HINDUNILVR

Equity Metrics

May 8, 2026

Hindustan Unilever Limited

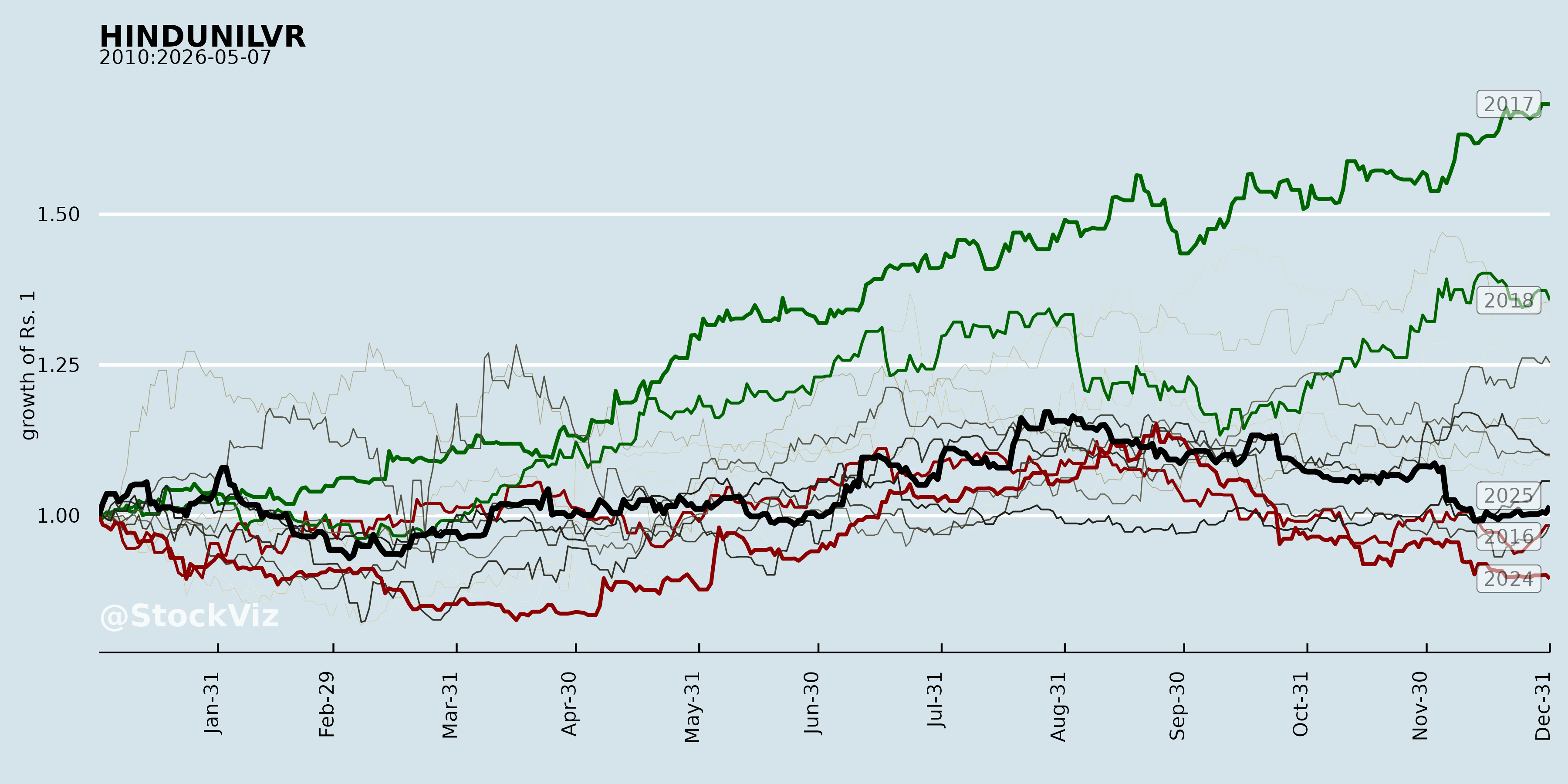

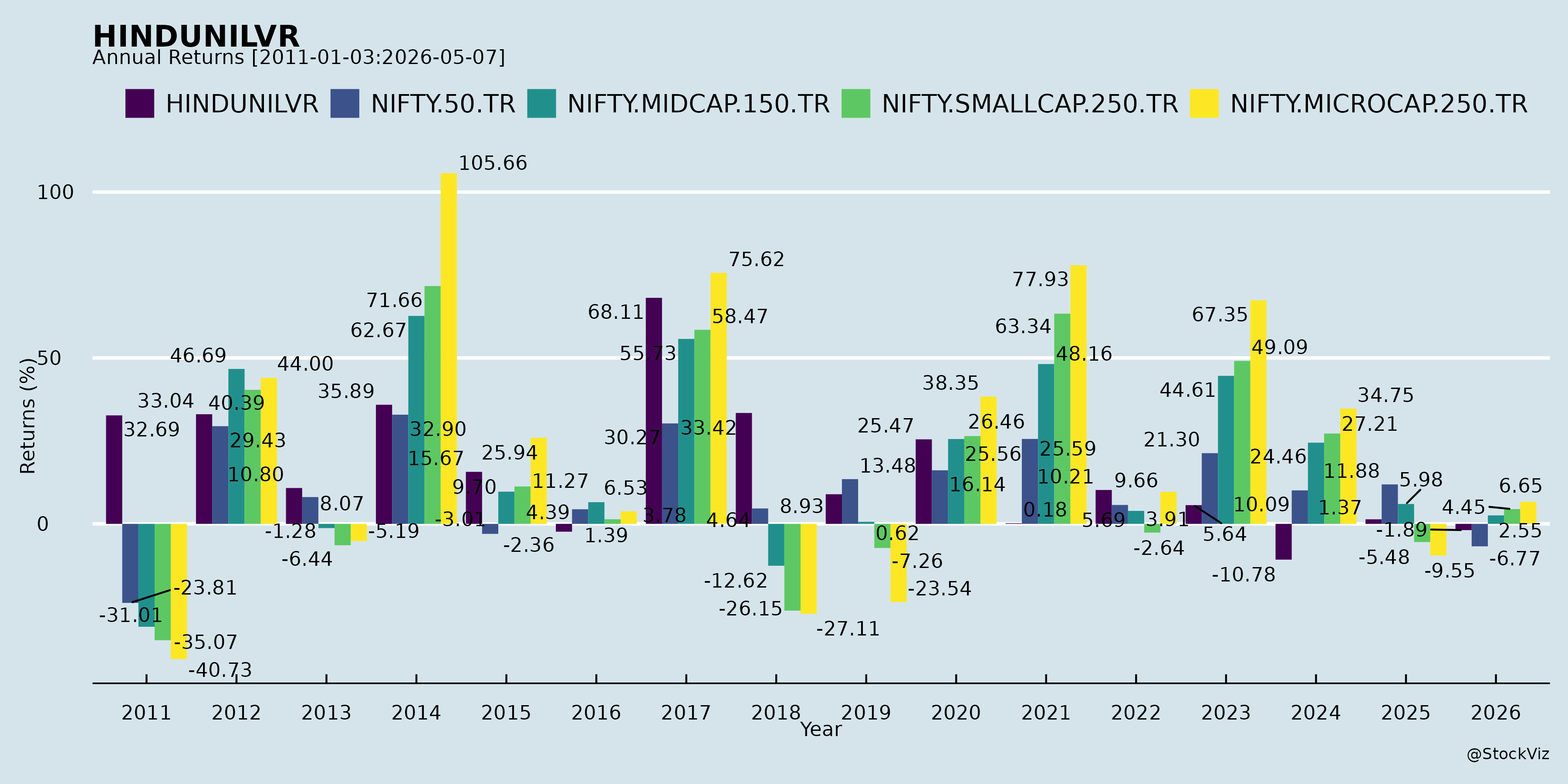

Annual Returns

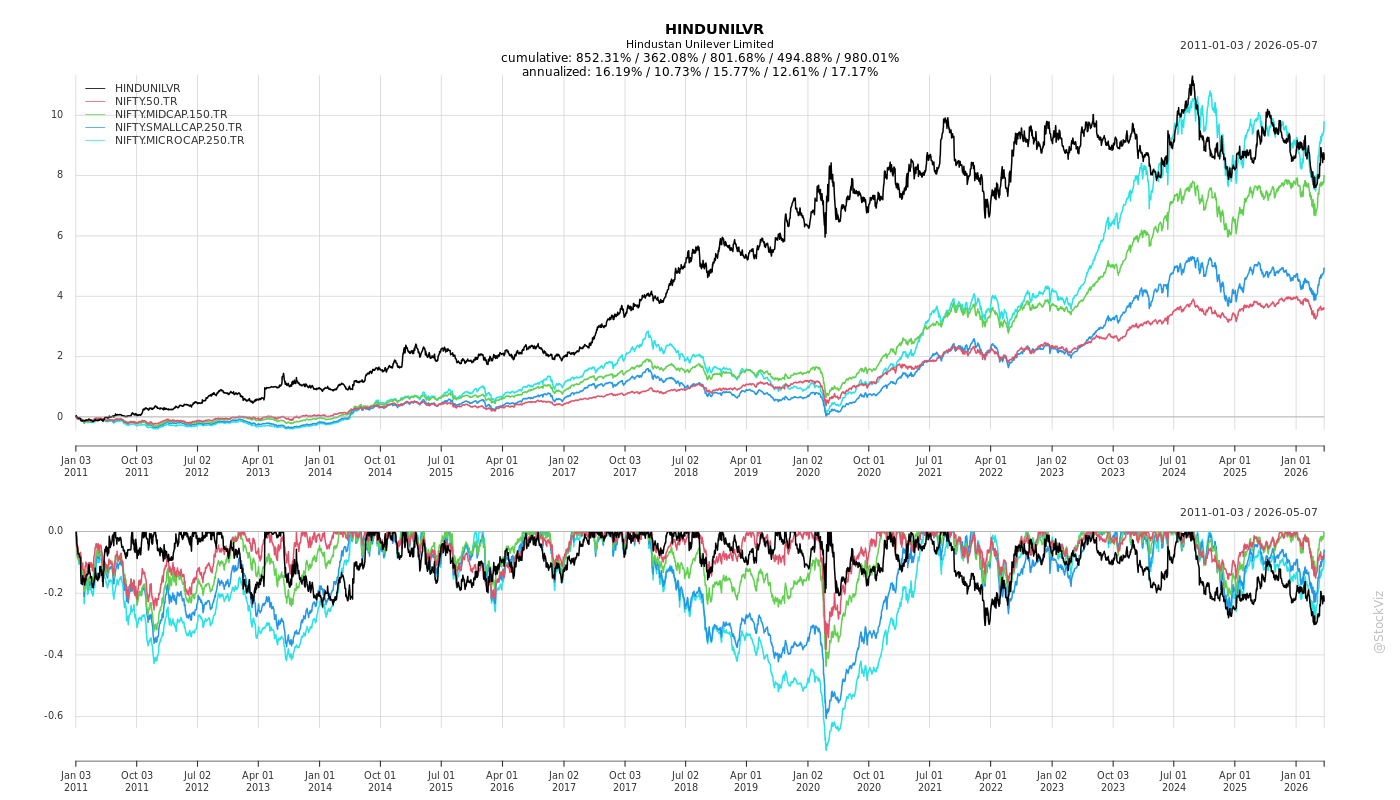

