Castings & Forgings

Industry Metrics

May 8, 2026

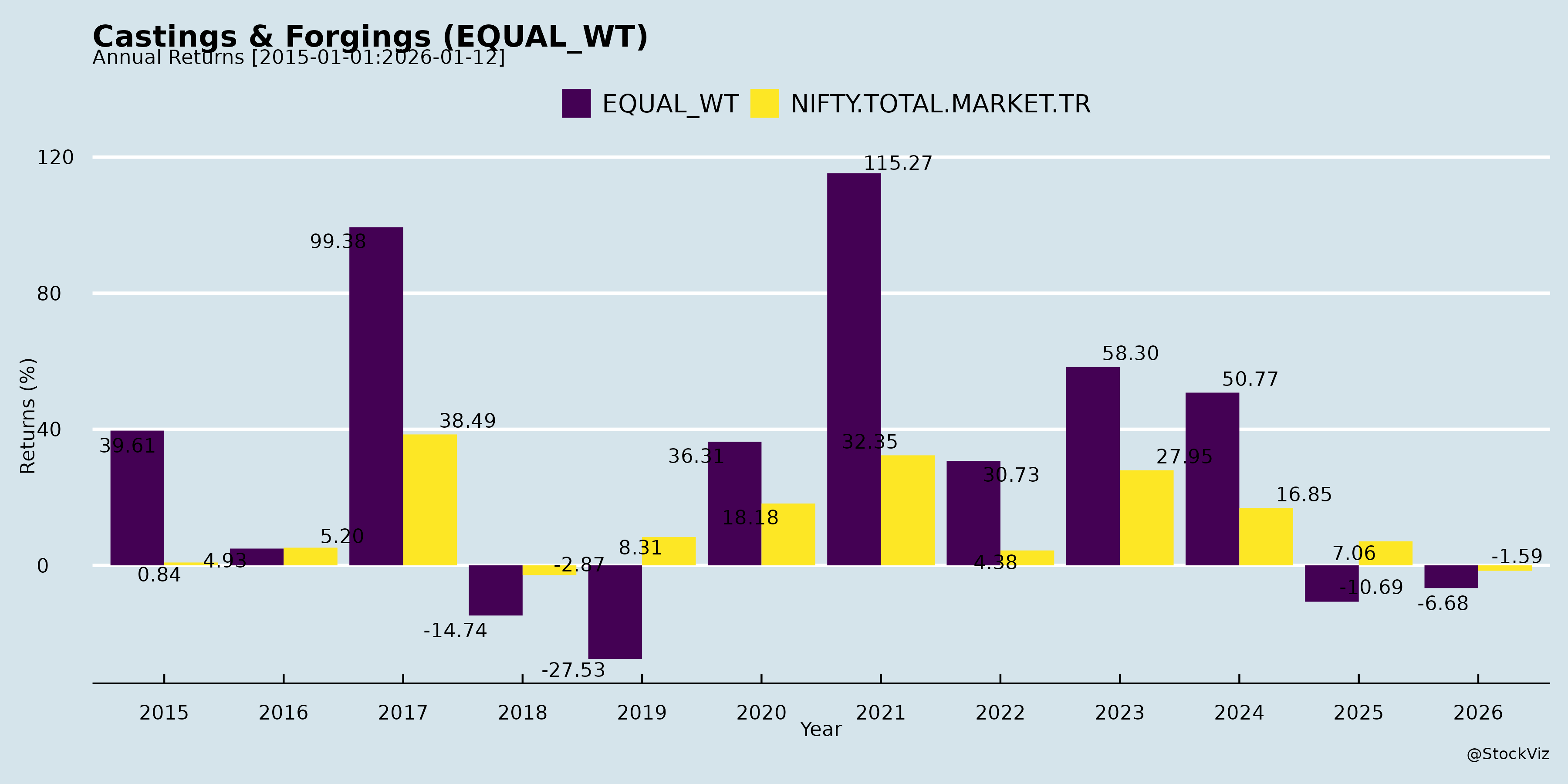

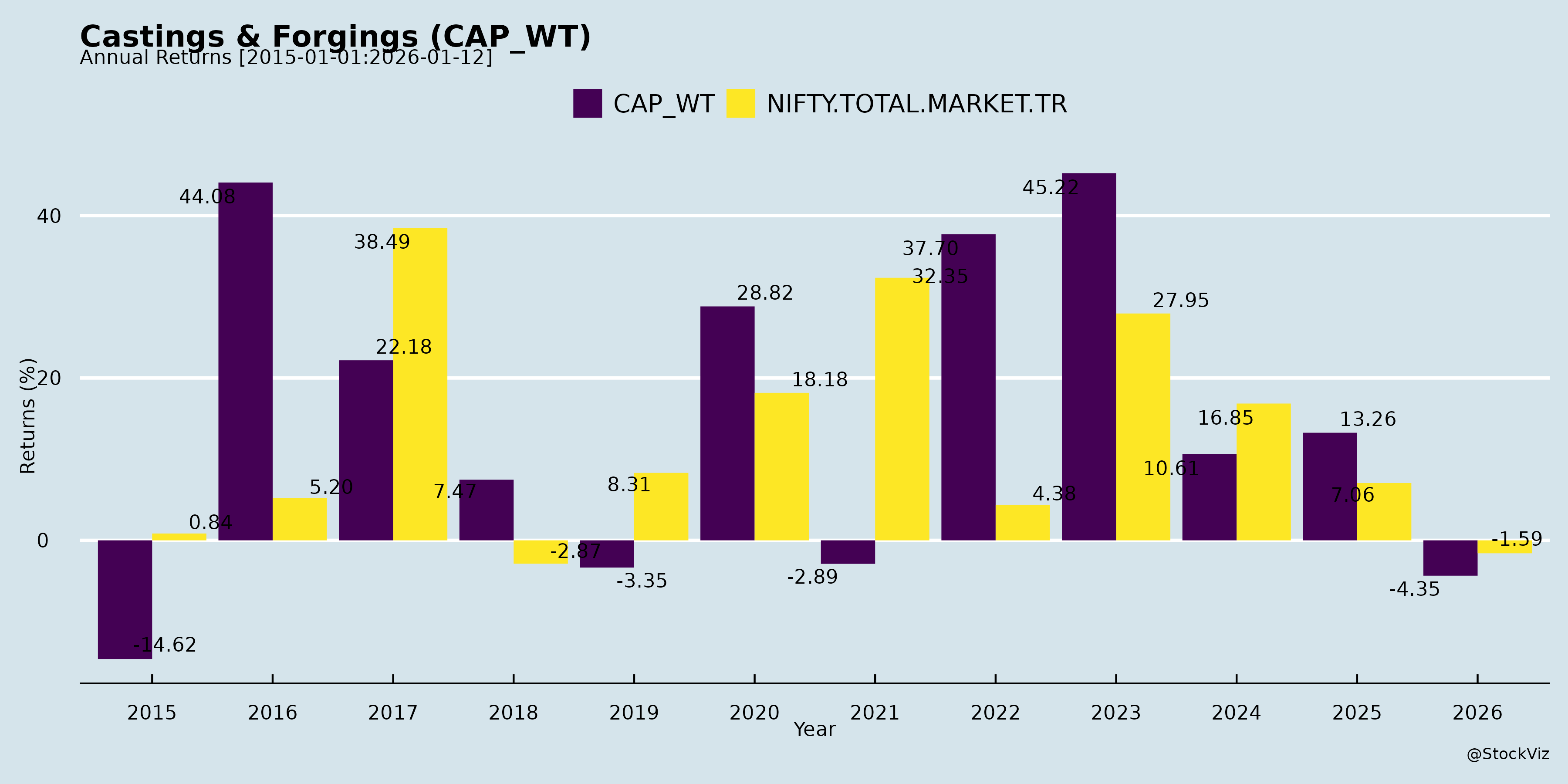

Annual Returns

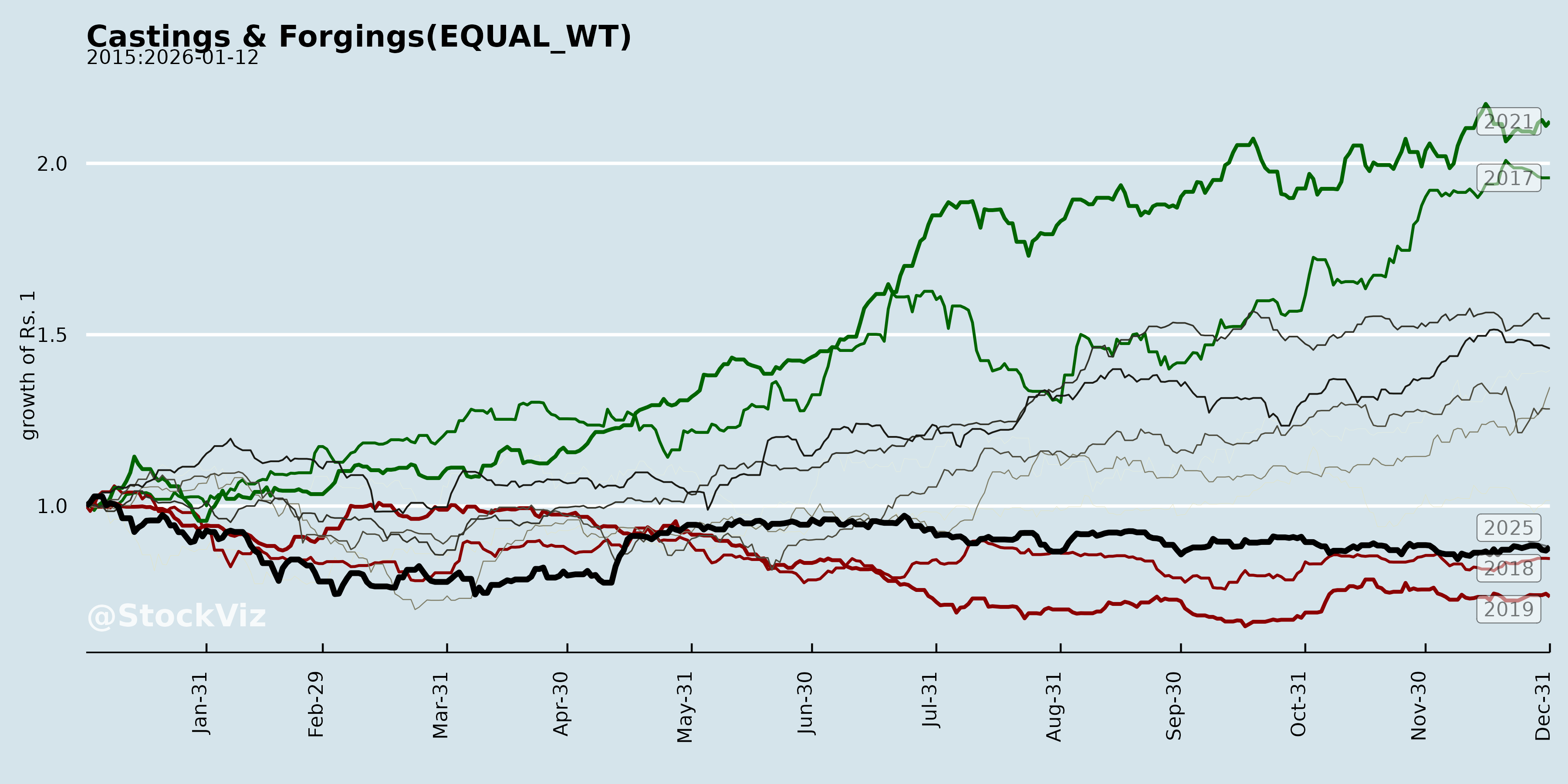

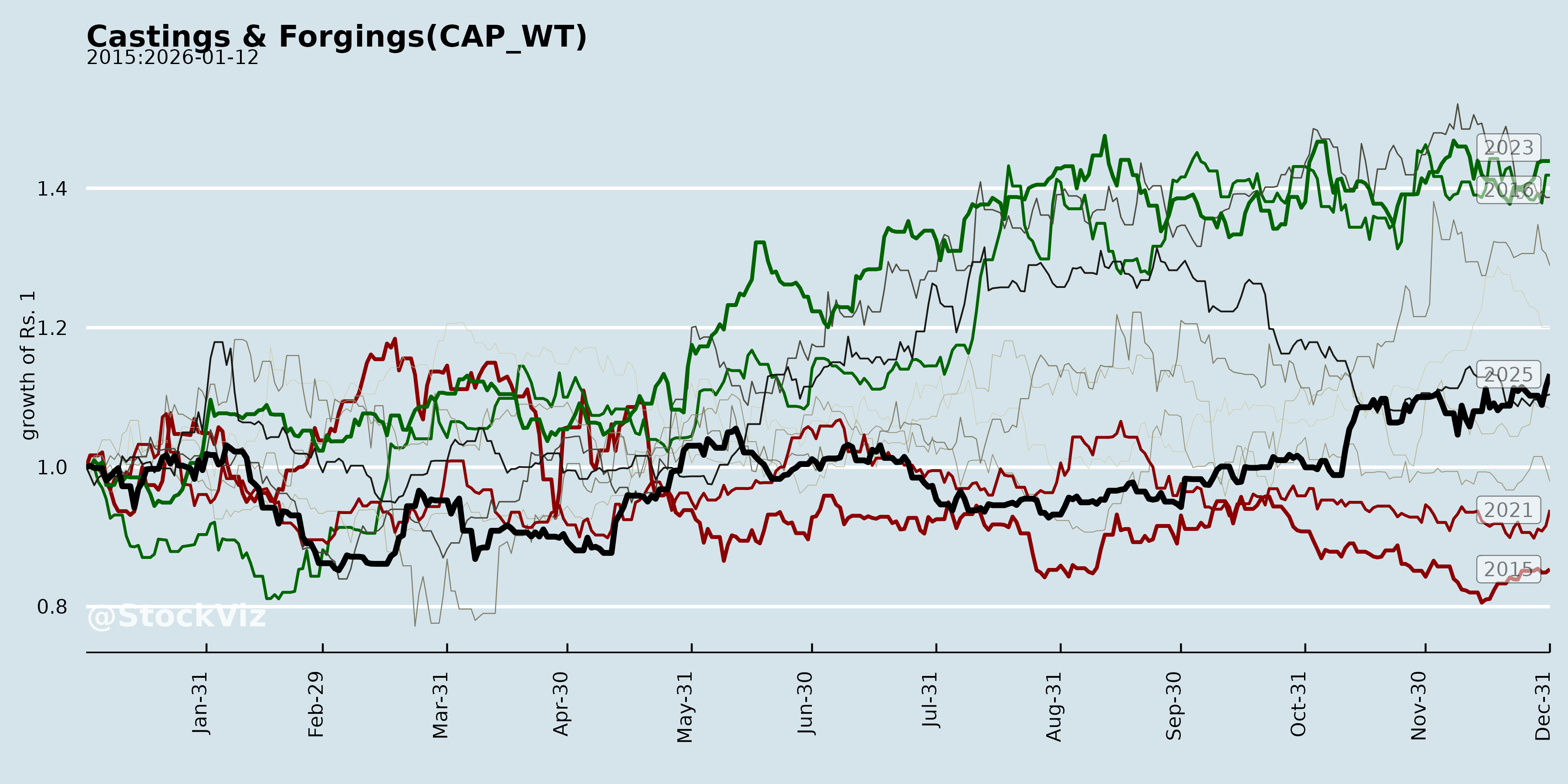

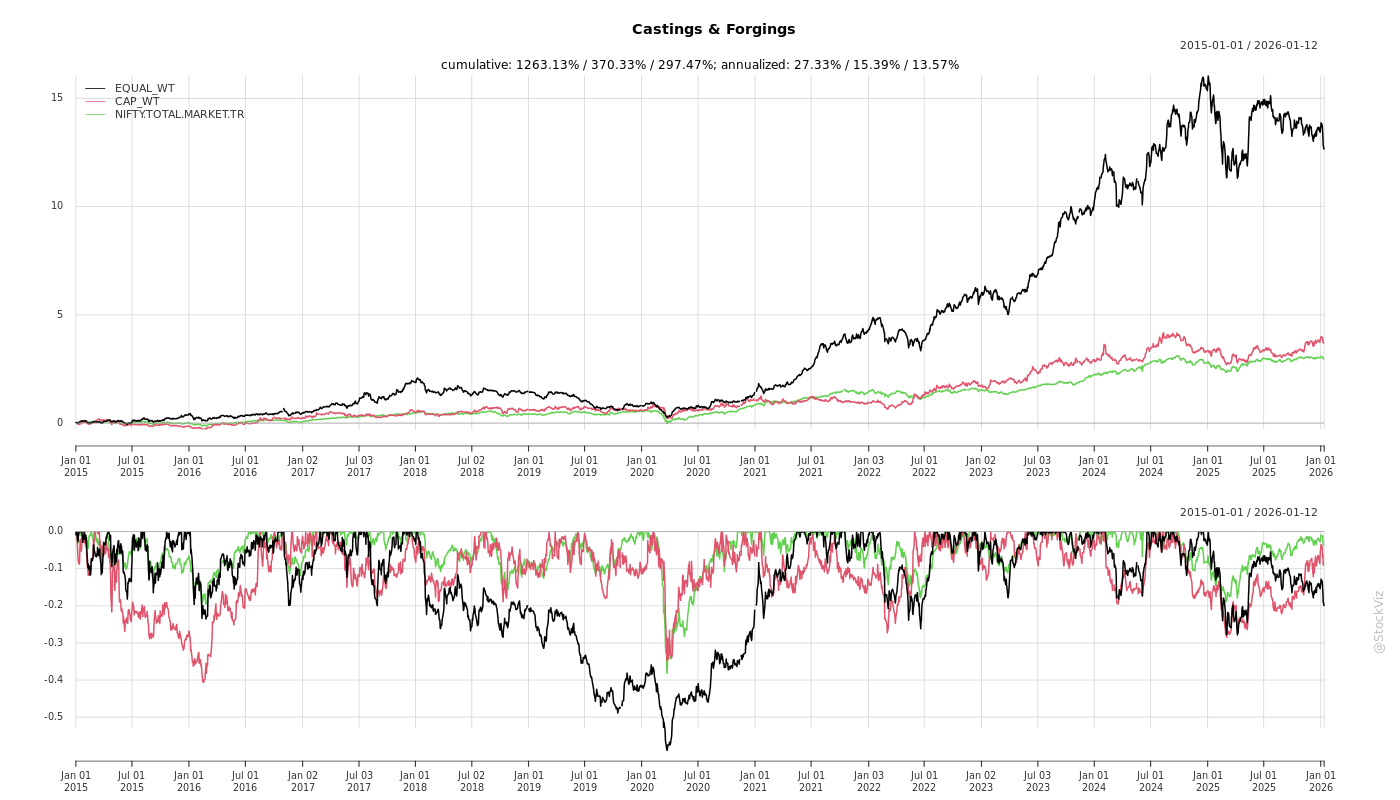

Cumulative Returns and Drawdowns

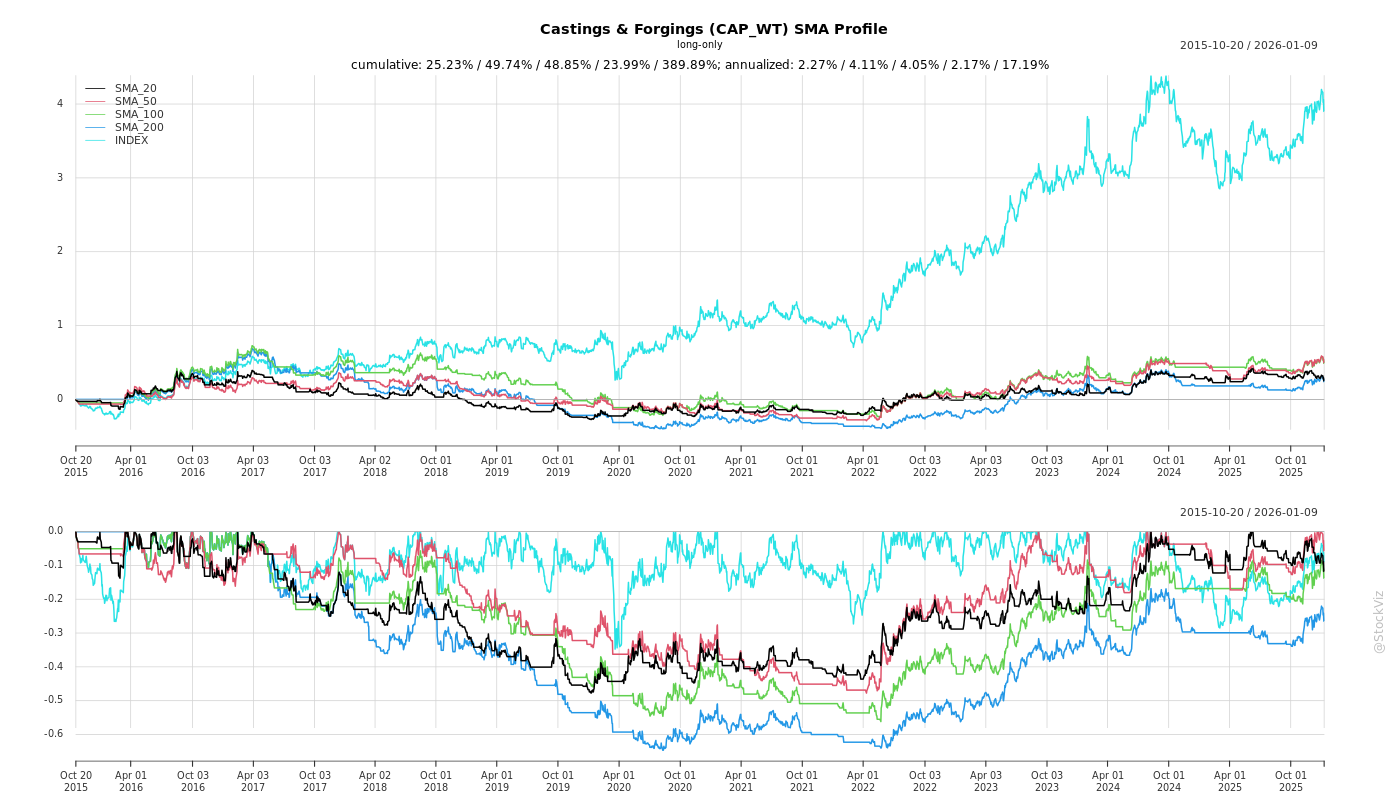

SMA Scenarios

Current Distance from SMA

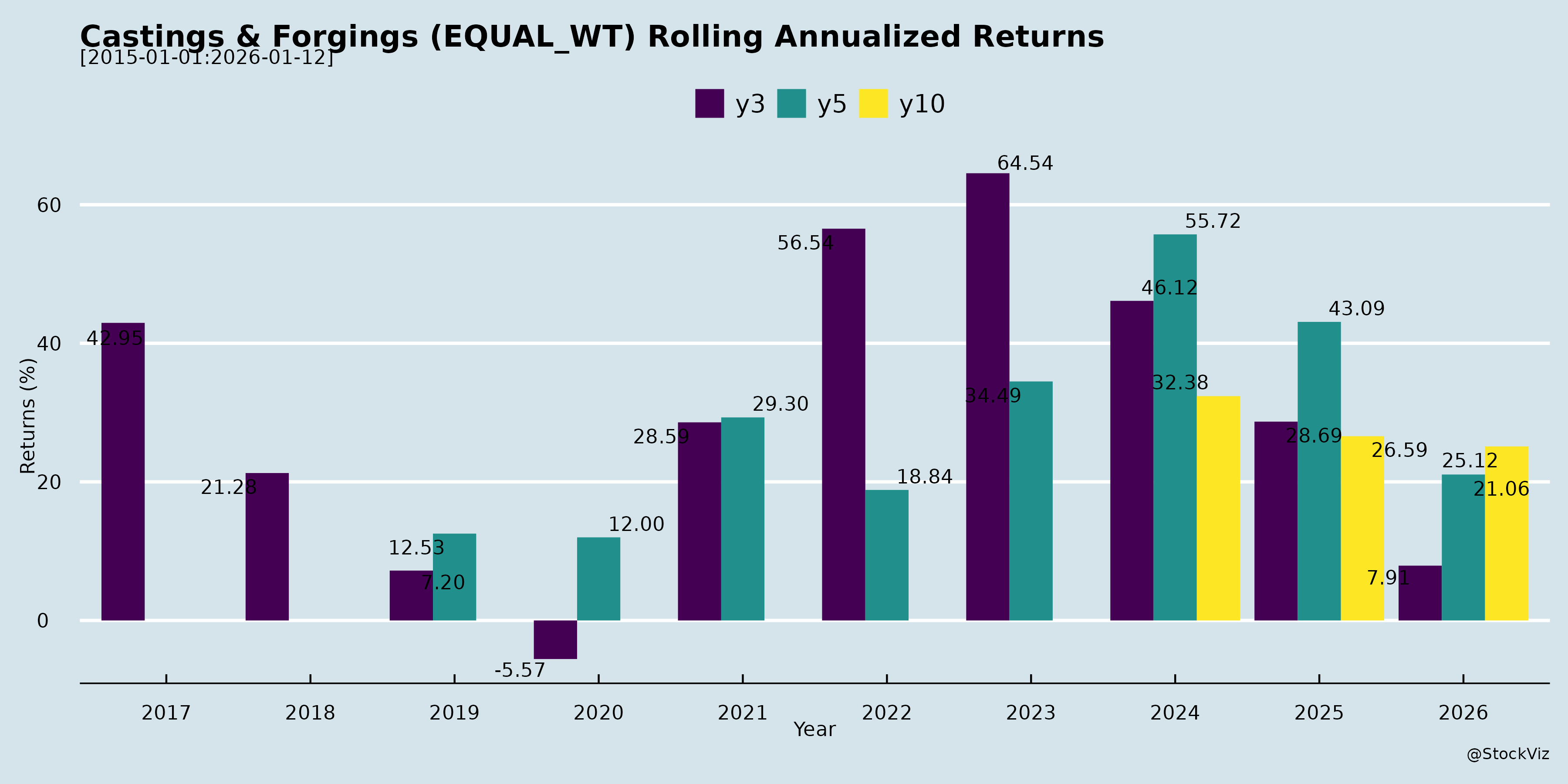

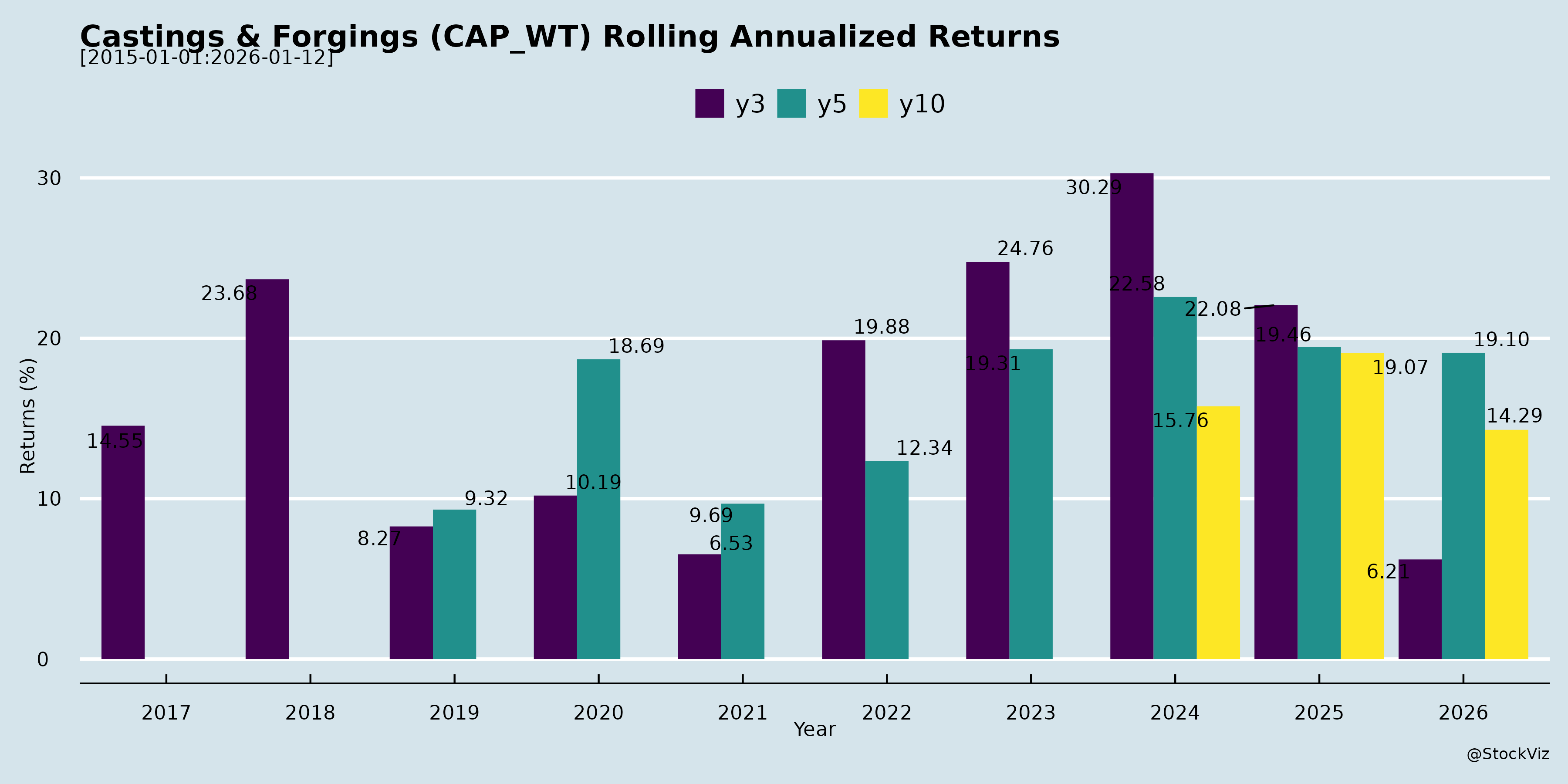

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-15

