JWL

Equity Metrics

May 8, 2026

Jupiter Wagons Limited

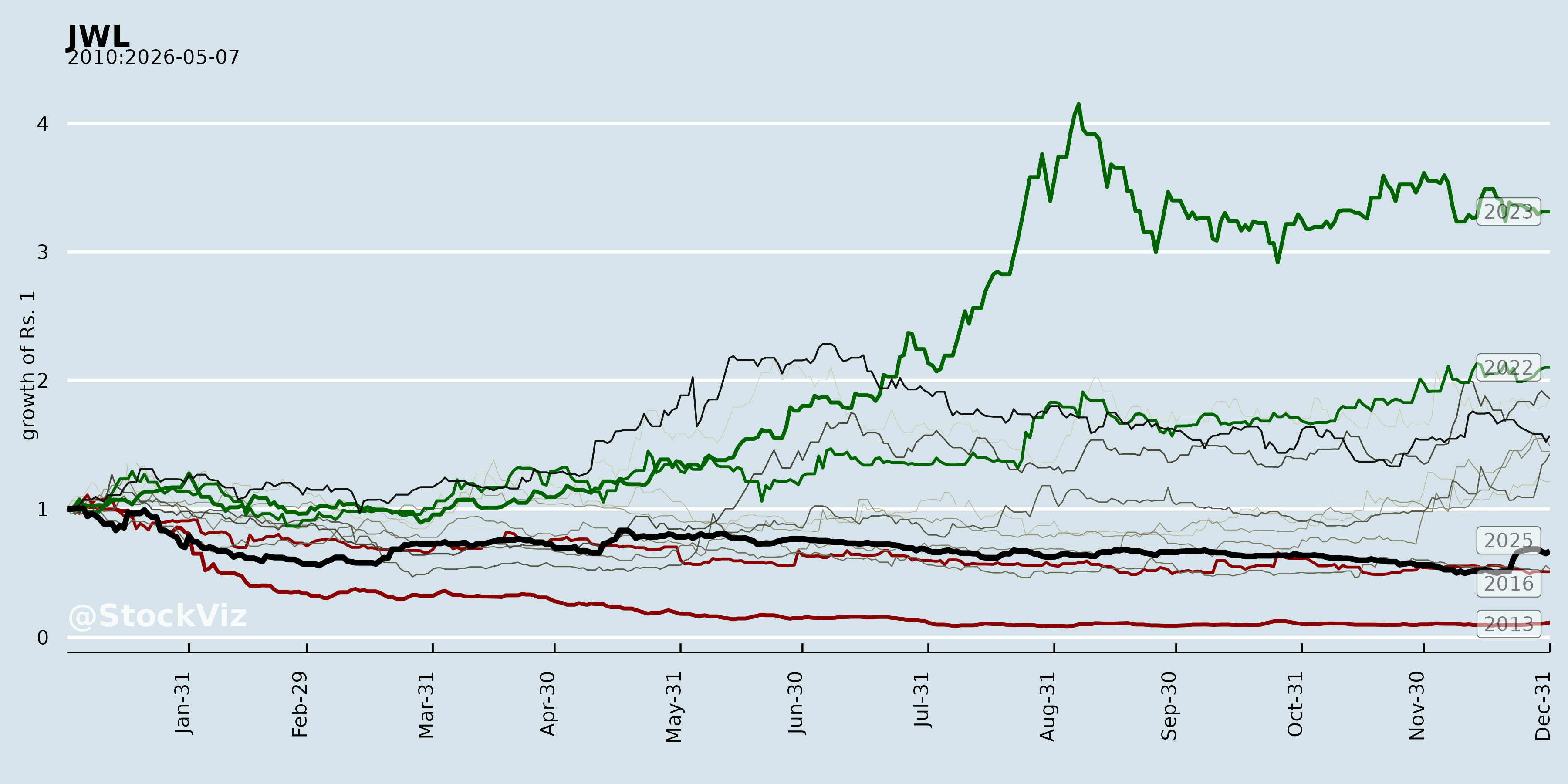

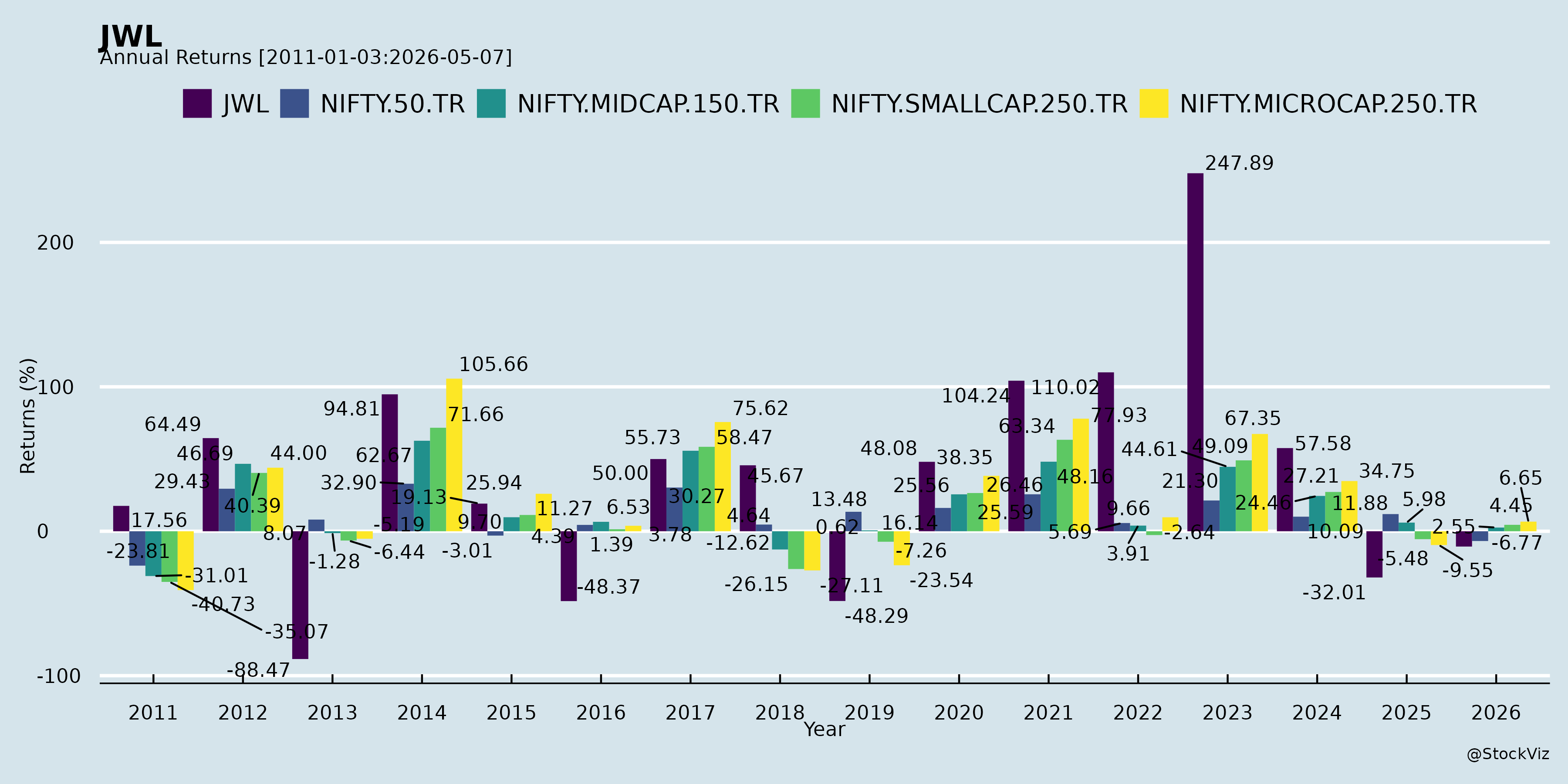

