INDIASHLTR

Equity Metrics

May 8, 2026

India Shelter Finance Corporation Limited

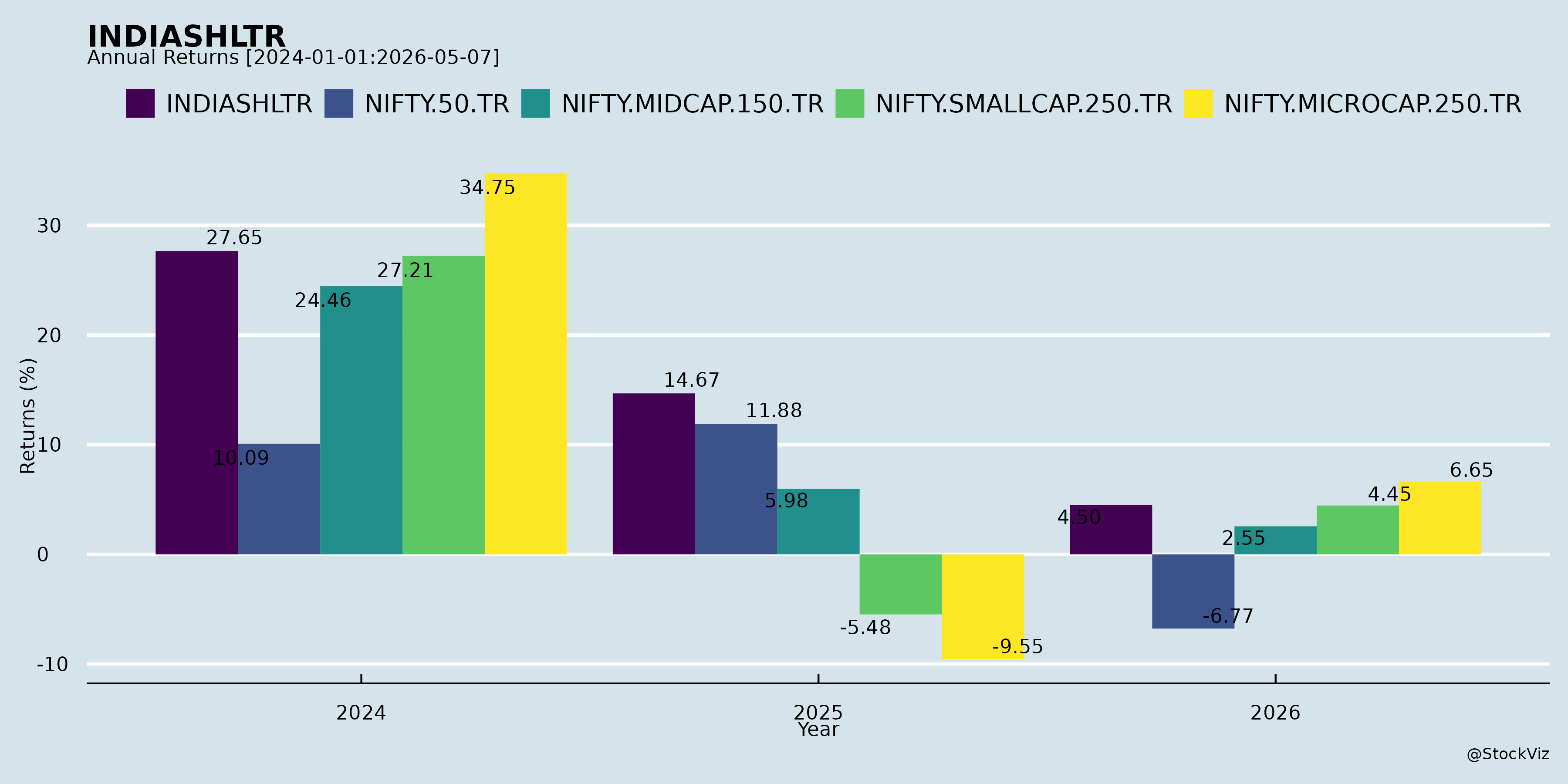

Annual Returns

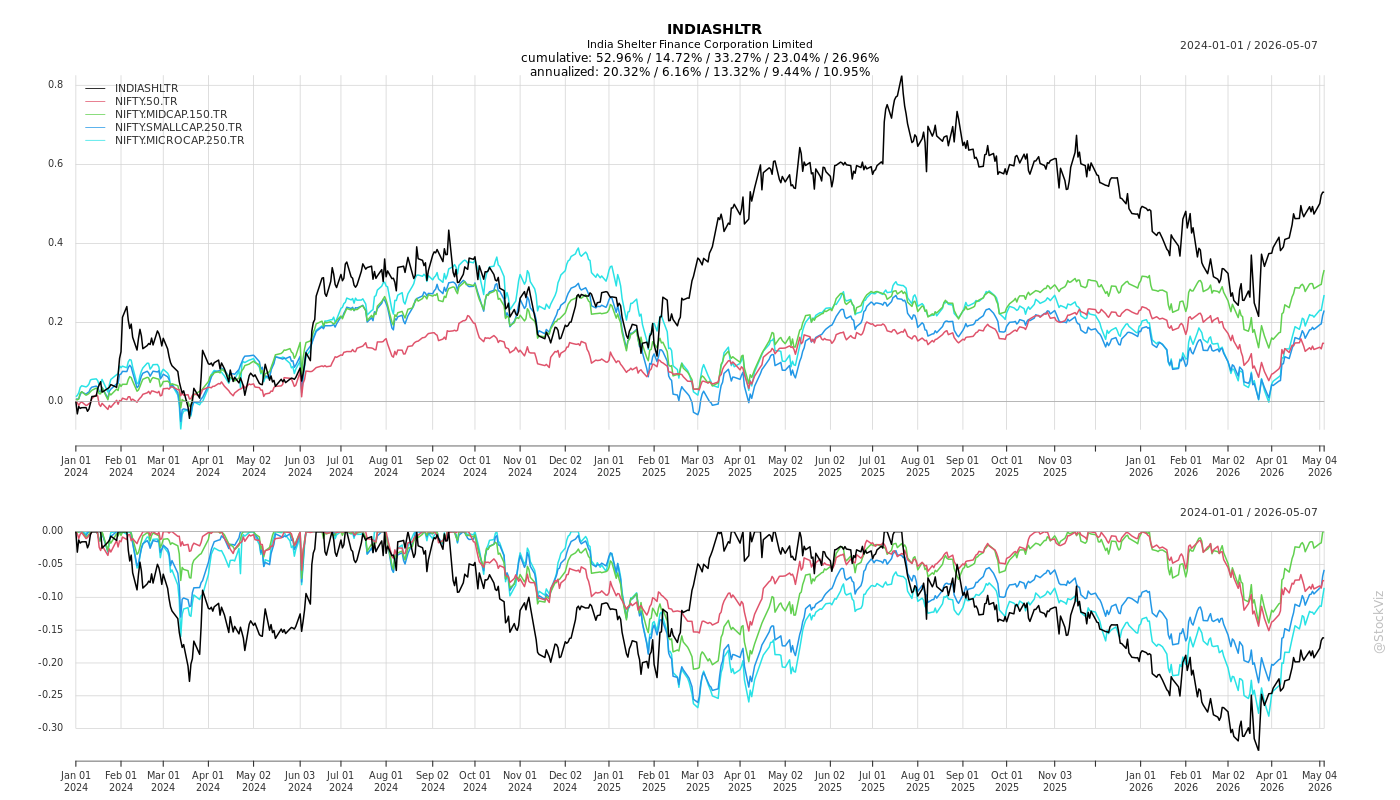

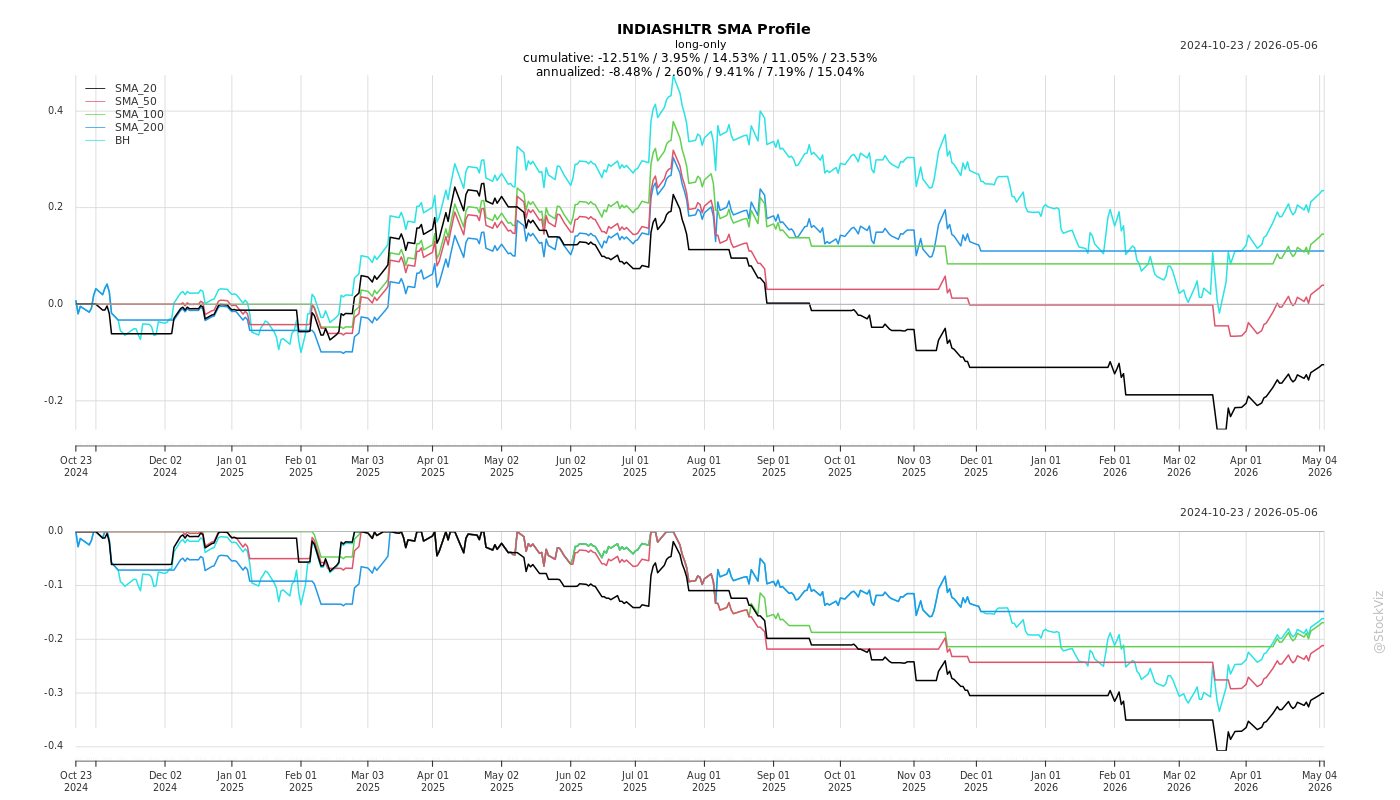