The manufacturing, forging, and precision engineering sectors have experienced a significant evolution in their operational landscapes, navigating a transition from severe macroeconomic and supply chain headwinds to unlocking highly lucrative, structural growth avenues.

Over time, the challenges and opportunities for these industries have evolved in the following ways:

The Evolution of Challenges

- Geopolitical Instability and Supply Chain Fragility: Manufacturers have increasingly had to contend with a tremendous amount of global instability, driven by geopolitical conflicts in regions such as the Middle East (Iran) and Southeast Asia [1, 2]. This has resulted in highly fragile shipping lanes, leading to severe risks regarding container availability, shipping line reliability, extended transit times, and extreme volatility in freight costs [3, 4].

- Trade Barriers and Protectionist Policies: A major historical challenge has been the rise of global protectionism, with countries erecting borders and imposing punishing tariffs to protect domestic interests [3-6]. Companies like AIA Engineering lost upwards of 75,000 to 80,000 tons of volume across regions like South Africa, Canada, and Brazil due to these duties [7-10]. Similarly, Tirupati Forge faced adverse impacts on its export-driven sales due to the U.S. tariff regime [11].

- Operational Disruptions and Customer Delays: Companies undergoing aggressive capacity expansions or relocations have faced short-term profitability hits. For instance, Synergy Green Industries and Balu Forge experienced disruptions and significantly higher outsourcing costs while relocating equipment and integrating new facilities [12-17]. Furthermore, unexpected commercial and warranty discussions have caused significant pushbacks in serial production and serial supply schedules from major customers [18-21].

- Raw Material Volatility and Depleting Ore Grades: For suppliers to the mining sector, a significant headwind is the depleting quality and grade of mined ore, which continuously reduces mine output [22-25]. Additionally, severe volatility in commodity prices, such as sudden spikes in copper and steel, heavily pressures profit margins because price corrections with customers often come with a one-quarter lag [26, 27].

