TATACONSUM

Equity Metrics

May 8, 2026

TATA CONSUMER PRODUCTS LIMITED

Annual Returns

Cumulative Returns and Drawdowns

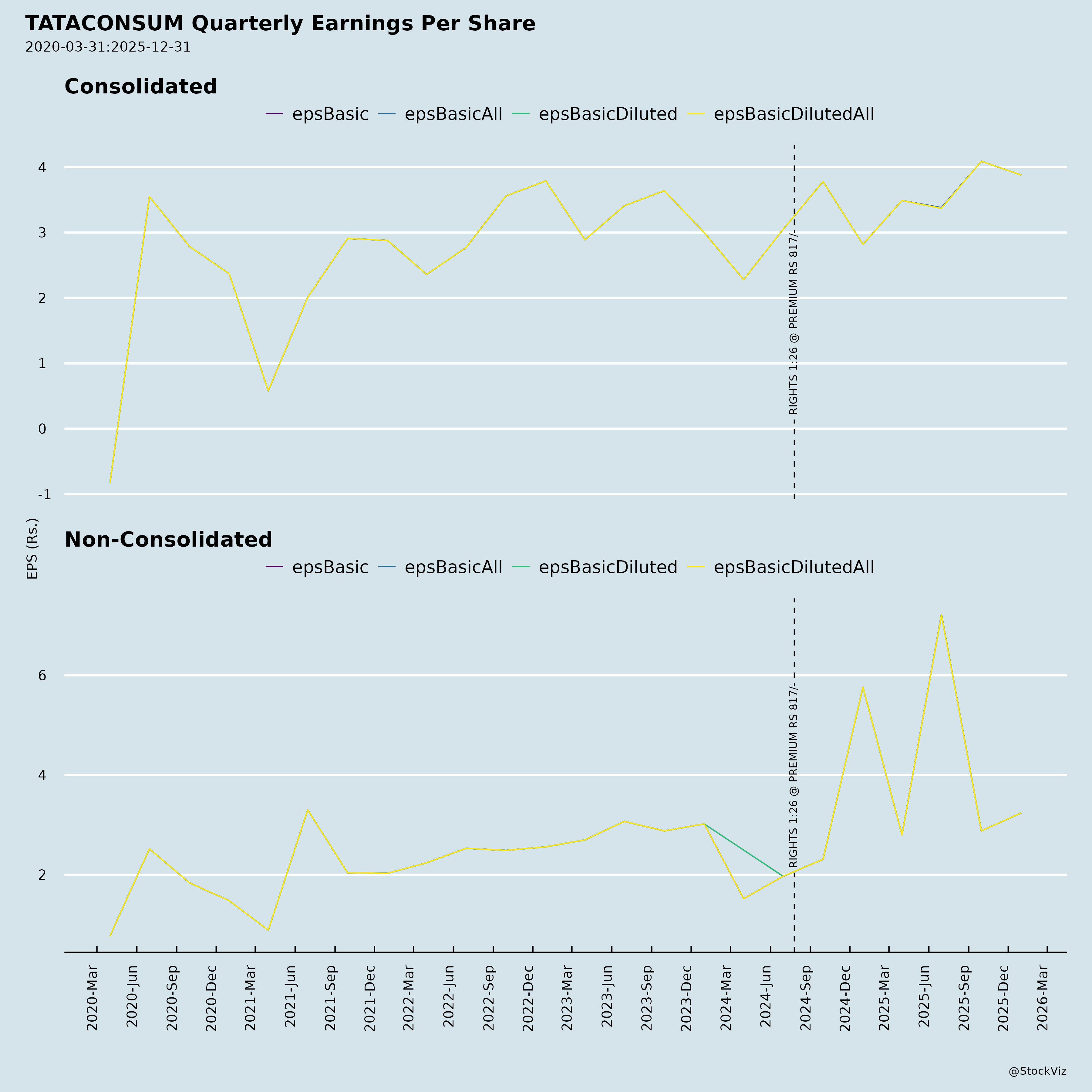

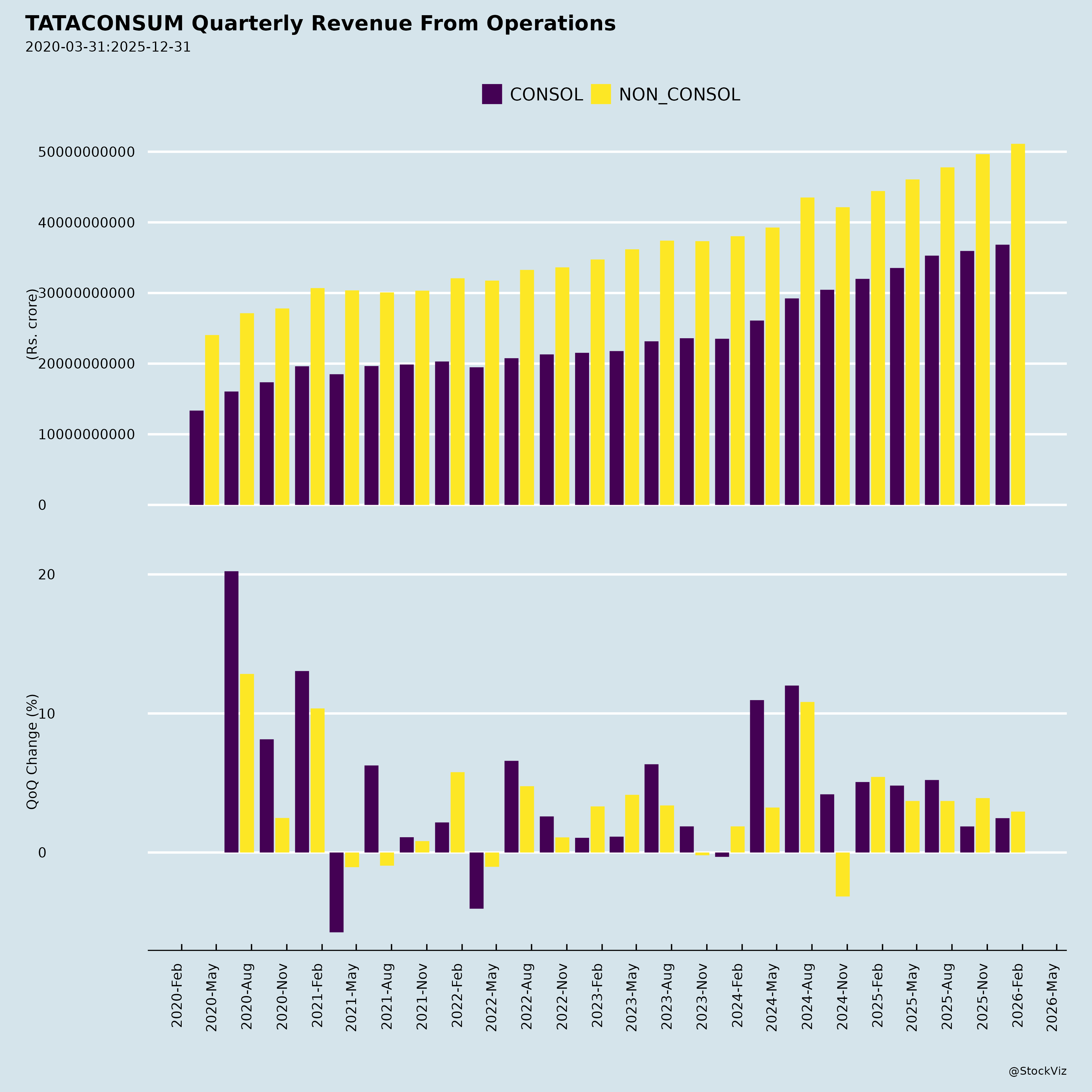

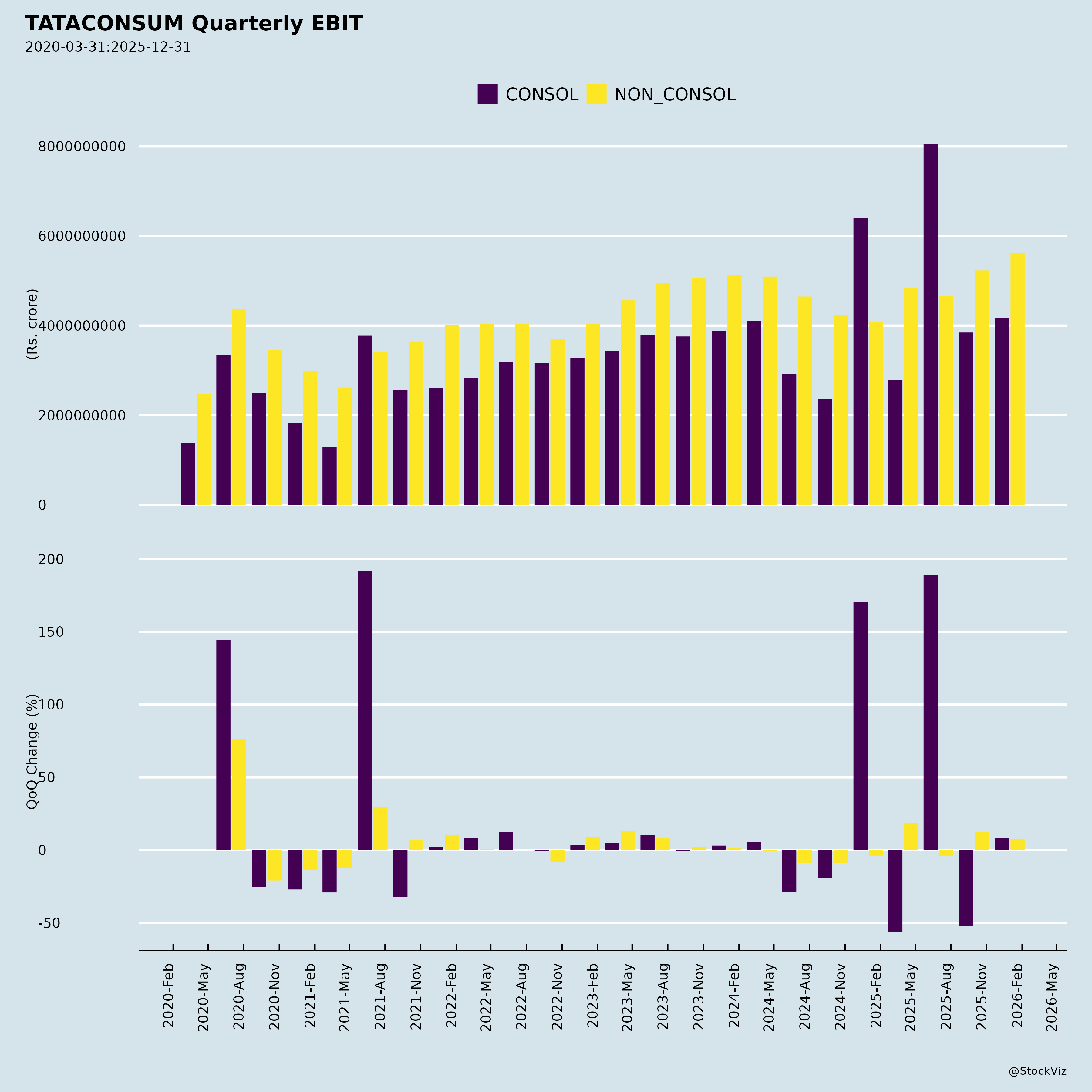

