NESTLEIND

Equity Metrics

May 8, 2026

Nestle India Limited

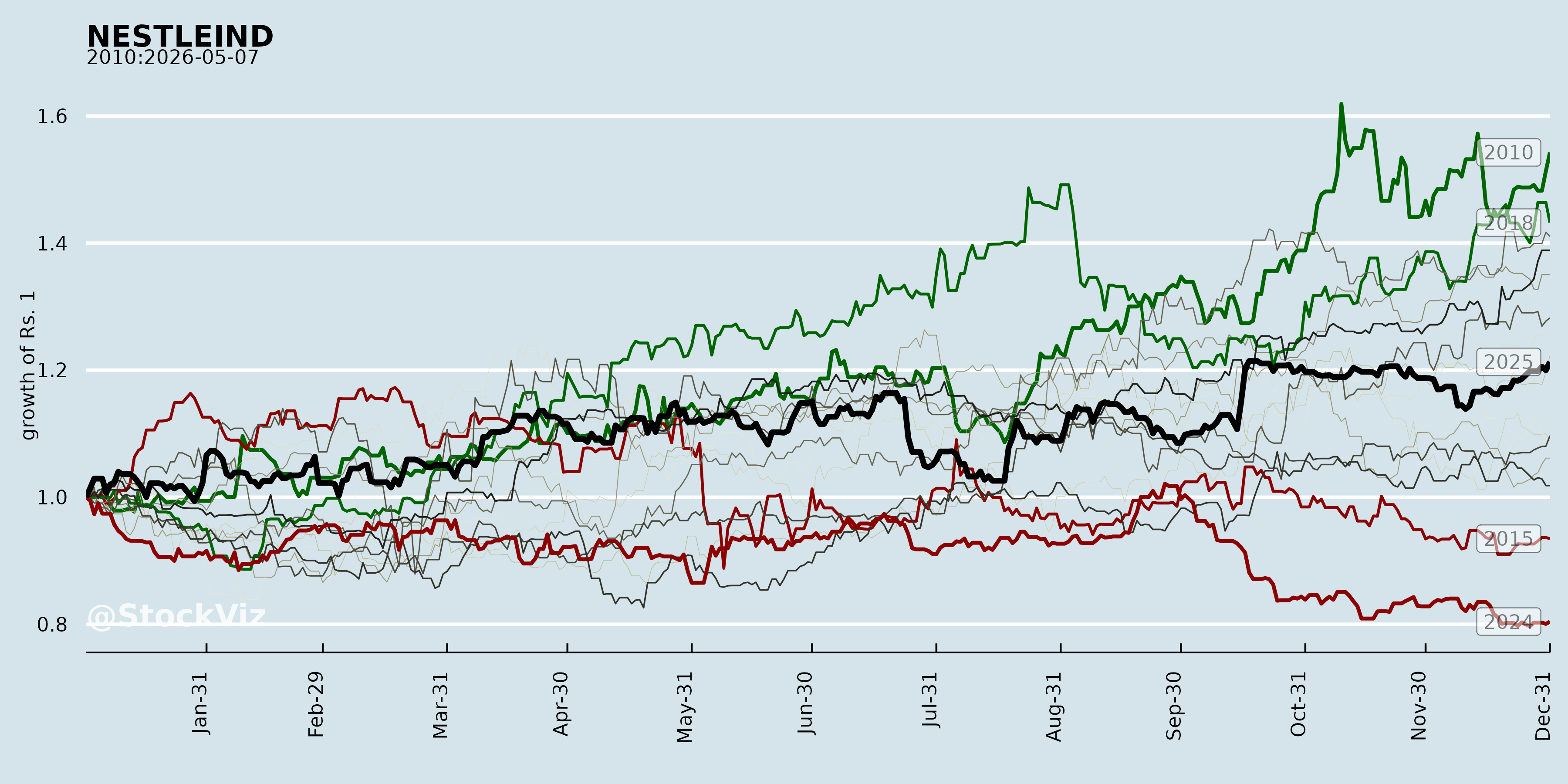

