EUREKAFORB

Equity Metrics

May 8, 2026

Eureka Forbes Limited

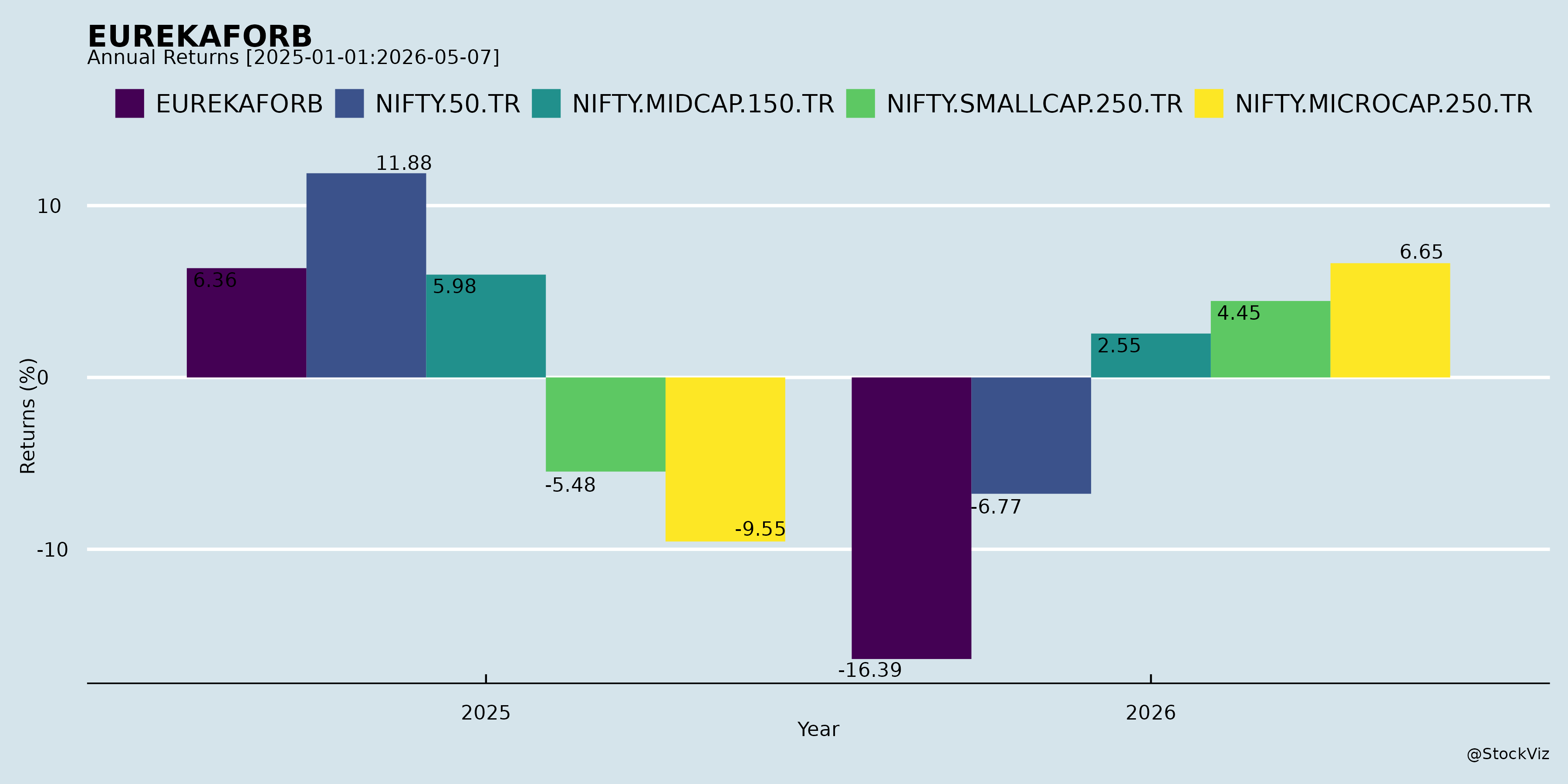

Annual Returns

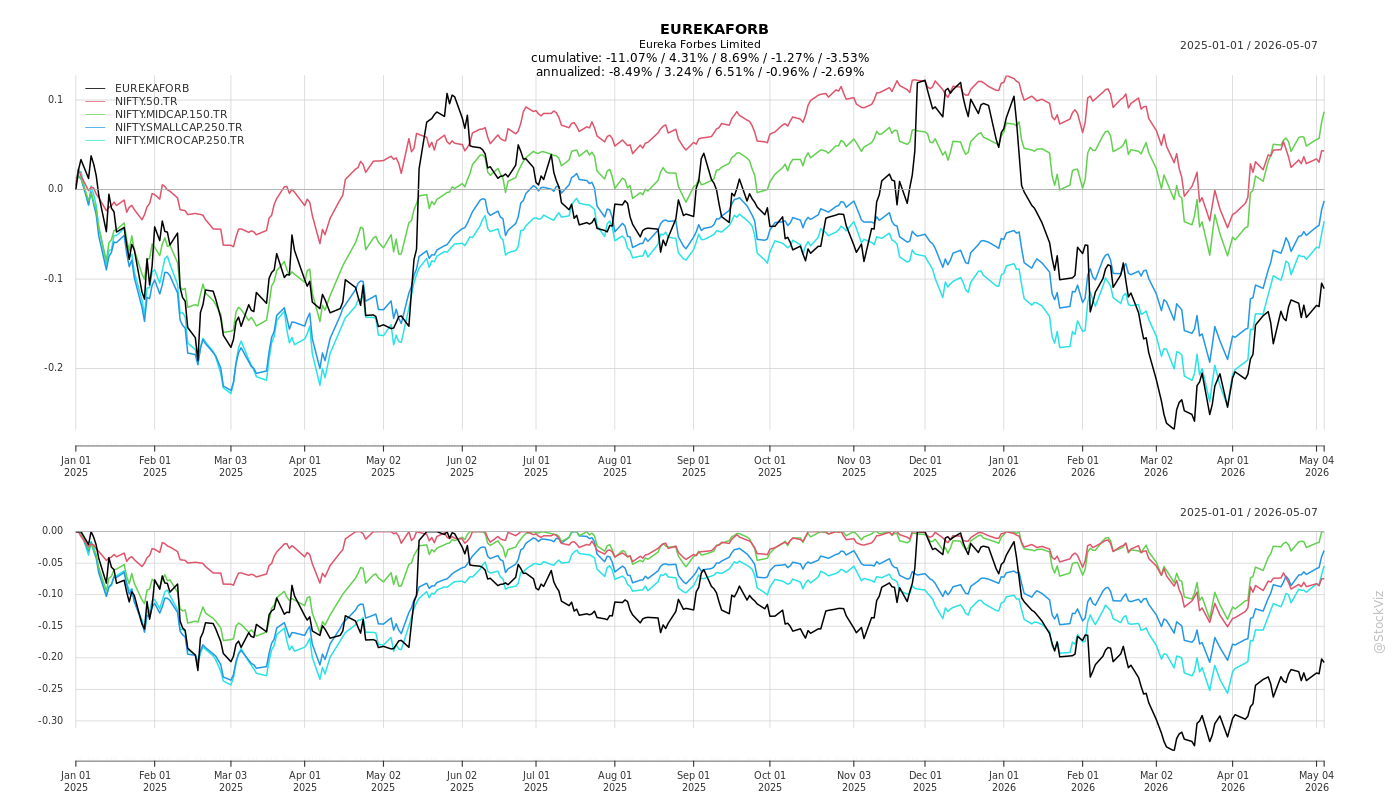