Fundamentals

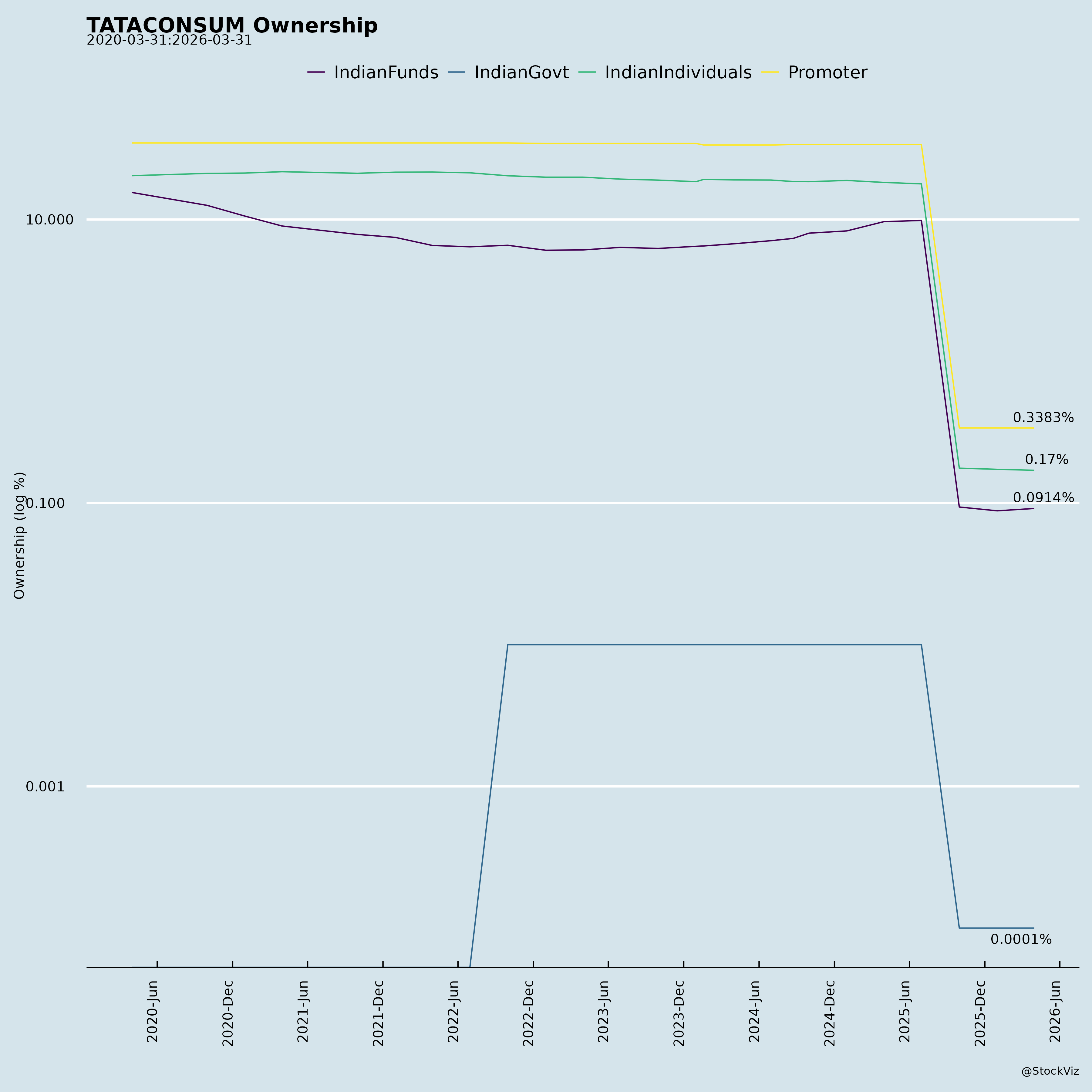

Ownership

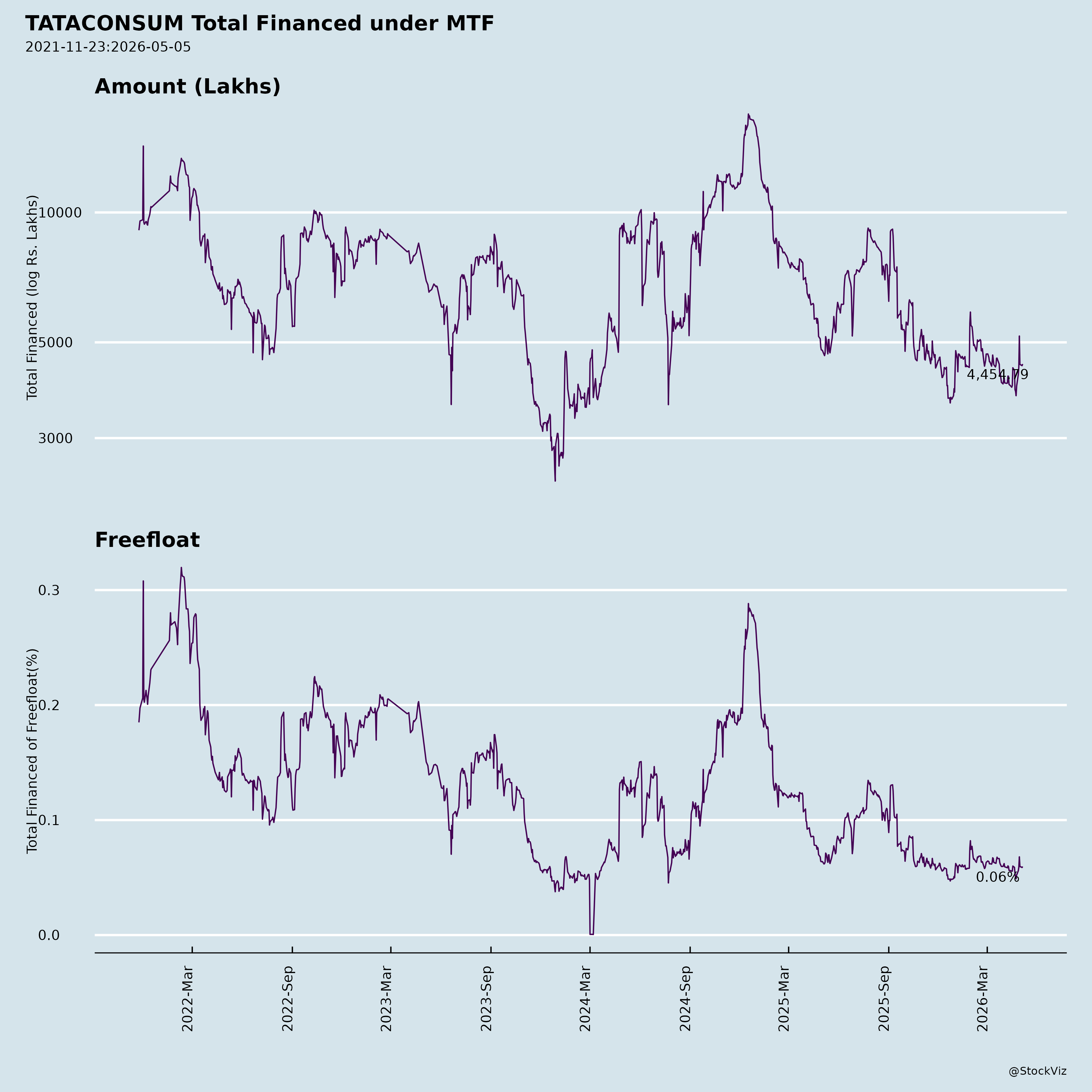

Margined

AI Summary

asof: 2025-12-08

Based on the provided financial, governance, and operational documents for Tata Consumer Products Limited (TCPL) — including unaudited standalone and consolidated financial results, auditor review reports, shareholder resolutions, and related disclosures up to September 30, 2025 — we can analyze the headwinds, tailwinds, growth prospects, and key risks for TATACONSUM (Scrip Code: 500800; TATACONSUM). This analysis will be grounded in recent performance, capital allocation trends, corporate actions, and strategic direction.

🔍 Company Overview

- Headquarters: Kolkata, India

- CIN: L15491WB1962PLC031425

- Sector: Consumer Goods – Branded Foods & Beverages (Tea, Coffee, Water, Snacks), Non-Branded Plantation & Extraction

- Subsidiaries/Associates Include: Tata Coffee, Organic India, Capital Foods Private Limited, Tata Starbucks, Teapigs, etc.

