Housing Finance Company

Industry Metrics

May 8, 2026

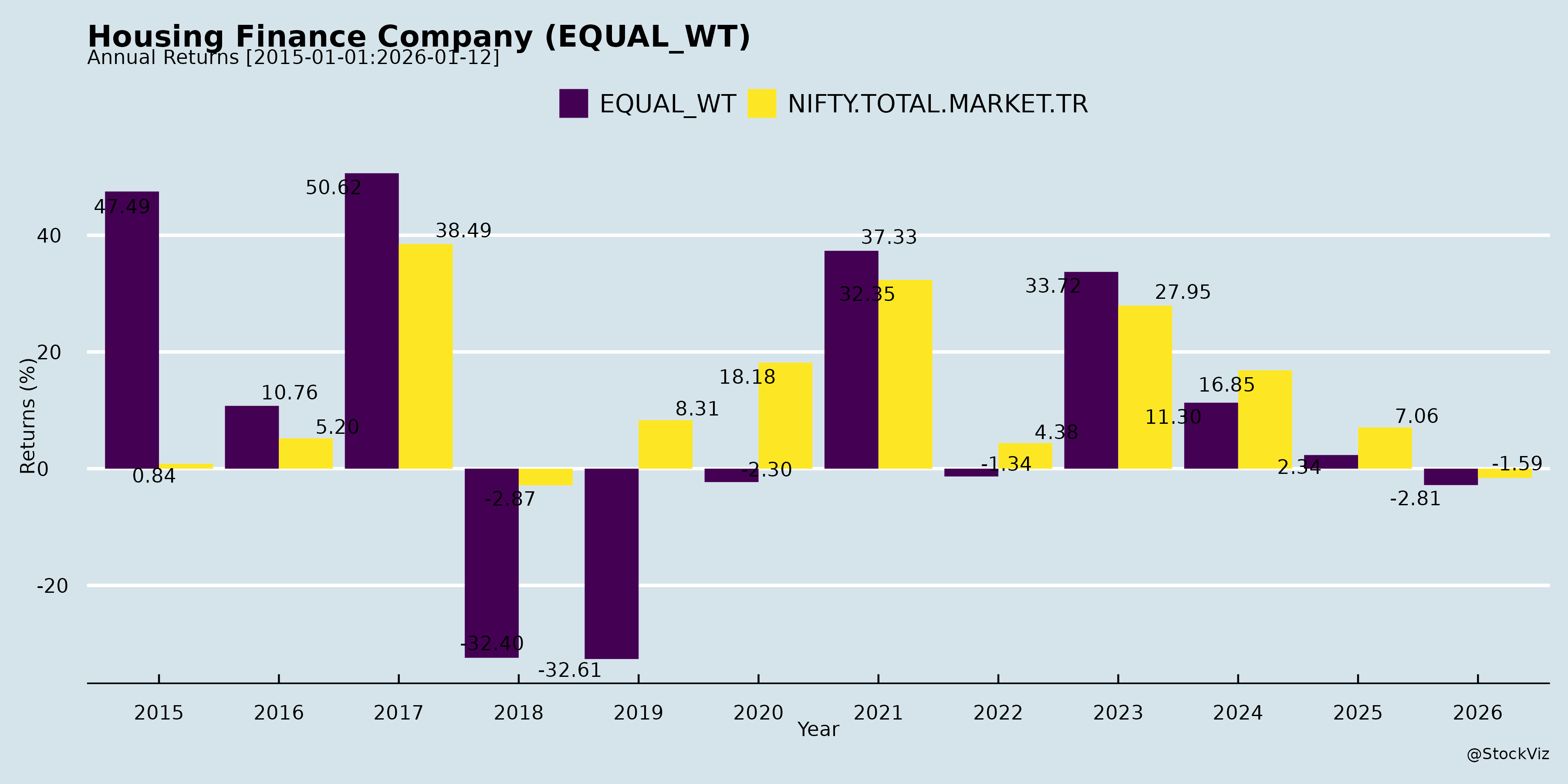

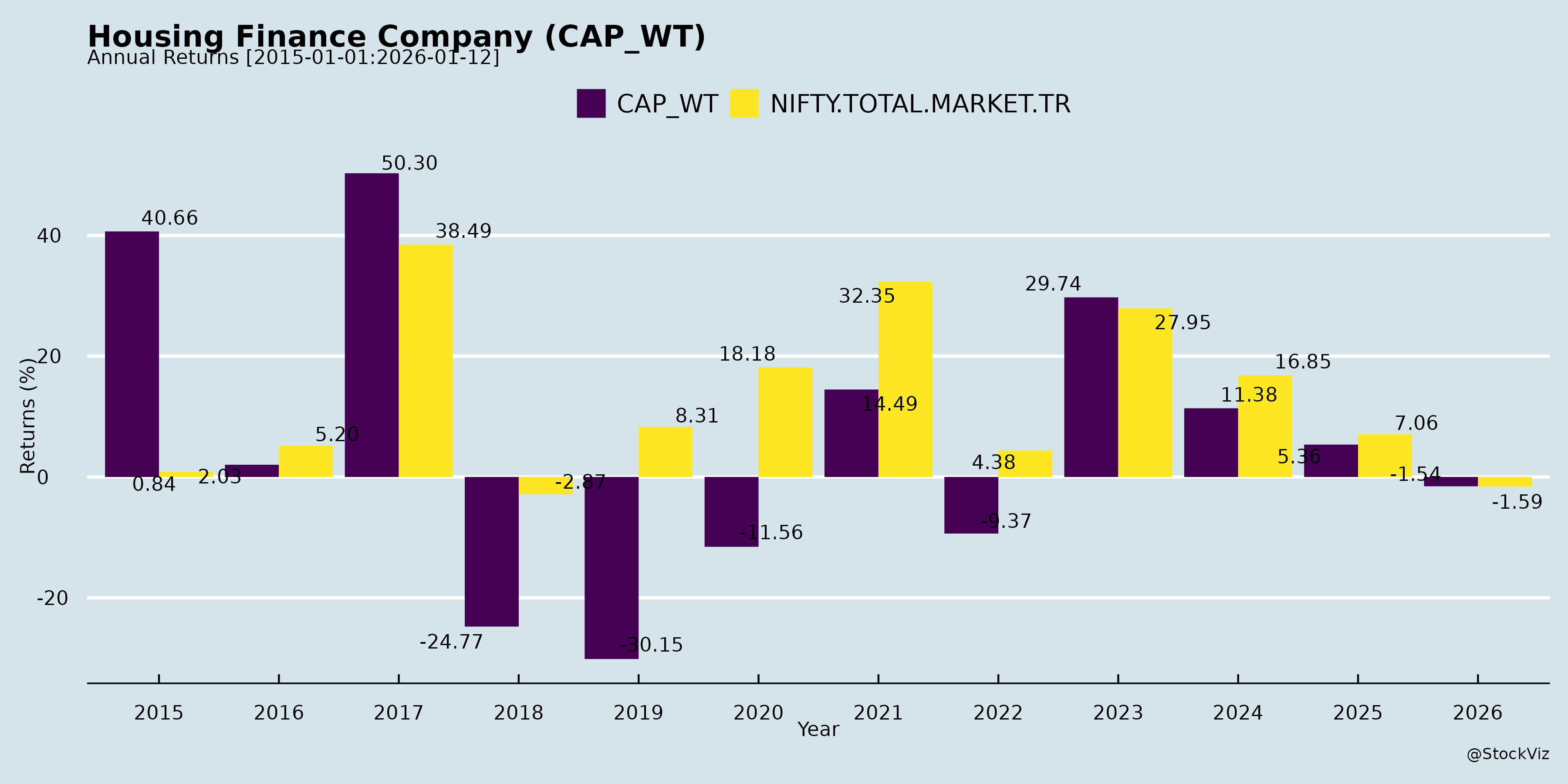

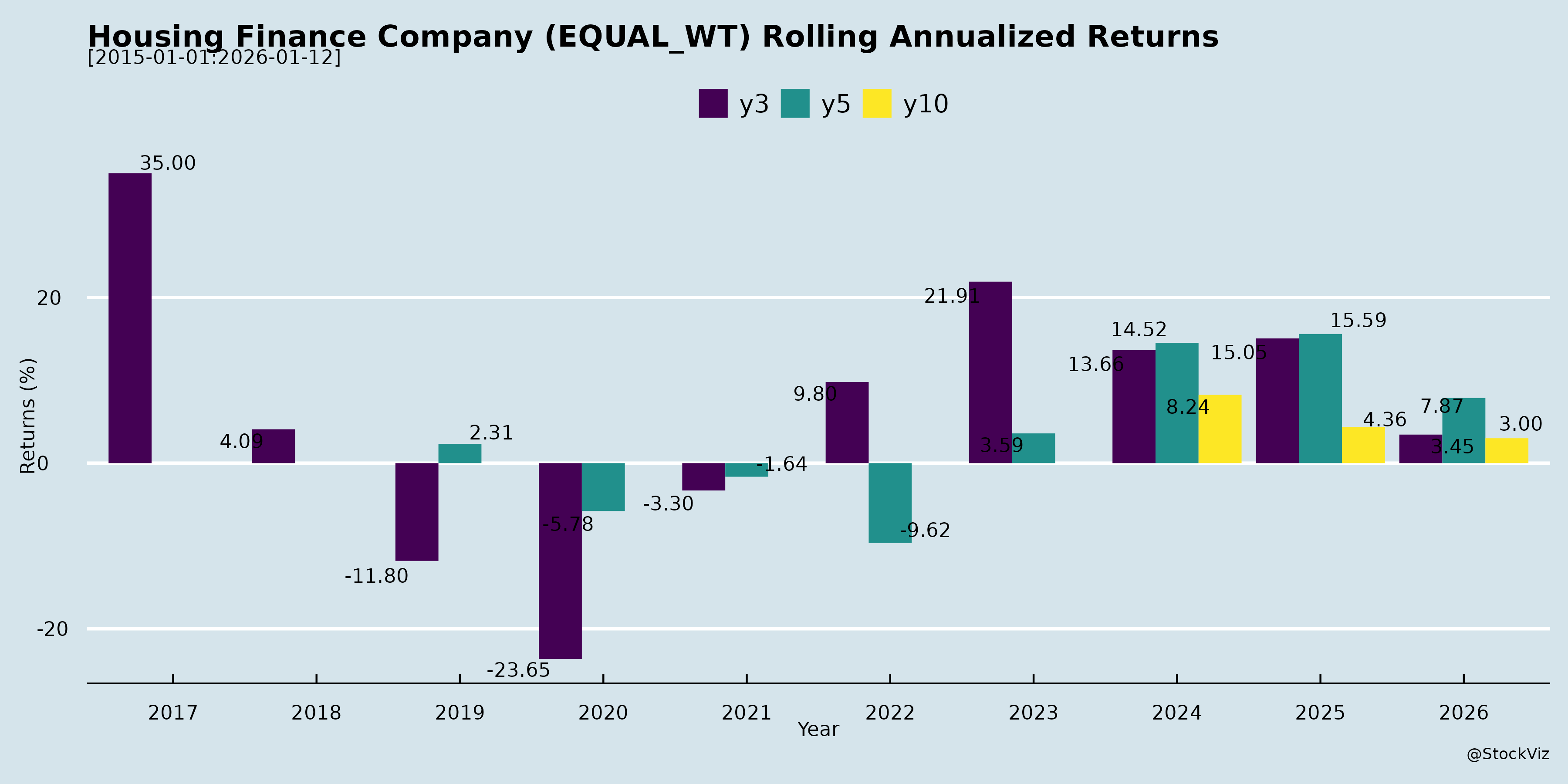

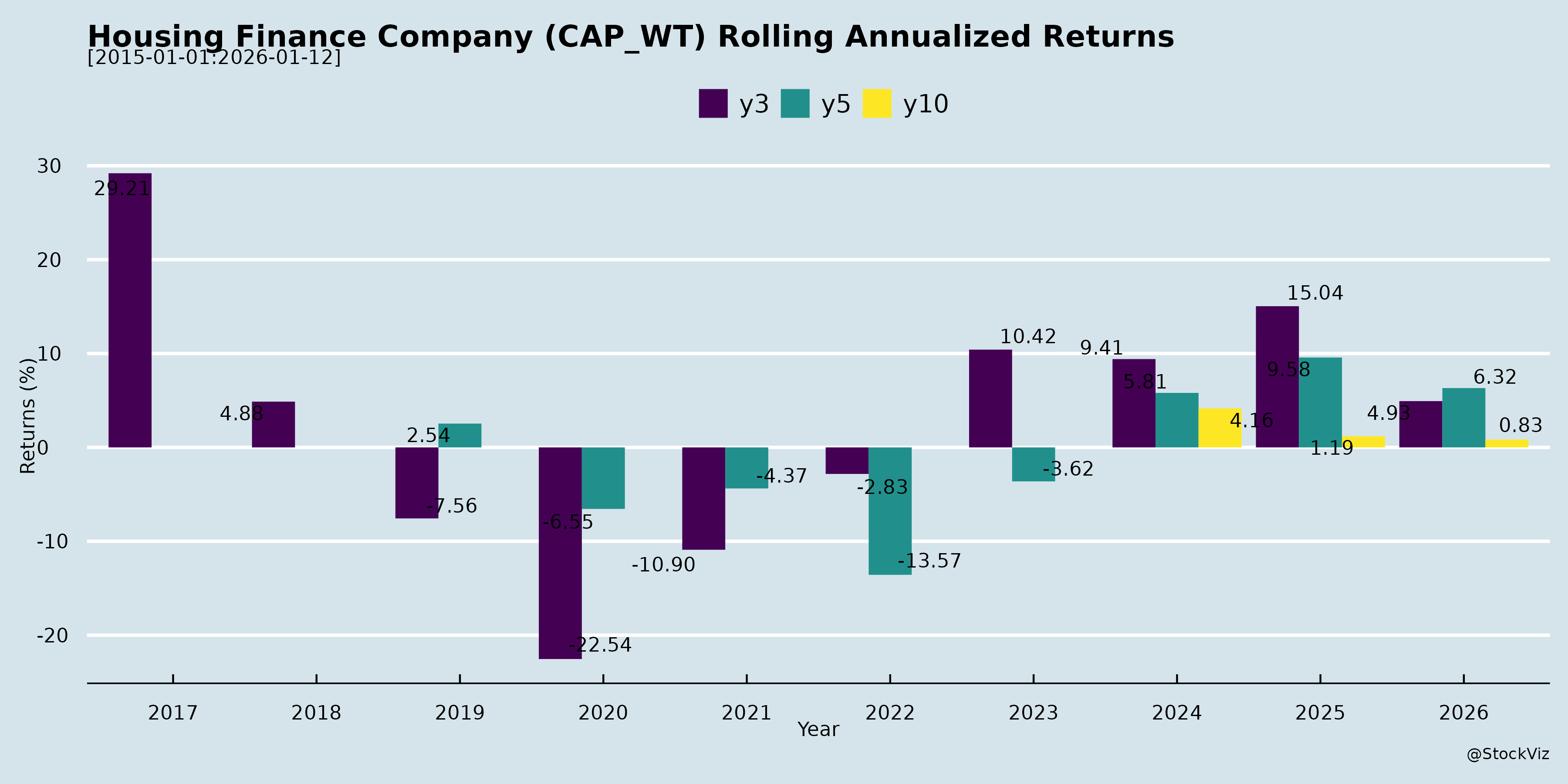

Annual Returns

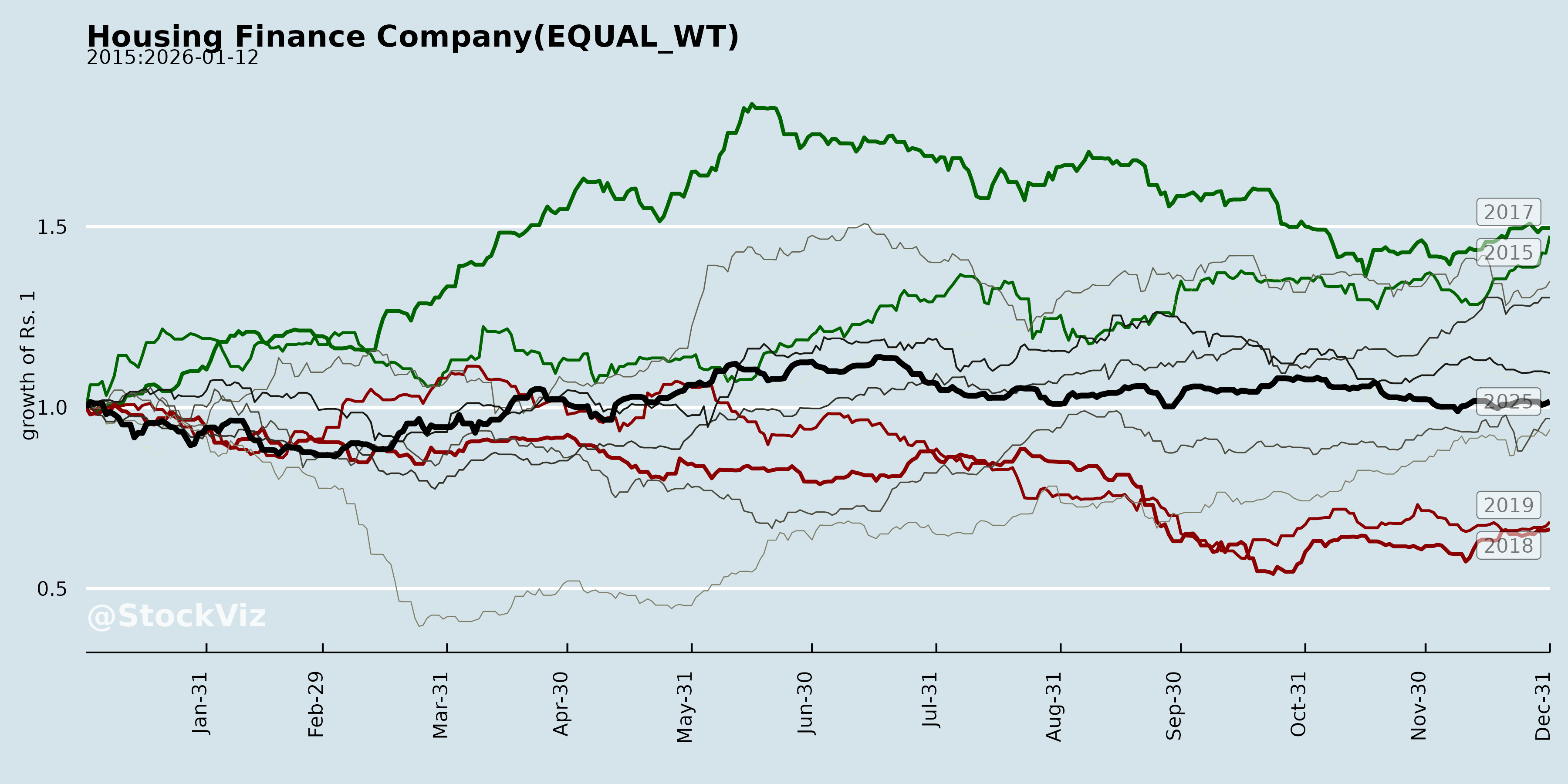

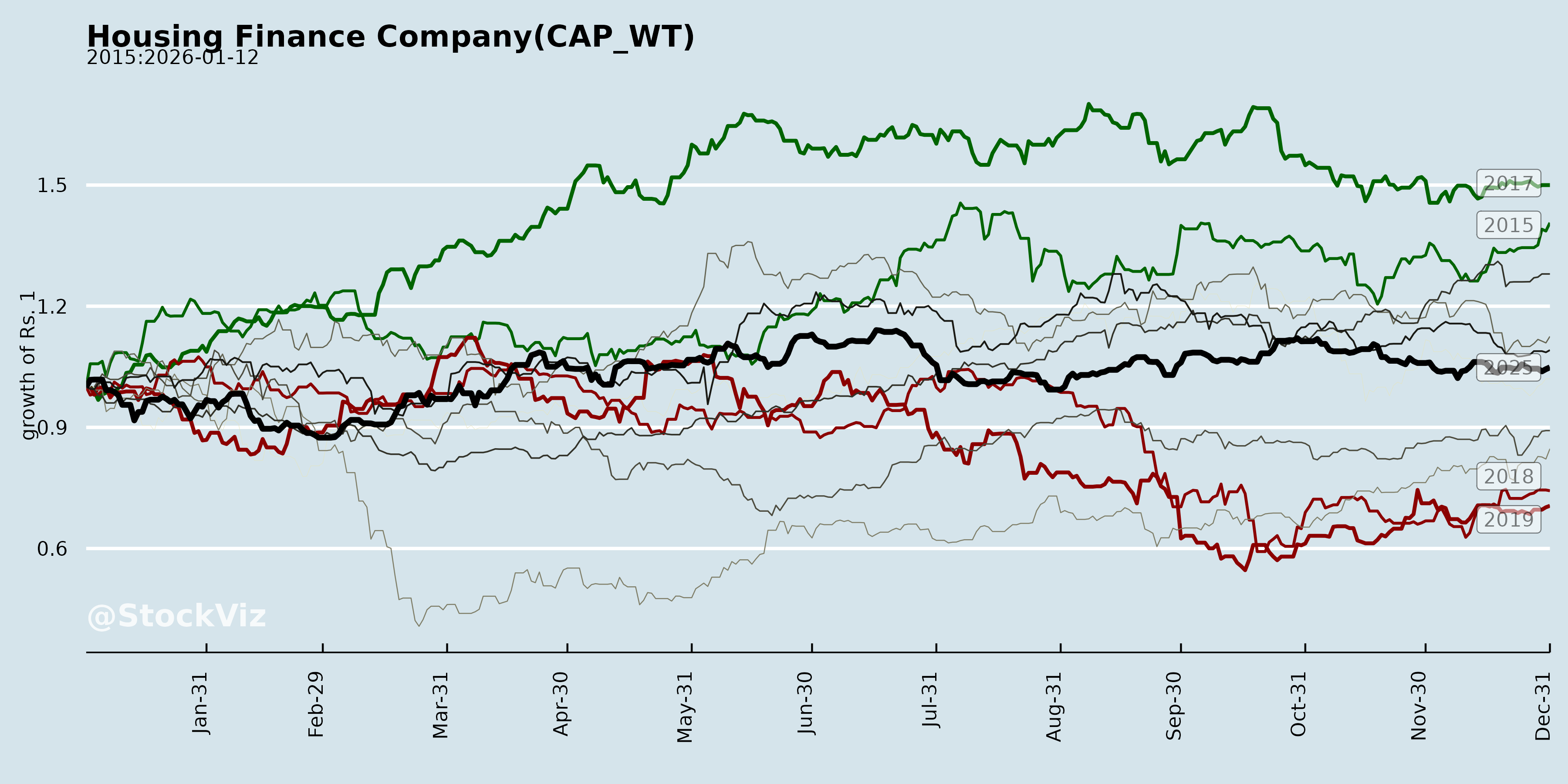

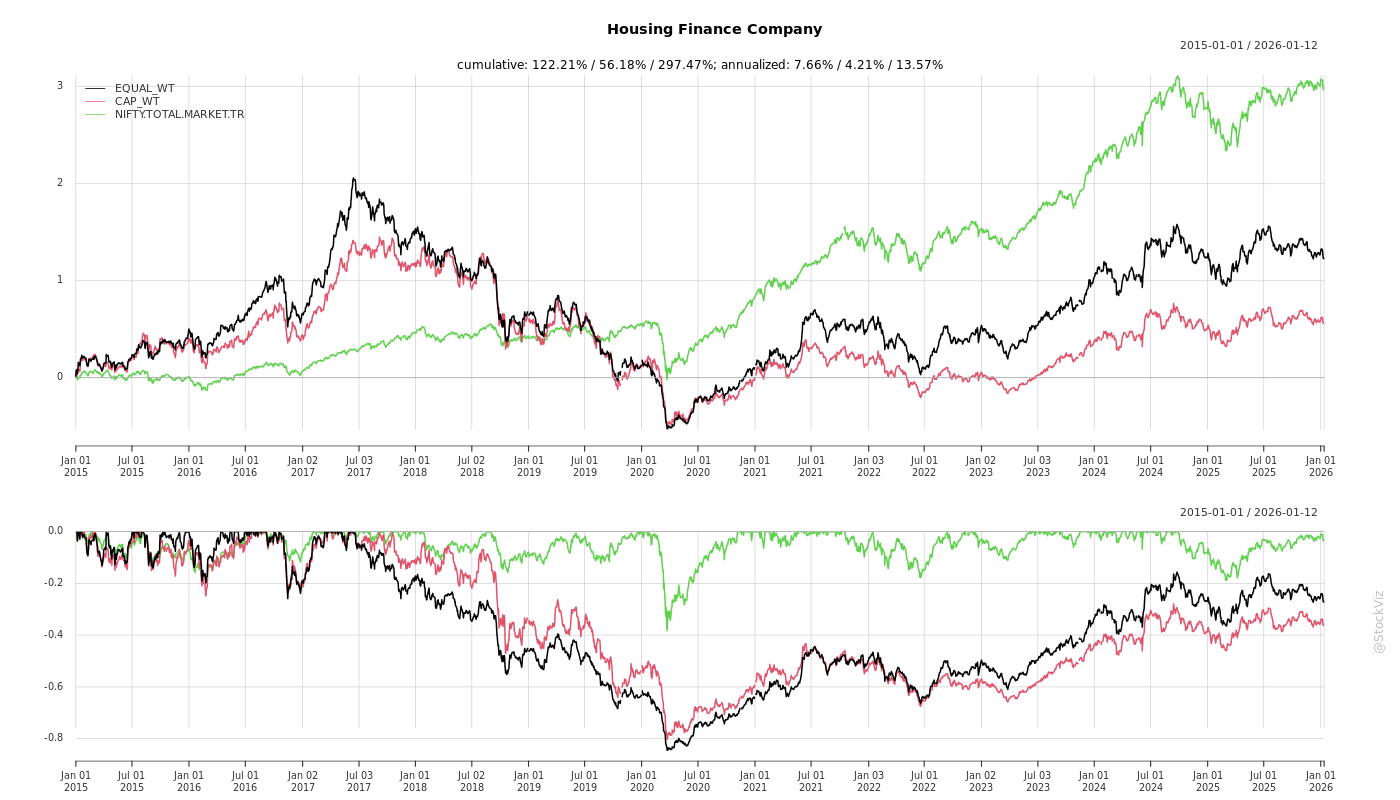

Cumulative Returns and Drawdowns

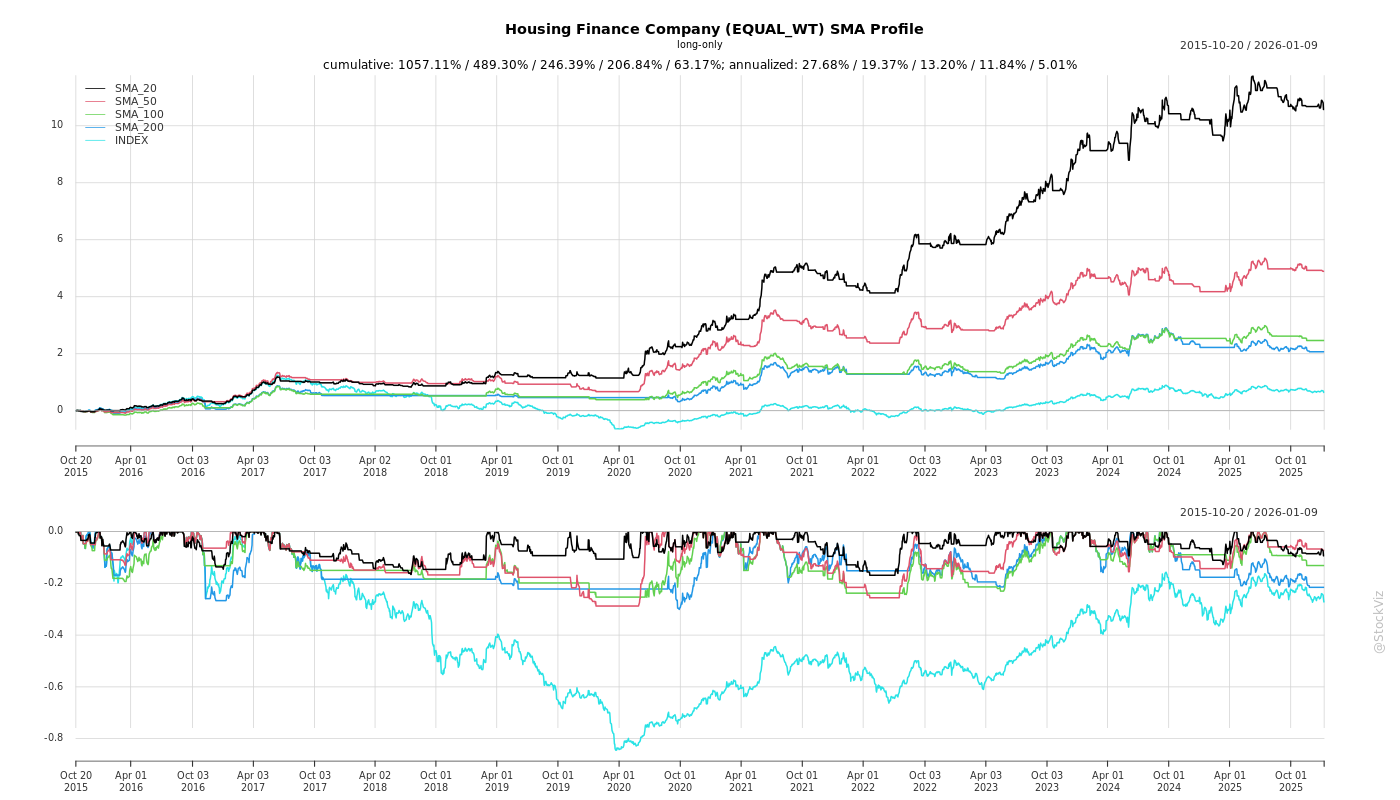

SMA Scenarios

Current Distance from SMA

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-16

The Evolution of Challenges

Historically, housing finance companies have had to navigate significant legacy hurdles, intense regional competition, and operational bottlenecks, which have steadily evolved over time:

- Overcoming Legacy Exposures and Legal Hurdles: Some companies have faced prolonged challenges stemming from their past leadership and legacy loan books. For example, Sammaan