Household Appliances

Industry Metrics

May 8, 2026

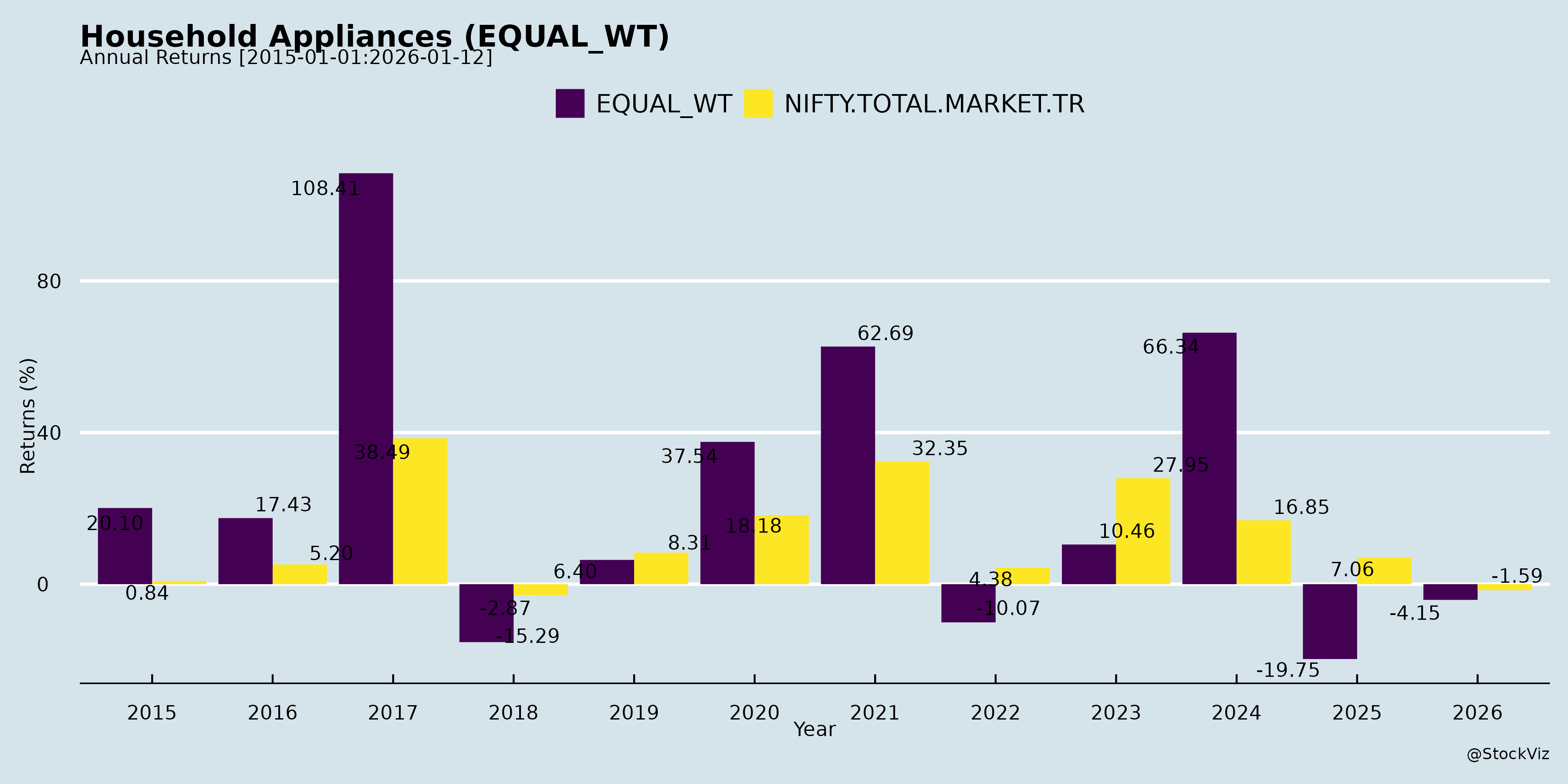

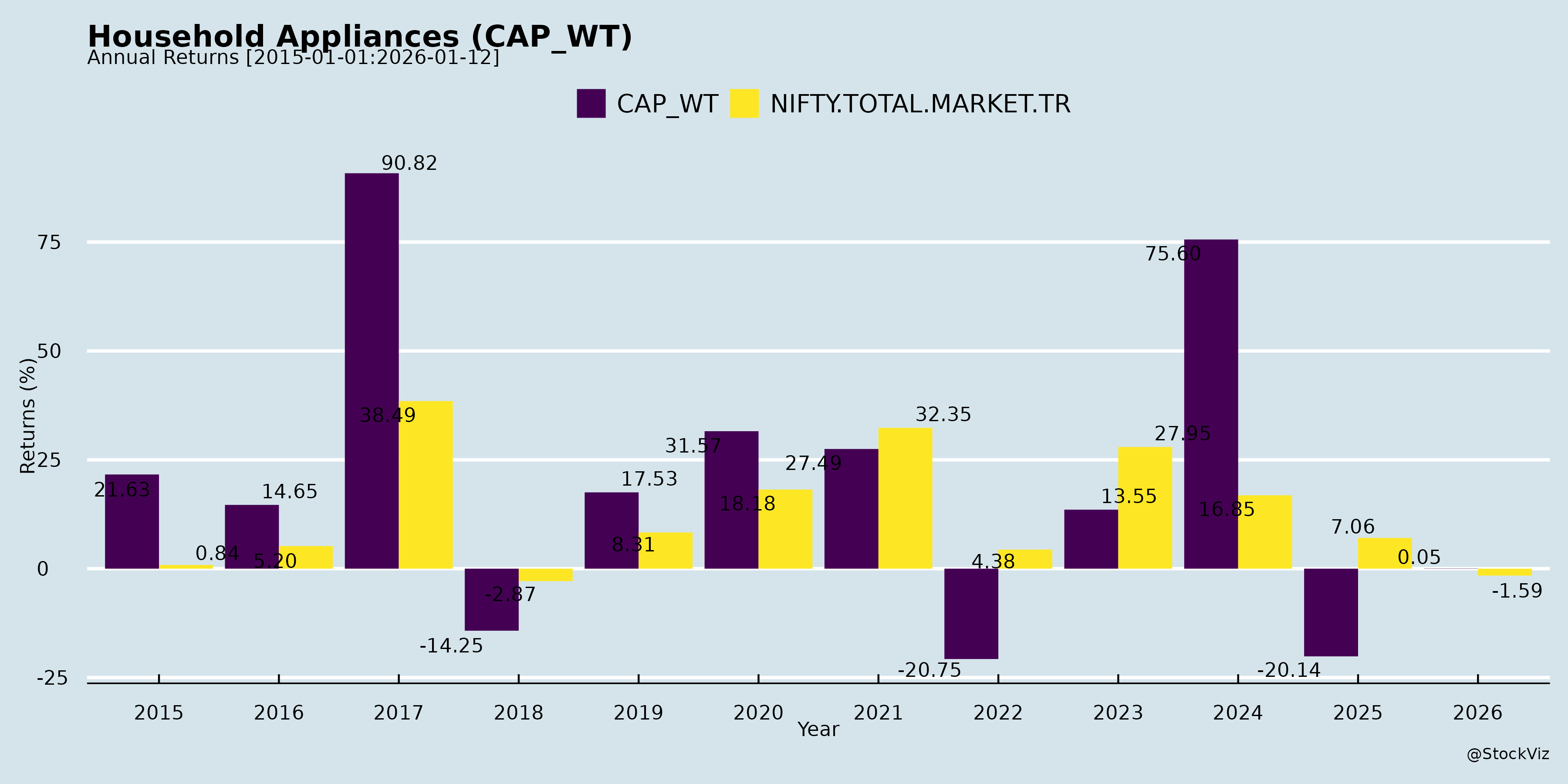

Annual Returns

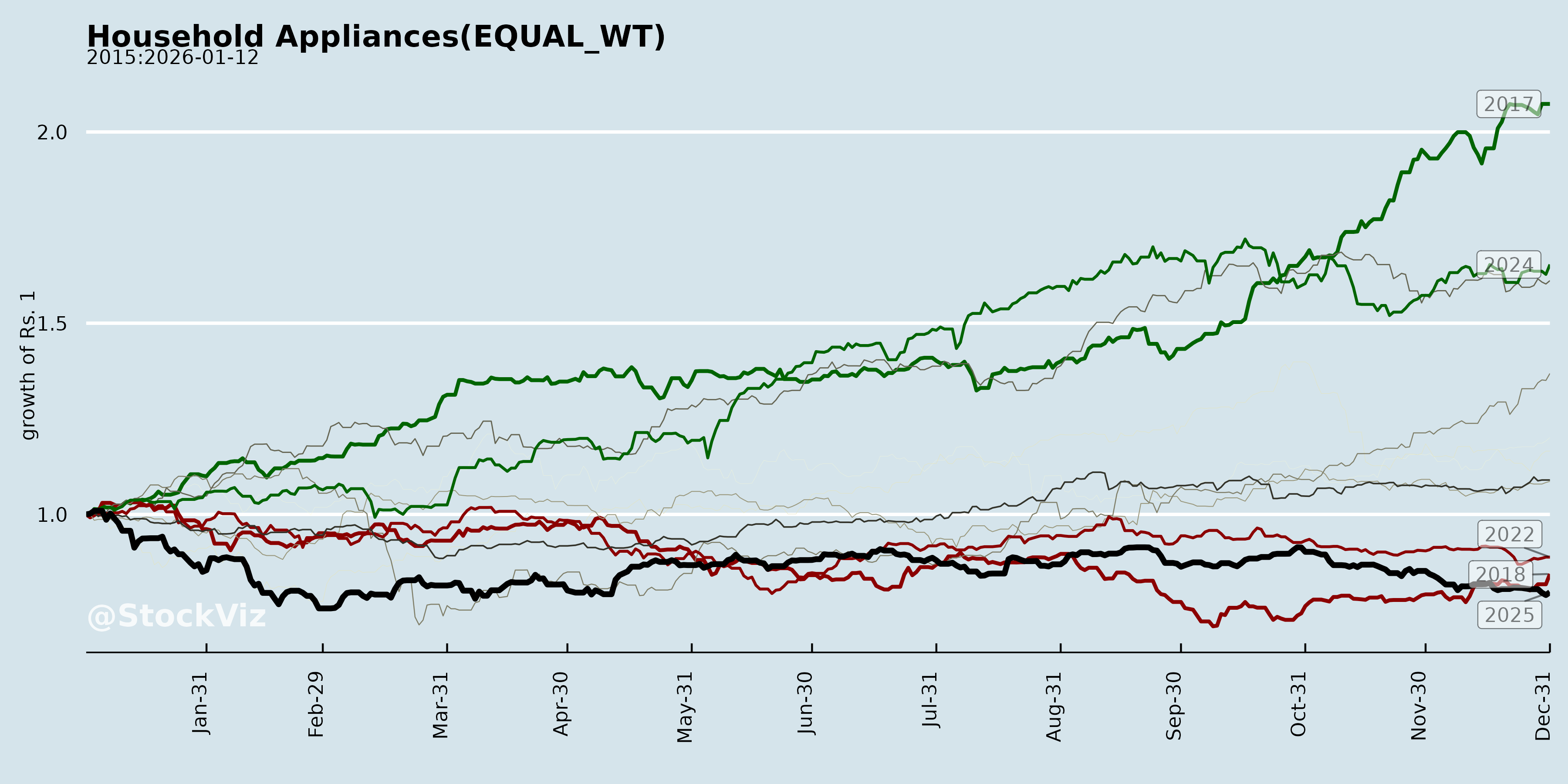

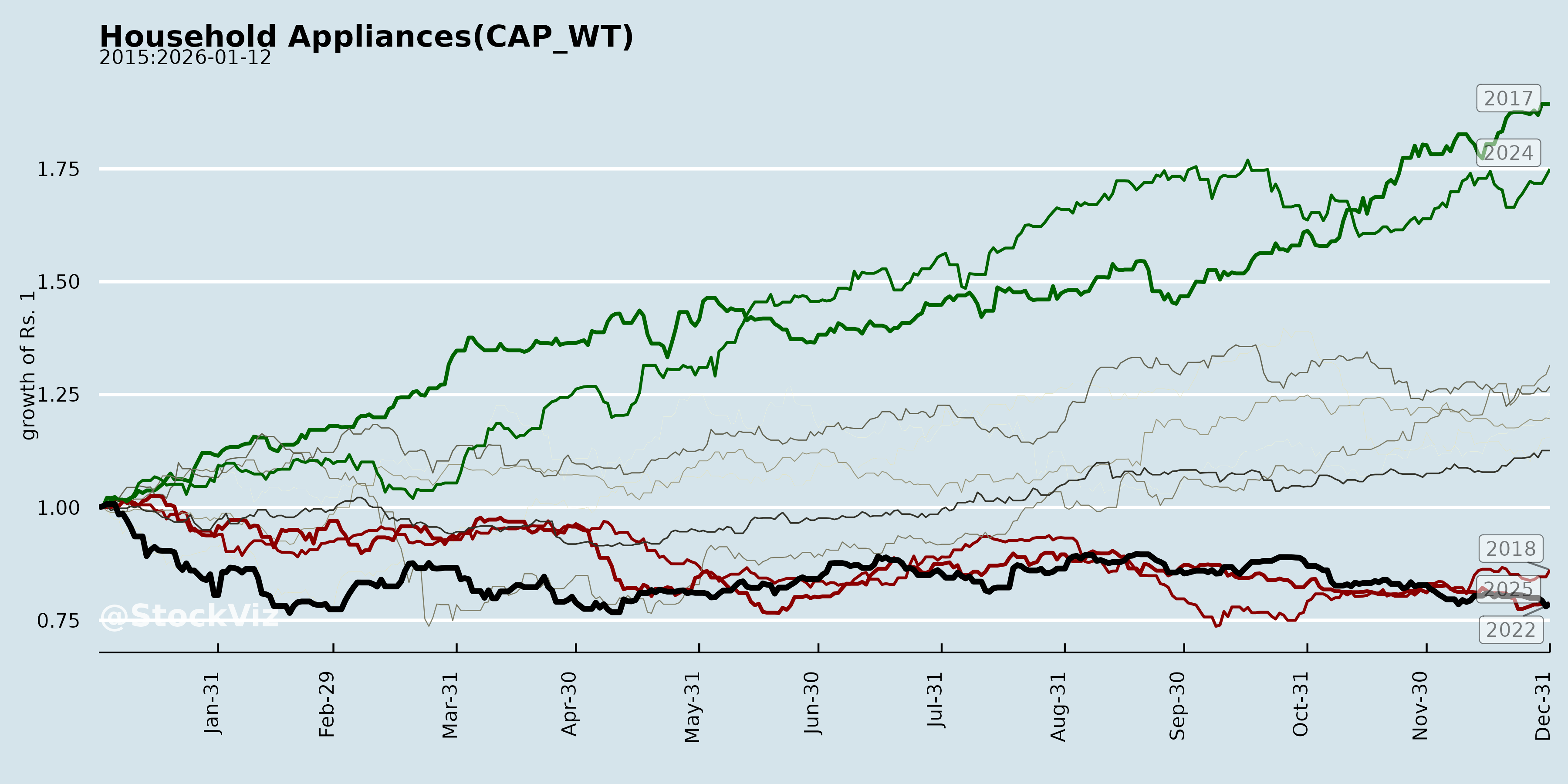

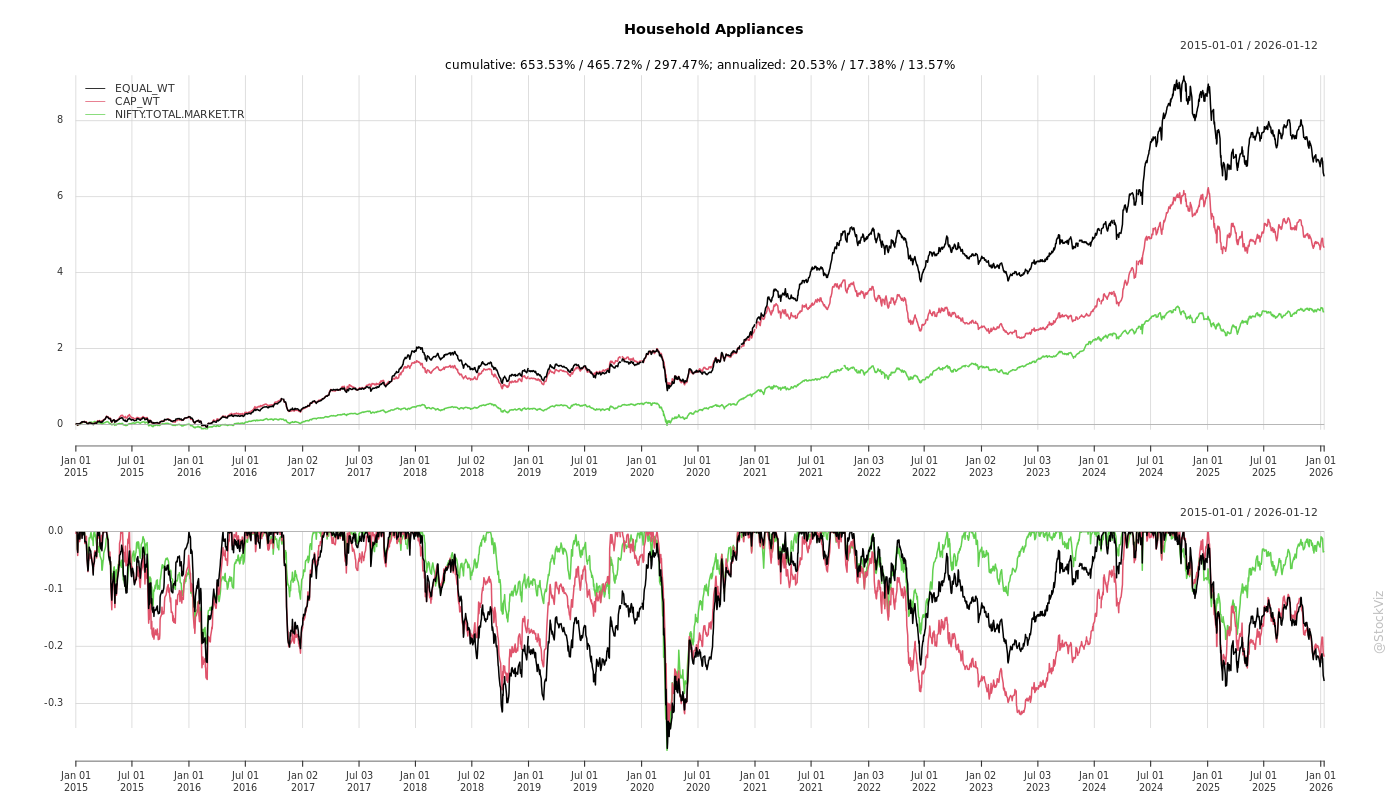

Cumulative Returns and Drawdowns

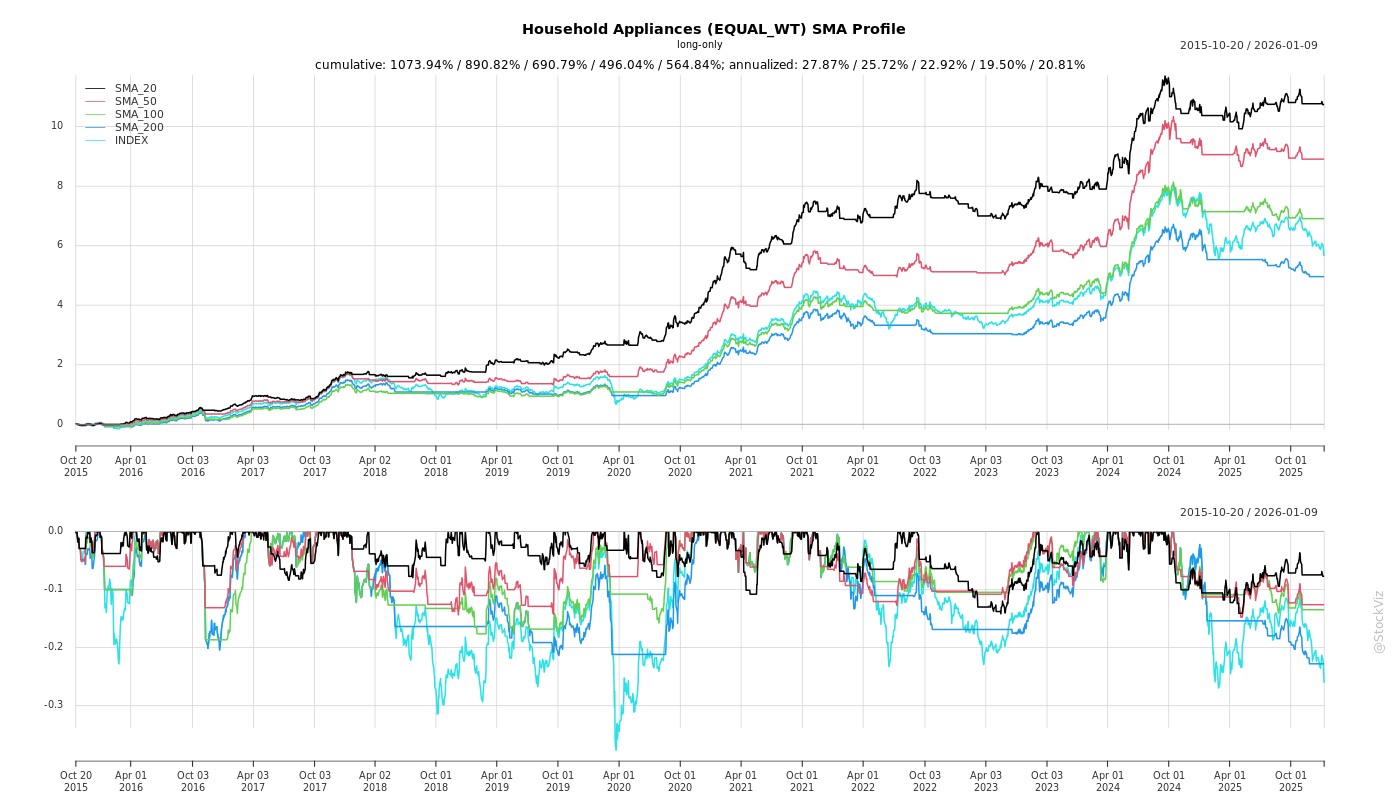

SMA Scenarios

Current Distance from SMA

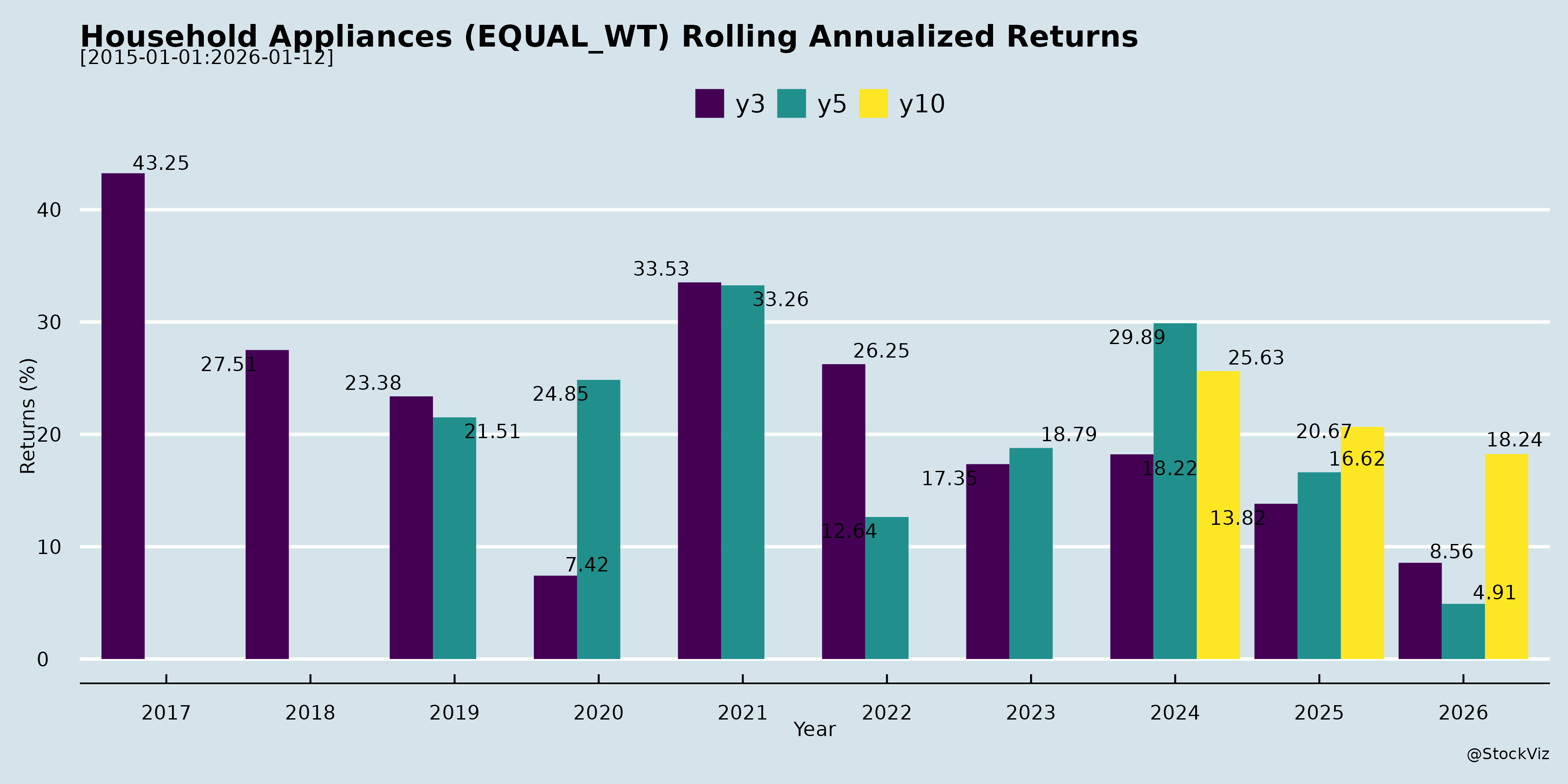

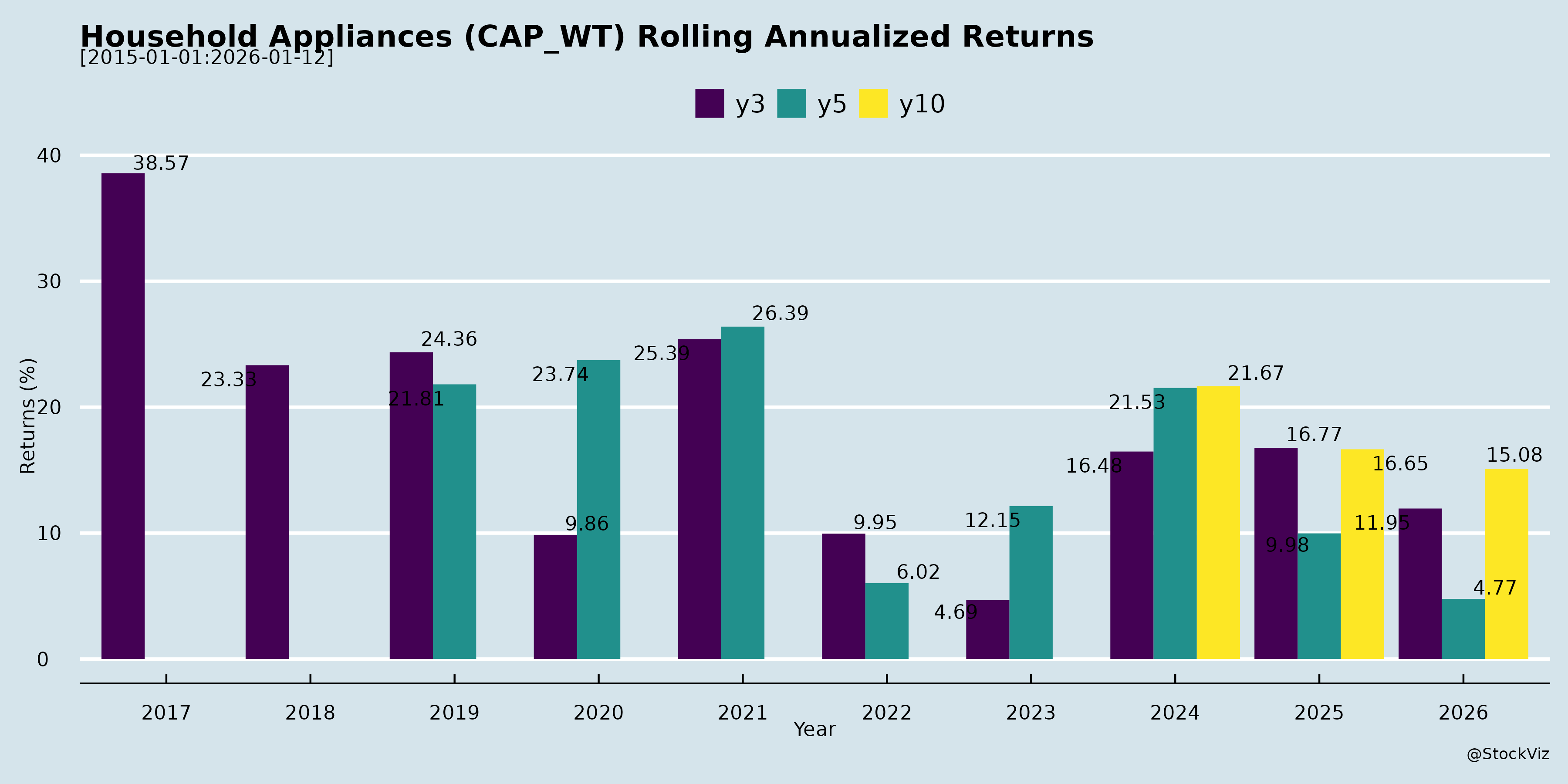