The Evolution of Opportunities

- Strategic Pivot to Defense and Aerospace: To mitigate historical challenges, companies have aggressively diversified into high-margin sectors like defense and aerospace, heavily bolstered by the government’s “Make in India” initiative, which earmarks 75% of its ₹6.8 lakh crore defense budget for domestic procurement [28, 29]. Global defense spending is projected to reach $2.5 trillion by 2028, presenting exponential growth avenues [29, 30]. Manufacturers are successfully commercializing production lines for 155mm artillery shells and entering the elite NATO supply chain [31-34].

- Favorable Shifts in Currency and Free Trade Agreements (FTAs): The depreciation of the Indian Rupee (INR) against the Chinese Yuan has virtually erased China’s historical cost advantage, making Indian manufacturers highly competitive and incentivizing OEMs to source domestically [35, 36]. Additionally, recent Free Trade Agreements with the U.S. and Europe, along with the rollback of certain tariff barriers, have drastically improved export sentiment and demand visibility [37-40].

- The Structural Bull Run in Critical Minerals and Renewables: The global transition to renewable energy, data centers, and EVs has created a “clear and present danger” of copper shortages; the world will need to mine as much copper in the next 20 years as it has in all of human history just to sustain a 3% growth rate [41-44]. This creates a massive, multi-decade opportunity for companies providing advanced grinding media and mill-liner solutions to global gold and copper miners to help them improve throughput without incurring major CapEx [23, 25, 45, 46]. In the renewable sector, changes in state tariff policies—such as penalizing solar generation while incentivizing wind—have driven a renewed surge in domestic demand for wind turbine castings [47, 48].

- Value-Added Engineering and Business Mix Optimization: Rather than chasing low-margin volume, companies have strategically pruned their order books to exit unrelated, legacy, or low-growth product lines [49, 50]. By upgrading to precision engineering technologies—such as 7-axis and 11-axis CNC machining, 25-ton hydraulic forging hammers, and warm forging—manufacturers are now capable of delivering mission-critical, fully machined components with micron-level accuracy [51-54].

- Captive Green Energy and ESG Integration: To optimize operational expenditures, heavy manufacturers are actively commissioning captive solar power plants. For example, Tirupati Forge’s 4.8 MW solar plant is projected to save ₹25 million to ₹50 million annually in electricity costs [55, 56]. Similarly, Synergy Green and Happy Forgings are leveraging captive solar infrastructure to significantly reduce their power costs and directly improve their bottom-line profitability while meeting ESG goals [57-59].

What are the headwinds affecting this industry?

asof: 2026-04-15

Geopolitical Instability and Trade Barriers The industry is grappling with a tremendous amount of instability stemming from geopolitics and regional wars, such as conflicts involving Iran and in the Southeast [1, 2]. This has led to a highly protectionist global environment where countries are increasingly imposing borders, duties, and protective measures [3, 4]. For instance, companies have collectively lost tens of thousands of tons in sales volumes over recent years due to punishing duties in countries like South Africa, Canada, and Brazil [5-12]. Additionally, ongoing uncertainty surrounding the U.S. tariff regime—which has seen tariffs as high as 50%—has adversely affected export-driven sales and volumes, and has forced suppliers to offer discounted pricing to help customers offset these heavy tariff burdens [13-16].

Shipping and Logistics Risks Due to the aforementioned geopolitical tensions, global shipping lanes have become fragile and highly unpredictable [1, 4]. This creates significant ongoing risks regarding container availability, shipping line availability, and extended transit times [1, 4]. Furthermore, the industry is facing extreme volatility in shipping costs, complicating international trade and profitability [1, 4].

Commodity Price Volatility and Resource Scarcity Companies are facing severe headwinds related to raw materials. Sudden surges and high volatility in commodity prices (with increases of 8-10% occurring over very short periods) are putting immediate pressure on margins, as there is typically a lag of a quarter or more before these increased costs can be passed on to customers [17-20]. Conversely, a decline in steel prices has also been cited as a factor dragging down top-line revenues for certain players [16].

There is also a structural crisis in the mining of critical metals like copper [21-24]. Existing mines are experiencing reduced production tonnages month-over-month due to depleting ore grades, meaning their output is actually going down [25-30]. Bringing new mines online to meet global demand takes 7 to 10 years and is heavily hindered by ecologically sensitive environments and local political issues [26, 29, 31, 32].

Operational and Execution Disruptions Internal operational shifts, such as relocating manufacturing equipment to new plant units or executing major capacity expansions, have caused severe disruptions [33-36]. Moving large workforces and equipment has resulted in unexpected delays, a lack of immediate output, and significantly higher outsourcing costs to meet existing customer schedules while internal machines were offline [37-42]. Challenges with civil execution and external contractors have further delayed project timelines [43, 44].

Commercial Delays and Demand Softness There is a general conservatism among customers when it comes to adopting new solutions or transitioning from a proof of concept to full commercial engagement, leading to a lack of clear signalling and delayed timelines [45-48]. Expected serial production for major clients has been dragged out or postponed due to extended commercial discussions and warranty-related queries [33, 35, 49, 50]. Additionally, there is notable demand softness in specific end-markets, such as the auto sector, which further weighs down sales performance [16].

Rising Labor Costs and Regulatory Changes The industry is seeing an increase in operating expenses due to high employee benefit costs and wage agreements necessary to retain quality staff [37, 51-53]. Furthermore, companies are having to make financial provisions for the implementation of new government Labor Codes, adding an additional layer of expense to their balance sheets [37, 40, 54, 55].

What are the key things to understand about this industry?

asof: 2026-04-15

The precision engineering, forging, and casting industry is undergoing a significant structural transformation driven by macroeconomic trends, geopolitical shifts, and technological advancements. Here are the key things to understand about the current state and trajectory of this industry:

1. Robust Market Growth and the “Make in India” Advantage The Indian forging industry is expanding at a Compound Annual Growth Rate (CAGR) of 9.8%, significantly outpacing the global forging industry’s growth rate of 7.6% [1, 2]. This growth is heavily supported by the automotive sector, which accounts for over 60% of India’s forging units [2]. Additionally, the industry is benefiting immensely from the government’s “Make in India” initiative and a strategic shift by global Original Equipment Manufacturers (OEMs) to outsource components from lower-cost manufacturing hubs [2].

Defense indigenization is a massive catalyst for this sector. With the Indian government earmarking 75% of its INR 6.8 lakh crore defense budget for domestic procurement, and projecting $130 billion in military spending over the next five years, forging companies are pivoting heavily to capture this high-margin market [3].