Capital has been dealing with a Public Interest Litigation (PIL) filed in 2019 regarding alleged quid pro quo transactions involving its erstwhile promoter [1-3]. Over the years, the challenge has evolved from an acute crisis to a sustained, methodical run-down of this legacy book, which has allowed the company to successfully reduce its debt by Rs 76,000 crores and distance itself entirely from the former promoter [4-6].

- Legacy Book Run-Downs Masking Growth: For established players like Repco Home Finance, a persistent challenge is that high volumes of new loan disbursements are often offset by the rapid run-down of their older, mature loan books due to prepayments and balance transfers (BT-outs) [7-10]. Because of these continuous run-downs, achieving double-digit Asset Under Management (AUM) growth remains a structural challenge, even when monthly disbursements reach record highs [7, 10].

- Asset Quality and Sticky Stage 2 Assets: Managing stressed assets has required long-term strategic shifts. Previously, Stage 2 assets for affordable housing financiers were alarmingly high—historically hovering around 14% for Repco [11]. Over time, this challenge has been systematically addressed by deploying dedicated collection verticals and recovery agencies, effectively bringing these assets down to 8%, with a further target of 7.5% [11-13].

- Geographic and Administrative Bottlenecks: Companies have faced hurdles in specific regional markets. For instance, growing competitive intensity from rival firms expanding into strongholds like Tamil Nadu has forced legacy players to rethink their market dominance [14, 15]. Furthermore, local administrative issues, such as unresolved e-Khata property documentation problems in Karnataka, have actively hindered disbursement speeds and branch growth in those specific areas [16, 17].