- Auditor: Deloitte Haskins & Sells LLP

📈 Fiscal Performance Snapshot (Quarter Ended September 30, 2025)

| Metric | Q2 FY26 (Sep ’25) | Q2 FY25 (Sep ’24) | YoY Growth |

|---|---|---|---|

| Revenue from Operations (Consolidated) | ₹4,965.9 Cr | ₹4,214.45 Cr | +18% |

| Net Profit (Group Consolidated) | ₹406.81 Cr | ₹367.21 Cr | +11% |

| EBIT (Profit before Exceptional Items & Tax) | ₹523.28 Cr | ₹424.24 Cr | +23% |

| Operating Margin (Consolidated) | 10.51% (vs 11.39% YoY) | — | Slight decline but stable core performance |

| Net Profit Margin (Consolidated) | 8.19% | 8.71% | Slight dip |

| Cash Flow from Operations (H1 FY26) | ₹203.41 Cr | ₹295.03 Cr | Down due to working capital adjustments |

📌 Note: Profit growth occurred despite adverse movements in commodity pricing and higher brand investments.

✅ TAILWINDS

1. Strong Revenue Growth Across Segments

- 18% overall revenue growth YoY (16% in constant currency).

- Driven by:

- +18% growth in India Branded Business

- +10% in International Branded Business

- +26% in Non-Branded Business (plantation/extraction)

- Demonstrates successful dual strategy: strengthening legacy brands and expanding agri-commodity base.

2. Improving Branded Business Operating Performance

- Branded margins improved due to tapering tea cost inflation in India.

- Despite inflationary pressure on coffee input costs internationally, operating leverage is being restored.

- Focus on value enhancement over volume suggests improved mix and pricing power.

3. Healthy Debt Metrics and Low Leverage

- Debt-Equity Ratio (Consolidated): 0.12x, well below sector average (~0.5–0.8x).

- Interest Service Coverage Ratio: 22.3x — very strong ability to service debt.

- Low net borrowings, ample liquidity: cash cushion allows flexibility for M&A or dividends.

4. Robust Free Cash Flow Generation

- Despite lower operating cash flow in H1, still positive FCF.

- Capex disciplined at ₹210 Cr (H1), primarily in PPE and development assets.

- Strong dividend policy continued, with ₹820 Cr dividend paid in H1.

5. Strategic Investments in High-Growth Subsidiaries

- Capital Foods (owner of Ching’s Secret & Smith & Jones) now a subsidiary.

- Approval of RMRs (Related Party Transactions) up to ₹1,650 Cr indicates deep integration plans.

- This unlocks cross-selling, shared distribution, and synergies in snacks/noodles space.

6. Strong Brand Positioning

- Portfolio includes iconic brands:

- Tetley (global presence)

- Tata Tea, Tata Coffee

- Organic India

- Teapigs (UK premium tea)

- Leadership in organic and wellness category gives first-mover advantages in evolving consumption patterns.

⚠️ HEADWINDS

1. Input Cost Volatility

- Coffee input costs remain elevated, especially in international markets.

- Though tea inflation is moderating in India, potential for rural wage pressures, weather risks (monsoon, frost), and global freight cost swings continue to be concerns.

2. Commodities-Driven Earnings Volatility

- Non-Branded Business margins impacted by reversal of prior-year fair value gains.

- Agri-commodity prices are inherently cyclical — profit volatility expected in this vertical.

3. Increasing Capex and Investment in Branding

- Higher marketing and branding investments temporarily compressed net margins (EBIT margin: ~10.5% vs 11.4% YoY).

- Returns may take time, especially in International markets where penetration is still growing.

4. Deterioration in Working Capital

- Trade payables down sharply (₹623 Cr outflow in H1), while receivables and inventory built up.

- Indicates extended payment terms to suppliers may have tightened, possibly due to negotiation power shifts post-pandemic.

- Could pressure near-term cash flows.

5. Foreign Exchange Exposure

- Significant international operations: revenue translation exposes earnings to INR volatility.

- Exchange gains/losses on translation were material in other comprehensive income (OCI), though not in P&L.

📈 GROWTH PROSPECTS

1. Integration with Capital Foods – Game-Changing Opportunity

- Capital Foods has seen explosive growth in instant noodles, sauces, and ethnic mixes (e.g., Ching’s).

- Potential for synergy via:

- Distribution cross-leveraging (rural/urban expansion)

- Export platform utilization

- R&D and sourcing aggregation

- TCPL can become a full-spectrum FMCG player beyond beverages.