Cumulative Returns and Drawdowns

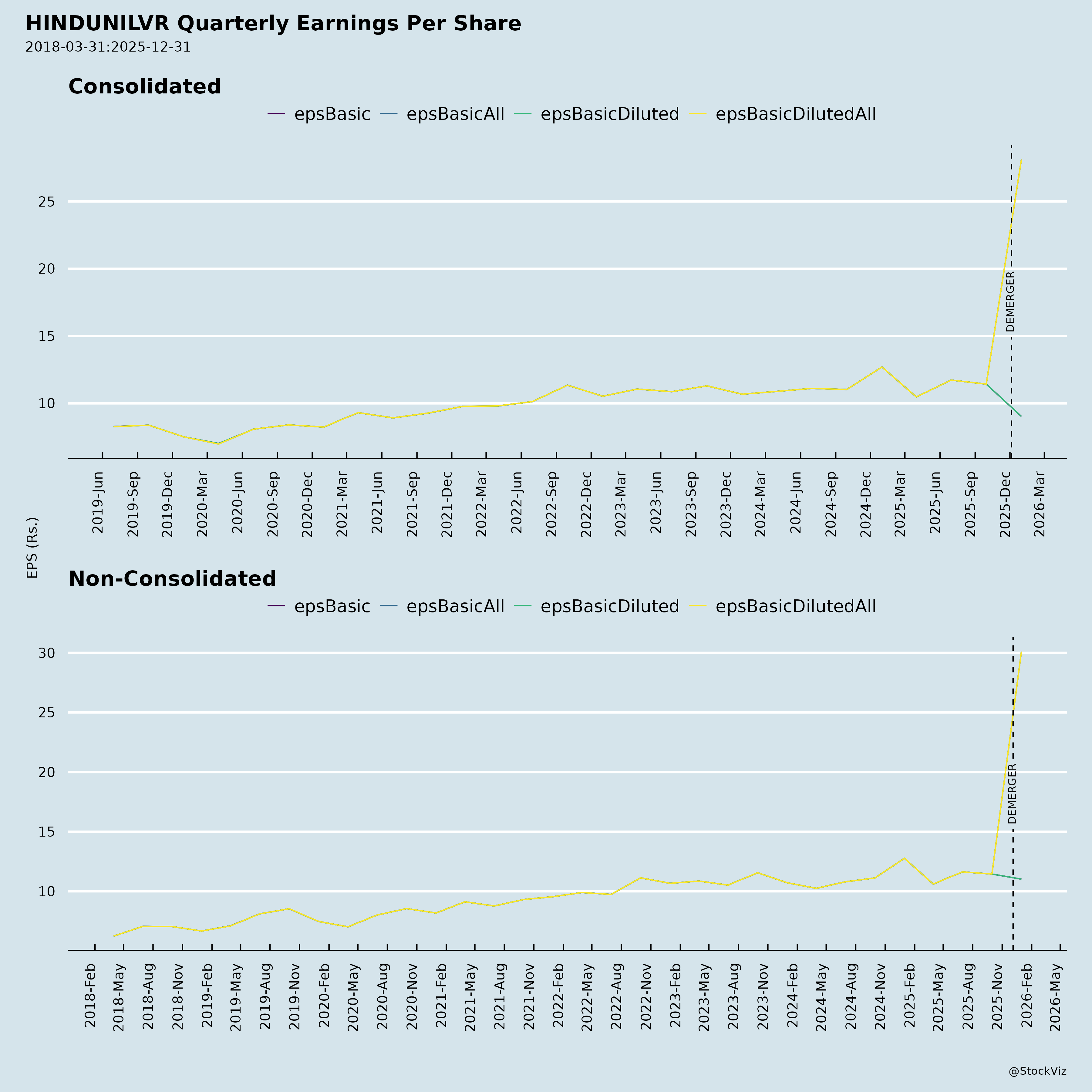

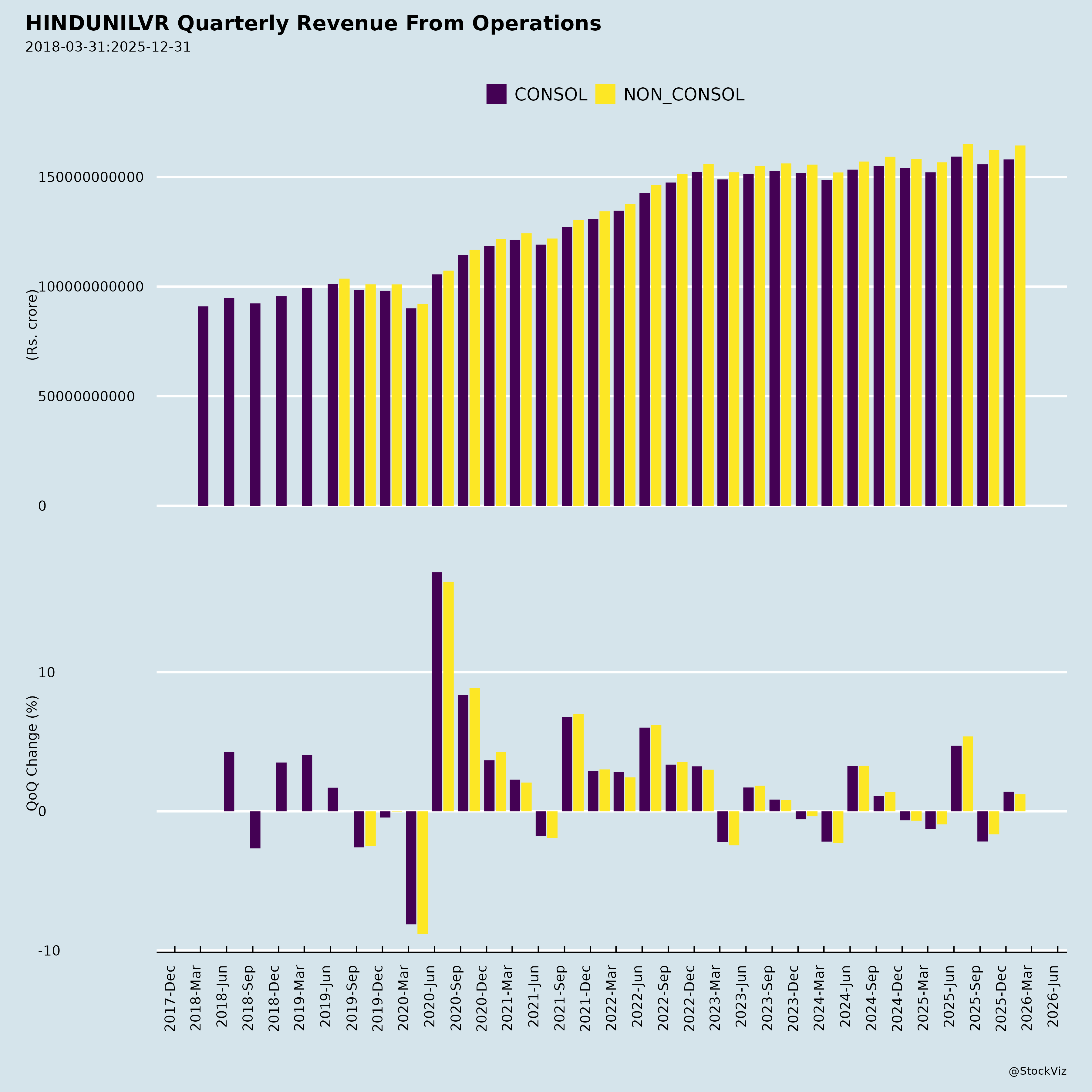

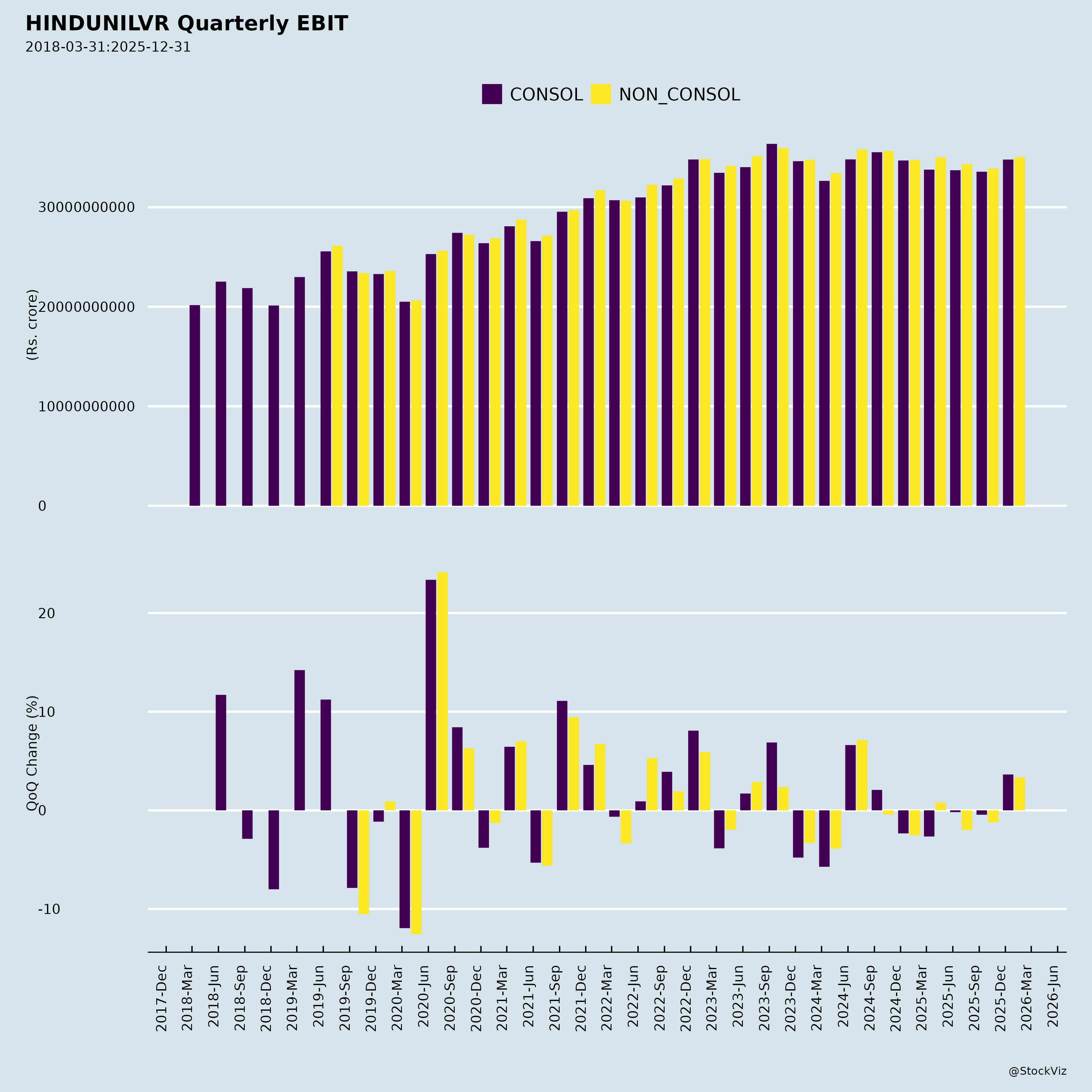

Fundamentals