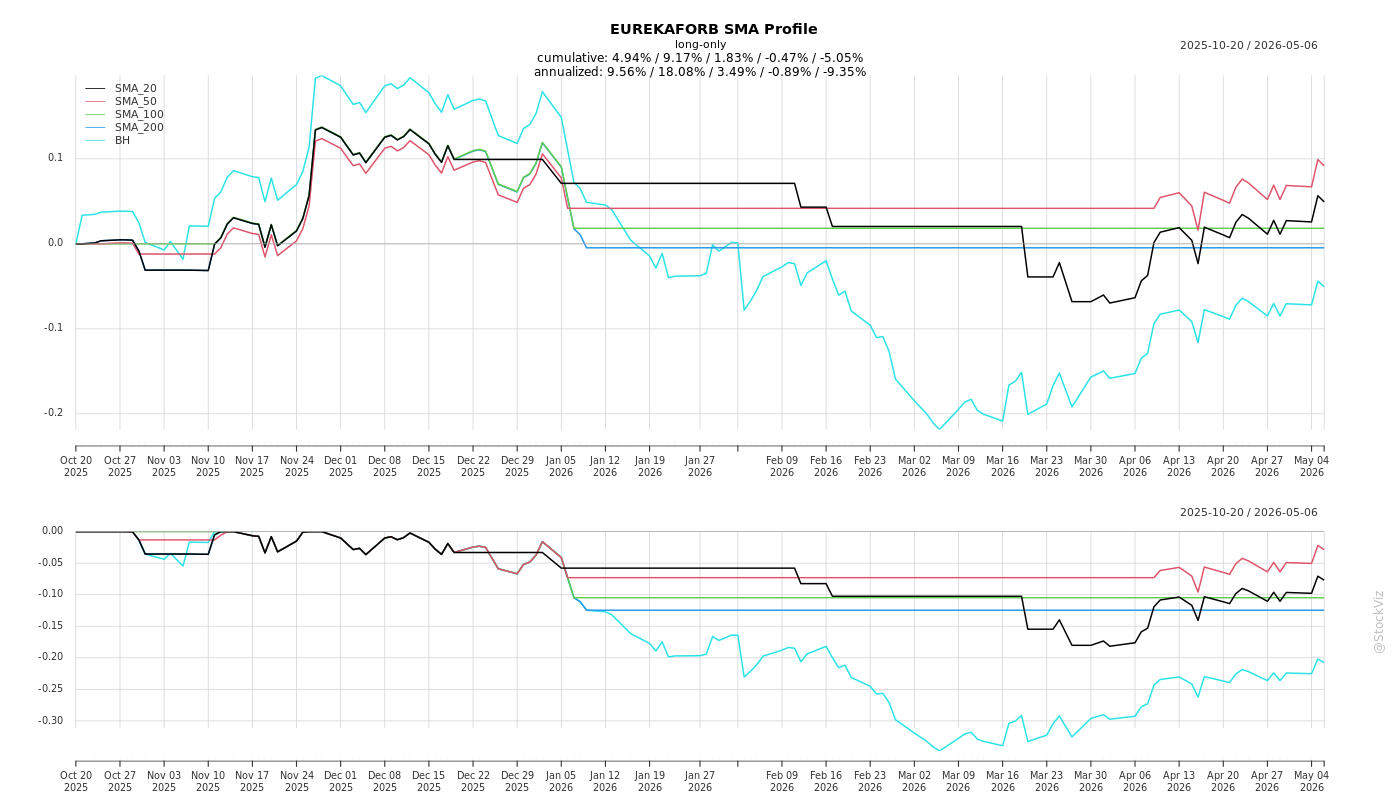

Cumulative Returns and Drawdowns

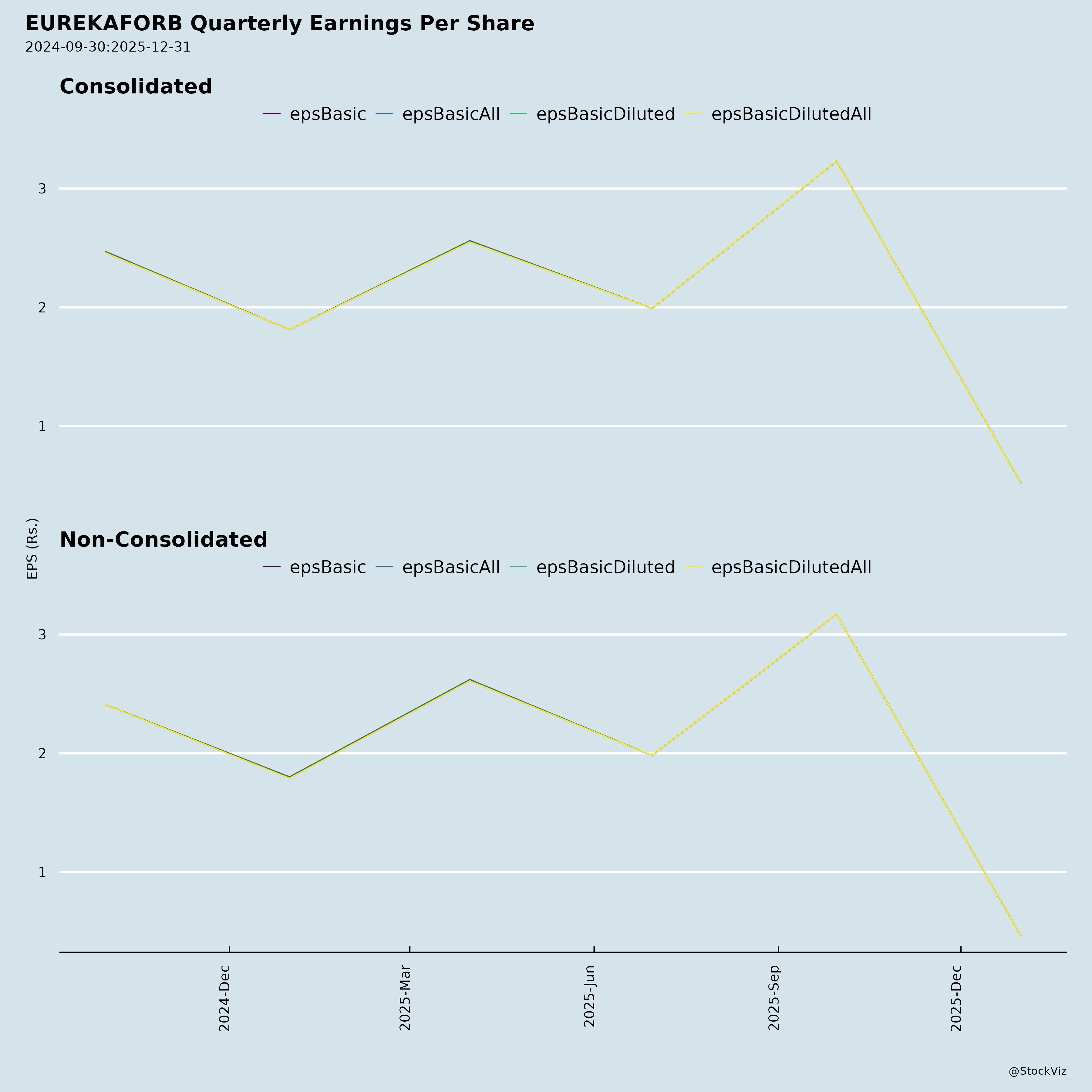