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-15

The challenges in the consumer durables and appliances industry have evolved to encompass complex macroeconomic, regulatory, and supply chain hurdles.

Historically, companies have grappled with shifting and erratic weather patterns, such as delayed monsoons, lean summers, and shorter second summers, which drastically impact the demand for seasonal categories like air conditioners, air coolers, and fans [1-5]. This unpredictable demand, coupled with post-festive slowdowns, has frequently led to elevated channel and trade inventories [2, 6, 7]. To resolve this, companies are being forced to structurally transition their business models from a volume-led primary push to a demand-led secondary off-take approach, deliberately normalizing channel health despite the short-term hit to primary sales and margins [8-11].

Simultaneously, competitive intensity has skyrocketed. An influx of new brands has triggered aggressive discounting and unseen levels of price reductions, commoditizing entry-level segments like direct-cool refrigerators and semi-automatic washing machines [12-16]. Additionally, the industry has faced a prolonged replacement cycle for highly penetrated products like refrigerators, stalling immediate demand generation [17, 18].

On the operational and regulatory fronts, the landscape has grown increasingly stringent. The continuous transition to revised, higher-efficiency Bureau of Energy Efficiency (BEE) star-rating norms has necessitated massive product re-engineering and caused significant cost escalations across the industry [19-24]. Moreover, businesses have faced extreme volatility in commodity prices—specifically a sudden and massive spike in copper and aluminum costs—along with the negative impacts of foreign exchange depreciation on imported materials [25-27].

Conversely, the opportunities in the sector have evolved into long-term structural tailwinds driven by changing consumer demographics, technological advancements, and new revenue streams.

