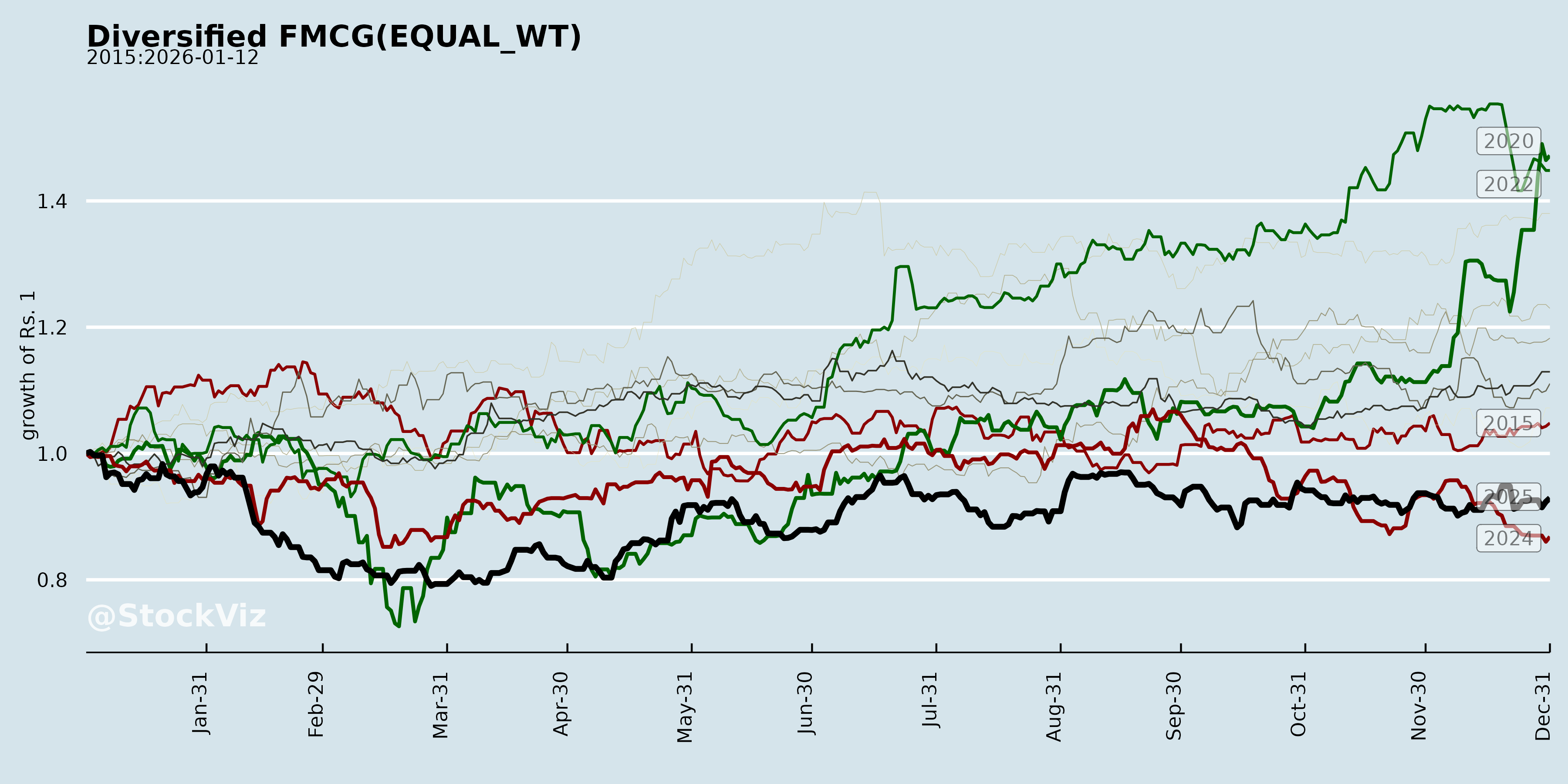

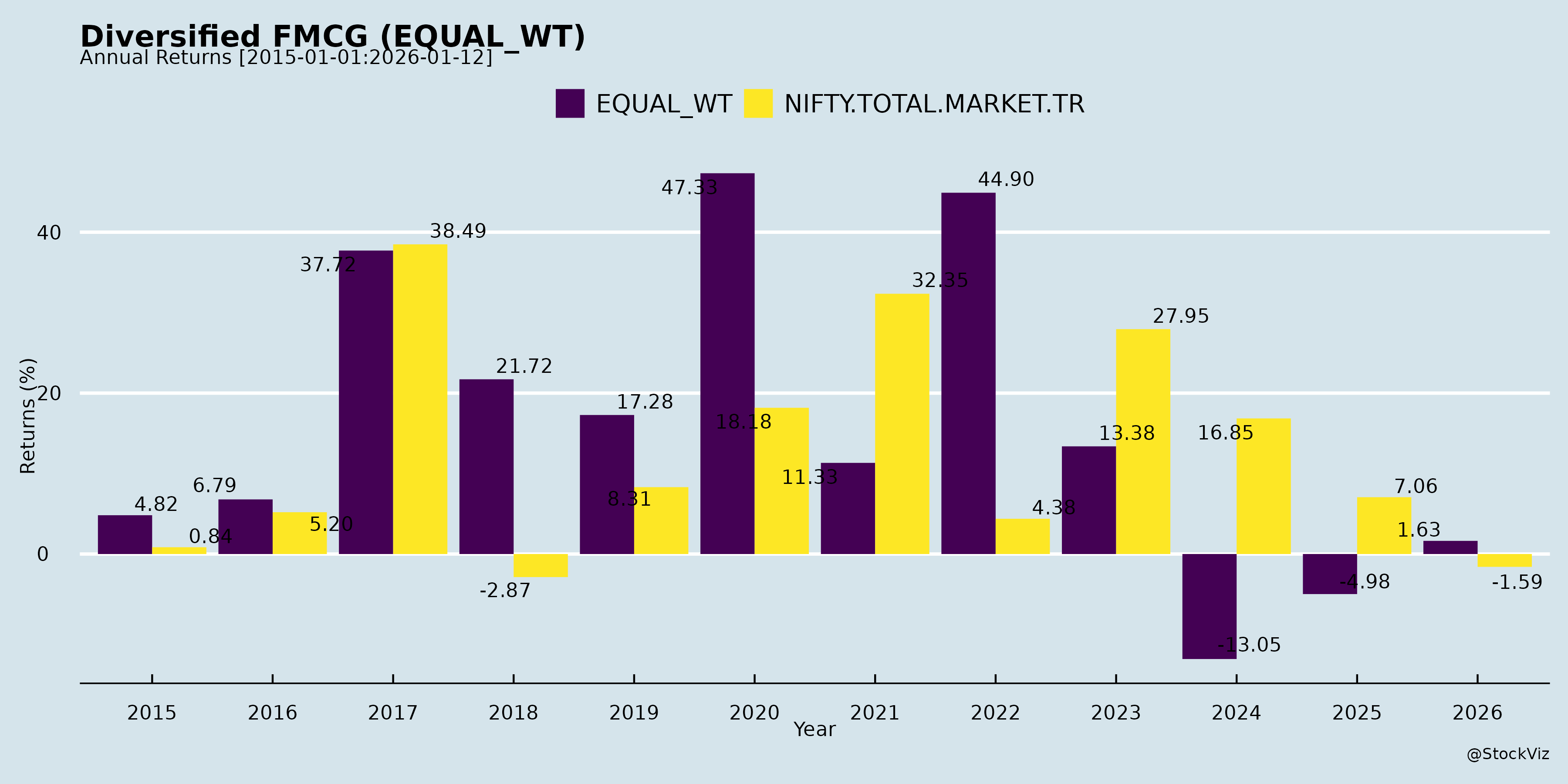

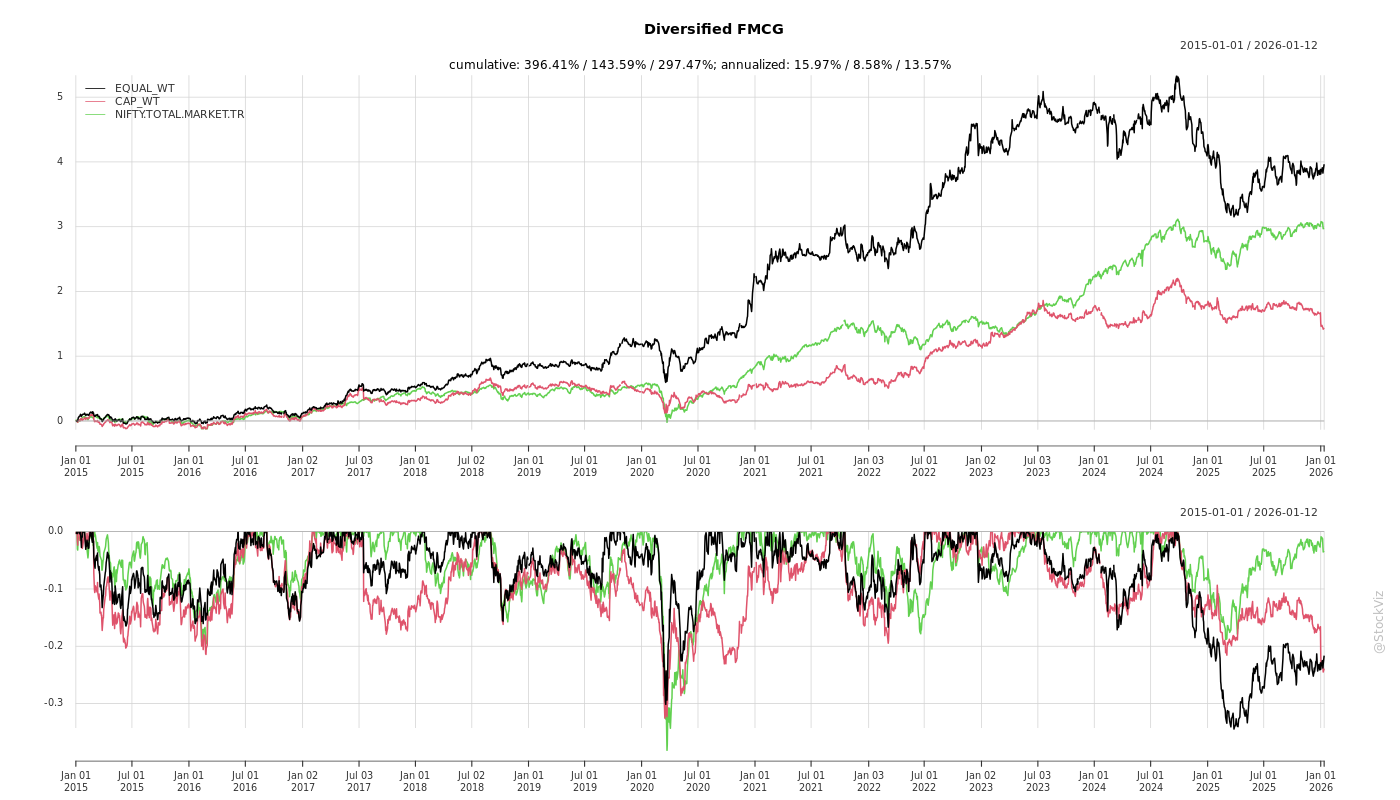

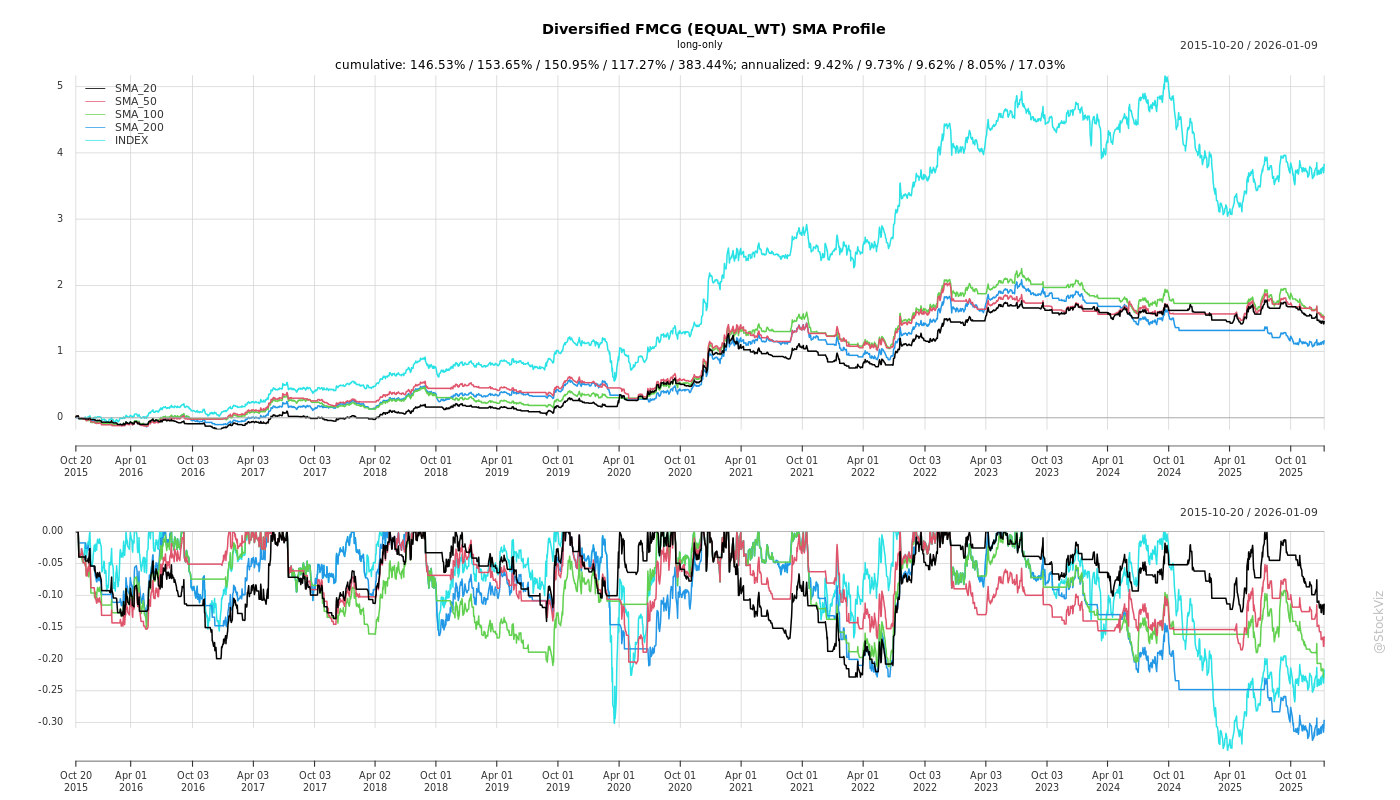

Diversified FMCG

Industry Metrics

May 8, 2026

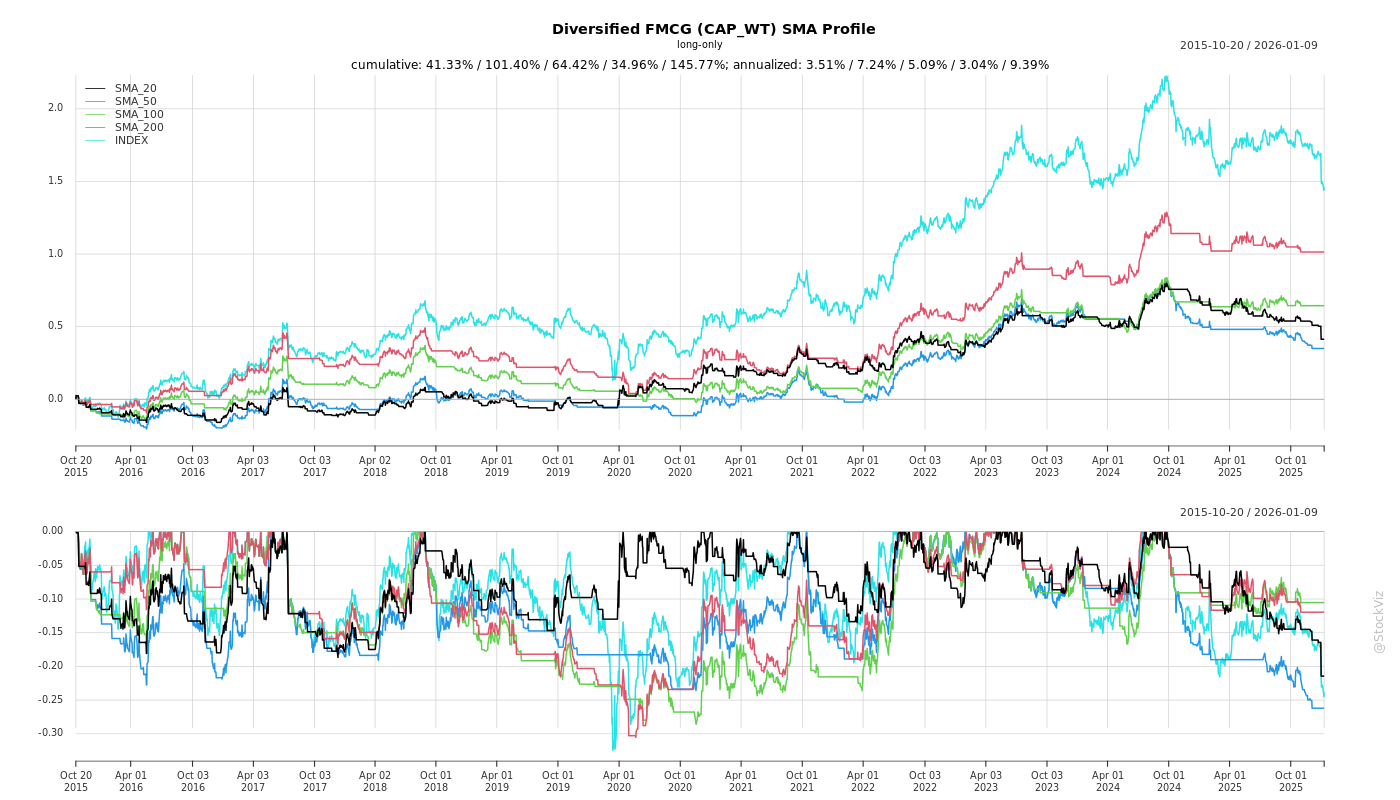

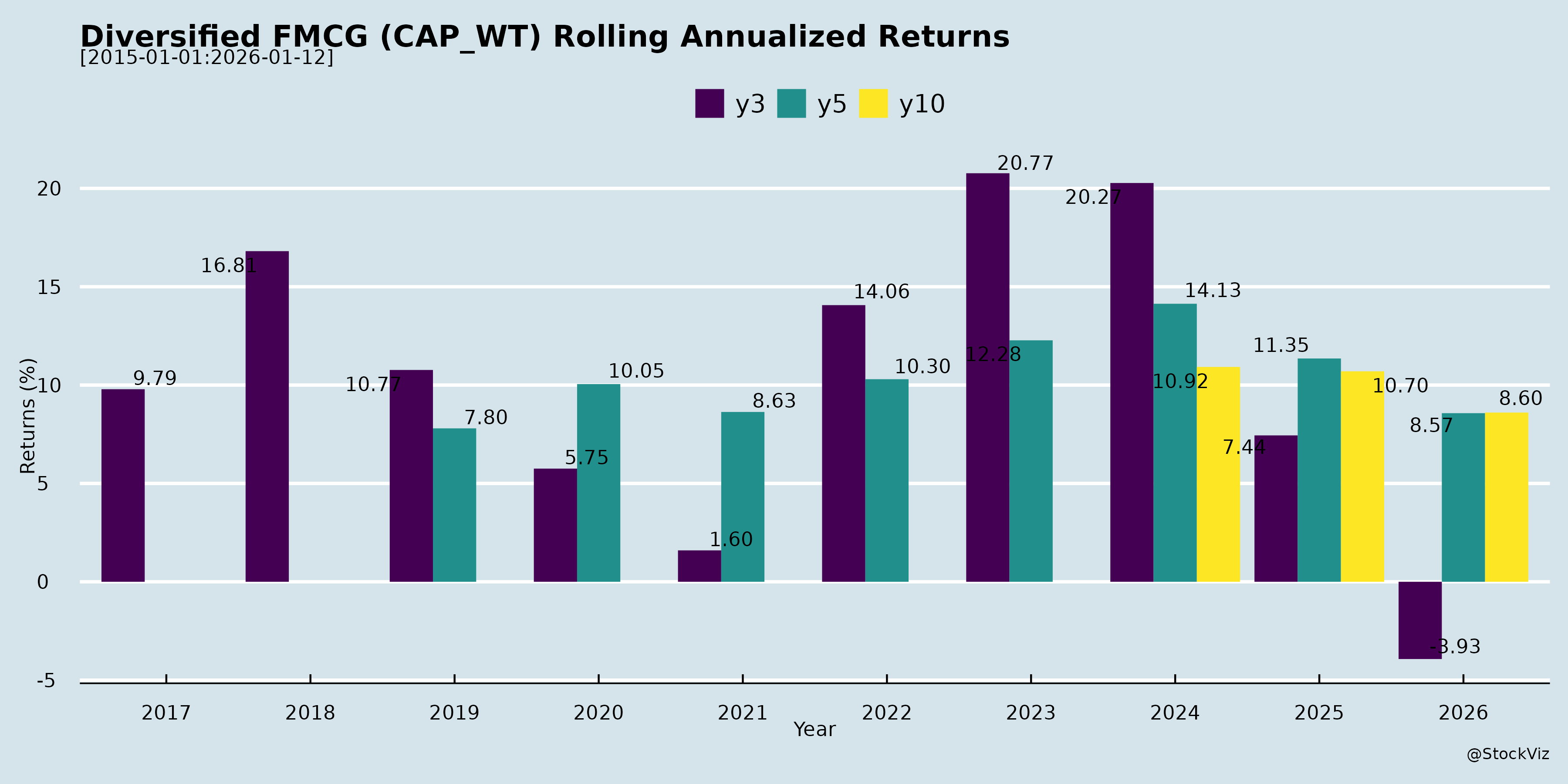

Annual Returns

Cumulative Returns and Drawdowns

SMA Scenarios

Current Distance from SMA

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-14