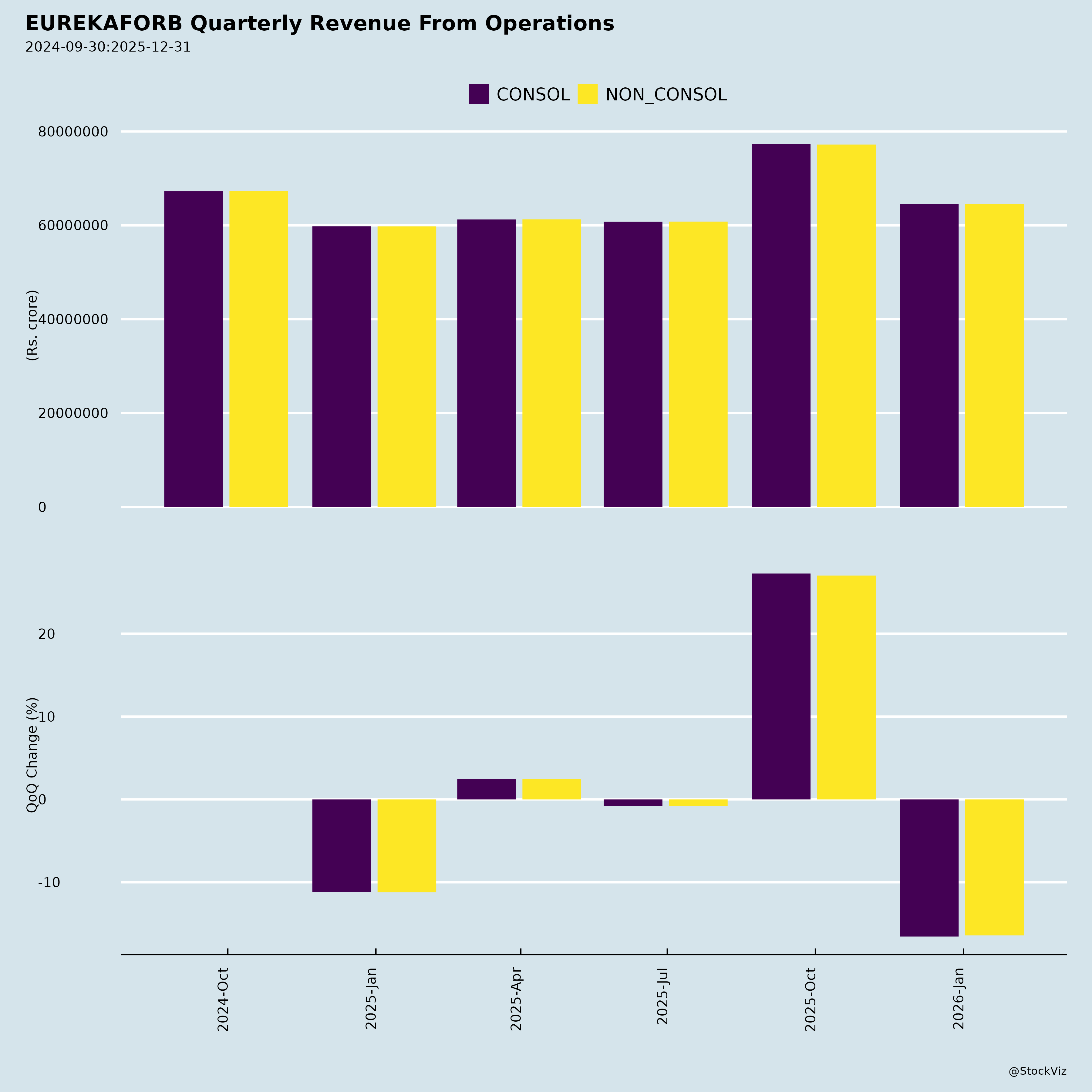

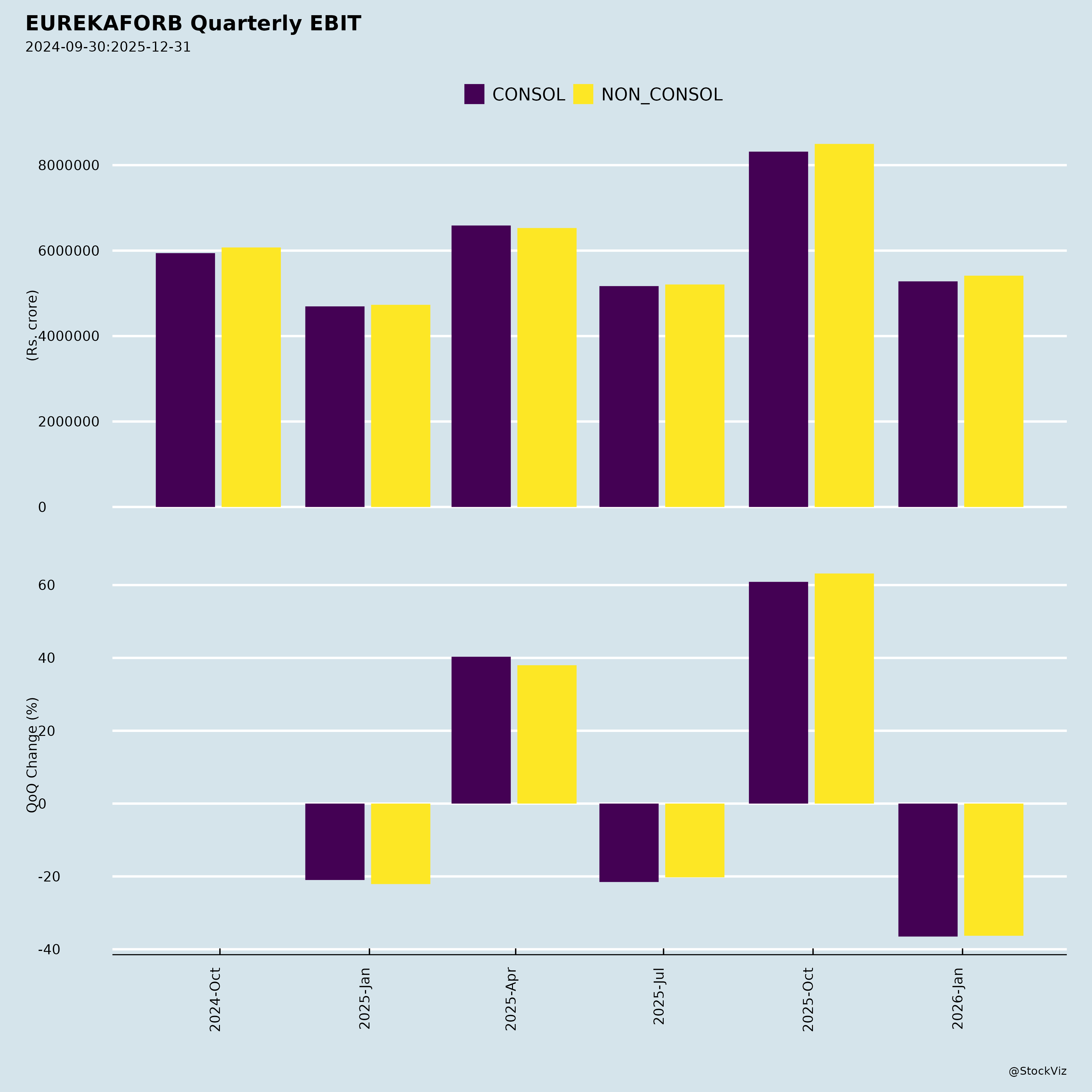

Fundamentals

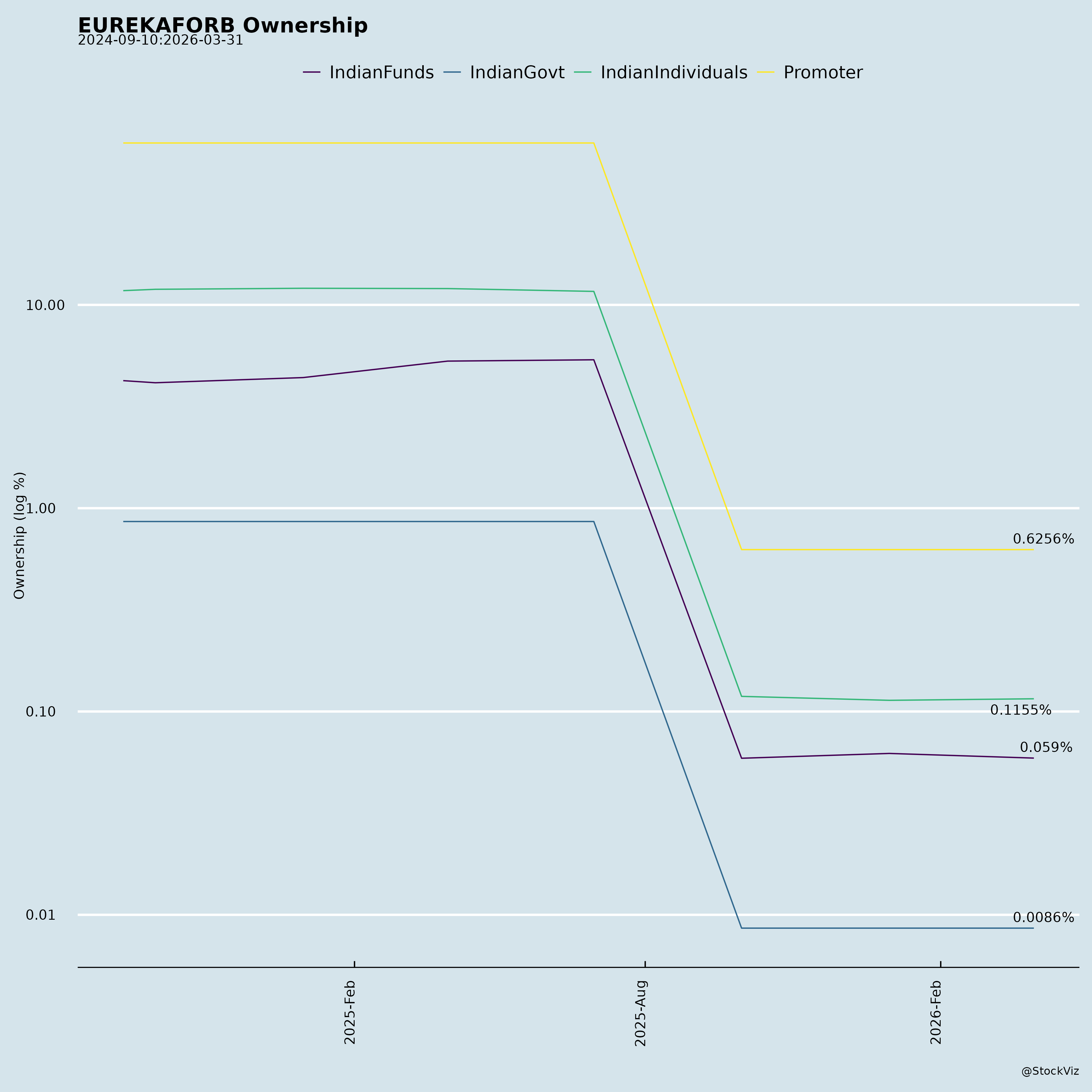

Ownership