Annual Returns

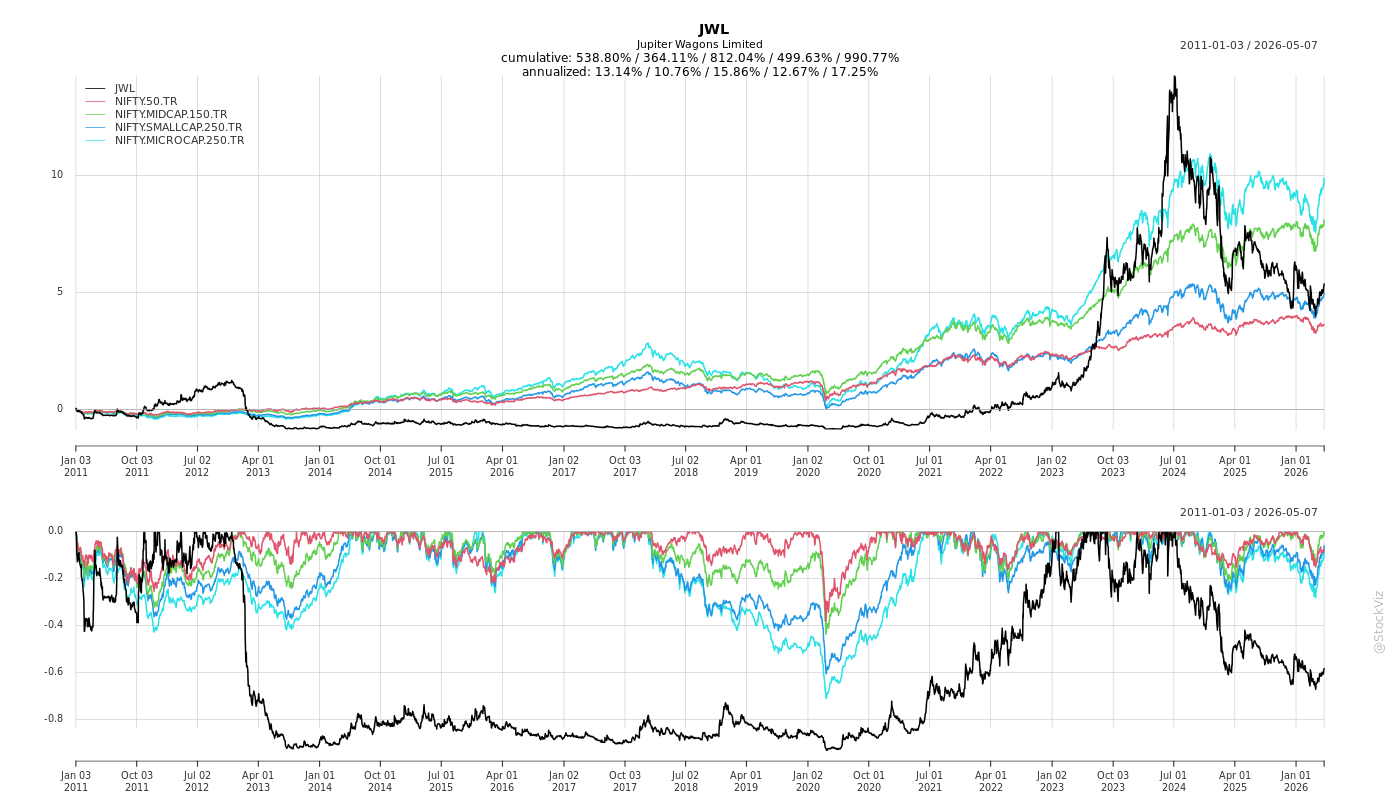