The challenges and opportunities across the industries represented in the sources—spanning sugar, biofuels, specialty chemicals, and fast-moving consumer goods (FMCG)—have evolved significantly over time, driven by shifting consumer preferences, sustainability goals, and regulatory changes.

Here is how these challenges and opportunities have evolved and are being addressed:

Evolving Opportunities

- Rise of Green Energy and Sustainability: The push for renewable energy and sustainable solutions has created massive opportunities. Davangere Sugar Company Limited (DSCL) is leveraging the demand-supply gap in India’s ethanol market, supported by the government’s achievement of a 20% ethanol blending target in 2025 [1, 2]. To capture this, DSCL is expanding its ethanol capacity from 65 KLPD to 85 KLPD and increasing sugarcane cultivation by 15,000 acres [3-5]. Similarly, Godavari Biorefineries Ltd (GBL) is capitalizing on sustainable raw materials by collaborating with Synthomer to commercialize bio-based butyl acrylate using bio-based butanol [6]. GBL is also set to commission a fungible grain-based ethanol capacity in Q1 FY27 to benefit from the restoration of the ethanol blending program [6].

- Growth in Premium and Niche Consumer Segments: Consumer demand is shifting toward premium and specialized products. Hindustan Unilever Limited (HUL) is investing up to ₹2,000 crores to expand its manufacturing capacity specifically for fast-growing premium categories in Beauty & Wellbeing and Home Care liquids, leveraging advanced automation to meet evolving consumer needs [7-9]. In the contract manufacturing space, Hindustan Foods Limited (HFL) recognized an opportunity with newer brands and Direct-to-Consumer (D2C) players who require faster innovation and smaller, flexible production runs [10-12]. To address this, HFL is acquiring the beauty care and cosmetic manufacturing business of Ultra Beauty Care Private Limited, which will also open up export-led opportunities [10, 12, 13].