The Evolution of Opportunities

As companies have adapted to macroeconomic shifts and technological advancements, their growth opportunities have expanded far beyond traditional mortgage lending:

- Transformative Global Investments and Diversification: The influx of massive global capital is fundamentally reshaping the sector’s scale. A landmark example is the Abu Dhabi-based International Holding Company (IHC) acquiring a 41.5% stake in Sammaan Capital for approximately $1 billion [18]. This backing provides an opportunity for the company to transition from a pure-play mortgage financier into a diversified Non-Banking Financial Company (NBFC) [19]. Over the next few years, this enables the expansion of their product suite from 4 to over 15 loan products (including MSME, personal, business, and gold loans) and scaling their network from 200+ to 1,500+ branches by FY 2029 [20].

- Technological Automation and AI Integration: The technological landscape has evolved from basic digital record-keeping to advanced, enterprise-wide Artificial Intelligence (AI) deployments. Aadhar Housing Finance is currently moving beyond pilot programs to fully integrate AI-led underwriting co-pilots, drastically improving their speed, risk management, and governance [21]. Similarly, Aavas Financiers has utilized its technological transformation to cut the turnaround time from loan login to sanction down from 13 days to just 6 days [22]. Lenders are also deploying mobile applications and APIs for sourcing, field investigations, and digital KYC, while still carefully balancing this with the “human touch” necessary for assessing low-income, cash-salaried borrowers [23-26].

- Favorable Government Policies and Subsidies: Macroeconomic policies have matured to provide robust tailwinds for the affordable housing market. The introduction of the Pradhan Mantri Awas Yojana (PMAY) 2.0 Interest Subsidy Scheme has significantly improved housing affordability for first-time buyers in the Economically Weaker Section (EWS) and Low-Income Group (LIG) segments [27]. Thousands of customers are already receiving these interest subsidies, which, alongside the benefits of the GST 2.0 framework that reduces construction costs, is heavily driving credit demand [22, 27].

- Broadened Co-Lending Frameworks: Regulatory evolutions have opened up highly lucrative co-lending opportunities. New, more inclusive co-lending regulations allow housing finance companies to seamlessly partner with various financial entities—including banks and all-India financial institutions—to acquire assets [28, 29]. These asset-light models allow companies to cover a wider suite of loan products without absorbing the full balance sheet risk, heavily boosting operational efficiency and expected cost savings [30-32].

