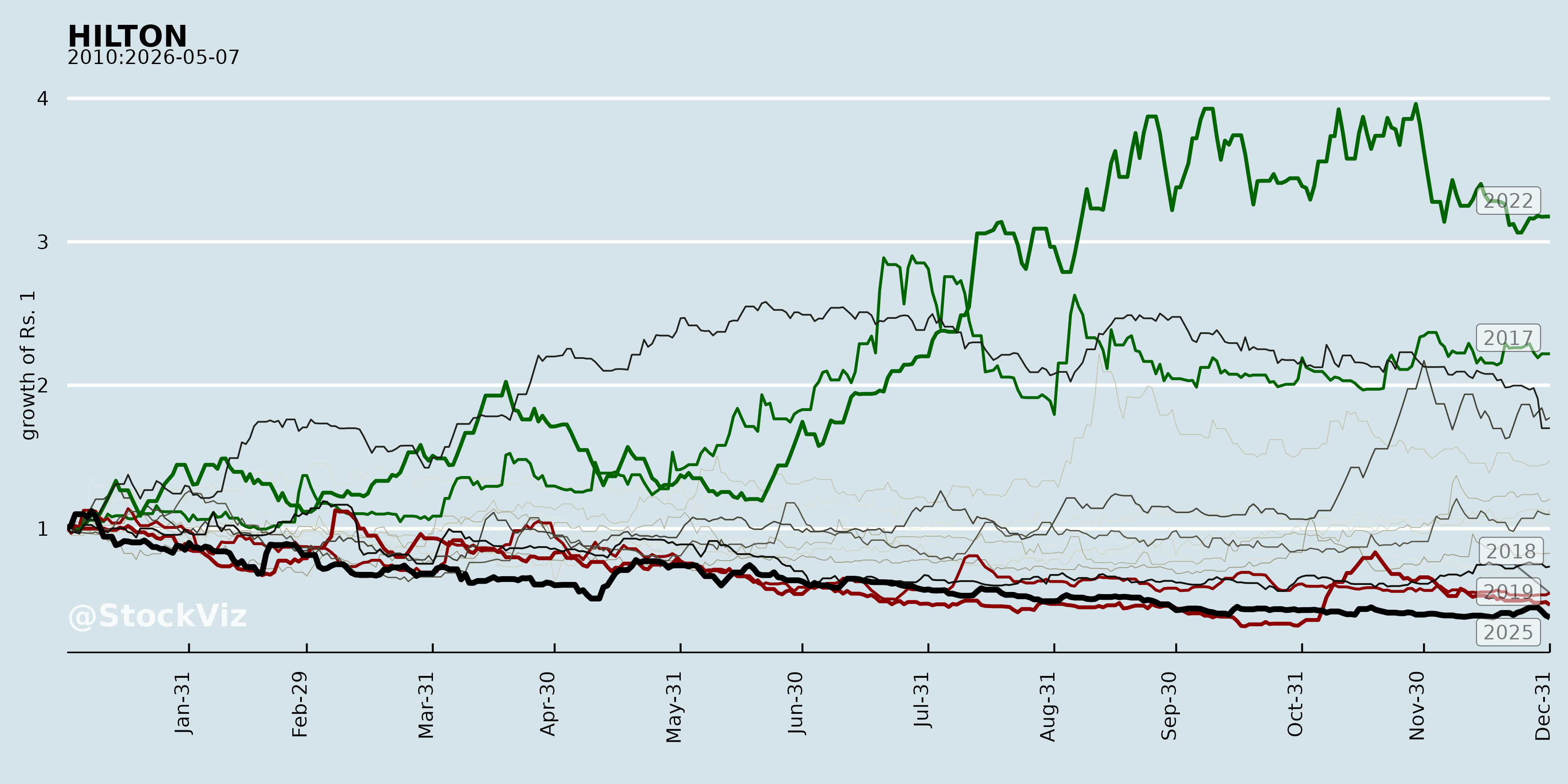

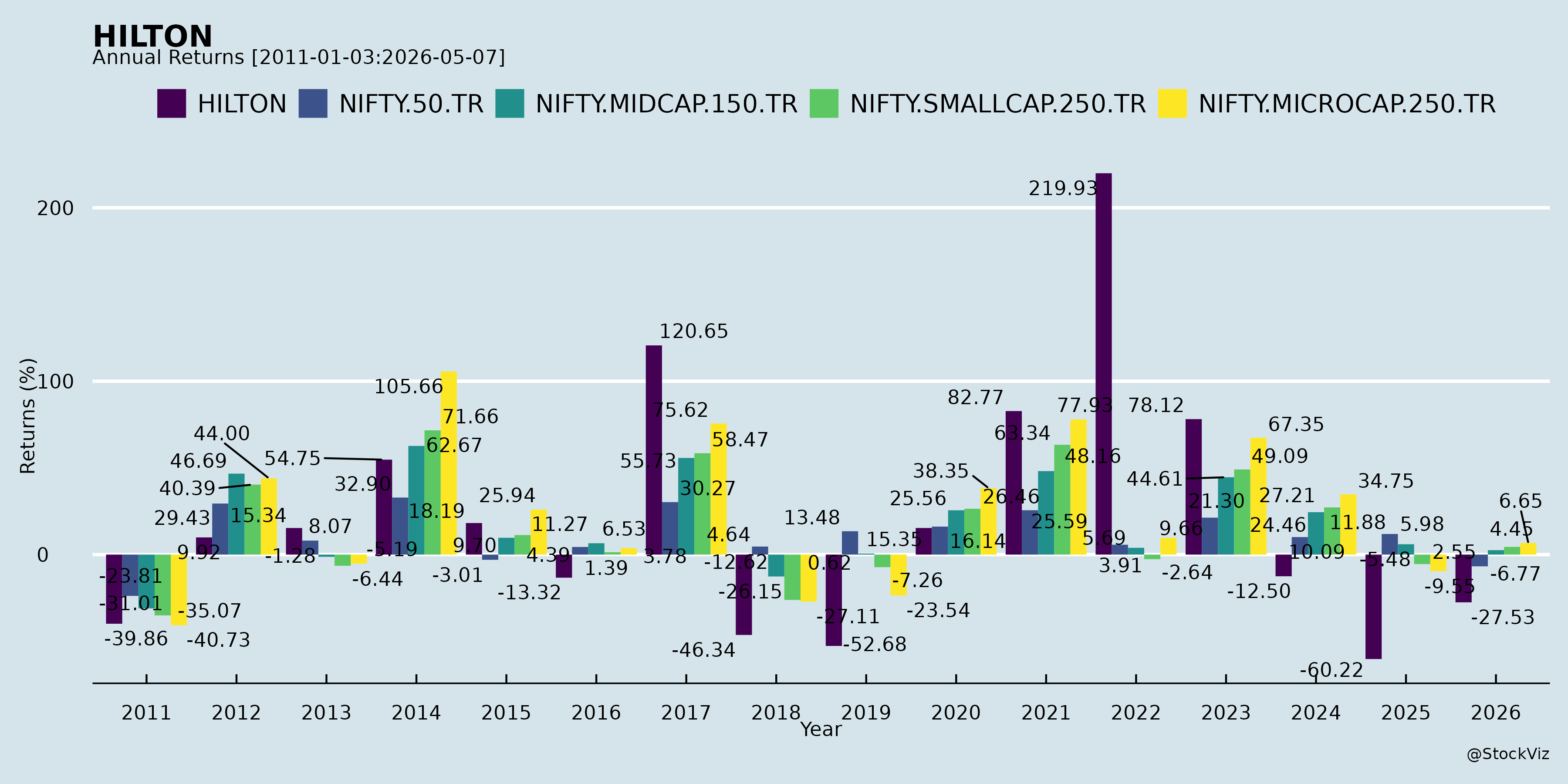

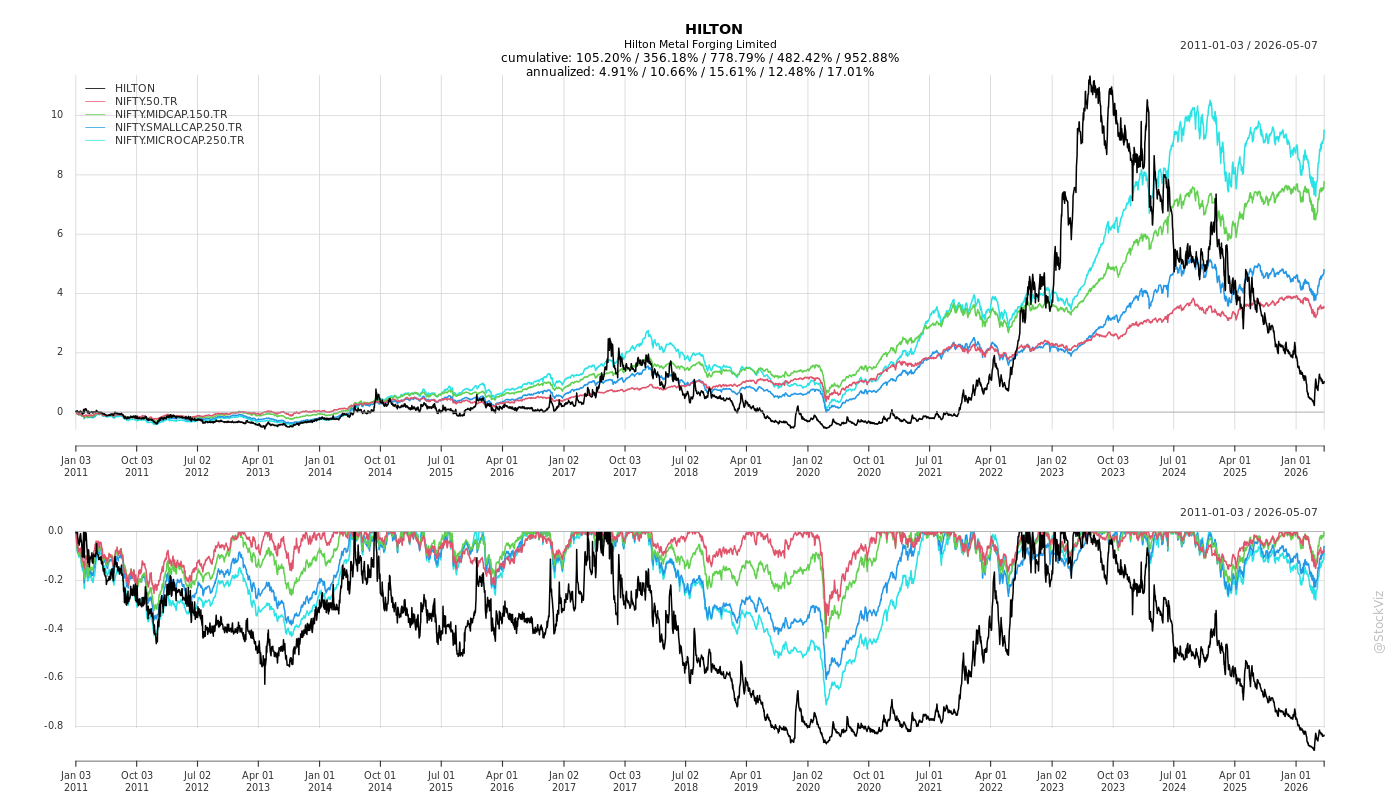

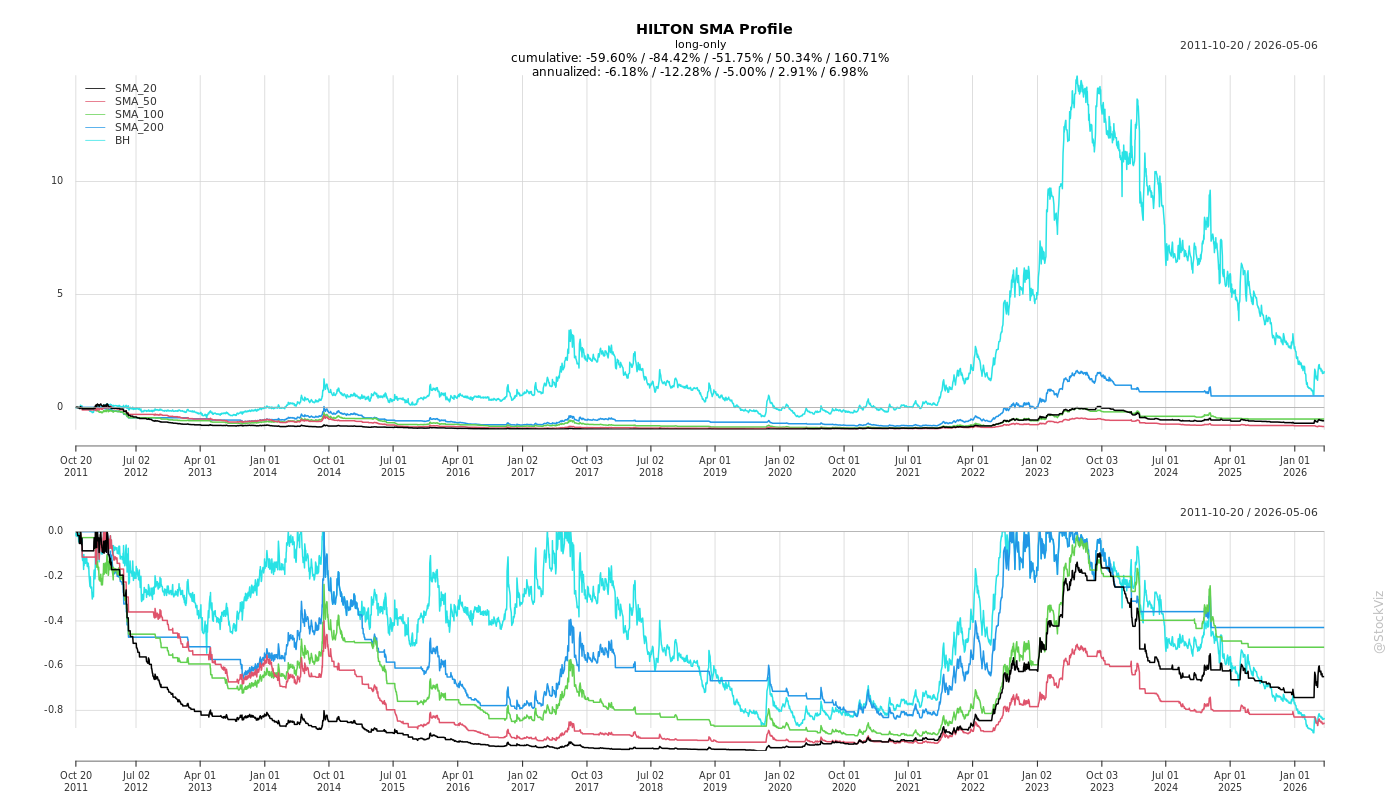