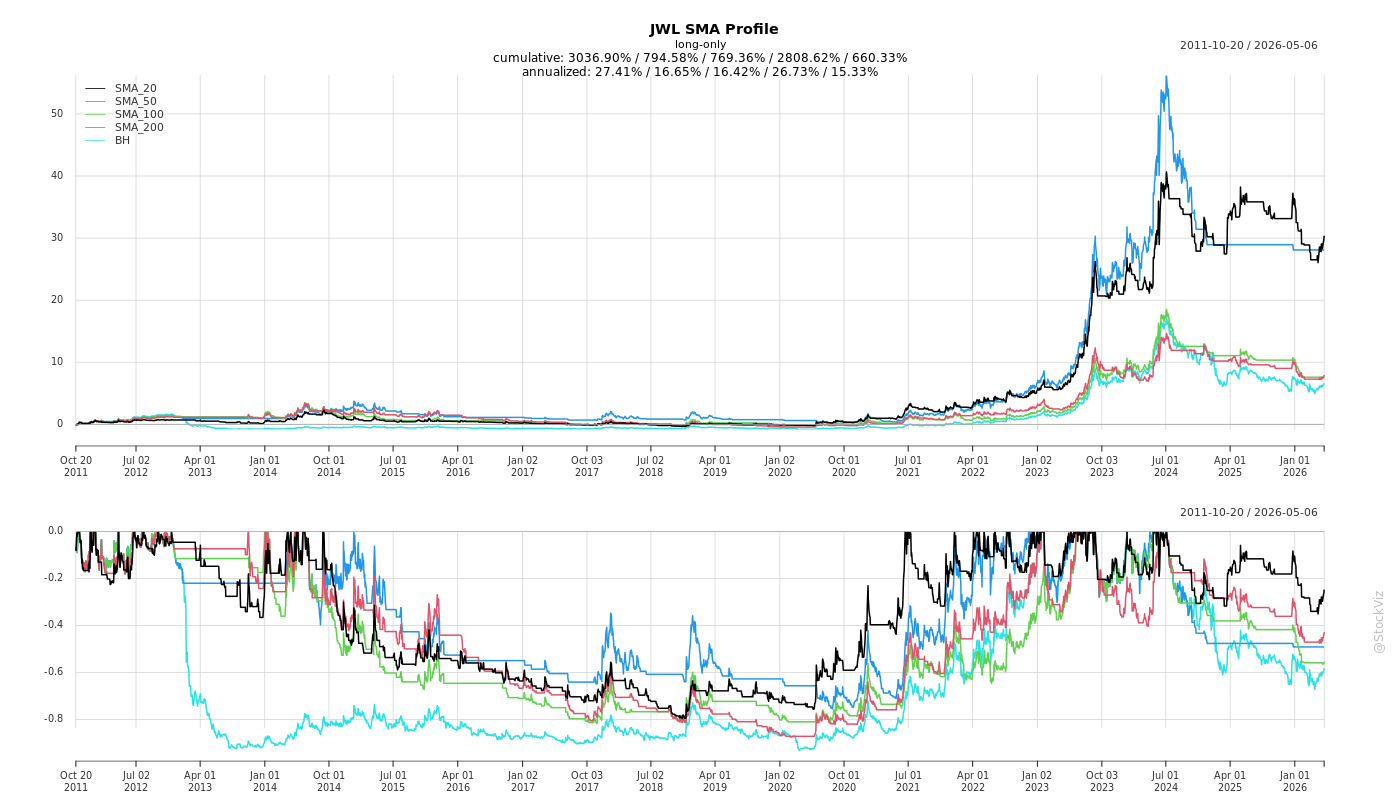

Cumulative Returns and Drawdowns