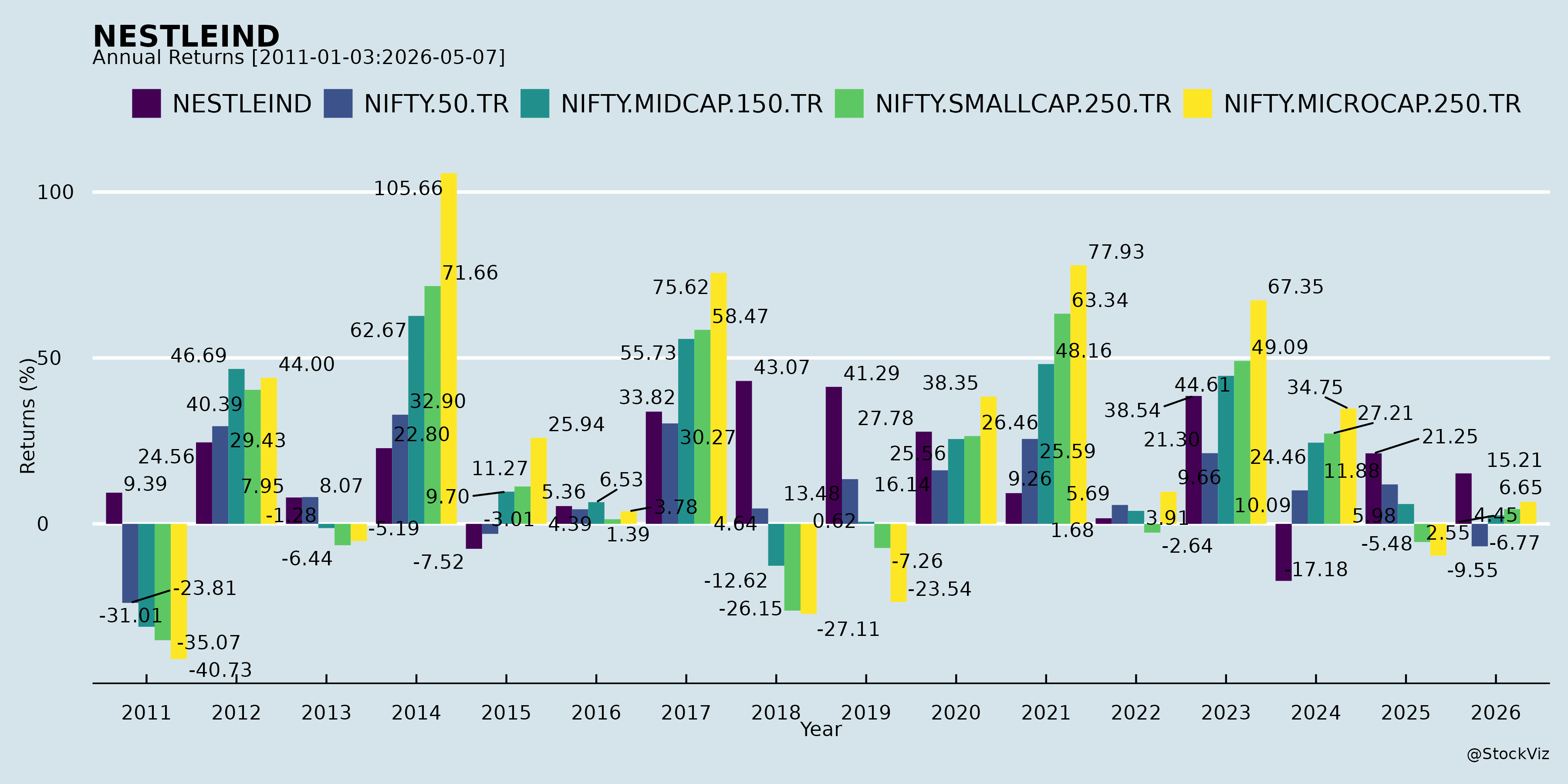

Annual Returns