2. Moving Up the Value Chain into High-Margin Sectors To capitalize on these new opportunities, companies are transitioning from basic forging to offering fully finished, precision-machined solutions. Manufacturers are deploying advanced technologies, such as 7-axis and 11-axis CNC machining lines, IoT-enabled equipment, and robotics, which allow them to process complex alloys (like titanium and aluminum) with micron-level accuracy [4-6].

This technological upgrade enables entry into highly specialized, margin-accretive sectors such as Aerospace, Railways, and Defence [6-8]. For example, Indian forging companies are now securing approvals to manufacture critical defense components like 155mm M107 artillery shells and have even been inducted into the global NATO supply chain [8-10].

3. Geopolitical Tailwinds and Changing Trade Dynamics While global protectionist measures and tariffs have historically caused volume losses in certain regions, the current geopolitical landscape strongly favors Indian manufacturers [11, 12]. * Currency Advantages: The depreciation of the Indian Rupee (INR) against the Chinese Yuan by approximately 15% has effectively erased China’s historical cost advantage, making Indian castings and forgings 3% to 5% cheaper than Chinese imports [13, 14]. * Tariff Barriers on Competitors: High tariffs imposed by the US on Chinese imports (up to 50%) have severely distorted China’s competitiveness, allowing Indian castings to become highly attractive in the US market [14]. * Free Trade Agreements (FTAs): Upcoming FTAs with regions like Europe and the United States are expected to unlock further long-term benefits and lower trade barriers for Indian auto-component and forging players [15, 16].

However, the industry must still navigate the risks of volatile shipping lanes, fluctuating container availability, and unpredictable freight costs caused by ongoing geopolitical conflicts [12, 17].

4. Sector-Specific Demand: Mining and Commodities The mining consumable wear-parts industry is experiencing a structural bull run, particularly in copper. Copper demand is skyrocketing due to the expansion of data centers, renewable energy transmission, and electronic devices [18, 19]. However, copper miners are grappling with declining ore grades, meaning they must process significantly more volume to yield the same amount of metal [20, 21].

To address this, forging and metallurgy companies are designing advanced high-chrome grinding media and mill liners [22]. These solutions are critical because they lower wear rates, reduce energy consumption, and increase crushing and grinding throughput, allowing miners to maintain or improve output without incurring major capital expenditures [21, 23, 24].

5. Sector-Specific Demand: Wind Energy and Conventional Power The casting industry is seeing a massive resurgence in demand from the energy sector. * Wind Energy Revival: After years of heavy solar installation, energy grids are realizing that round-the-clock power cannot rely on solar alone [25]. Regulatory shifts—such as local electricity boards penalizing solar generation while incentivizing wind power—have drastically altered cost dynamics, sparking a rush for wind turbine installations [25]. * Conventional Power Expansion: The Indian government’s clearance for 80,000 megawatts of conventional power installations has created an enormous backlog for OEMs [26]. This translates into a highly visible, decade-long demand pipeline for massive 25 to 30-tonne castings [26, 27].

6. Business Mix Optimization and Operational Discipline To improve structural profitability, leading companies are aggressively undertaking “business mix optimization” [28, 29]. Rather than chasing random top-line revenue growth, manufacturers are deliberately pruning low-margin, non-core product lines and exiting relationships with high credit-risk customers [28, 30, 31]. By freeing up capacity and eliminating misfit businesses, companies can dedicate their resources to high-volume, high-value OEM programs that offer better economies of scale and capacity utilization [31].

Finally, the industry remains sensitive to raw material and commodity price volatility [32]. Increases in commodity prices generally squeeze margins in the short term, though companies typically manage this risk through back-to-back hedging and price-adjustment contracts that pass costs onto the customer with a one-quarter lag [32].

What are the tailwinds affecting this industry?

asof: 2026-04-15

Favorable Trade Dynamics and Currency Shifts The casting, forging, and precision engineering industry is benefiting significantly from shifting global trade policies and currency fluctuations. The depreciation of the Indian Rupee (INR) by almost 15% against the Yuan has dramatically improved the competitiveness of the Indian market, effectively erasing the previous cost advantage held by China and strongly incentivizing original equipment manufacturers (OEMs) to source locally rather than importing [1, 2]. Globally, buyers are actively seeking non-Chinese suppliers to mitigate supply chain risks [3, 4].

Additionally, reductions in trade tariffs have bolstered export viability. For instance, U.S. tariffs on Chinese goods previously created market distortions, but with tariffs on Indian castings dropping back to 18%, Indian manufacturers have become highly competitive in the U.S. market [5, 6]. Relief in U.S. tariffs on engineering and auto-related products has further improved trade sentiment, providing excellent medium-term demand visibility since over 50% of certain export demands are linked to the U.S. [7, 8]. Furthermore, upcoming Free Trade Agreements (FTAs) with Europe and the U.S. are anticipated to provide long-term structural advantages to Indian auto-component and forging players [9, 10]. India’s ecosystem—which encompasses the whole value chain from design and pattern making to production and metallurgy—makes it uniquely positioned to capture this demand [11, 12].

Surge in Defense Spending and “Make in India” The defense sector is providing a massive growth runway, driven by both domestic policy and international geopolitical tensions. Global defense spending is rising sharply due to geopolitical instability and the rapid depletion of weapon stockpiles, with global defense budgets projected to reach USD 2,546.9 billion by 2028 at a CAGR of 4.9% [13, 14].

Domestically, the government’s “Make in India” and “Atmanirbhar Bharat” initiatives are highly prioritizing local manufacturing [15-17]. The Ministry of Defence has received a budget allocation of INR 6.8 lakh crore, with 75% explicitly earmarked for procurement from domestic manufacturers [14, 18]. India is projected to spend $130 billion on its military over the next five years, driving an expected 13% CAGR in the domestic defense sector from FY23 to FY30 [14, 18]. This is prompting engineering companies to successfully pivot toward high-precision defense manufacturing, such as the production of large-caliber artillery shells and aerospace components [17, 19, 20].

Commodity Supercycle and Mining Inefficiencies The mining consumable industry is experiencing a massive tailwind due to a structural bull run in key metals, particularly copper. The world will need to mine as much copper in the next 18 to 20 years as it has in the entirety of human history just to maintain a standard 3% global growth rate, fueled heavily by the exponential demand from AI data centers, renewable energy infrastructure, and electronic devices [21, 22].