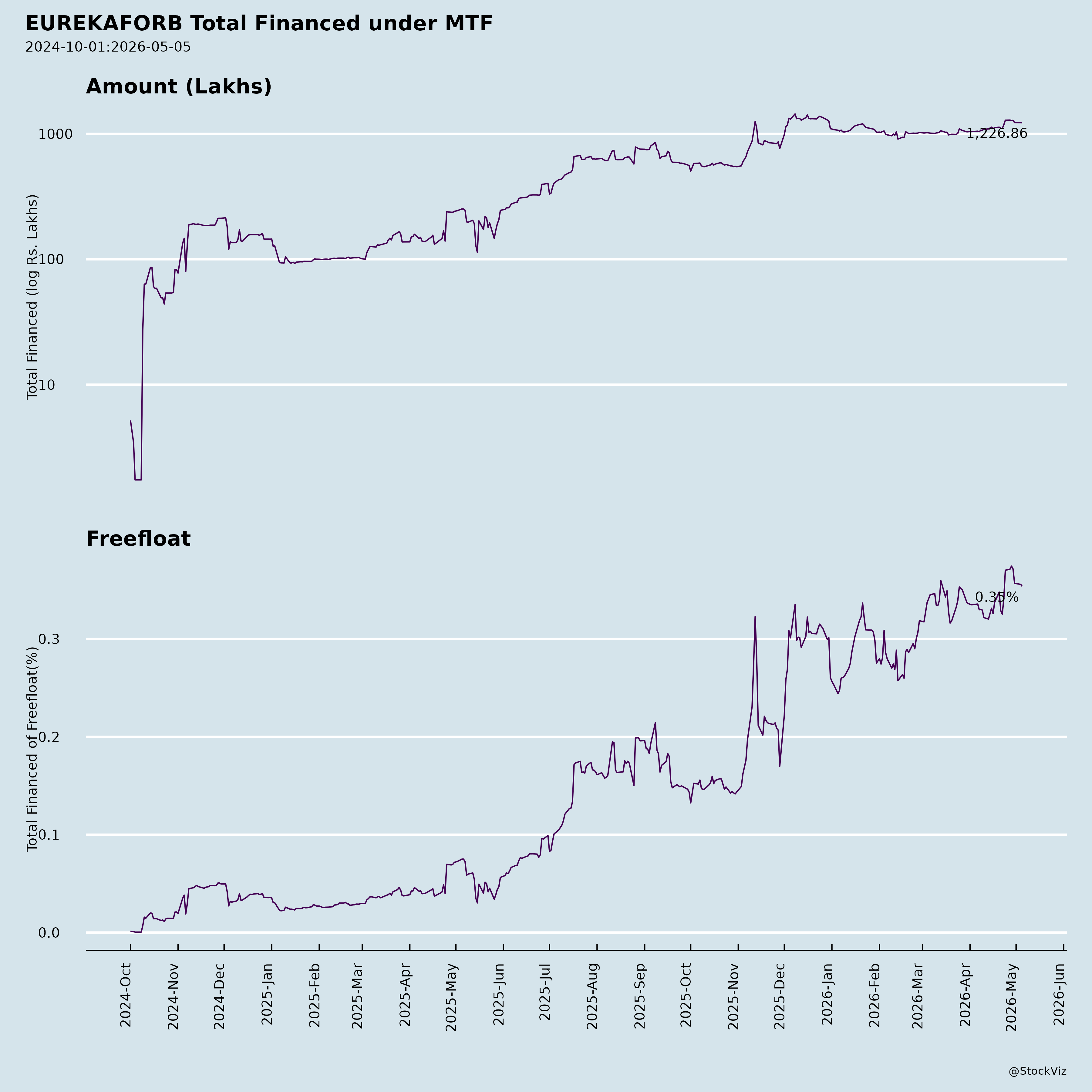

Margined

AI Summary

asof: 2025-12-04

Eureka Forbes Limited: Headwinds, Tailwinds, Growth Prospects & Key Risks Summary

Headwinds

- Competitive Intensity

- New entrants (e.g., Flipkart, Amazon) and private labels are intensifying pressure on product categories like water purifiers and vacuum cleaners.

- Existing players like Havells and Bajaj offer differentiated products, forcing price competition.

- New entrants (e.g., Flipkart, Amazon) and private labels are intensifying pressure on product categories like water purifiers and vacuum cleaners.