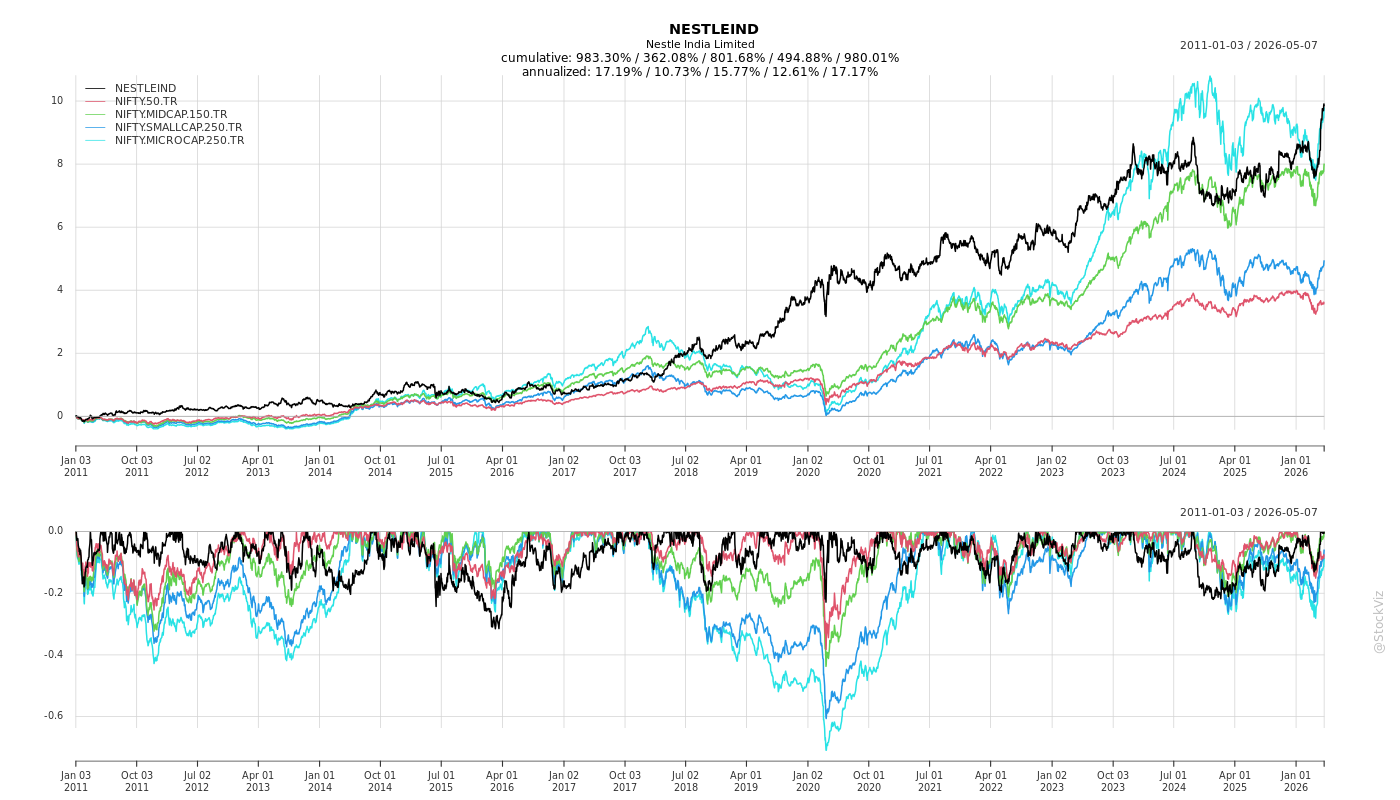

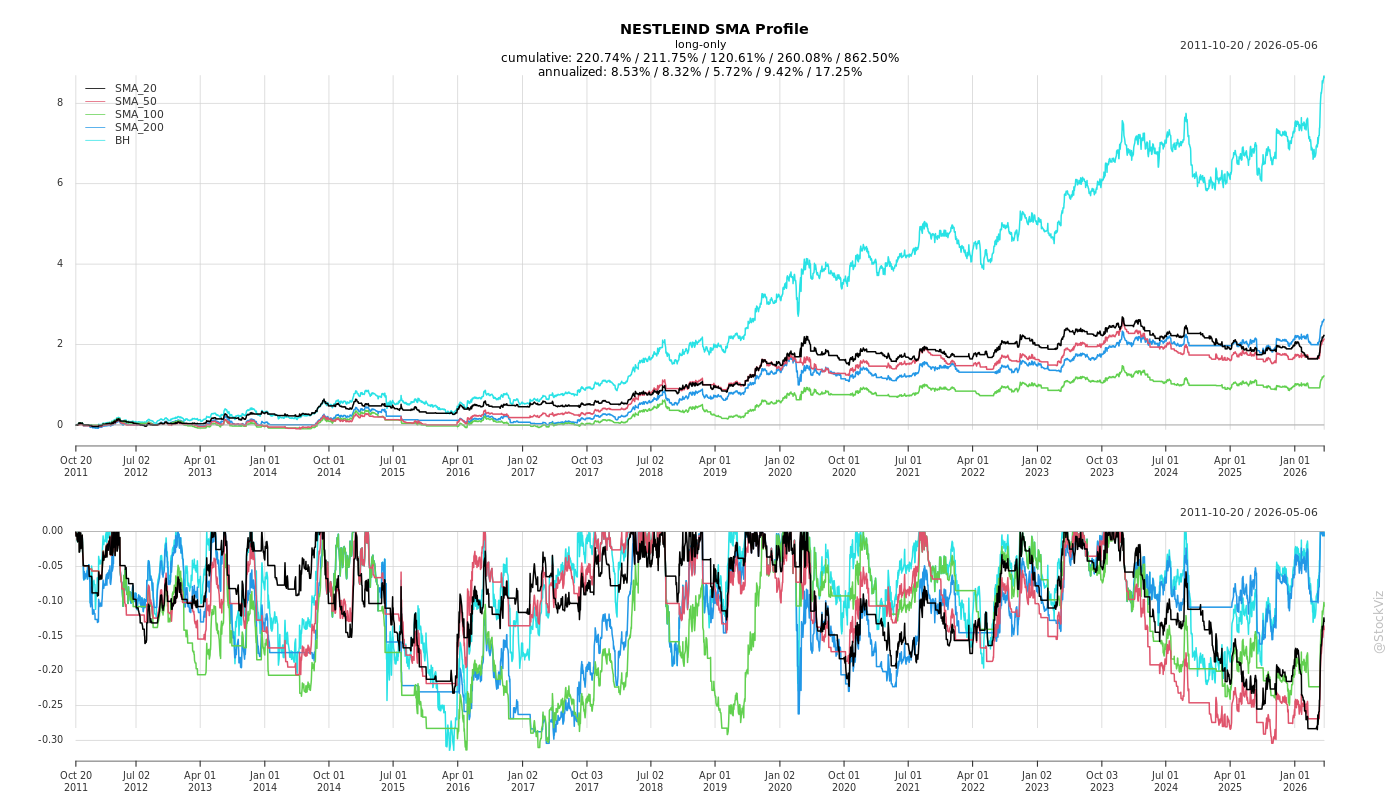

Cumulative Returns