3. Plantation Modernization and Non-Branded Scale

- Non-Branded business growth (26%) signals effective vertical integration.

- Extraction and commodity sales now contribute more reliably to earnings.

- Future carbon credit monetization at estates possible.

4. International Expansion Beyond Tea

- Building presence in US, Canada, UK, Australia, Africa.

- Organic India USA, Tata Coffee Vietnam, and Star Alliance (Tata Starbucks) provide scalable platforms.

- Beverage expansion (especially RTD coffee/tea) offers long-term growth.

5. Dividend Stability Attracts Long-Term Investors

- Shareholders rewarded despite strategic investments.

- Payout ratios remain sustainable (~70–80%) given net margins and solid equity base.

- Dividend yield ~1.0–1.2% historically — attractive in stable consumer space.

🔒 KEY RISKS

1. Regulatory & Compliance Risk

- High volume of related-party transactions (e.g., with Capital Foods) requires transparency and arm’s length compliance.

- Scrutiny from SEBI, MCA, and institutional investors on MRPTs (Material Related Party Transactions) is expected.

2. Dependency on Commodity Cycles

- While branded business diversifies risk, ~12% of revenue from Non-Branded (plantation) remains subject to monsoon, disease, global prices.

- Negative EBIT impact if prices correct downward in tea/coffee markets.

3. Execution Risk in Integration

- Integrating large subsidiaries (e.g., Capital Foods) involves cultural, systemic, and brand alignment risks.

- Poor integration could lead to dilution of ROI, write-downs.

4. Foreign Operation Volatility

- India contributes ~64% of consolidated segment revenue; balance from internationally volatile markets.

- Geopolitical risks (Africa, Middle East), currency swings, and trade regulations could hurt margins.

5. Competition in Branded Space

- Intense competition from:

- HUL (Bru, Red Label)

- ITC (Sunfeast, Aashirvaad Noodles via recent snack push)

- Nestle India (Maggie, Nescafé)

- Patanjali & emerging D2C players

- Pricing power challenge in mass-market segments.

📊 Key Ratios & Financial Health (Consolidated)

| Ratio | Sep 2025 | Mar 2025 | Trend |

|---|---|---|---|

| Current Ratio | 1.54 | 1.54 | Stable |

| Quick Ratio (approximate) | ~1.1 | ~1.2 | Slight dip (inventory buildup) |

| Net Debt to Equity | ~0.12 | ~0.11 | Low leverage |

| ROE (approx., trailing) | ~12.8% (based on Q2 run rate) | 12.87% FY25 audited | Maintained |

| Inventory Turnover (annualized) | 5.44x | 5.53x | Normalizing, not alarming |

| Debtors Turnover | 19.18x | 19.95x | Slight delay in collections |

💡 Note: TCPL maintains high-quality balance sheet — suitable for further inorganic growth.

🎯 Strategic Takeaways

| Aspect | Verdict |

|---|---|

| Business Resilience | ✅ Strong |

| Growth Momentum | ✅ Positive |

| Free Cash Flow | ⚠️ Stable but under pressure |

| Valuation Headroom | ✅ High |

| Governance | ✅ Robust |

| Investor Returns | ✅ Attractive |

🏁 Conclusion: Investment Summary for TATACONSUM

| Category | Assessment |

|---|---|

| Outlook | Positive – structural growth story with brand-led recovery and agri-commodity play |

| Key Bull Case | Successful integration of Capital Foods can transform TCPL into a multi-category FMCG leader, driving long-term EPS re-rating |

| Valuation Cue | Currently trading at ~35–40x P/E — premium justified if growth sustains above 15% |

| Recommendation | Hold / Accumulate on Dips – strong for long-term investors seeking inflation-resistant, dividend-paying consumer stock |

| Risk Profile | Moderate – low financial risk, but operational leverage to commodity prices and integration execution |

✅ TCPL is transitioning from a “tea company” to a “total consumer products company”.

This shift, supported by strong governance, balance sheet strength, and strategic clarity, makes it a compelling growth play in the Indian consumer sector.

Final Note: Monitor next quarter’s Capital Foods integration updates, RPT utilization, and working capital trends — these will be key indicators of strategic momentum.

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.