Favorable Demographics and Underpenetrated Markets: The industry is benefiting from deep macroeconomic shifts, including rapid urbanization, a fast-growing middle class, rising female workforce participation, and near-universal electrification [28, 29]. Because core appliances like room air conditioners, refrigerators, and water purifiers still have relatively low household penetration in India, there is a massive, multi-decade runway for growth driven by first-time buyers, particularly in Tier 3, 4, and 5 markets [18, 30-32].

Premiumization and De-commoditization: To escape margin-eroding price wars, companies are actively moving consumers up the value chain [33-35]. A major opportunity lies in de-commoditizing products through aesthetic and technological differentiation, such as introducing premium glass-door refrigerators, high-capacity front-load washing machines, built-in kitchen appliances, and heavy-duty, smart Wi-Fi-enabled air conditioners [16, 35-40].

Category Expansion into Health, Hygiene, and Efficiency: The market has evolved to prioritize wellness and energy savings. There is exponential, break-out growth in emerging categories like robotic vacuum cleaners, water softeners, and air purifiers—the latter driven by acute consumer awareness of worsening air quality and water contamination in metropolitan areas [41-44]. Furthermore, to combat the high cost of copper and meet energy standards, there is a lucrative structural shift toward Brushless DC (BLDC) fans, which use less copper and appeal to energy-conscious consumers [45-47]. Brands are also aggressively expanding their total addressable market by venturing into adjacent segments like residential wires, switchgears, and solar rooftops [48, 49].

Local Manufacturing and the B2B/ODM Boom: Supported by the “Make in India” initiative, there is a surging opportunity in backward integration and domestic manufacturing [50, 51]. Original Design Manufacturers (ODMs) are successfully setting up highly scalable, localized manufacturing ecosystems to produce air conditioners, washing machines, and LED televisions for multinational brands [50, 52]. Companies are also investing in captive component manufacturing—such as domestic AC motors—to break reliance on imports and compete directly with Chinese pricing [53-55].

Monetizing the Aftermarket and Services: Finally, companies are transforming their after-sales service from a basic support function into a highly profitable, recurring revenue engine [56]. By capitalizing on their large installed customer bases, brands are driving double-digit growth in Annual Maintenance Contract (AMC) bookings and launching proprietary, simplified consumable assortments—like long-life nanopore water filters—to appropriate a larger share of the lucrative aftermarket [56-59].

What are the headwinds affecting this industry?

asof: 2026-04-15

Weak Consumer Demand and Unfavorable Weather Patterns The industry has been grappling with a sluggish and weak market environment, particularly impacting core categories like refrigerators, air conditioners, air coolers, and fans [1-4]. Demand was noticeably muted due to a post-festive slowdown that did not align with earlier growth projections [5-8]. Furthermore, unseasonal rains, delayed or weak summers, and early monsoons significantly dampened the sales of seasonal cooling products [9-12]. In some instances, the industry anticipated a “second summer” to help liquidate stocks, but this supplementary liquidation window failed to materialize, further exacerbating the demand slump [4, 13].

Elevated Channel Inventory and Deleveraging As a direct consequence of the sudden demand slowdown and weak summer seasons, the industry faced highly elevated trade inventory levels [5, 12, 14, 15]. To restore channel health, companies have been forced to initiate deliberate inventory normalization strategies, shifting from a volume-led primary billing push to a secondary off-take execution model [13, 15, 16]. While prudent for long-term health, this tactical flushing out of stock has resulted in sharp short-term declines in primary sales and negative EBIT margins due to operating deleverage [13, 17]. Additionally, companies have had to absorb margin pressures by running aggressive promotional campaigns and discounts to move this excess stock off channel partners’ shelves [13, 18].

Severe Commodity Inflation and FOREX Pressures The industry is currently navigating a highly volatile and inflationary raw material environment [19, 20]. Manufacturers are facing steep increases in the costs of key commodities such as copper, aluminum, and galvanized plain (GP) steel [21-24]. Copper, in particular, has seen unprecedented price spikes, surging by nearly 40% in a single year, severely impacting categories with high copper content like induction motor fans and wires [25-27].

Coupled with raw material inflation, foreign exchange (FOREX) headwinds have heavily impacted cost structures [19, 23, 28]. The depreciation of the Indian Rupee against the US Dollar—with the dollar reaching around INR 90 (an approximate 6% depreciation from the previous year)—has significantly driven up the cost of imported components, effectively erasing the financial benefits gained from internal cost-innovation programs [23, 24].

Intense Competition and Threat of Commoditization The consumer durables space is experiencing unprecedented levels of competition, characterized by unseen levels of price reductions and heavy discounting [29-33]. The influx of numerous new brands into the market over the past few years has intensified the fight for market share, with many new entrants utilizing aggressive pricing as their primary penetration tool [31, 34-36]. This extreme competitive intensity has led to the commoditization of staple categories like Direct Cool (DC) refrigerators and semi-automatic washing machines, where products are frequently sold based solely on price and capacity, thereby limiting the ability of established players to achieve margin expansion [37-40].

Regulatory Compliance Costs and Energy Rating Transitions Regulatory changes represent a massive structural headwind for the engineering and durables sectors [41, 42]. A major challenge is the transition to the new Bureau of Energy Efficiency (BEE) energy star rating norms that took effect in January 2026 [43-46]. Entire portfolios of high-volume products, particularly refrigerators, air conditioners, and ceiling fans, have required costly re-engineering to comply with these stricter energy changes [21, 44, 47-49]. These new BEE ratings, combined with commodity impacts, have resulted in estimated production cost escalations of 8% to 10% [50, 51]. Due to the heavy market competition, companies are finding it difficult to fully pass these regulatory cost increases onto consumers without sacrificing volume, leading to compressed profitability [47, 52-54]. Furthermore, companies had to absorb one-time exceptional financial hits due to provisions related to new government Wage and Labour Codes [55-58].

Elongated Replacement Cycles and Deferred Purchases In highly penetrated categories, particularly refrigerators, the replacement cycle is actively lengthening [59-62]. Unlike air conditioners, which frequently undergo energy-rating upgrades that prompt consumers to buy newer models, refrigerators currently lack a compelling trigger to drive frequent consumer replacement [60, 62]. Additionally, regulatory adjustments such as the reduction in GST rates (e.g., from 28% to 18%) have previously caused short-term demand deferments as consumers and channel partners paused purchases to wait for revised pricing structures to settle [12, 63, 64].