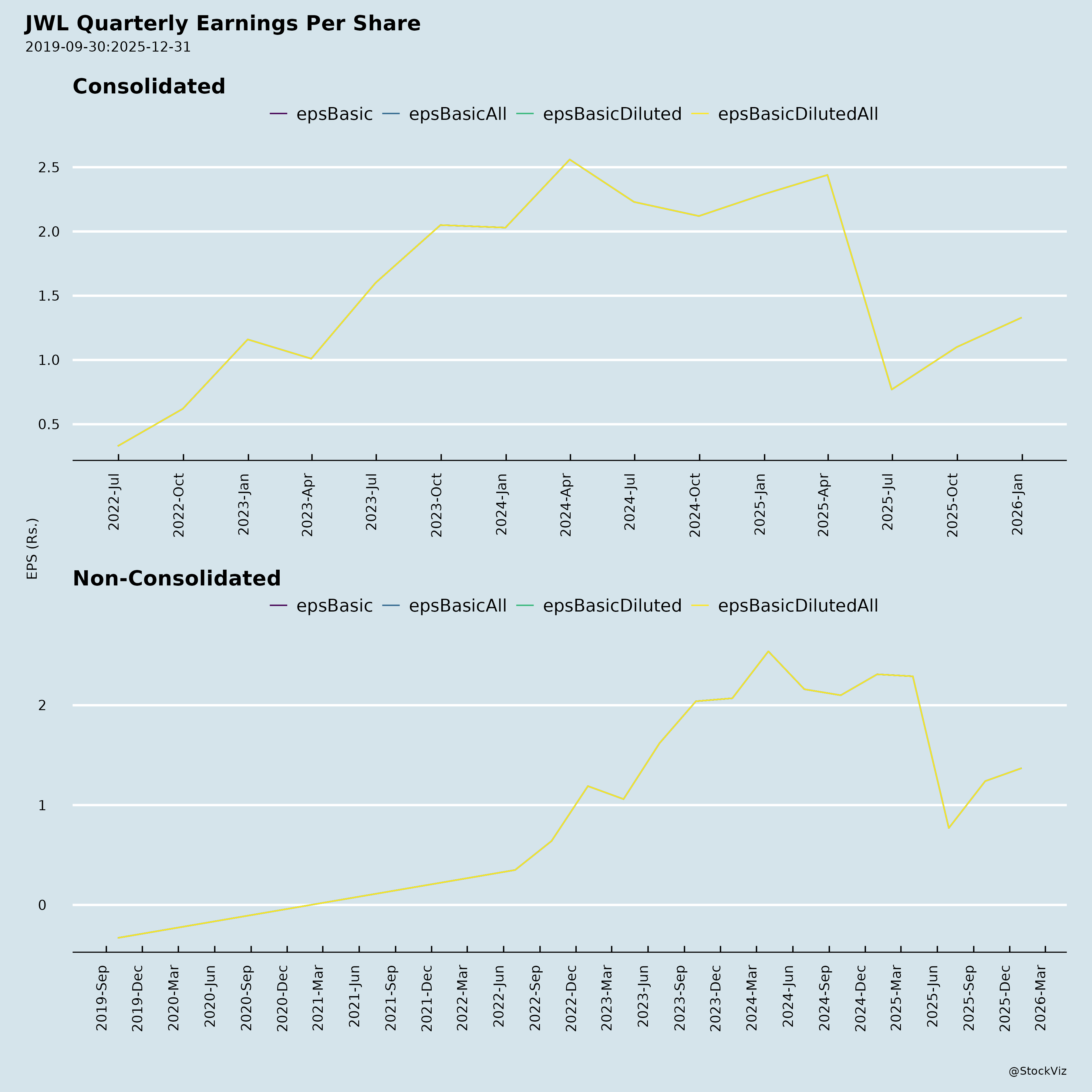

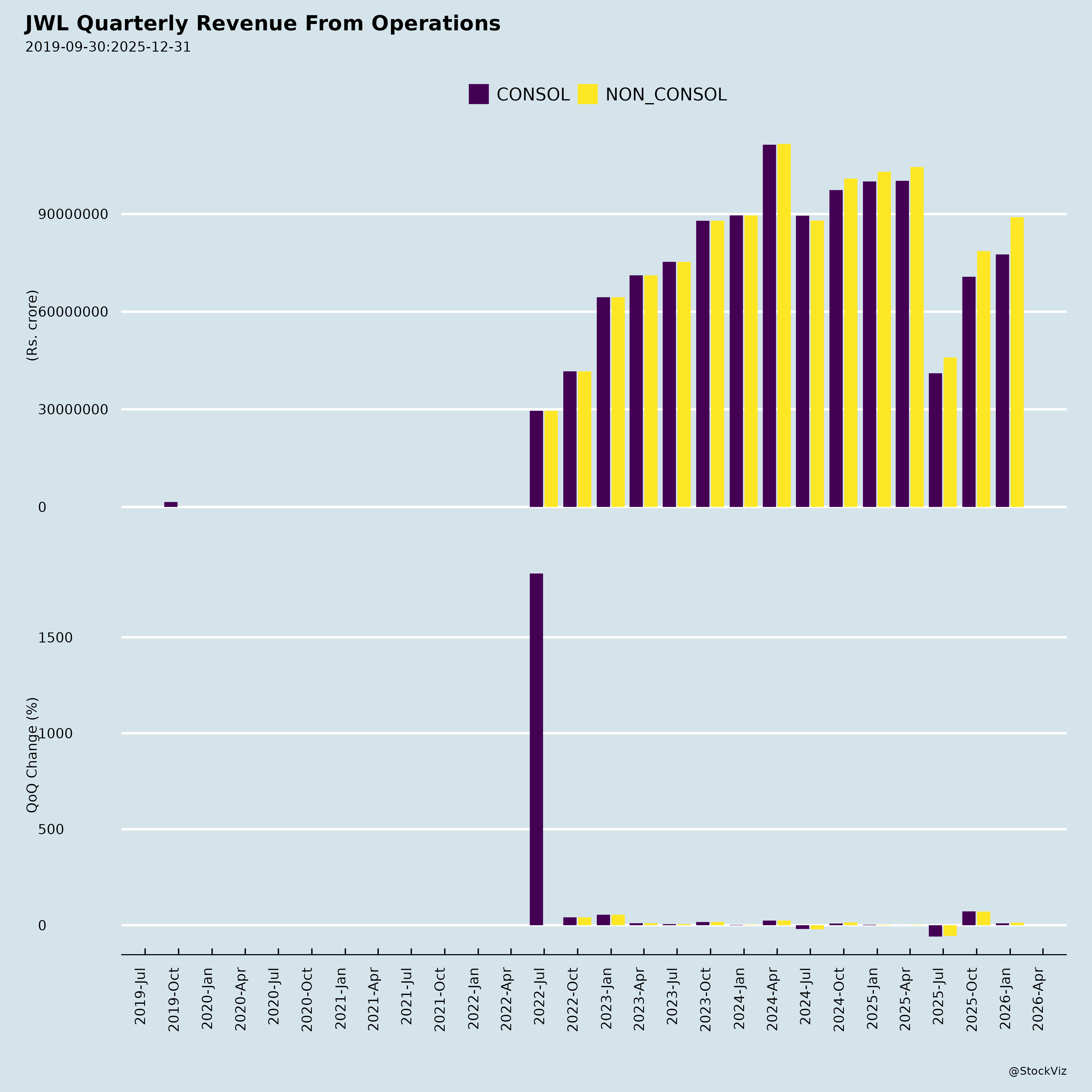