and Drawdowns

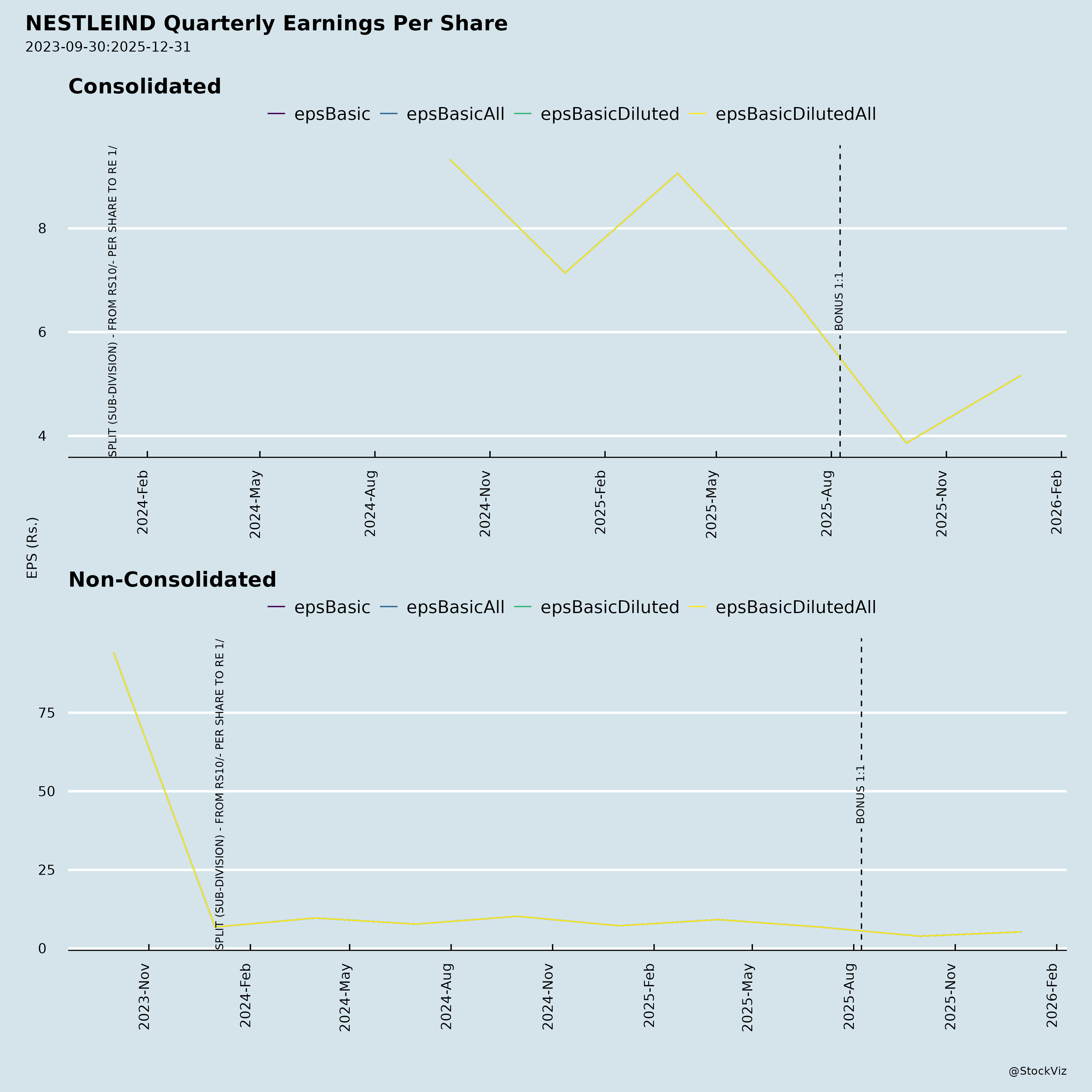

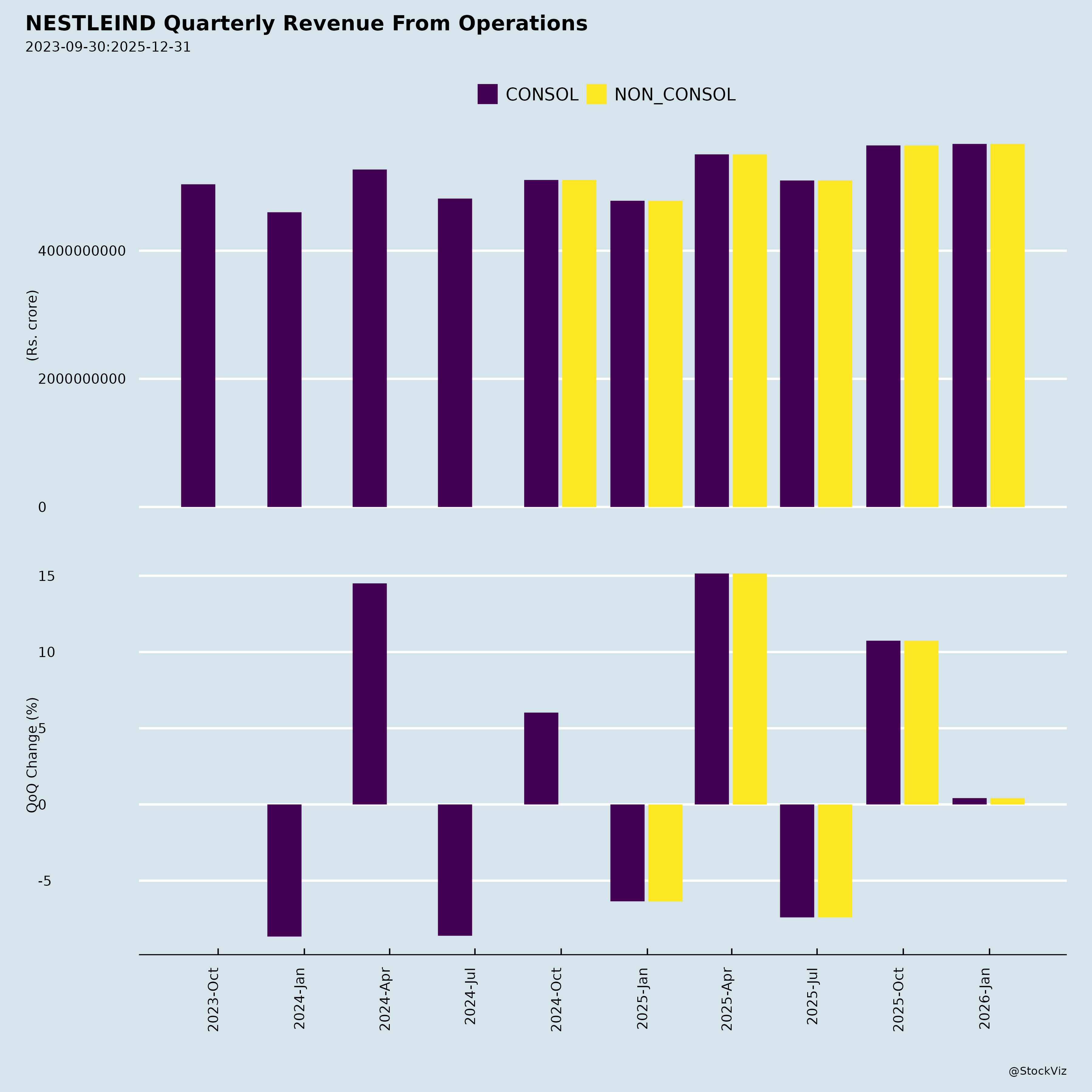