Cumulative Returns and Drawdowns

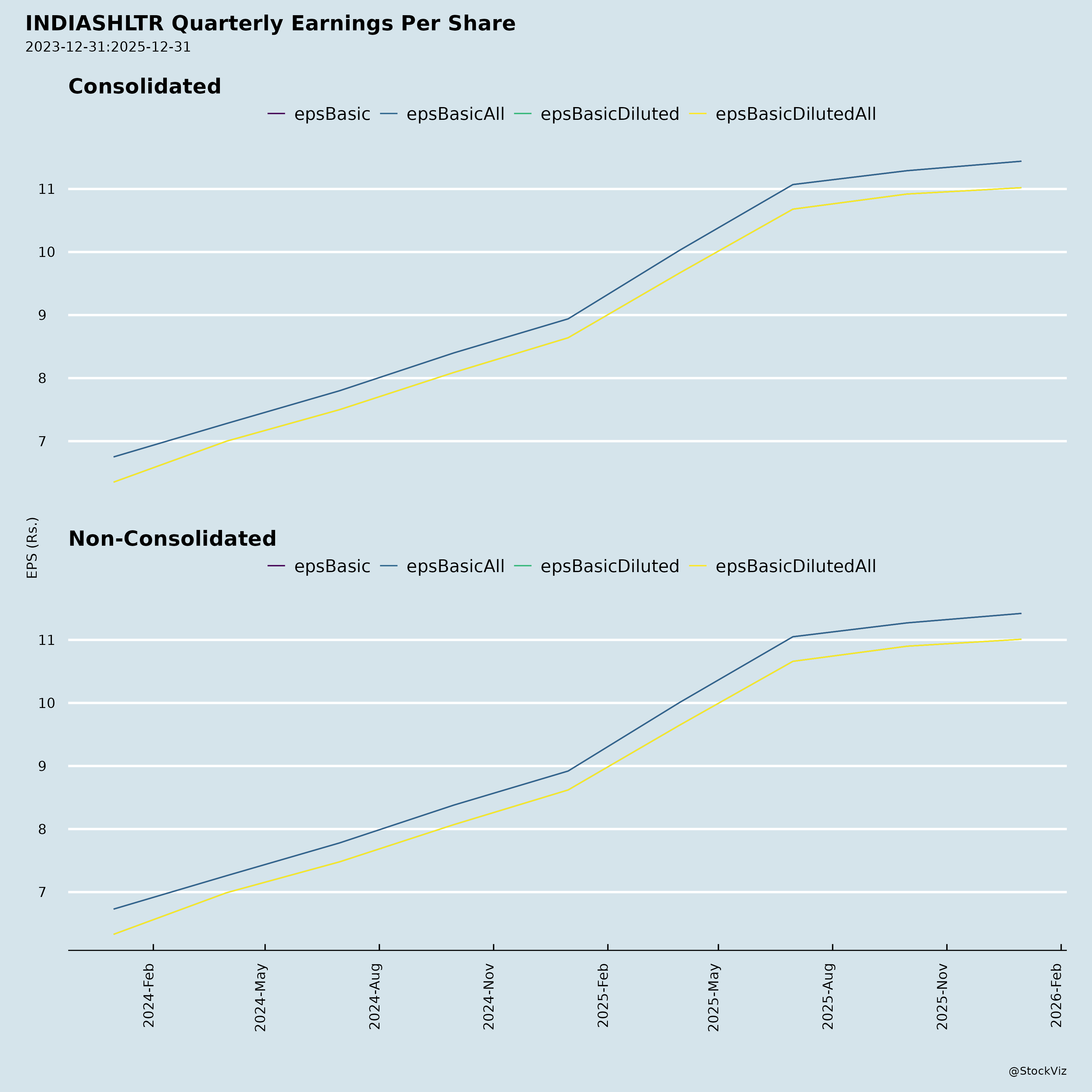

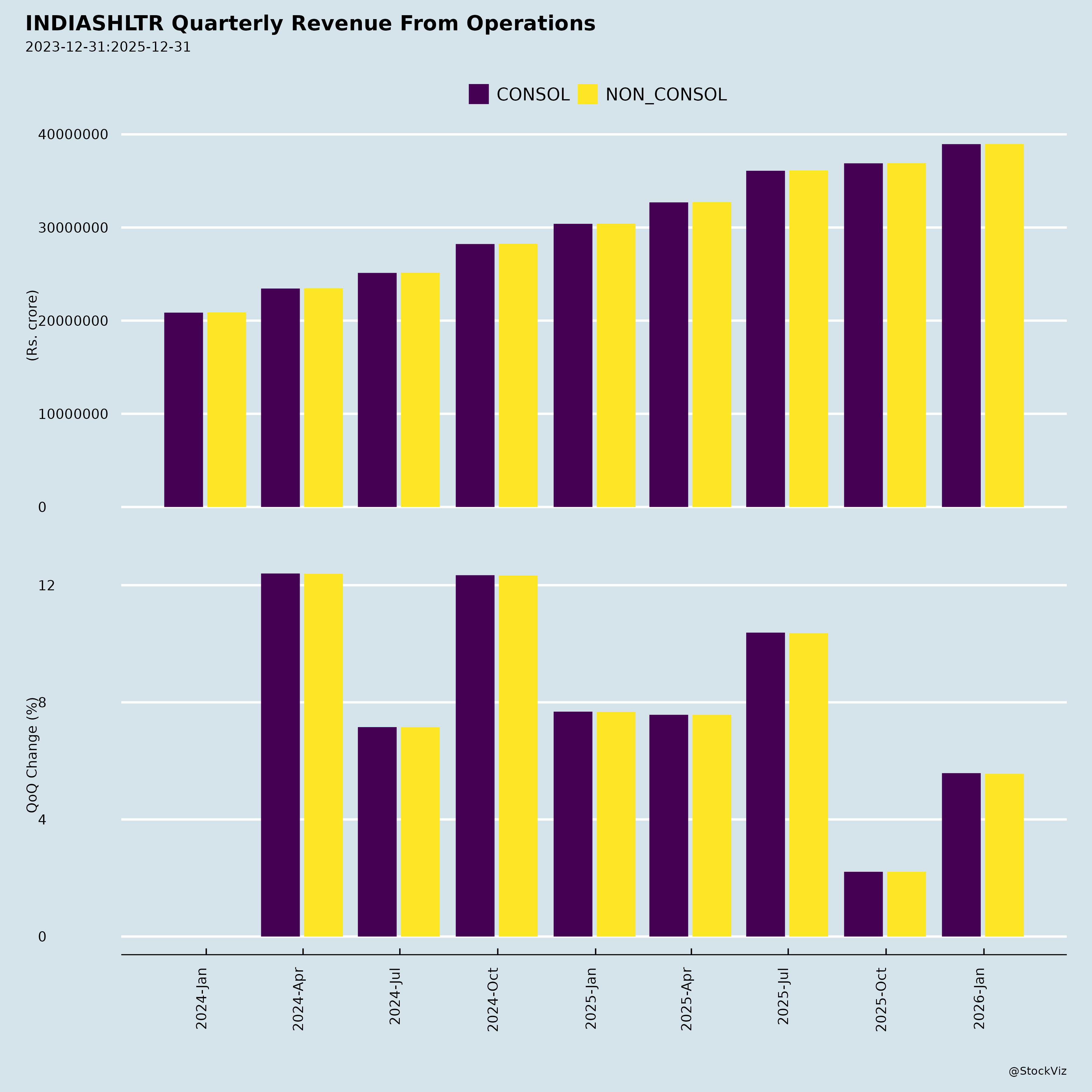

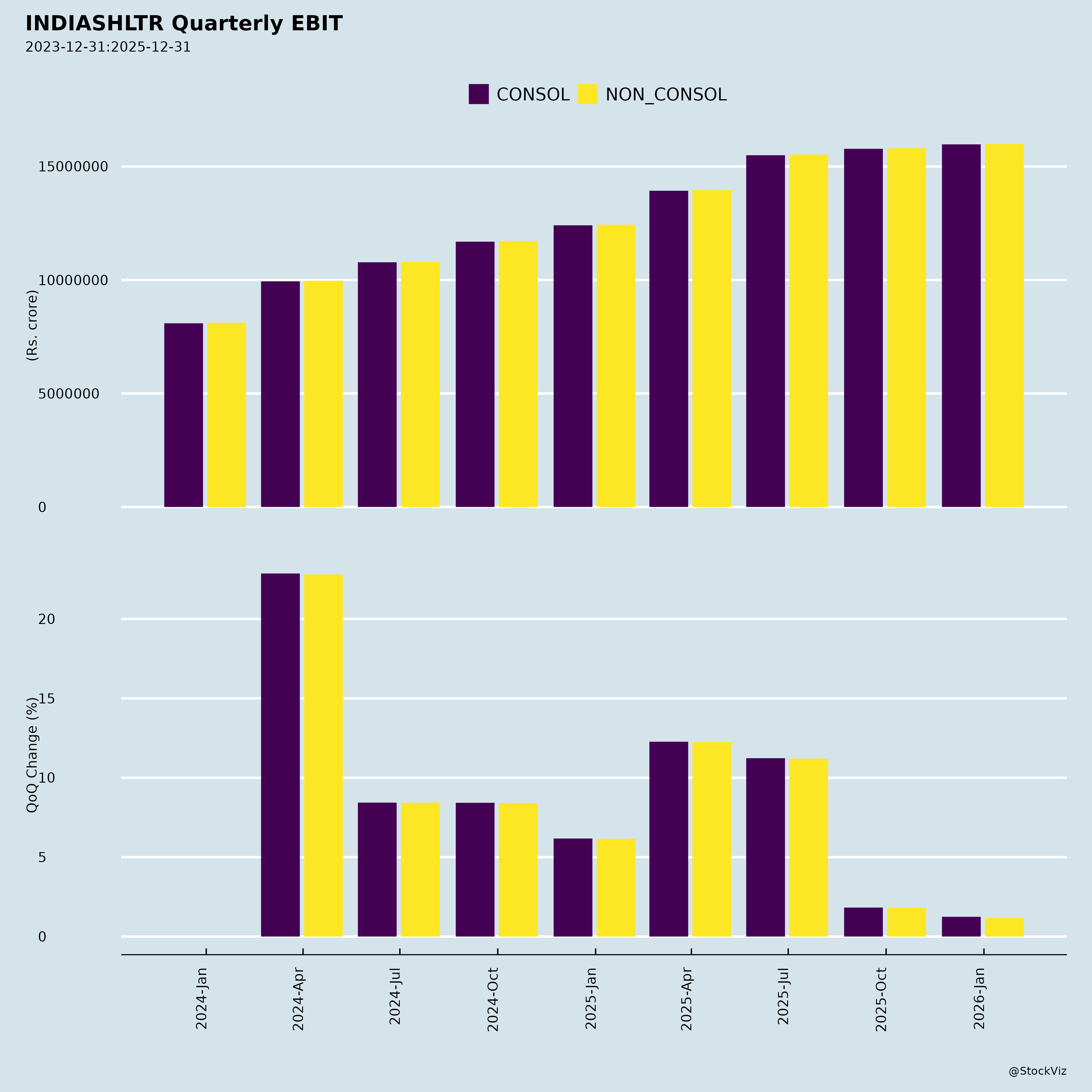

Fundamentals