- Advancements in R&D and Intellectual Property: Opportunities are emerging from deep-tech and proprietary research. GBL recently received a Japanese patent for a novel anti-cancer molecule that inhibits V-ATPase activity and treats viral infections, thereby adding significant value to its antiviral and specialty chemicals portfolio [14, 15].

Evolving Challenges

- Regulatory and Compliance Shifts: Changes in government policy remain a persistent threat [2]. A major recent challenge for Indian manufacturers has been the implementation of the new Labour Codes, which consolidated 29 existing labor laws and became effective on November 21, 2025 [16, 17]. This forced companies to reassess their employee benefit obligations, resulting in unexpected financial impacts. For instance, HFL recognized an incremental liability of ₹3.50 crores as an exceptional item [16, 18], while GBL recorded an estimated impact of ₹7.87 crores [17, 19, 20].

- Climate Vulnerability and Raw Material Sourcing: Agricultural dependencies expose companies to severe climatic and supply chain risks. DSCL notes that its operations are highly vulnerable to climatic fluctuations that affect sugarcane availability, coupled with rising competition from regional sugar mills [2].

- Managing Seasonality and Operational Costs: The seasonal nature of the sugar and agricultural business heavily impacts quarterly financial performance [21-23]. To remain competitive and secure its supply chain, GBL had to agree to pay additional harvesting charges to contractors for the 2023-2024 sugar season, resulting in a substantial exceptional expense of ₹26.65 crores [21, 22, 24]. To combat these seasonal challenges, GBL is actively investing in debottlenecking, capacity optimization, and technology to improve efficiency [25]. Meanwhile, HFL is mitigating operational inefficiencies by leveraging spare land at its newly acquired 6-acre site to build a beverage manufacturing facility, unlocking better utilization and synergies [13, 26].

What are the headwinds affecting this industry?

asof: 2026-04-14

Based on the provided documents, the primary headwinds and risks affecting the sugar, ethanol, and bio-based chemicals industry include:

- Vulnerability to Climate and Raw Material Supply: The industry has a high dependency on sugarcane supply, making it highly vulnerable to climatic fluctuations [1]. Unpredictable weather can significantly affect crop yields, which in turn disrupts raw material availability and overall production capacity [1].

- Regulatory and Policy Changes: The sugar and ethanol sectors are highly sensitive to the impact of government regulations and face ongoing exposure to changes in government policies [1]. Furthermore, significant shifts in the broader political and economic environment—both domestically in India and in key international markets—along with changes in tax laws, can pose substantial challenges to operations [2].

- Rising Competition: Companies face a direct threat from increasing competition from regional sugar mills, which can pressure market share and influence pricing dynamics within the sector [1].

- Macroeconomic and Financial Pressures: The industry is susceptible to general downtrends in the global or domestic market [2]. Additionally, financial and operational headwinds such as exchange rate fluctuations, rising interest rates, and other increasing costs can negatively impact cash flow projections and business income [2].

- Operational and Technological Risks: Companies must navigate challenges related to technological changes, potential litigation, and maintaining stable labour relations, all of which can disrupt smooth operations and increase costs [2].

What are the key things to understand about this industry?

asof: 2026-04-14

Based on the sources provided, the key insights into the industry primarily cover the Sugar and Ethanol sectors, with additional notable trends in the FMCG and Beauty & Personal Care (BPC) contract manufacturing sector.

Here are the key things to understand about these industries:

1. The Sugar Industry

- Strong Market Growth & Demand: India’s cane sugar market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.2% from FY25 to FY30 [1]. This is largely driven by surging domestic consumption for daily household use and wide applications across the food, beverage, and confectionery sectors [1].

- Rising Production: India remains a leading producer of sugar, with output expected to increase by 18% to 34.90 million tonnes during the 2025–26 sugar season [1]. The backbone of India’s sugar economy relies on key production states such as Maharashtra, Uttar Pradesh, Karnataka, Gujarat, and Tamil Nadu [1].

- Shift Toward Organic Sugar: There is a growing consumer preference for organic sugar due to its natural processing methods, nutritional benefits, and high demand from health-conscious and Ayurvedic segments [1].

- Export Momentum & Diversion Strategies: The industry maintains strong export momentum, having exported 4.24 lakh tonnes of sugar by April of the 2024-25 marketing year [1]. Additionally, to support the biofuel sector, the government allowed the diversion of 40 Lakh Metric Tonnes (LMT) of sugar for ethanol production for the ESY 2024-25 [1].