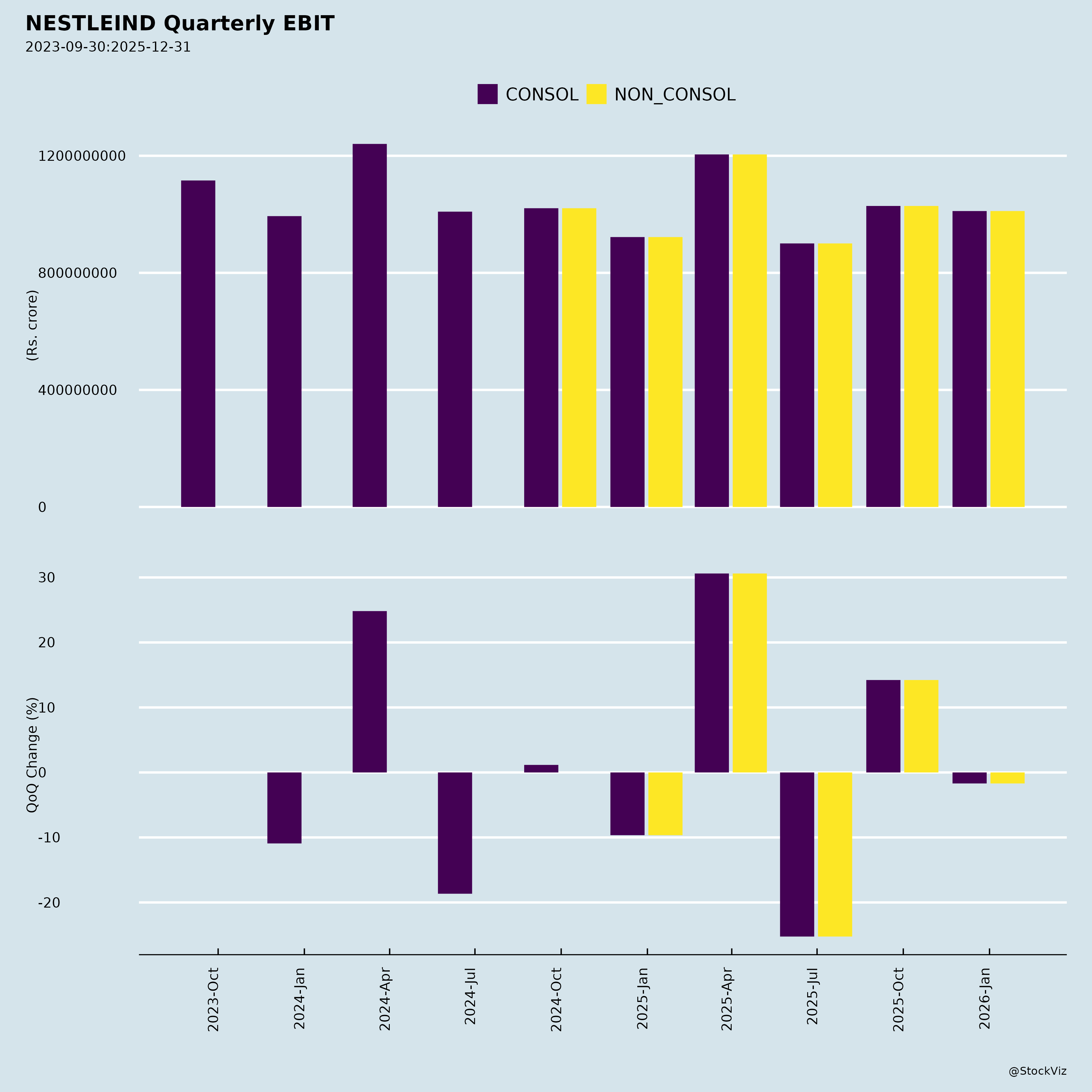

Fundamentals