What are the key things to understand about this industry?

asof: 2026-04-15

The consumer durables and home appliances industry in India is characterized by vast under-penetration, structural macroeconomic tailwinds, and intense operational complexities. Here are the key things to understand about the dynamics of this sector:

Massive Headroom for Growth and Low Penetration The industry is currently riding a wave of structural growth supported by rapid urbanization, rising middle-class disposable incomes, growing female workforce participation, and widespread electrification [1, 2]. Despite these tailwinds, penetration levels remain exceptionally low. For instance, refrigerator penetration in India is still under 36-37%, with industry expectations to drive this toward 65-70% over the next two decades [3]. Similarly, the room air conditioner (RAC) category is projected to more than double, expanding from approximately 14 million units to 30 million units by FY30 [1]. While urban centers drive replacement demand, Tier 3, 4, and 5 markets are emerging as the crucial engines for new growth [1].

Extreme Sensitivity to Seasonality and Weather Business performance is heavily dictated by seasonal weather patterns. A “lean summer,” a delayed monsoon, or a shorter-than-expected second summer immediately dampens retail offtake for cooling products like air conditioners, refrigerators, and air coolers [4-8]. Conversely, harsh heat waves drive robust volume growth [9]. Because seasonal volatility can leave companies with massive unsold inventories, brands are actively diversifying into “Round-The-Year” (RTY) product portfolios—such as water heaters, small kitchen appliances, and residential wires—to create more stable, multi-engine revenue streams [10-14].

Intense Competitive Rivalry and Pricing Wars The entry of numerous new brands over the last several years has created an incredibly fragmented and aggressive competitive landscape [15, 16]. Categories like direct-cool refrigerators and semi-automatic washing machines are highly prone to commoditization, where players use extreme discounting or “capacity games” (e.g., selling 9kg machines at the price of 8kg models) to grab market share [17, 18]. This leads to unseen levels of price reductions and heavy promotional expenditures that continually pressure corporate profit margins [15, 19-21].

The Strategic Shift Towards Premiumization and De-commoditization To survive the price wars, companies are fiercely focusing on decommoditizing their offerings through premiumization, aesthetics, and technology [22-26]. Brands are launching highly differentiated products, such as customized glass-door refrigerators that serve as living room showpieces, auto-defrost technologies that solve specific consumer pain points, front-load washing machines, and IoT-enabled smart ACs featuring AI-driven cooling and anti-virus filtration [27-31]. By offering unique, premium features, companies aim to elevate gross margins and protect brand value rather than just chasing sheer volume. [24, 32-35]

Heavy Impact of Regulatory Changes (BEE Norms) Because this is an engineering-heavy industry, regulatory changes—specifically the Bureau of Energy Efficiency (BEE) star rating upgrades—are massive systemic events [36-38]. Transitioning to new energy norms requires extensive re-engineering of products and inevitably drives up manufacturing costs. For example, a recent BEE transition increased the Bill of Materials (BOM) cost by 3% to 5% for 3-star ACs and 5% to 8% for 5-star ACs [39, 40]. Companies must dynamically manage pricing to pass these regulatory costs onto consumers without destroying demand. [37, 41, 42]

Commodity Volatility and Freight Costs Profitability is highly vulnerable to fluctuations in the prices of core commodities like copper, aluminum, and steel [43, 44]. Unprecedented spikes in copper prices, for instance, force immediate price hikes in wire and copper-heavy fan segments, which can temporarily suppress volume growth [45-48]. Furthermore, logistics and freight costs play a major role and vary wildly by product mix; bulky items like refrigerators incur significantly higher freight costs as a percentage of revenue compared to higher-value, space-efficient items like air conditioners [49-51].

Supply Chain Localization and the OEM/ODM Ecosystem The industry is undergoing a massive shift toward domestic manufacturing, supported by the “Make in India” initiative and changing global supply chains [52-54]. Original Equipment/Design Manufacturers (OEMs/ODMs) are scaling up aggressively, creating massive industrial parks to supply global and domestic brands with finished goods and critical components like PCBs, motors, and plastic molded parts [52, 55-57]. Backward integration is a key strategic lever being used to reduce dependence on imports, shorten lead times, and optimize supply chain resilience. [58-61]

Channel Inventory and Working Capital Management Channel health dictates primary sales performance. When consumer demand (secondary sales) slows down post-festivals or due to poor weather, inventory piles up at the distributor and retail levels [5, 8, 62, 63]. To correct this, companies frequently have to execute “channel normalization” strategies—deliberately halting primary billing to distributors while ramping up consumer promotions to flush out the excess stock. [21, 64-66]. Transitioning from a primary-push model to a secondary-offtake model is viewed as a necessary, albeit painful, structural change to ensure long-term ROI for channel partners and predictable revenue for manufacturers [67-69].

What are the tailwinds affecting this industry?

asof: 2026-04-15

Macroeconomic and Demographic Shifts The consumer durables and appliances industry is benefiting from several profound macroeconomic and demographic changes. The underlying resilience of the domestic economy, supported by steady GDP growth, provides a strong foundation for the sector [1, 2]. Growing middle-class incomes and rising affluence are structurally shifting consumption patterns, with the middle class projected to reach 1 billion people by 2047 [3-6].

Rapid urbanization is another massive tailwind; by 2036, it is expected that 40% of the Indian population will reside in towns and cities [6]. This urban expansion is directly driving demand for premium housing and the adoption of built-in kitchen solutions across Tier I and Tier II markets [7, 8]. Additionally, an increasing female labor force participation rate—which rose to 37% in 2023—coupled with unpredictable domestic help, has led to a greater reliance on convenience appliances and an increased frequency of home cleaning post-COVID [6].

Massive Headroom for Market Penetration Across several sub-categories, extremely low historical penetration rates offer a long runway for structural growth: * Refrigerators and Kitchen Appliances: Refrigerator penetration in the country remains low at less than 36-37%, with the industry aiming to push this toward 65-70% over the next two decades as the bottom half of the income pyramid begins to spend more [9, 10]. Premium built-in kitchen categories (like Elica) are even more underpenetrated at less than 5% [11, 12]. * Air Conditioners (RAC): The room air conditioner market has significant headroom, as an estimated 150 million households in India are expected to afford ACs in the future [13]. The category is projected to expand from roughly 14 million units to 30 million units by FY30 [5]. * Geographic Expansion: Unserved demand is being unlocked in rural and semi-urban markets, with Tier 3, 4, and 5 markets now emerging as critical growth engines that are outpacing Tier 1 and 2 cities [5, 14].