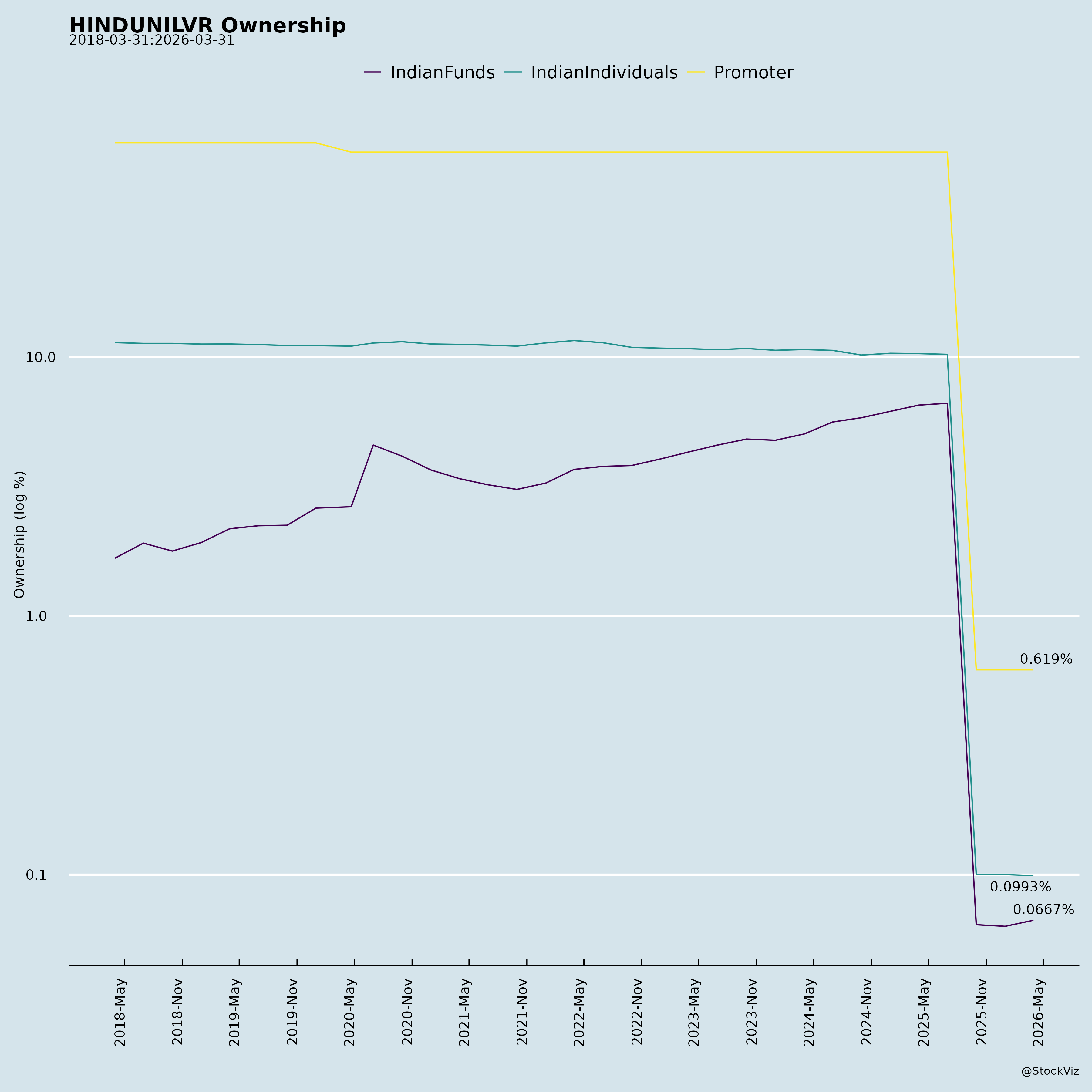

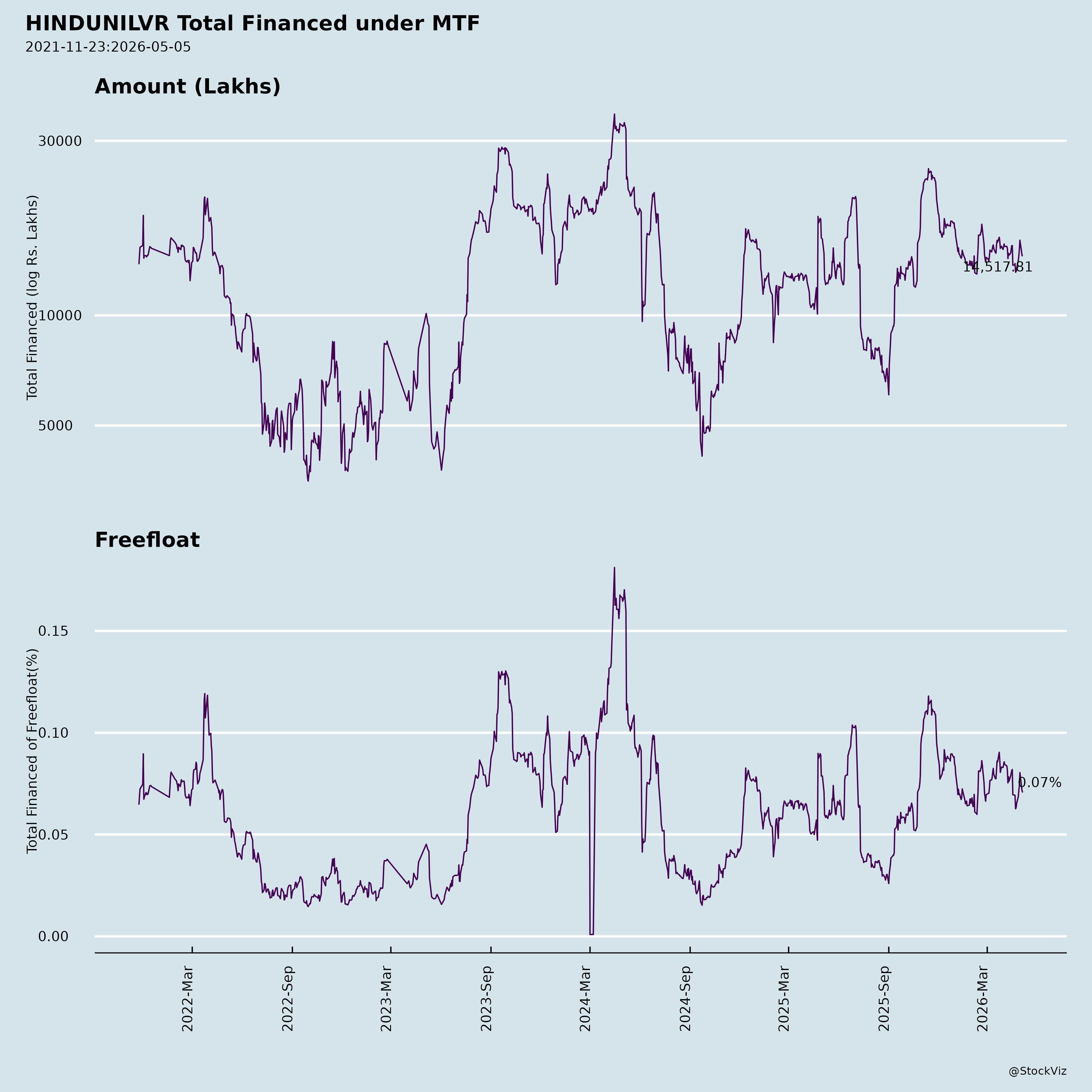

Ownership

Margined

AI Summary

asof: 2025-12-03

Analysis of Hindustan Unilever Limited (HINDUNILVR) – Headwinds, Tailwinds, Growth Prospects, and Key Risks

Overall Snapshot (Based on SQ’25 and H1 FY’26 Results, Oct 2025): - Financials: SQ’25 USG +2% (UVG flat), H1 USG +3% (UVG +5%). EBITDA margin 23.2% (-90 bps YoY SQ’25; -110 bps H1). PAT +4% SQ’25 (+5% H1); PAT bei -4%. Sales ₹16,061 cr SQ’25; interim dividend ₹19/share. - Strategic Context: Transitory GST disruptions and monsoon impacted Q2, but management eyes H2 recovery. Focus on volume-led growth via premiumisation, innovations, and portfolio transformation (Ice Cream demerger via KWIL scheme progressing). New CEO Priya Nair approved; board strengthened with Bobby Parikh (ID). - Market Position: Resilient with >85% #1 brands, 19 brands >$1bn turnover, 9mn retailer reach, 80bn annual consumer interactions.