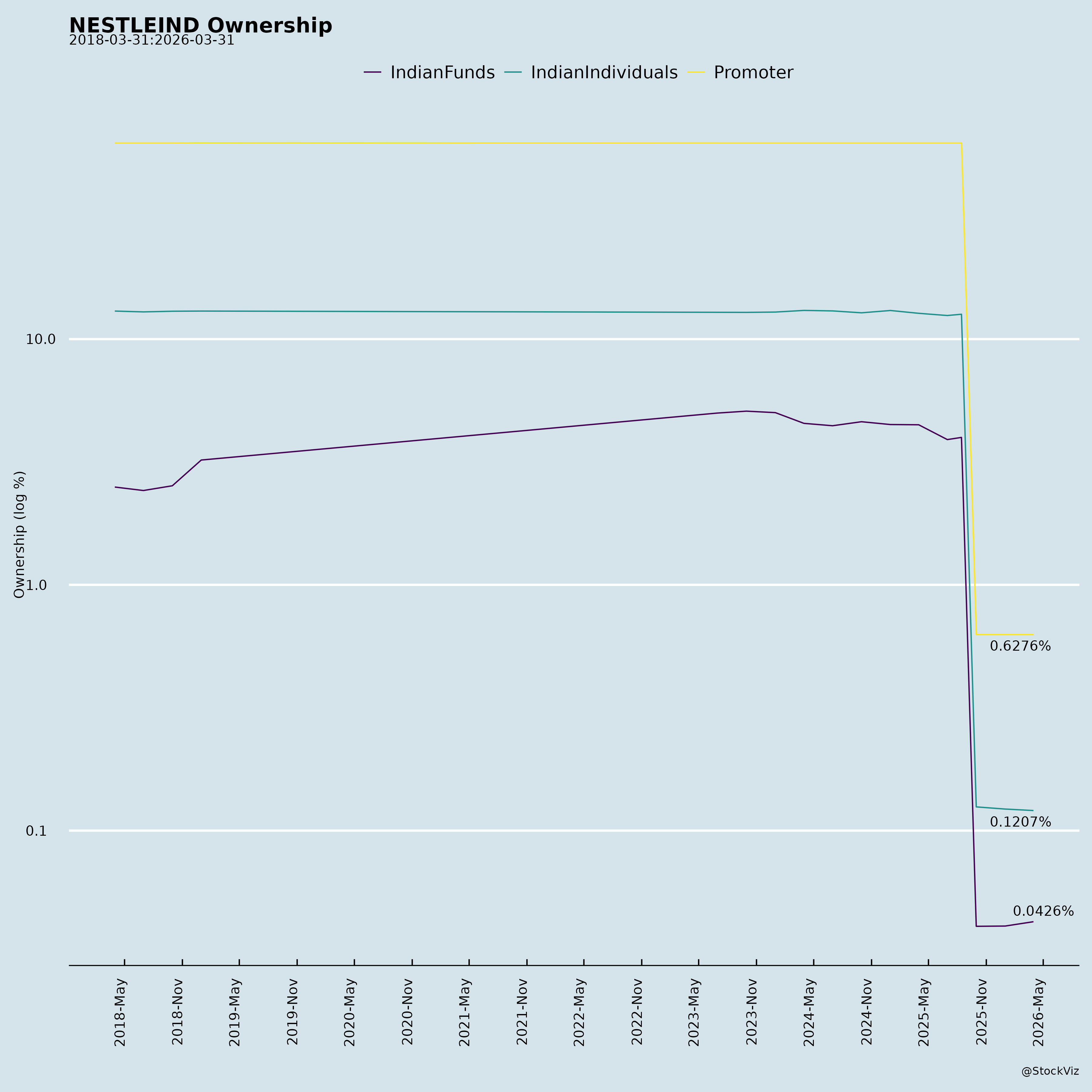

Ownership

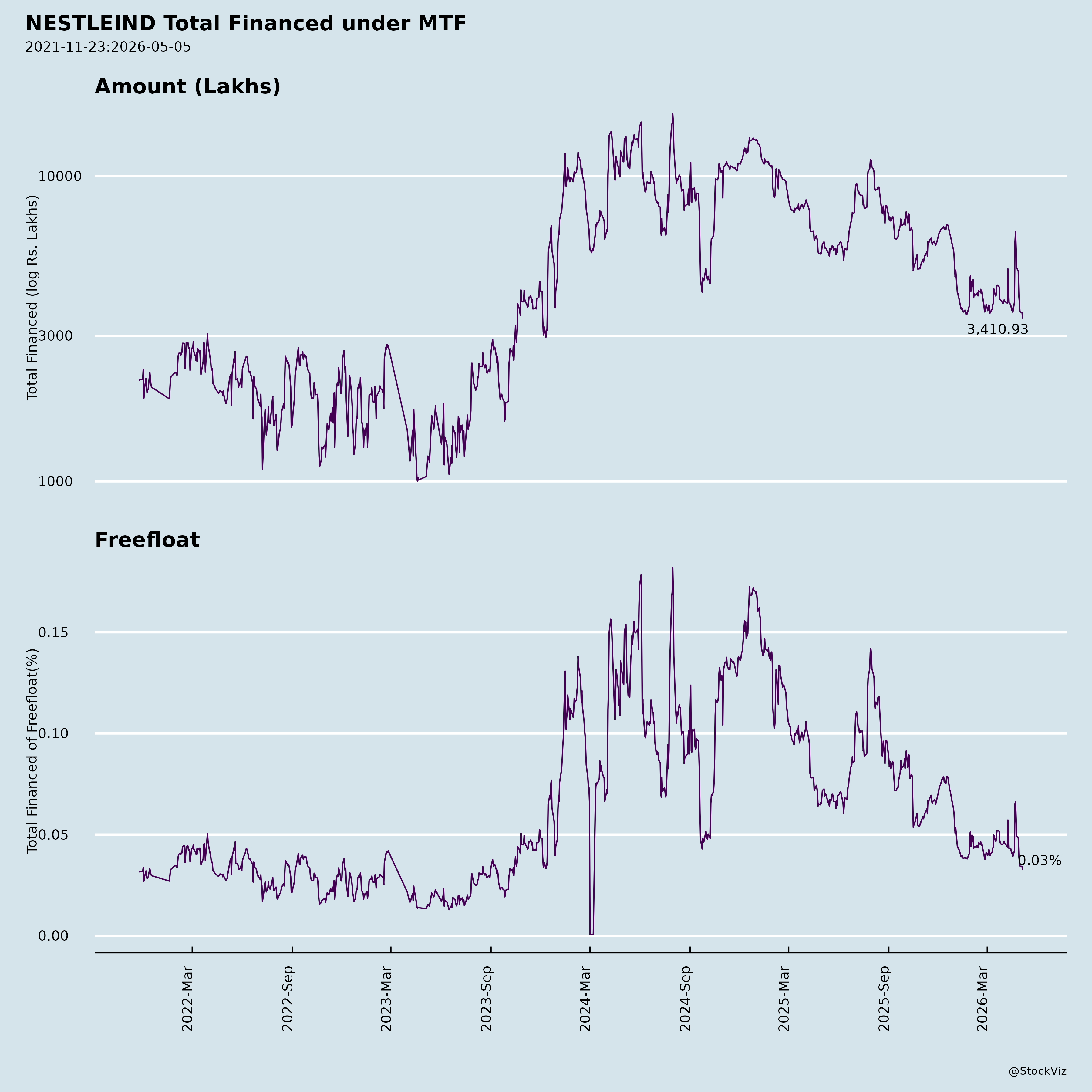

Margined

AI Summary

asof: 2025-12-03

Summary Analysis for NESTLEIND (Nestlé India Limited)