Heightened Health, Hygiene, and Environmental Awareness Changing environmental conditions are actively driving consumer demand for health-focused and climate-control appliances: * Water Quality: Growing awareness of the hazards of drinking untreated water—due to alarmingly poor groundwater quality and the risk of contamination in transit—is creating sustained tailwinds for point-of-use water purifiers [15-19]. This is synergizing perfectly with the expansion of piped water access, which reached 77.2% of households in 2024 [6]. * Air Quality: Worsening air pollution, which is now visibly experienced by residents in most metros and large towns, is causing a rise in respiratory health issues. This has drastically increased category awareness and generated breakout demand for air purifiers [20-25]. * Climate Intensity: Increasing climate intensity and shifting weather patterns are driving sustained demand for residential cooling solutions [5]. Interestingly, the traditional “seasonality” of air conditioner sales is reducing, leading to much more uniform demand across different quarters of the year [26, 27].

Regulatory and Infrastructure Drivers Government initiatives, tax reforms, and infrastructural development are significantly accelerating industry growth: * GST Reductions: The reduction of GST rates on appliances—such as the landmark cut from 28% to 18% on air conditioners—has been a structural game-changer. It has improved product affordability, unlocked pent-up consumer demand, and accelerated the democratization of energy-efficient cooling and appliances like cookers across urban and semi-urban India [28-33]. * Energy Efficiency (BEE) Transitions: The transition to upgraded Bureau of Energy Efficiency (BEE) star-rating norms is pushing the industry toward sustainable, higher-efficiency products and has spurred proactive consumer buying ahead of price-structure revisions [29, 30]. * Electrification: Deepening rural electrification, which has reached 96.7% of households [6], is directly expanding the total addressable market. Newly electrified villages and hinterlands in the North and East are experiencing high growth for appliances and voltage stabilizers [34, 35]. * Domestic Manufacturing Support: Government initiatives like the Atmanirbhar Bharat scheme and the impending imposition of mandatory BIS standards are poised to drastically boost domestic manufacturing and reduce reliance on imported components, such as Chinese AC motors [36-39].

Commercial and B2B Expansion In the commercial sector, the refrigeration business is experiencing strong structural momentum [40]. This is heavily driven by growth in out-of-home consumption, the rapid expansion of food retail, quick commerce, and modern trade formats, all of which require reliable, temperature-controlled storage and logistics for fresh and frozen foods [40, 41]. Furthermore, companies are successfully leveraging omnichannel acceleration, using digital platforms and alternative channels to expand their reach and generate consistent demand throughout the year [42].

What is the general outlook of this industry?

asof: 2026-04-15

The general outlook for the consumer durables, home appliances, and electricals industry is highly optimistic in the long term, characterized by strong structural growth, expanding addressable markets, and a shift towards premium and energy-efficient products. However, the sector is currently navigating several short-term macroeconomic and operational headwinds.

Long-Term Structural Growth and Massive Headroom for Penetration The industry is at a significant inflection point, driven by low current penetration levels and favorable demographic shifts. * Air Conditioners (ACs): India’s room AC industry is witnessing sustained structural growth and is projected to more than double from approximately 14 million units to 30 million units by FY30 [1]. It is estimated that nearly 150 million households in India will eventually be able to afford air conditioners, indicating massive headroom for future penetration [2]. * Refrigerators and Washing Machines: Refrigerator penetration in India is currently low at around 36% to 37%, with the industry aiming to push this towards 65% to 70% over the coming decades [3]. A significant pickup in durable replacements, particularly for refrigerators and washing machines, is anticipated over the next one to five years as the income levels of the bottom half of the population rise [3, 4].

Key Macroeconomic and Demographic Drivers The domestic economy’s resilience and steady GDP growth are providing a strong foundation for industry demand [5]. * Emerging Geographies: While urban centers drive replacement demand, Tier 3, 4, and 5 markets are emerging as the primary growth engines for first-time adoption, outpacing Tier 1 and 2 cities [1]. Companies are actively enhancing their penetration into these rural and semi-urban markets to capture unserved demand [6]. * Premiumization and Urbanization: Increasing urbanization and a rise in premium housing demand are boosting the adoption of built-in kitchen solutions and premium lifestyle appliances across Tier 1 and Tier 2 markets [7].

Health, Climate, and Environmental Catalysts Evolving environmental conditions and heightened health awareness are rapidly expanding specific product categories: * Air and Water Purifiers: The worsening air quality across the country, especially in major metros, is causing a rise in respiratory health issues, which in turn is driving sustained, geographically broad-based demand for air purifiers [8, 9]. Similarly, growing awareness regarding the hazards of untreated groundwater—which often contains pesticides, mercury, lead, and arsenic—is creating long-term tailwinds for point-of-use water purifiers [9]. * Climate Intensity: Increasing climate intensity and warmer, prolonged summers are directly contributing to higher demand for reliable residential cooling solutions [1].

Regulatory Shifts and Technological Upgrades The industry is currently transitioning to comply with new, higher-efficiency Bureau of Energy Efficiency (BEE) star-rating norms [10, 11]. This regulatory push is unlocking pent-up consumer demand for sustainable cooling solutions and energy-efficient products [12]. For example, in the ceiling fan category, there is a distinct structural shift away from traditional induction copper-motor fans toward energy-efficient BLDC (Brushless Direct Current) fans [13, 14].

Commercial and B2B Expansion Beyond residential appliances, the commercial refrigeration business is experiencing robust momentum [15]. This is being propelled by the rapid expansion of food retail, quick commerce, out-of-home consumption, and an increasing need for reliable temperature-controlled storage and logistics [2, 15].

Short-Term Headwinds and Challenges Despite the highly favorable long-term trajectory, the industry is currently managing several immediate friction points: * Elevated Trade Inventory and Soft Demand: Recently, the sector has faced a post-festive slowdown in consumer demand and muted retail offtake, leading to elevated inventory levels in trade channels (particularly in e-commerce and summer-related categories) [16-19]. * Unprecedented Commodity Inflation: Manufacturers are grappling with severe raw material inflation, notably an unprecedented spike in copper prices (which surged by nearly 40%), forcing companies to implement calibrated price hikes across their portfolios [20, 21]. * Intense Competition: The market remains hyper-competitive, with an influx of new brands over the last few years leading to aggressive discounting and unseen levels of price reductions as players fight for market share [22-24]. * Weather Volatility: Because a large portion of the industry relies on summer products (ACs, coolers, fans), unseasonal weather patterns—such as delayed, weak, or shorter summers—can easily disrupt sales and lead to inventory build-ups [25-27].

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.