Term Challenges Despite the buoyant outlook, the industry is navigating a few notable challenges: * Overcapacity and Competitive Intensity: The all-India capacity utilization currently hovers around 70%, and with significant new capacity additions in the pipeline, competitive intensity will remain high in the near term [28-30]. * Cost Pressures: Ongoing geopolitical uncertainties and global economic slowdowns pose risks to supply chains [31]. A recent surge in pet coke and granule prices threatens to increase fuel and packaging costs, which may impact profit margins for one to two quarters until price hikes can fully absorb them [32, 33].

Structural Shifts and ESG Integration Finally, the industry is undergoing a massive transformation in how it operates. Deeper ESG (Environmental, Social, and Governance) integration and the adoption of technology-enabled construction practices will dictate how companies compete in the future [1, 34]. There is a pronounced strategic shift toward maximizing blended, eco-friendly cement (like slag and PPC), expanding alternative fuels and raw materials (AFR) capacity, and increasing renewable energy footprints [35, 36]. Additionally, institutional consumers are increasingly demanding high-quality, high-strength “Green Cement” for major structural projects like highways and metro systems, rewarding companies with strong R&D capabilities [1, 34].

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.