Nestlé India reported robust Q2 FY26 (ended Sep 30, 2025) results with total sales of ₹5,630 Cr (up 10.9% YoY), driven by volume-led double-digit domestic sales growth (10.8%, highest ever quarterly at ₹5,411 Cr). EBITDA margin held strong at 22.0%, PAT at ₹753 Cr, and EPS at ₹3.90 (restated for bonus issue). Three of four product groups (Confectionery, Beverages, Prepared Dishes) delivered strong volume growth, aided by brands like KITKAT, NESCAFÉ, and MAGGI. However, input costs rose, and a recent GST demand poses a minor regulatory headwind. Overall, the company is well-positioned for sustained growth via penetration, premiumization, and capacity expansion, though commodity volatility remains a watchpoint. No material financial/operational impact from disclosures.

Tailwinds (Positive Catalysts)

- Strong Volume-Led Growth: Domestic sales hit record high; 3/4 product groups (Confectionery: KITKAT #2 global market; Beverages: NESCAFÉ market share gains; Prepared Dishes: MAGGI double-digit volumes) drove double-digit growth. Pet Food (PURINA) and Nestlé Professional (OOH, #2 in Zone AOA, fastest growing) hit highs.

- Channel Momentum: E-commerce accelerated (festive, quick commerce, launches like KITKAT Delights/MAGGI Double Masala); Organized Trade/OOH/Export all high double-digit.

- Strategic Initiatives: New Gujarat MAGGI line boosts capacity; omni-channel/rural expansion; GST rate cuts to enhance affordability/consumption.

- Financial Health: Net cash from ops ₹23,140 Mn (up YoY); reduced borrowings (₹479 Mn current); bonus shares (1:1) issued, capitalizing reserves.

- Macro Support: Flush milk season expected to soften prices; coffee/cocoa stabilizing.

Headwinds (Challenges)

- Margin Pressure: Material costs rose to 45.8% of sales (vs. 43.6% YoY) due to higher consumption/purchases; EBITDA resilient but monitored.

- Mixed Segment Performance: Milk Products & Nutrition showed muted growth in parts despite positives (MILKMAID, toddler milks).

- Commodity Risks: Edible oils firm/tight global supply; potential upside pressures post-festive.

- Regulatory Notice: GST order (Dec 1, 2025) demands ₹82.8 Cr tax + interest + penalty (2018-23); non-material per company, to be challenged.

Growth Prospects

- High Potential in Core Areas: Penetration-led strategy targets rural/quick commerce; premiumization (NESCAFÉ Gold, KITKAT variants); innovations (Polo Sharebag, NESCAFÉ RTD exports to UAE/Saudi/Singapore).

- Capacity & Investments: Accelerated capex in brands/manufacturing; Sanand expansion signals “Make in India” commitment.

- Export/Adjuncts: High double-digit export growth (MAGGI/NESCAFÉ/KITKAT); Pet/OOH scaling fast.

- Outlook: “Fast, Focused, Flexible” transformation; festive/GST tailwinds; FY26 sales growth guided implicitly via volume focus (prior exceptional gains normalized EPS comparable).

- Projections: Analysts may revise upwards; consensus likely eyes 10-12% sales CAGR, 20%+ margins sustained.

Key Risks

| Risk Category | Details | Mitigation |

|---|---|---|

| Commodity Volatility | Edible oils rising; milk/coffee/cocoa sensitive to global supply. | Hedging, flush season; diversified sourcing. |

| Regulatory/Litigation | GST demand (₹248 Cr total exposure); potential appeals. | Company plans challenge; stated “no material impact”. |

| Execution/Competition | FMCG slowdown risks; reliance on KITKAT/MAGGI/NESCAFÉ (top drivers). | Omni-channel, innovations; single “Food” segment focus. |

| Macro/Consumer | Rural/urban consumption fragility; inflation. | Volume strategy, affordability via GST pass-through. |

| Financial | Dividend payouts (₹9,642 Mn in H1); capex (₹3,878 Mn). | Strong FCF (₹23 Bn ops cash); low debt. |

| Other | Associate (Dr. Reddy’s JV) share of loss (₹227 Mn); forex/unrealized gains. | Equity method; stable. |

Investment View: Bullish near-term on volume momentum and strategic execution; monitor Q3 commodities/GST appeal. Stock likely supported at current levels post-results (trading ~₹2,400-2,500 pre-results context). Target upside 10-15% in 12M on 25-30x FY26 EPS.

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.