- Strategic Geographic Expansion: To counter regional competition, companies are evolving their footprints by heavily targeting under-penetrated Tier 2 and Tier 3 markets. Financiers are actively shifting their growth focus toward emerging urban regions in the Eastern and Western sections of India, specifically targeting states like Maharashtra, Madhya Pradesh, Rajasthan, Uttar Pradesh, and Uttarakhand [33-37].

What are the headwinds affecting this industry?

asof: 2026-04-16

The implementation of the new Labour Codes is a significant regulatory headwind affecting profitability across the housing finance industry. Following the Government of India’s notification of four new Labour Codes (which consolidate 29 existing labor laws), multiple companies have had to estimate and provision for increased employee benefit expenses, particularly related to past service costs, gratuity, and leave encashment [1-5]. For instance, Aadhar Housing Finance reported an incremental impact of Rs. 15.92 crores towards gratuity and compensated absences [5], while Repco Home Finance recognized approximately Rs. 5 crores for similar provisions [1, 6]. PNB Housing Finance and Aptus Value Housing Finance also cited financial impacts and one-time expenses related to these labor code changes [2, 4].

Legacy book rundowns and balance transfer-outs (BT-outs) pose a major structural challenge to maintaining strong Asset Under Management (AUM) growth. Older institutions are finding that despite logging high new loan disbursements, their net AUM growth remains muted because older, maturing loans are being rapidly paid down or transferred to competitors. Repco Home Finance noted that their monthly rundown is between Rs. 170 crores to Rs. 200 crores, which severely offsets their new disbursements [7-10]. Because the company is 25 years old, a significant portion of its older book has high principal appropriation, making the legacy book effect an ongoing structural headwind [8, 11, 12]. Similarly, Sammaan Capital continues to direct high priority toward managing and running down its legacy loan exposures inherited from an earlier era [13-15].

Intense regional competition is pressuring incumbents to defend their market share and forcing them to pivot their growth strategies. The entry and expansion of new players into specific geographic strongholds have heightened competitive intensity. For example, Repco Home Finance acknowledged growing competition in Tamil Nadu due to companies like Aavas expanding their footprint in the region [16-19]. To combat this, companies are being forced to aggressively focus on expanding into non-traditional states (such as western and eastern India) to dilute their regional concentration [17, 19].

Regional administrative and bureaucratic bottlenecks can unexpectedly stall disbursement targets. Repco Home Finance specifically highlighted that its growth in the state of Karnataka has been slower than expected due to unresolved “e-Khata” property documentation issues [20, 21]. Such localized administrative hurdles prevent housing finance companies from achieving their planned disbursement volumes in affected states [20, 21].

Macroeconomic uncertainties and seasonal collection volatility remain persistent risks. Home First Finance noted that the industry must navigate global uncertainties arising from trade, tariffs, and geopolitics, while also progressing out of a generally challenging credit cycle [22, 23]. Aavas Financiers similarly referenced operating within an overall “tight macro environment” [24]. Furthermore, localized and seasonal factors can disrupt cash flows; Aptus Value Housing Finance reported experiencing seasonal volatility in collections—particularly around festive periods—which caused a slight uptick in early delinquency metrics like 30+ Days Past Due (DPD) [25].

What are the key things to understand about this industry?

asof: 2026-04-16

The housing finance and Non-Banking Financial Company (NBFC) industry is undergoing significant transformation, characterized by distinct strategic shifts in target demographics, product offerings, technology adoption, and funding models. The key things to understand about this industry include:

1. Focus on Affordable, Low, and Middle-Income Segments The industry is heavily focused on penetrating the affordable housing market, specifically targeting first-time homebuyers, the Economically Weaker Section (EWS), and Low-Income Groups (LIG) [1-3]. Companies are strategically expanding their footprint into semi-urban, rural, and Tier 2/3 geographies to capture demand from these underserved communities [2-4]. Because a large portion of these customers—such as blue-collar workers and cash-salaried individuals—have limited access to formal banking credit, housing finance companies fill a critical gap in the market [5, 6].

2. Product Diversification Beyond Pureplay Mortgages While retail mortgages remain the core of the business, companies are evolving from pureplay mortgage lenders into diversified NBFCs [7]. To enhance their Return on Assets (RoA) and Return on Equity (RoE), lenders are broadening their product suites to include mid-market and low-income loan assets, such as secured and unsecured MSME financing, personal loans, business loans, gold loans, and Loans Against Property (LAP) [7-9].

3. Integration of Advanced Technology vs. “Touch and Feel” Underwriting Technological adoption is a major growth enabler, with institutions transitioning to digital-first operating models [3]. Companies are implementing comprehensive digital systems, including AI-led underwriting co-pilots, digital lead onboarding, e-KYC, e-payment gateways for disbursals, and the utilization of account aggregator data and credit bureau insights [3, 10, 11]. Some companies execute over 92% of their agreements digitally and route more than 94% of collections through digital channels [11].

However, traditional personal interaction remains critical for risk assessment [5]. Because the target customer base often lacks vanilla, easily verifiable salaried profiles, a 100% tech-driven approach is not always feasible [5]. The physical “touch and feel” of the customer through personal discussions and field investigations is essential to properly assess the risk of self-employed and low-income borrowers [5, 12].

4. Asset-Light Models and Diverse Sourcing Channels To scale responsibly, companies are increasingly adopting asset-light strategies and co-lending arrangements [13, 14]. Co-lending regulations have become highly inclusive, allowing housing finance companies to technically integrate and originate loans in partnership with banks, other NBFCs, and financial institutions across all loan types [14-16].

On the origination front, growth is driven by highly diversified sourcing channels. Lenders maintain a balanced mix of internal direct sales teams, brand sales managers, and third-party empanelments like Direct Selling Agents (DSAs) and connectors to drive loan disbursements [17-19]. For instance, some firms actively balance their growth to come 50% from internal teams and 50% from DSA channels [20, 21].