2. The Ethanol & Biofuels Industry

- Explosive Market Expansion: The Indian ethanol market is experiencing rapid growth. It was valued at USD 3.00 billion in 2024 and is expected to surge to USD 10.07 billion by 2033, registering a CAGR of 14.40% [2].

- Key Growth Drivers: This expansion is fueled by rising government blending mandates, favorable policies, increased sugarcane production, technological advancements, and a growing demand for cleaner fuels in the automotive and industrial sectors [2].

- Accelerated Blending Targets: Through the Ethanol Blended Petrol (EBP) Programme, India successfully achieved its target of 20% ethanol blending in petrol in 2025—five years ahead of its original 2030 deadline [3].

- Massive Economic & Infrastructure Impact: The push for ethanol has led to significant infrastructure boosts, enhancing the country’s ethanol distillation capacity to 1,810 crore litres per annum [4]. The program has resulted in over ₹1.36 lakh crore in foreign exchange savings by reducing crude oil import dependency [3, 4]. Furthermore, it has profoundly impacted the rural agricultural economy, with ₹1.18 lakh crore disbursed to farmers and ₹1.96 lakh crore paid to distilleries [3, 4].

- Favorable Pricing: The government has established revised and remunerative pricing for ethanol, such as fixing the price of ethanol from C-Heavy Molasses at ₹57.97 per litre for ESY 2024–25, ensuring stable returns for suppliers [3].

3. FMCG and Beauty & Personal Care (BPC) Manufacturing

- Demand for Agility and Smaller Production Runs: The Beauty and Personal Care category is steadily growing and attracting newer D2C (Direct-to-Consumer) brands. These newer entrants require faster innovation cycles and smaller, more flexible production runs, shifting the dynamics of contract manufacturing [5].

- Focus on Premium Categories & Technology: Major FMCG players are strategically focusing their investments on fast-growing premium categories within Beauty, Wellbeing, and Home Care [6]. To keep up with evolving consumer needs and emerging channels, the industry is heavily investing in advanced automation and digital technologies to create more agile, efficient, and future-ready supply chains [6].

- Sustainability Integrations: There is an increased focus on sustainability across manufacturing, with large companies aiming to develop facilities that operate on 100% renewable energy [7].

What are the tailwinds affecting this industry?

asof: 2026-04-14

The Sugar Industry is currently experiencing robust growth driven by several key macroeconomic and consumer-driven tailwinds:

- Surging Domestic Demand: The cane sugar market in India is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.2% between FY25 and FY30 [1]. This strong demand is sustained by consistent daily household consumption and extensive applications across the food, beverage, and confectionery sectors [1].

- Rising Preference for Organic Sugar: There is a growing consumer shift toward organic sugar [1]. This trend is fueled by the product’s natural processing, associated nutritional benefits, and high demand from health-conscious demographics and the Ayurvedic sector [1].

- Strong Production and Export Momentum: India remains a leading producer, with sugar output projected to rise by 18% to reach 34.90 million tonnes in the upcoming 2025–26 sugar season [1]. Furthermore, the industry is seeing strong export figures, having exported 4.24 lakh tonnes of sugar by April of the 2024–25 marketing year [1].

- Ethanol Diversion Support: The industry is benefiting from the authorized diversion of 40 Lakh Metric Tonnes (LMT) of sugar for ethanol production for the 2024-25 Ethanol Supply Year (ESY) [1]. This diversion helps balance sugar supply and demand, ensuring better price stability and alternative revenue streams for sugar mills [1, 2].

The Ethanol and Biofuel Industry, which is heavily integrated with sugar manufacturing, is also benefiting from a massive structural transformation, with its market value expected to surge from USD 3.00 Billion in 2024 to USD 10.07 Billion by 2033 (a 14.40% CAGR) [3]. The tailwinds for this sector include:

- Aggressive Government Blending Mandates: The industry is being propelled by the government’s Ethanol Blended Petrol (EBP) Programme, which successfully achieved a 20% ethanol blending target in petrol in 2025—five years ahead of the original 2030 deadline [2].

- Lucrative Pricing and Incentives: The government has introduced revised, favorable pricing to ensure price stability and remunerative returns for producers [2]. For example, the price of ethanol derived from C-Heavy Molasses was increased to ₹57.97 per litre for ESY 2024–25 [2, 4, 5].

- Expanding Automotive and Industrial Adoption: Demand is accelerating due to the rising adoption of cleaner fuels in the automotive sector, supported by the rollout of flexi-fuel vehicles and the increasing availability of E-20 and E-100 fuels [4, 6]. Ethanol is also seeing growing industrial applications [4].

- Massive Infrastructure Investments: Favorable policies and government incentives have led to significant investments in both greenfield and brownfield ethanol plants [4, 6]. This has successfully enhanced the national ethanol distillation capacity to 1,810 crore litres per annum [6]. Long-Term Off-take Agreements (LTOAs) and technological advancements further secure the industry’s future growth [4, 6].