- Operational Scaling Challenges

- Scaling service operations (AMC bookings and filters) requires robust digital infrastructure and talent, which is still evolving.

- Legacy system integrations for service automation pose integration risks.

- Scaling service operations (AMC bookings and filters) requires robust digital infrastructure and talent, which is still evolving.

- Macroeconomic Sensitivity

- Demand for durables (e.g., water purifiers, vacuum cleaners) is discretionary, making it vulnerable to economic slowdowns.

- Inflationary pressures could erode margins if input costs rise faster than pricing power.

- Demand for durables (e.g., water purifiers, vacuum cleaners) is discretionary, making it vulnerable to economic slowdowns.

- Regulatory & Compliance Risks

- GST 2.0 and evolving data privacy norms may impact pricing and service delivery.

- Antitrust scrutiny on pricing practices in the service sector.

- GST 2.0 and evolving data privacy norms may impact pricing and service delivery.

Tailwinds

- Underpenetrated Markets

- Water purifier penetration at 6%, vacuum cleaners at 2%, and air purifiers still nascent.

- $10–12K Cr TAM potential in H2 FY30 across products/services.

- Water purifier penetration at 6%, vacuum cleaners at 2%, and air purifiers still nascent.

- Service Revenue Explosion

- AMC bookings grew 10%+ YoY; filters market untapped (>$1K Cr TAM).

- AI-powered digital service platform (D2C, remote troubleshooting) reduces costs and improves retention.

- AMC bookings grew 10%+ YoY; filters market untapped (>$1K Cr TAM).

- Premiumization & Ecosystem Growth

- Robotics portfolio (50%+ revenue from premium SKUs) drives higher margins.

- Partnerships with influencers, e-commerce platforms, and retail chains expand reach.

- Robotics portfolio (50%+ revenue from premium SKUs) drives higher margins.

- Digital Transformation Momentum

- 2.4 Mn+ active app downloads; AI hyper-personalization boosts conversion rates.

- Service GTM tools (e.g., video troubleshooting) reduce technician dependency.

- 2.4 Mn+ active app downloads; AI hyper-personalization boosts conversion rates.

Growth Prospects

- Product Category Expansion

- Water Purifiers: New 2-year filter kits and universal filters will drive volume growth ($10–12K Cr TAM by FY30).

- Robotics: Fully automated cleaning stations and AI-enabled vacuums targeting high-income segments.

- Softener & Air: Post-COVID demand recovery expected.

- Water Purifiers: New 2-year filter kits and universal filters will drive volume growth ($10–12K Cr TAM by FY30).

- Service Monetization

- AMC Penetration: Target 40%+ AMC penetration via AI-driven retention campaigns.

- Filters Upsell: Convert 20% of non-AMC customers to filter subscribers.

- CaaS (Customer as a Service): Expand B2B service contracts with real estate players.

- AMC Penetration: Target 40%+ AMC penetration via AI-driven retention campaigns.

- Digital & Ecosystem Play

- D2C Platform: Reduce retail dependency; capture 40%+ of service revenue by FY26.

- B2B Partnerships: Supply smart water/air systems to housing societies and commercial clients.

- D2C Platform: Reduce retail dependency; capture 40%+ of service revenue by FY26.

Key Risks

- Execution Risk in Service Digitalization

- Poor adoption of AI platforms could delay ROI targets (e.g., service costs vs. benefits).

- Margin Dilution

- Aggressive pricing to penetrate rural markets or compete with private labels may pressure gross margins.

- Talent Retention

- High turnover in technical roles (robotics, R&D) could stall innovation momentum.

- Regulatory Volatility

- Changes in GST, data privacy (e.g., AI-driven customer data usage), and product certifications.

- Economic Downturn Impact

- A slowdown could reduce discretionary spending on premium durables, affecting top-line growth.

Conclusion

Eureka Forbes has strong fundamentals, with multiple tailwinds (underpenetrated markets, digital scalability, and service upside) driving a 2x revenue/3x EBITDA growth target by FY30. The transformative strategy in service automation and category expansion positions it for long-term dominance. However, operational execution risk, competitive headwinds, and macro exposure remain critical concerns. Success hinges on rapidly scaling its digital service platform while maintaining premium pricing discipline.

Recommendation: Neutral to Buy with a 12–18 month horizon, betting on sustained product growth and service monetization, while monitoring competitive responses and macro trends.

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.