5. Robust Funding and Asset Liability Management (ALM) Access to diversified funding at competitive pricing is a cornerstone of the industry [22]. Companies secure capital through various avenues, including bank term loans, National Housing Bank (NHB) financing, External Commercial Borrowings (ECB), issuance of Non-Convertible Debentures (NCDs), and Pass-Through Certificates (PTCs) [3, 23]. Maintaining a stable, well-matched Asset Liability Management (ALM) position with adequate liquidity in all maturity buckets is an area of high focus to ensure companies can reliably fuel their disbursement requirements [24-26].

6. Stringent Asset Quality and Legacy Book Resolution Managing asset quality and reducing credit costs are ongoing priorities [27, 28]. Companies dedicate significant resources to running down “legacy” loan books—older exposures that do not align with their current forward-looking, retail-focused strategies [29-31]. To improve portfolio health, management teams actively focus on recovering cash and reducing non-performing assets (NPAs), specifically targeting the steady reduction of sticky “Stage 2” and “Stage 3” bad assets through dedicated collection verticals and legal actions like SARFAESI notices [28, 32-34].

What are the tailwinds affecting this industry?

asof: 2026-04-16

Favorable Macroeconomic Landscape and Formalization The housing finance and NBFC industry is operating within a highly resilient Indian economy, which remains one of the fastest-growing major economies globally despite global uncertainties stemming from trade, tariffs, and geopolitics [1, 2]. Recent macroeconomic developments, including progress on India-US trade engagements, have further strengthened the country’s economic outlook [3]. Furthermore, the increasing formalization of the Indian economy, paired with strong regulatory oversight from the Reserve Bank of India (RBI), has positioned NBFCs perfectly to advance financial inclusion and bridge the gap between traditional banking and rising consumer credit demand [2].

Government Policies and Subsidy Schemes A highly supportive government policy landscape acts as one of the most significant tailwinds for the sector, particularly for affordable and low-income housing [1, 4]. The government’s Atmanirbhar Union Budget and its continued focus on capital expenditure (capex), affordable housing, and developing tier-2 and tier-3 markets reinforce a positive structural backdrop for Housing Finance Companies (HFCs) and NBFCs [3].

Crucially, government initiatives like the Pradhan Mantri Awas Yojana (PMAY) 2.0 and its Interest Subsidy Scheme (ISS) are playing a massive role in driving consumer demand [4, 5]. By providing direct interest subsidies, this scheme has substantially improved housing affordability and bolstered sentiment for first-time homebuyers, particularly within the Economically Weaker Section (EWS) and Low-Income Group (LIG) segments [4, 5]. Furthermore, industry leaders anticipate that forthcoming Union Budgets will continue to provide additional boosts and thrusts to the housing sector to support sustained demand [6, 7].

Tax Frameworks and Construction Costs The real estate and housing finance market is directly benefiting from the ongoing advantages of the GST 2.0 framework [4]. This optimized tax structure reduces overall construction costs for property developers, thereby placing the housing market on a much stronger structural footing and encouraging highly resilient buyer sentiment [4].

Conducive Interest Rates and Liquidity The sector is currently experiencing a highly favorable interest rate environment and supportive market liquidity, which are collectively improving the conditions for robust credit growth [3, 5]. Reductions in overall borrowing costs for housing financiers have directly supported margin expansion and increased profitability across the industry [6].

Firm Property Prices and Sustained Demand Overall market dynamics point to sustained housing demand and healthy credit growth [6, 7]. This resilient homebuyer sentiment is further backed by firm and stable property prices, establishing a strong, low-risk foundation for lending activities and sustainable expansion in the housing finance sector [3].

What is the general outlook of this industry?

asof: 2026-04-16

The general outlook for the housing finance and Non-Banking Financial Company (NBFC) industry is highly positive, driven by strong macroeconomic tailwinds, robust credit demand, and highly supportive government policies.

Economic Resilience and the Role of NBFCs India remains one of the world’s fastest-growing major economies, demonstrating continued resilience despite global uncertainties arising from trade, tariffs, and geopolitics [1, 2]. Within this formalized economic landscape, the NBFC sector is playing a pivotal role in bridging the gap between traditional banking and the rising demand for credit [1]. Bolstered by strong regulatory oversight from the Reserve Bank of India, NBFCs and Housing Finance Companies (HFCs) are well-positioned to advance financial inclusion and sustain the country’s growth momentum [1, 3].

Supportive Government Policies and Initiatives The policy landscape has turned highly favorable, reinforcing a positive structural backdrop for housing finance, especially in the affordable housing segment and tier-2 and tier-3 markets [2, 3]. Key government drivers include: * Pradhan Mantri Awas Yojana (PMAY) 2.0: The Interest Subsidy Scheme (ISS) under PMAY 2.0 is playing a critical role in driving demand across the low-income and affordable housing segments [4]. By improving affordability for first-time homebuyers—particularly in the Economically Weaker Section (EWS) and Low-Income Group (LIG) segments—the scheme continues to bolster homebuyer sentiment and drive disbursement growth [4, 5]. * GST 2.0 Framework: The ongoing benefits of the GST 2.0 framework are actively reducing construction costs for developers, placing the housing market on a very strong footing as the industry moves deep into 2026 [4]. * Union Budget and Capex Thrust: Initiatives from the Atmanirbhar Union Budget, along with a continued focus on capital expenditure, are expected to provide an additional boost to the housing sector [3, 6]. This continuous government thrust is anticipated to support sustained demand and healthy credit growth moving forward [6].

Favorable Liquidity and Interest Rate Environment Recent macroeconomic developments, alongside progress in India-US trade engagements, have strengthened India’s overall outlook by supporting market liquidity and creating a conducive interest rate environment [3]. This supportive rate backdrop, combined with firm property prices and resilient buyer sentiment, is actively improving the conditions for credit growth across the industry [3, 4].

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.