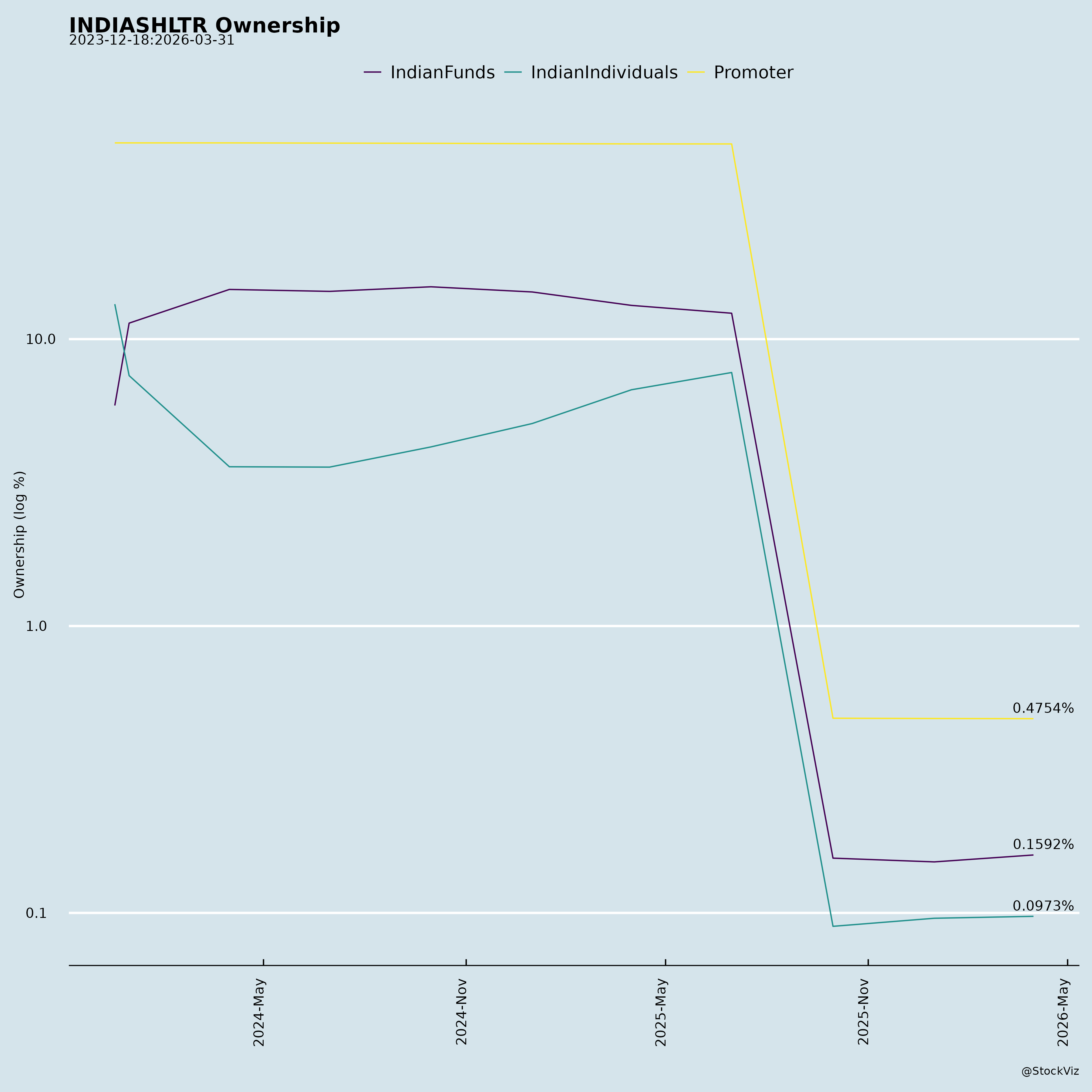

Ownership

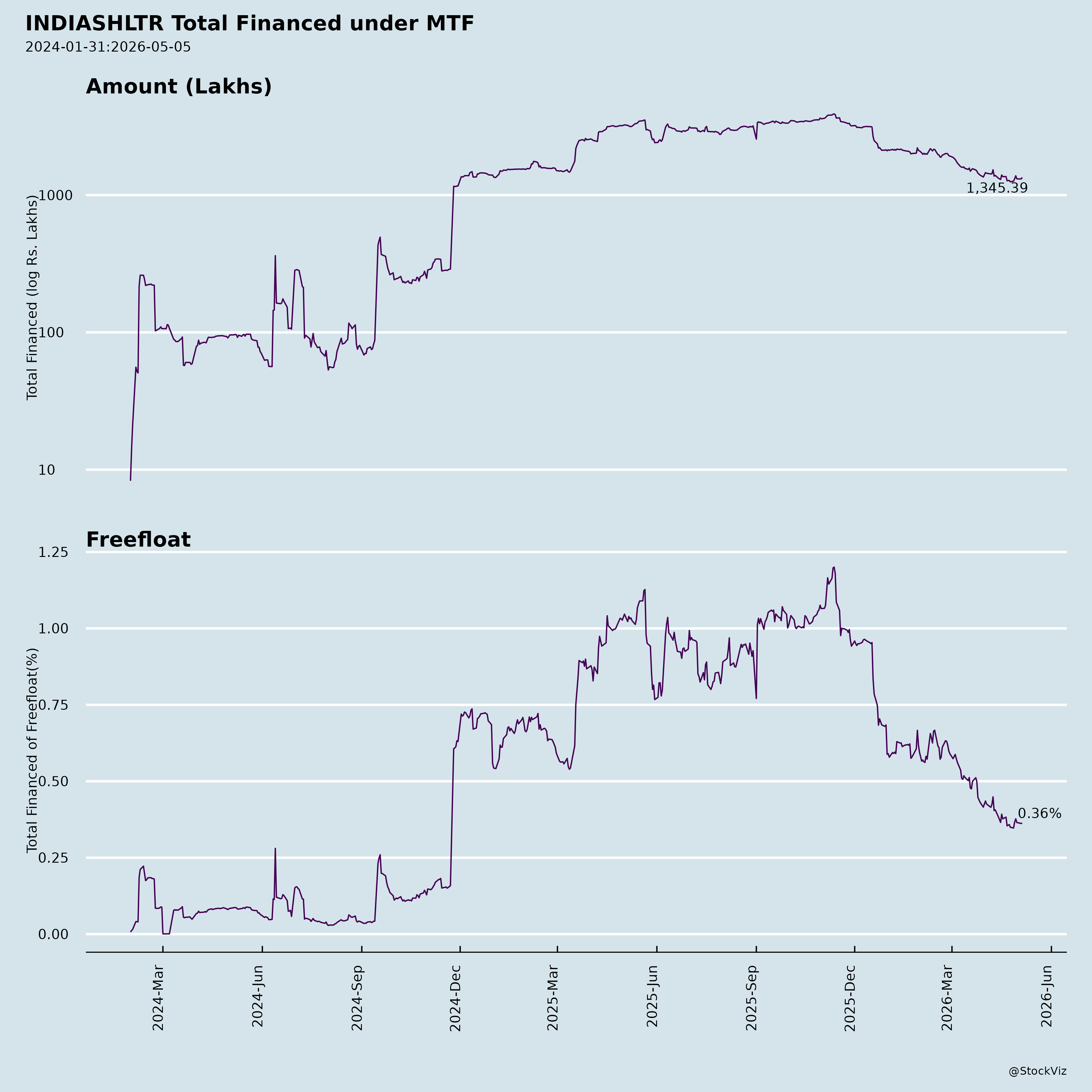

Margined

AI Summary

asof: 2025-12-03

Analysis of India Shelter Finance Corporation Limited (INDIASHLTR)

India Shelter Finance Corporation (ISFC) is a housing finance company focused on affordable home loans and loans against property (LAP) for low/middle-income (EWS/LIG), self-employed borrowers in Tier 2/3 cities (91% portfolio). Q2/H1 FY26 results show robust AUM growth (31% YoY to Rs.9,252 Cr), stable asset quality (Gross Stage 3 at 1.2%), and strong profitability (H1 PAT Rs.241 Cr, +39% YoY; RoE 17.2%). Below is a structured summary of tailwinds, headwinds, growth prospects, and key risks, based on the provided filings (investor presentation, financial results, board outcomes, etc.).

Tailwinds (Supportive Factors)

- Strong Execution & Growth Momentum: AUM +31% YoY (Rs.9,252 Cr), disbursements +18% YoY (H1 Rs.1,817 Cr). Branch network expanded to 299 (15 states, +9 QoQ), driving granular portfolio (ATS Rs.10L, 1.24L customers).