HILTON

Equity Metrics

May 8, 2026

Hilton Metal Forging Limited

Annual Returns

Cumulative Returns and Drawdowns

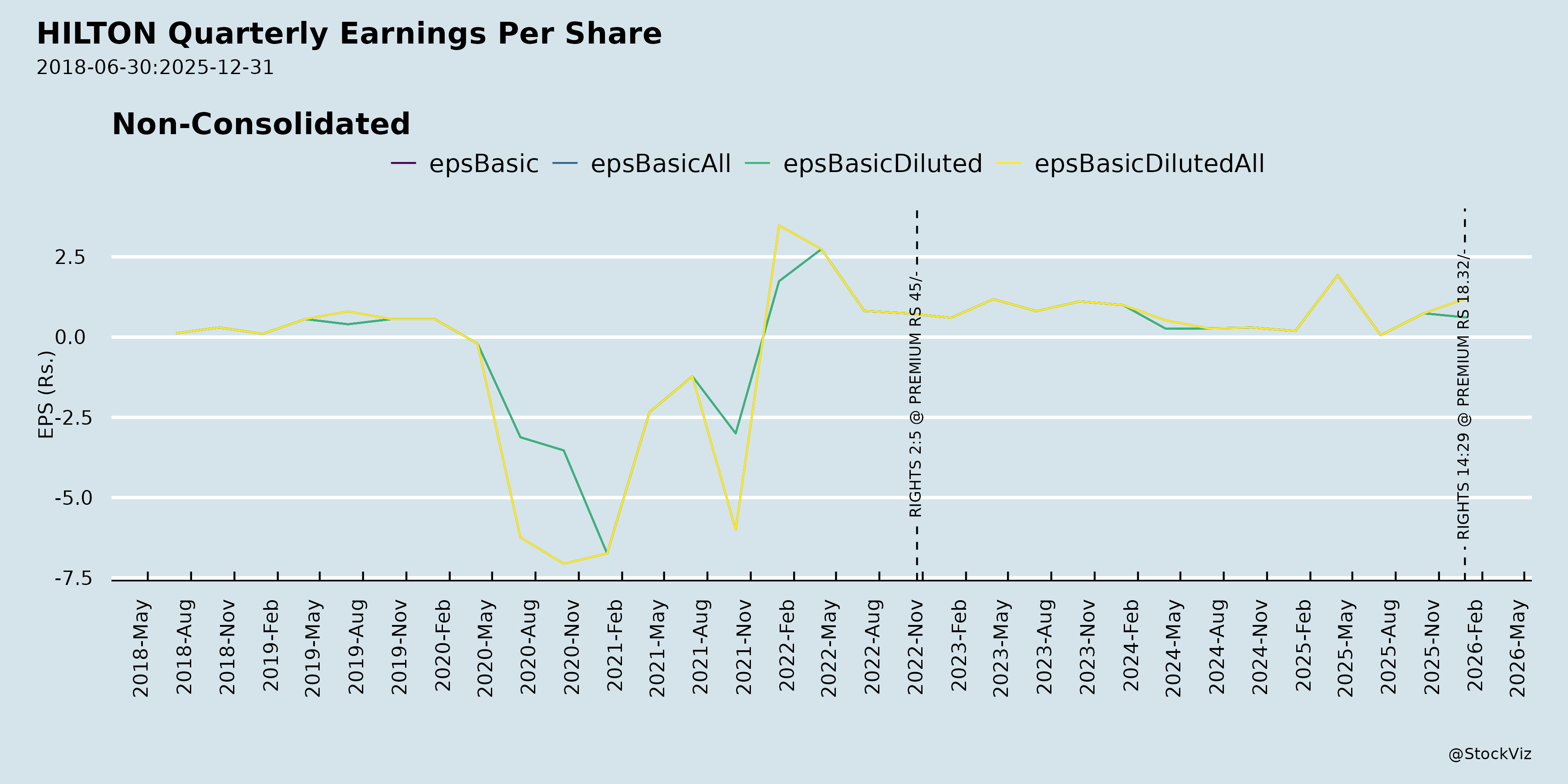