Concurrently, mines are facing the severe challenge of depleting ore grades, meaning their overall output is declining even as demand skyrockets [23, 24]. This dichotomy creates a “clear and present danger” of global copper shortages [25, 26]. Consequently, miners are desperate to improve their crushing and grinding efficiencies without incurring massive capital expenditures [23, 27]. This provides a massive opportunity for providers of high-chrome grinding media and mill liners, especially considering that the penetration of high-chrome solutions is currently only 25% to 35% in a massive addressable market of 1.5 to 2 million tons [28, 29].

Renewables Rebalancing and Conventional Power Expansion The energy sector is witnessing a dual-pronged tailwind affecting both renewable and conventional power equipment manufacturers: * Wind Energy Resurgence: After years of heavy solar installation, energy regulators are realizing that solar alone cannot provide reliable round-the-clock power, leading to a resurgence in the wind energy sector [30, 31]. Regulatory changes are actively driving this shift; for example, the Maharashtra MSCB recently penalized solar generation by 25% while incentivizing wind by 25%, creating a 50% tariff difference that is pushing developers back toward wind turbine installations [30, 31]. * Conventional Power Revival: At the same time, the Government of India has cleared 80,000 megawatts of conventional power installations [32, 33]. This massive clearance has created enormous order backlogs for major OEMs like L&T and BHEL that exceed their internal capacities, resulting in substantial, repetitive business opportunities for heavy casting and forging suppliers to provide power equipment parts over the next decade [32-35].

Automotive, Infrastructure, and Global Outsourcing Finally, the broader automotive and infrastructure sectors are demonstrating robust growth. There is a global rise in infrastructure and construction investments [15, 36]. Domestically, there is healthy demand in key end-markets including commercial vehicles, passenger vehicles, and farm equipment [37, 38]. Furthermore, India is rapidly emerging as a global forging hub supported by advancements in forging technologies (like closed-die and precision forging) and a strategic shift by global OEMs to increasingly outsource components from manufacturers in lower-cost countries [15, 16, 36].

What is the general outlook of this industry?

asof: 2026-04-15

The general outlook for the forging, casting, and precision engineering industry is highly optimistic, characterized by robust demand across domestic and international markets, aggressive expansion into high-value strategic sectors, and significant improvements in operational efficiency.

Surging Demand in Core and Emerging Sectors The industry is experiencing strong growth momentum driven by key domestic end-markets such as Commercial Vehicles (M&HCV), passenger vehicles, farm equipment, and tractors [1-3]. Beyond automotive, the power generation sector is a massive growth driver; the Government of India has cleared 80,000 megawatts of conventional power installations, leading to huge backlogs for major infrastructure clients that guarantee demand for large industrial castings over the next decade [4, 5]. Furthermore, the renewable energy sector—specifically wind energy—is seeing a major resurgence. Because solar installations have surged in recent years without corresponding wind growth, regulatory bodies (like in Maharashtra) are increasingly incentivizing wind power to balance round-the-clock energy needs, creating a massive demand for wind turbine castings and gearboxes [6, 7].

Strategic Pivot Towards Defence and Aerospace A transformative trend across the industry is the aggressive foray into defence and aerospace manufacturing. This pivot is heavily supported by the government’s “Make in India” initiative and substantial increases in the defence budget, where up to 75% of allocations are earmarked for procurement from domestic manufacturers [8-10]. Companies are securing massive, long-term contracts to manufacture critical munitions, such as 155mm M107 and 152mm artillery shells, setting up fully automated production lines capable of producing hundreds of thousands of units annually [11-14]. Advancements in precision manufacturing have even enabled Indian firms to be inducted into the NATO supply chain for artillery shell bodies and to secure stringent global aerospace certifications for manufacturing complex components like turbine blades [12, 15, 16].

Favourable Global Trade Dynamics and Export Competitiveness The industry is benefiting immensely from macroeconomic tailwinds and a shift away from Chinese dependency: * Currency Advantage: The depreciation of the Indian Rupee (INR) against the Chinese Yuan has virtually eliminated the previous price gap between the two countries, making Indian castings highly competitive and encouraging domestic OEMs to source locally rather than importing from China [17-20]. * Trade Agreements and Tariffs: Improving India-US trade relations and relief from punitive US tariffs on engineering and auto products have significantly strengthened export visibility and demand [21-24]. Upcoming Free Trade Agreements (FTAs) with Europe and the US are viewed as highly advantageous, allowing Indian manufacturers to leverage lower tariffs to capture market share from other medium- and low-cost countries [25, 26]. * Outsourcing Trends: Global OEMs continue to shift their component outsourcing towards manufacturers in emerging hubs like India [27, 28].

Structural Bull Run in the Global Mining Sector Companies catering to the mining sector are experiencing extraordinary demand, particularly driven by copper, gold, and iron ore extraction. The world is facing a severe structural deficit in copper due to the massive requirements of global electrification, data centers, and renewable energy grids [29-32]. Furthermore, as global ore grades continually deplete, mining operations require drastically higher throughput to maintain production volumes [33-36]. This creates a massive, inelastic demand for highly efficient, high-chrome grinding media and specialized mill liners, prompting companies to secure large multi-million dollar contracts with major global mines [37].

Aggressive Capacity Expansion and Technological Upgrades To capture these growth opportunities, companies are executing their largest-ever capital expenditure (Capex) programs. The industry is rapidly scaling up its infrastructure by: * Installing heavy 8,000 to 10,000-tonne hydraulic and mechanical forging presses [38-40]. * Integrating advanced Industry 4.0 automation, robotics, and cutting-edge 7-axis and 11-axis CNC machining lines [16, 41, 42]. * Transitioning from supplying raw forgings to providing fully finished, precision-machined, and assembled components, directly moving up the value chain to capture higher margins [43, 44].

Margin Expansion Through Operational Efficiency Alongside top-line growth, the industry is structurally improving its profitability. Management teams are engaging in active business mix optimization—deliberately pruning low-volume, low-margin, and legacy export programs to free up capacity for high-value strategic accounts [45-49]. Additionally, widespread investments in captive renewable energy (like large-scale solar plants) are significantly reducing power costs, while automation and improved machine conditioning are maximizing overall equipment effectiveness (OEE) and EBITDA margins [42, 50-55].

Potential Headwinds While the outlook is overwhelmingly positive, the industry must navigate a few macro challenges. These include geopolitical uncertainties that cause fragile shipping lanes, container shortages, and volatile freight costs [56-59]. Additionally, sudden fluctuations in commodity prices (such as steel and copper) can temporarily pressure margins until price adjustments are negotiated with customers in subsequent quarters [60-63]. However, the overall consensus is that strong domestic policies, technological upgrades, and shifting global supply chains have positioned the industry for sustainable, multi-year growth.

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.