- Broader Economic and Environmental Alignment: The push for ethanol aligns perfectly with broader national goals, such as the Atmanirbhar Bharat initiative, by reducing dependency on crude oil imports and saving over ₹1.36 lakh crore in foreign exchange [2, 6]. Furthermore, the industry is a massive driver of rural empowerment, having disbursed ₹1.18 lakh crore to farmers and generating substantial local employment [2, 6].

What is the general outlook of this industry?

asof: 2026-04-14

The provided sources highlight the general outlook for multiple sectors, specifically the Sugar and Ethanol industry, as well as the FMCG and Beauty & Personal Care (BPC) industry.

The Sugar Industry The Indian cane sugar market is positioned for steady expansion, expected to grow at a Compound Annual Growth Rate (CAGR) of 5.2% over the forecast period of FY25–30 [1]. This growth is primarily driven by rising domestic consumption [1]. India’s sugar output is projected to surge by 18% to reach 34.90 million tonnes in the upcoming 2025–26 sugar season [1].

Key trends driving the sugar industry include: * Surging Domestic Demand: Sugar maintains a consistently high demand due to daily household usage and its extensive application across the food, beverage, and confectionery sectors [1]. * The Organic Sugar Trend: There is a growing consumer preference for organic sugar, fueled by its natural processing, nutritional benefits, and demand from Ayurvedic and health-conscious consumer segments [1]. * Strong Export Momentum: India successfully exported 4.24 lakh tonnes of sugar by April of the 2024-25 marketing year [1]. * Ethanol Diversion: The industry’s outlook is further supported by government policies that allowed the diversion of 40 Lakh Metric Tonnes (LMT) of sugar specifically for ethanol production during the 2024-25 Ethanol Supply Year (ESY) [1].

The Ethanol and Biofuels Industry The ethanol market shows a highly robust and lucrative outlook, propelled by India’s push towards sustainable mobility and green energy. * Rapid Market Expansion: Valued at USD 3.00 Billion in 2024, the Indian ethanol market is projected to more than triple to USD 10.07 Billion by 2033, expanding at a remarkable CAGR of 14.40% from 2025 to 2033 [2]. * Blending Mandates and Milestones: A monumental achievement for the industry is that India successfully reached its 20% ethanol blending target in petrol in 2025—completing this goal five years ahead of the original 2030 deadline [3]. The Ethanol Blended Petrol (EBP) Programme has already saved over ₹1.36 lakh crore in foreign exchange and disbursed ₹1.18 lakh crore to farmers, significantly boosting rural incomes and the agricultural economy [3, 4]. * Favorable Pricing and Infrastructure: To promote price stability and ensure remunerative returns for producers, the pricing for ethanol derived from C-Heavy Molasses was revised to ₹57.97 per litre for the 2024–25 ESY, an increase from ₹56.58 per litre [3, 5]. Consequently, national ethanol distillation capacity has been enhanced to 1,810 crore litres per annum [4]. * Future Growth Drivers: The industry’s future is underpinned by Long Term Off-take Agreements (LTOAs), the anticipated rollout of Dedicated Ethanol Plants (DEPs) in ethanol-deficit states, and the increasing availability of flexi-fuel vehicles alongside E-20 and E-100 fuels [4]. Other growth catalysts include favorable government policies, expanding biofuel infrastructure, technological advancements, and rising demand for cleaner fuels in the automotive and industrial sectors [5].

FMCG, Beauty & Personal Care (BPC), and Bio-based Chemicals The fast-moving consumer goods and specialty chemicals sectors are experiencing a strong shift towards premiumization, sustainable operations, and agile manufacturing. * Expansion in Beauty & Personal Care: The BPC category continues to experience strong growth, increasingly attracting new direct-to-consumer (D2C) brands [6, 7]. These newer brands require faster innovation cycles and smaller, more flexible production runs [7]. To meet this demand, contract manufacturers are acquiring specialized cosmetic facilities to provide agile solutions for both domestic and export markets [6-8]. * Premiumization and Strategic Investments: Large FMCG companies are heavily investing in high-growth, premium segments. For instance, Hindustan Unilever Limited announced a proposed investment of up to ₹2,000 crores over two years to expand its manufacturing capacity specifically for fast-growing premium categories within Beauty & Wellbeing and Home Care liquids [9, 10]. This aligns with corporate strategies focused on “fewer, bigger bets” to dominate high-growth demand spaces [11]. * Supply Chain Modernization and Sustainability: The industry is focusing on advanced automation and digital technologies to create future-ready, agile supply chains that can quickly respond to evolving consumer needs and emerging retail formats [11]. Simultaneously, there is a strong emphasis on environmental responsibility, with companies targeting 100% renewable energy for their facilities [12]. Furthermore, chemical manufacturers are accelerating the industry’s transition to sustainable raw materials by developing green chemistry solutions, such as bio-based alternatives to fossil-based monomers [13].

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.