- Profitability & Efficiency: Spreads expanded to 6.4% (+30bps YoY), CoF down 10bps QoQ to 8.5%. H1 PAT +39% YoY, RoA 5.9%, RoE 17.2%. Opex/AUM improved to 4.2% (from 4.4%). High digital adoption (95% collections, 99% e-signing).

- Asset Quality Resilience: Gross/Net Stage 3 stable at 1.2%/0.9%; 30+ DPD 4.7%; PCR 25%; credit cost 0.5%. Proven through cycles (15-year vintage).

- Balance Sheet Strength: Networth Rs.2,915 Cr; liquidity Rs.2,082 Cr (16% of AUM); CRAR 57%; diversified funding (32 lenders, avg. tenure 8 yrs); ratings upgraded to AA-.

- Market Tailwinds: Underserved segment (72% EWS/LIG; housing shortage 100mn units, Rs.68tn loan demand). 100% secured book, LTV 52%, FOIR 49%.

- Governance & ESG: Experienced MD/CEO/board; ESOP alignment (9% pool); BRSR disclosure; high ESG score (69.9); women borrowers 69%.

Headwinds (Challenges)

- Moderating Disbursement Growth: Q2 +12% YoY (vs. 31% AUM), signaling potential demand softness or cautious underwriting amid high rates/self-employed exposure (75%).

- Margin Pressure: Spreads stable but CoF sticky; DA as % AUM at 16% (near guided 18% cap).

- Opex Scaling: Employee count 4,276 (+15% YoY); vintage-wise AUM/branch improving but new branches (40<1yr vintage) dilute productivity short-term.

- Geographic Concentration: Rajasthan 31% AUM (down from 41% in FY18, but still key).

- Macro/Regulatory: High interest rates, rural/semi-urban slowdown (91% Tier II/III); RBI scrutiny on co-lending/assignments (disclosures show Rs.66 Cr transferred).

Growth Prospects

- High Potential Market: Affordable housing penetration low (12% mortgage/GDP); EWS/LIG demand Rs.45tn. Target 25-30% AUM CAGR (historical 38% FY19-25).

- Distribution Expansion: Contiguous growth in 15 states; AUM/branch potential (mature >3yr: Rs.44 Cr vs. overall Rs.31 Cr).

- Product/Tech Leverage: 59% home loans (up from 57%); tech (BRE, Salesforce, AI) for scalability; digital collections 95%+.

- Funding Optimization: Long-term borrowings priority; co-lending scale-up; ratings support lower CoF.

- Profitability Upside: RoE path to 18-20% via spreads (target 6.5%+), opex leverage (to 3.5-4%), credit cost <0.5%.

- Projections: FY26 AUM Rs.11,000-12,000 Cr; PAT Rs.500-550 Cr (consensus-aligned); sustained 20%+ RoE.

Key Risks

| Risk Category | Description | Mitigants |

|---|---|---|

| Credit/Asset Quality | High self-employed (75%), Tier II/III exposure; 30+ DPD up to 4.7%. Potential slippage in slowdown. | Robust underwriting (in-house BRE, 100+ checks); stable Stage 3 (1.2%); PCR 25%. |

| Liquidity/Funding | Rising rates/CoF; reliance on banks (54% mix). | Rs.2,082 Cr buffer; diversified 32 lenders; strong ALM surplus. |

| Execution/Operational | Branch ramp-up risks; tech integration. | Proven scale (299 branches); 99% in-house sourcing. |

| Regulatory/Compliance | RBI norms (ECL, co-lending disclosures); HFC registration. | Compliant (CRAR 57%); non-material sub liquidation disclosed. |

| Macro/Economic | Rural distress, monsoons, elections; competition from banks/NBFCs. | Granular portfolio (ATS Rs.10L); 15-yr vintage resilience. |

| Concentration | Rajasthan 31%; LAP 41%. | Diversifying (e.g., UP 7%, TN 6%); home loans 59%. |

Overall Outlook: Positive. ISFC benefits from structural tailwinds in affordable housing, with execution strength (growth + quality). FY26 on track for 25-30% AUM/PAT growth; RoE >17%. Monitor disbursement momentum and macro stress. Valuation attractive at ~2.5x FY26 BVPS (peer avg. 3x+). Recommendation: Accumulate on dips. (Data as of Q2FY26; future performance not guaranteed.)

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.