Tailwinds (Positive Catalysts)

- GST Reforms: New-age changes (1,200+ SKUs repriced) to boost disposable income, sentiment, and premiumisation; full benefits passed to consumers for demand uplift.

- Category Strengths:

- Home Care: Mid-singles UVG (liquids double-digit).

- Beauty & Wellbeing: +5% USG (Skin Care high-singles; Health & Wellbeing triple-digit via OZiva).

- Foods: Beverages double-digit (Tea high-singles, Coffee robust).

- Strategic Investments: A&P +80 bps YoY (10.3%); launches (Vaseline Cloud Soft, Pond’s Hydra Miracle, Comfort Perfume Deluxe, Horlicks PRO Fitness, BRU Gold).

- Leadership & Governance: Priya Nair (30+ yrs Unilever exp., ex-Beauty & Wellbeing President) as CEO (99.88% shareholder approval). Bobby Parikh (ex-EY CEO, Infosys/ Biocon ID) as ID/ Risk Chair.

- Portfolio Power: Deep distribution moat; AI efficiencies; consumer segmentation (Power Spenders/Premiumisers/Democratisers); “Fewer, bigger bets” in high-growth spaces.

- KWIL Scheme: Ice Cream separation advancing (office shift, board reconstitution); unlocks value per SEBI observations.

Headwinds (Challenges)

- GST Transition: Temporary disruptions (trade de-stocking, delayed buying, pricing shifts) across categories (Hair Care decline, Personal Care flat, Packaged Foods muted, Ice Cream YoY drop).

- External Factors: Prolonged/intense monsoon hit Ice Cream/demand; stable but weak FMCG volume trends (rural/urban flat MAT Sep’25).

- Margin Pressure: EBITDA dip from investments; Gross Margin -10 bps; commodity divergence.

- Category Weakness: UVG declines (Personal Care high-singles; Lifestyle Nutrition turnover drop post-pricing); Oral Care marginal decline.

- Macro: Subdued consumption; rural recovery pending.

Growth Prospects

- Near-Term (H2 FY’26): Normal trading post-Oct; low-single digit pricing (if commodities stable); H2 > H1. EBITDA margins steady ex-Ice Cream.

- Mid/Long-Term:

- Volume-Led Acceleration: Radical segmentation, modern core brands (e.g., Surf Excel, Lux refresh), premiumisation (Future Core/Market Makers).

- High-Growth Bets: Health & Wellbeing (triple-digit sustained); ecom/Channels of Future (double-digit); digital marketing/sales (AI-powered).

- Ice Cream Unlock: KWIL scheme (post-approval) to streamline FMCG focus.

- Robust Moats: #1 employer; innovation pipeline; 3-yr share plans tied to growth/TSR/sustainability.

- Outlook: Competitive UVG trajectory; supportive macros (GST tailwinds).

| Category | SQ’25 USG/UVG | Key Driver |

|---|---|---|

| Home Care | Flat / Mid-singles | Liquids premiumisation |

| Beauty & Wellbeing | +5% / Flat | Skin/Health growth |

| Personal Care | Flat / High-singles decline | GST hit |

| Foods | +3% / Low-singles | Beverages offset Ice Cream |

Key Risks

| Risk Category | Description | Mitigation |

|---|---|---|

| Execution/Operational | GST lingering into Nov; transformation delays (e.g., premiumisation, sales machine). | Agile pricing; frontline focus. |

| Macro/External | Commodity volatility; weak rural demand; monsoons/climate. | Hedging; distribution depth. |

| Regulatory/Corporate | KWIL scheme delays (NCLT/SEBI approvals); tax/forex fluctuations. | Continuous disclosures. |

| Competitive | Intense pricing wars; market share erosion in weak categories. | #1 positions; innovations. |

| Financial | Margin sustained pressure from A&P/capex; PAT bei dip. | Cost efficiencies (AI). |

| Leadership/Other | New CEO integration; forex/tax on global comp (Priya Nair’s package ~₹27cr target). | Proven Unilever track record. |

Balanced View: HUL’s resilient model shines amid headwinds (GST/monsoon), with strong tailwinds from reforms/leadership/portfolio. Growth hinges on H2 recovery and execution of “volume-led” priorities—positioned for mid-teens EPS growth long-term if macros aid. Recommendation: Hold/Buy on dips; monitor Q3 results (Jan 2026) for GST normalcy. (Analysis based solely on provided docs; no external data.)

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.