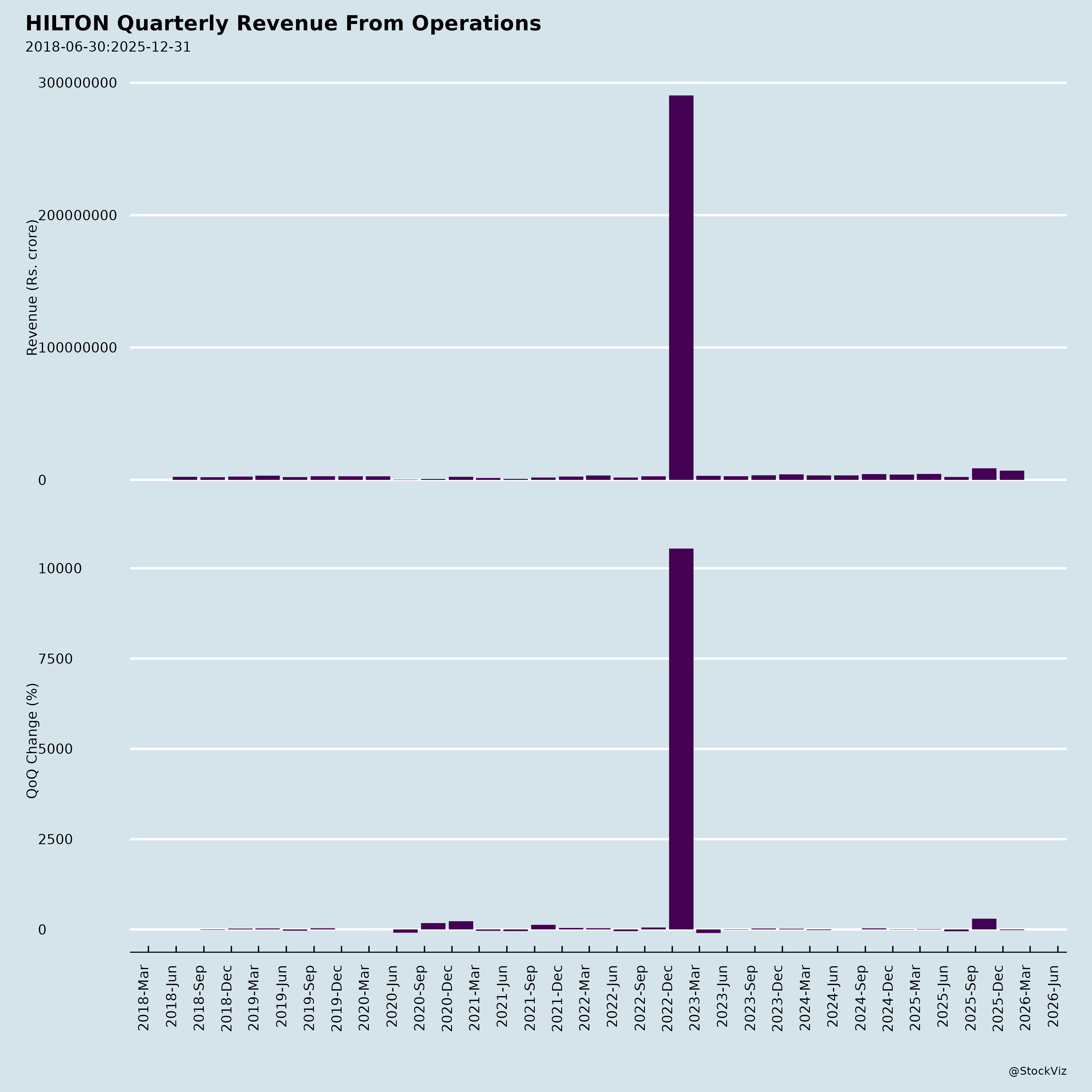

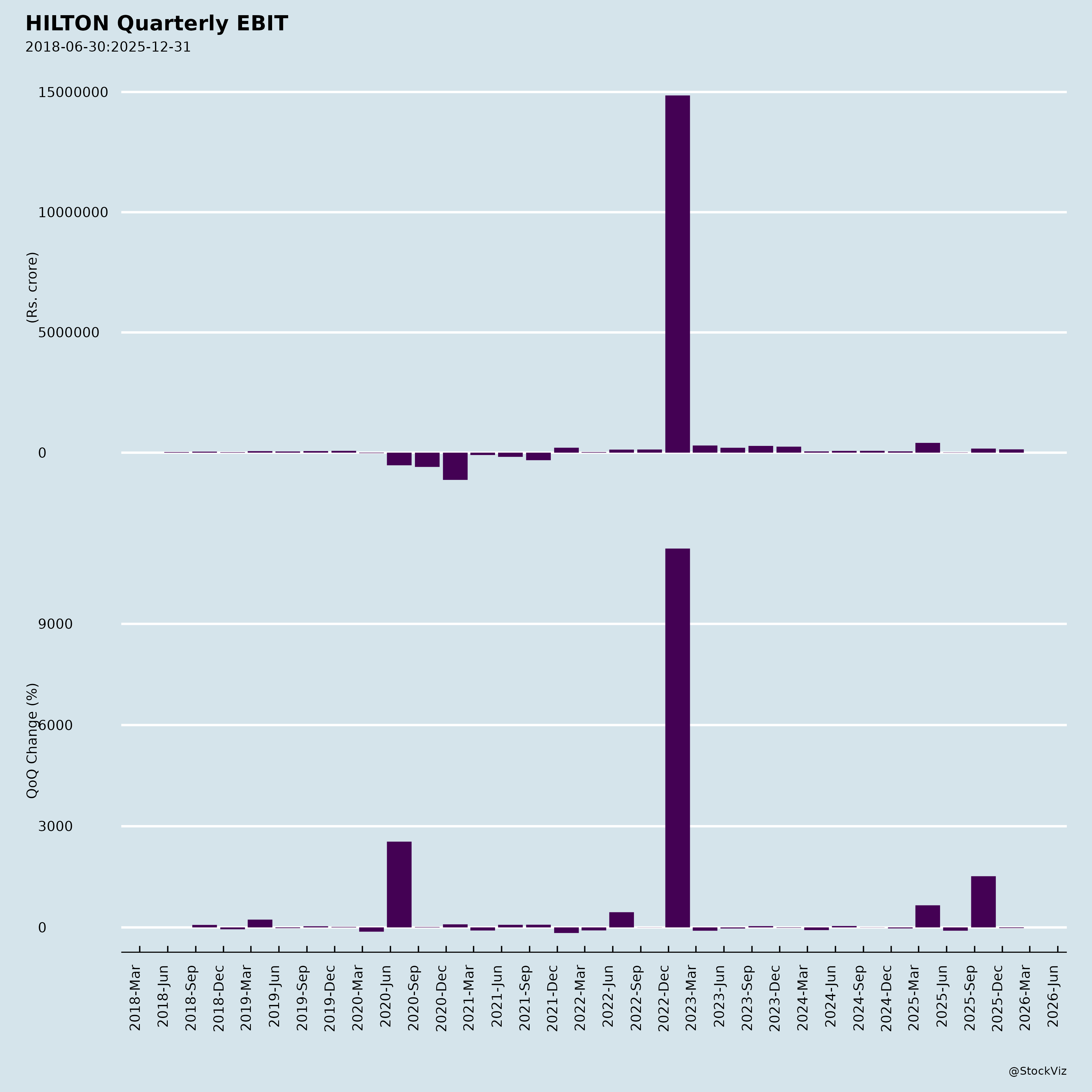

Fundamentals

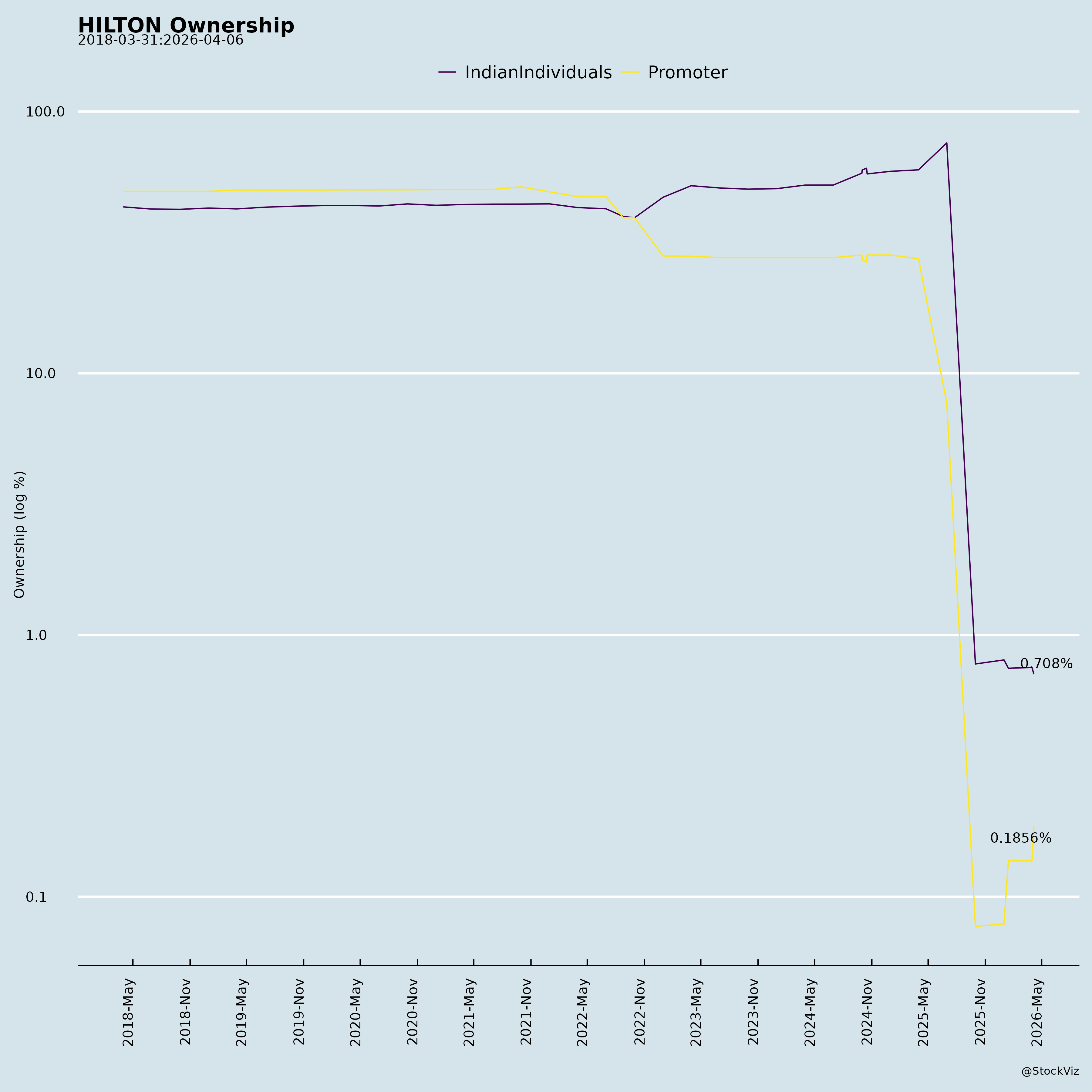

Ownership

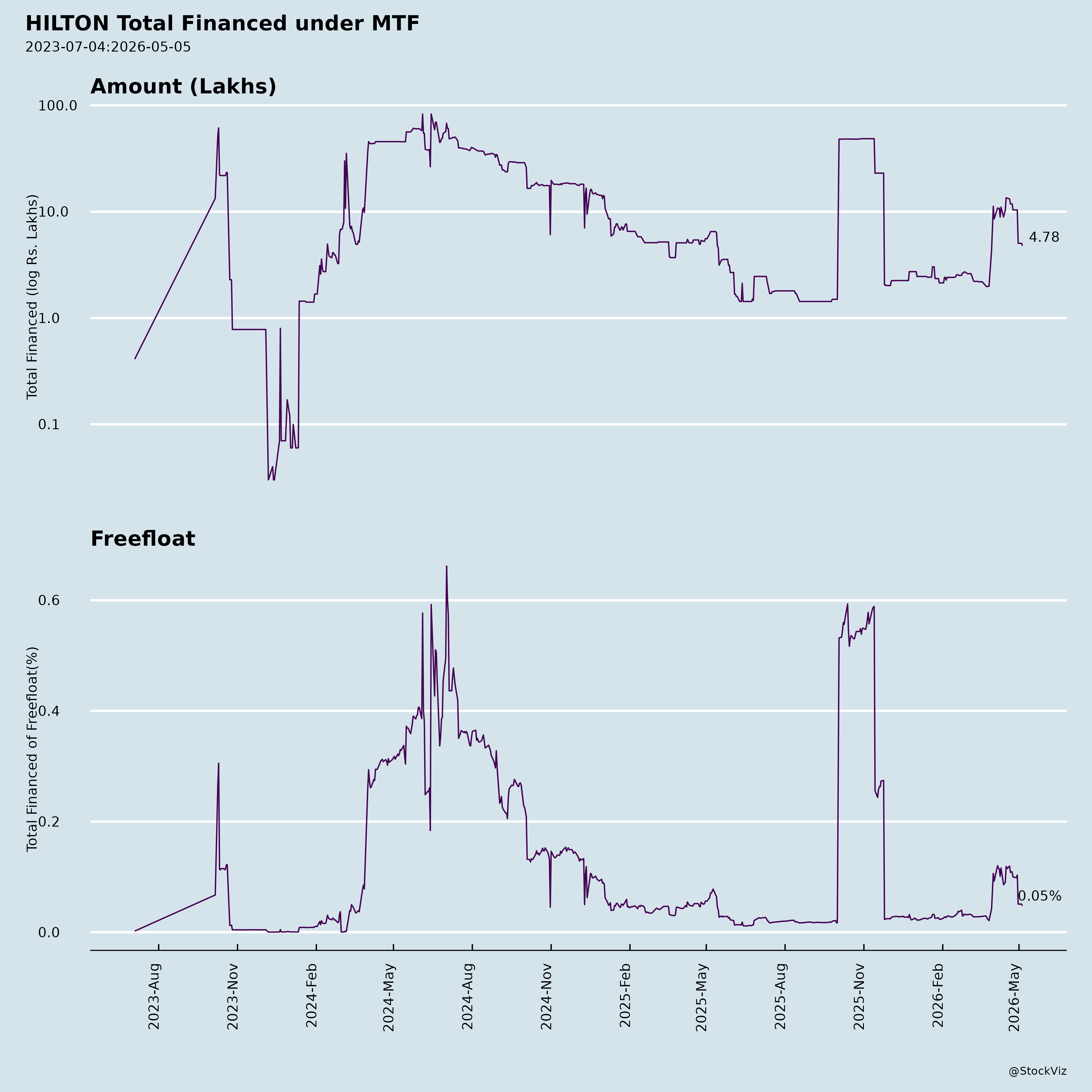

Margined

AI Summary

asof: 2025-11-27

Analysis of Hilton Metal Forging Ltd. (HILTON: NSE/BSE)

Company Overview: Hilton Metal Forging Ltd. (CIN: L28900MH2005PLC154986) is a government-recognized export house manufacturing forging components (e.g., flanges, forged fittings). It is listed on BSE (532847) and NSE (HILTON). Recent filings (Q2/H1 FY26 results for quarter/half-year ended Sep 30, 2025; EGM notice for Dec 2, 2025) show robust revenue growth amid expansion plans, but with working capital strains and debt buildup. FY25 full-year revenue was ₹16,305 Lacs with PAT ₹618 Lacs; H1 FY26 revenue jumped 41% YoY to ₹10,969 Lacs, PAT up 58% to ₹189 Lacs.

Tailwinds (Positive Factors)

- Explosive Revenue Growth: Q2 FY26 revenue surged to ₹8,764 Lacs (4x QoQ from ₹2,205 Lacs; 100% YoY from ₹4,375 Lacs), driven by operations (raw materials consumed up sharply). H1 revenue +41% YoY signals strong order book, export demand, or capacity ramp-up.

- Profitability Momentum: PAT H1 FY26 at ₹189 Lacs (+58% YoY); EPS ₹0.81 (basic/diluted). Margins stable despite scale-up; low exceptional items.

- Certifications & Recognition: ISO 9001:2015, PED 2014/68/EU, AD-2000 Merkblatt WO – enhances export credibility in forging sector.

- Strategic Moves: EGM seeks to increase authorized capital (₹35 Cr to ₹55 Cr) for future equity raises (rights issue postponed but hinted). Investment limit hike to ₹50 Cr under Sec 186 allows diversification into assets (real estate, gold, stocks, etc.) for yield optimization.

- Balance Sheet Strength: Equity base solid at ₹11,749 Lacs (52% of assets); other equity up to ₹9,409 Lacs. PPE +22% YoY to ₹2,934 Lacs; CWIP at ₹2,152 Lacs signals capex.

Headwinds (Challenges)

- Working Capital Drag: Inventories +9% to ₹9,143 Lacs; trade receivables +29% to ₹5,053 Lacs (current) – led to negative operating cash flow of -₹564 Lacs in H1 FY26 (vs +₹273 Lacs FY25). Trade payables up 44% to ₹4,122 Lacs indicates stretched suppliers.

- Debt Burden: Total borrowings up to ₹6,744 Lacs (non-current +29%, current -8%); finance costs H1 ₹311 Lacs. Debt/Equity ratio not disclosed but implied leverage rising.

- Cash Burn: Net cash decrease of ₹22 Lacs in H1; capex ₹253 Lacs amid negative ops cash flow strains liquidity. Earmarked deposits (₹637 Lacs) suggest restricted cash.

- Postponed Fundraising: Rights issue deferred for deeper deliberation – signals potential liquidity/funding gap despite growth.

- Macro Pressures: Forging sector exposed to volatile steel/raw material prices, global trade slowdowns (e.g., exports to EU/US).

Growth Prospects

- High: Revenue trajectory (Q2 4x QoQ) positions for FY26 doubling (projected ₹25,000+ Lacs if sustained). Export house status + certifications support international orders. Capex (CWIP ₹2,152 Lacs) for capacity expansion.

- Fundraise Enablers: Auth capital increase unlocks equity dilution (e.g., rights/FPO). ₹50 Cr investment flexibility for high-yield assets amid surplus funds.

- Diversification: Potential into new asset classes; single-segment ops (Ind AS 108 compliant) but scalable in forging demand (auto, oil&gas, infra).

- EGM Outcomes: Passage (Dec 2 via VC/OAVM) could catalyze growth; record date Nov 24, e-voting Nov 29-Dec 1.

Key Risks

| Risk Category | Description | Mitigation/Impact |

|---|---|---|

| Liquidity/Execution | Negative ops cash flow; high WC cycle (receivables/inventories). Rights delay. | Monitor Q3 results; high if growth continues without funding. |

| Debt & Interest | Borrowings up 20%+ YoY; finance costs 3% of revenue. | Refinance risk in rising rate environment; Debt Service Coverage not disclosed. |

| Related Party | CFO Mohak Malhotra (promoter relative) remuneration hike to ₹60 Lacs/annum (Ordinary Resolution). Arm’s length but scrutiny risk. | Shareholder approval needed; governance flag. |

| Operational | Single segment; raw material volatility (83% of Q2 expenses). Forex gains minor (₹13 Lacs). | Supply chain disruptions; 100% e-voting reliance for EGM. |

| Market/Regulatory | Metals cyclicality; SEBI/MCA compliance (e.g., Reg 30/47 disclosures). Share capital alteration needs filings. | Stock volatility (recent filings show promoter control). |

| Other | No subsidiaries/JVs; audit limited review (no full audit till FY26). OCR noise in filings (irrelevant). | Expansion delays if EGM resolutions fail. |

Overall Summary: Bullish near-term on growth (Strong Buy tailwinds from revenue surge/capex) but cautious on liquidity/debt (monitor Q3 cash flow). FY26 PAT could exceed FY25 if Q2 momentum holds, fueled by exports/expansion. EGM critical for capital flexibility; risks tilted toward execution/financing. Target upside 20-30% if rights issue materializes post-EGM; downside on WC mismanagement. Investors: Watch debt ratios, EGM voting (cut-off Nov 24), next board meet for rights update. (Data as of Nov 13, 2025 filings).

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.