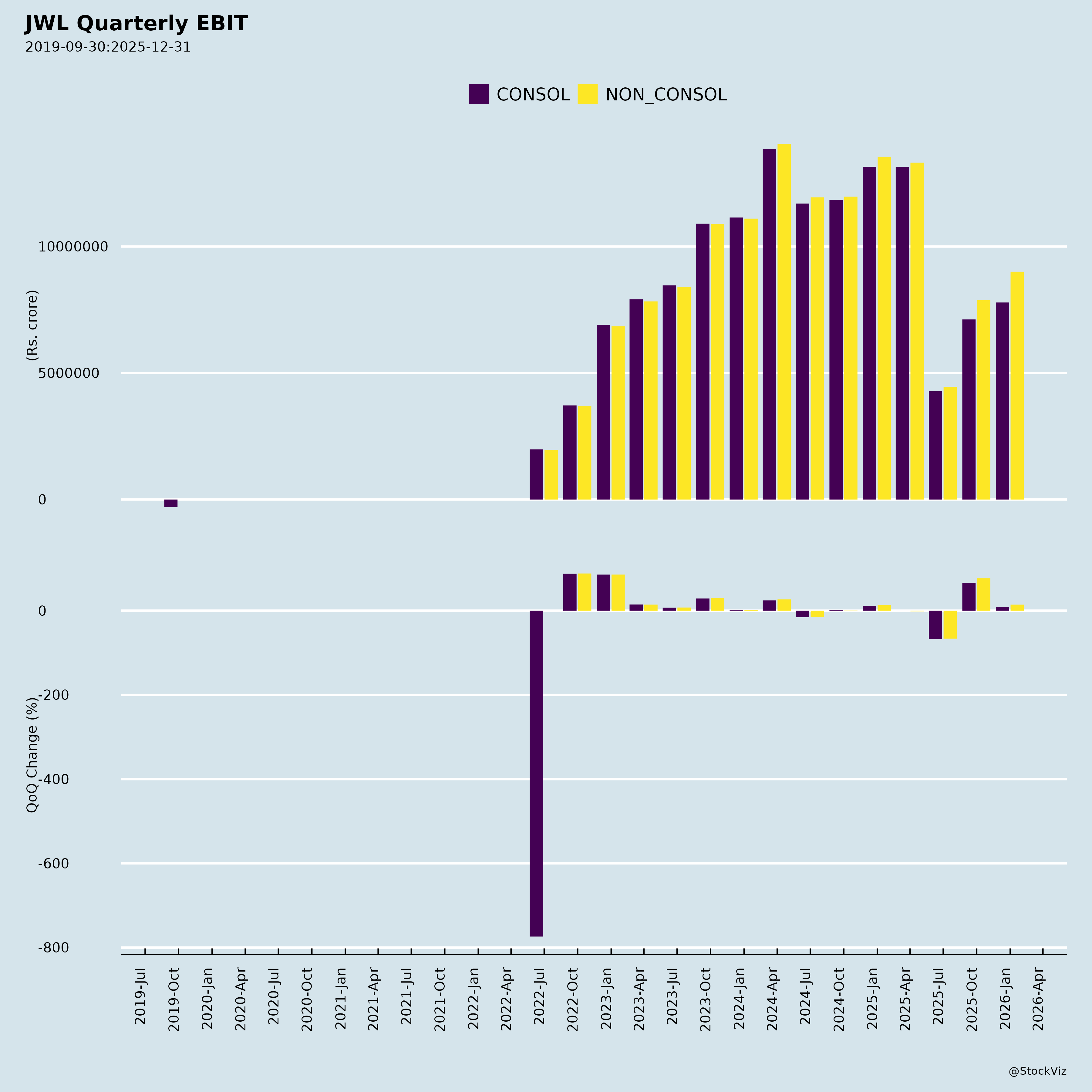

Fundamentals

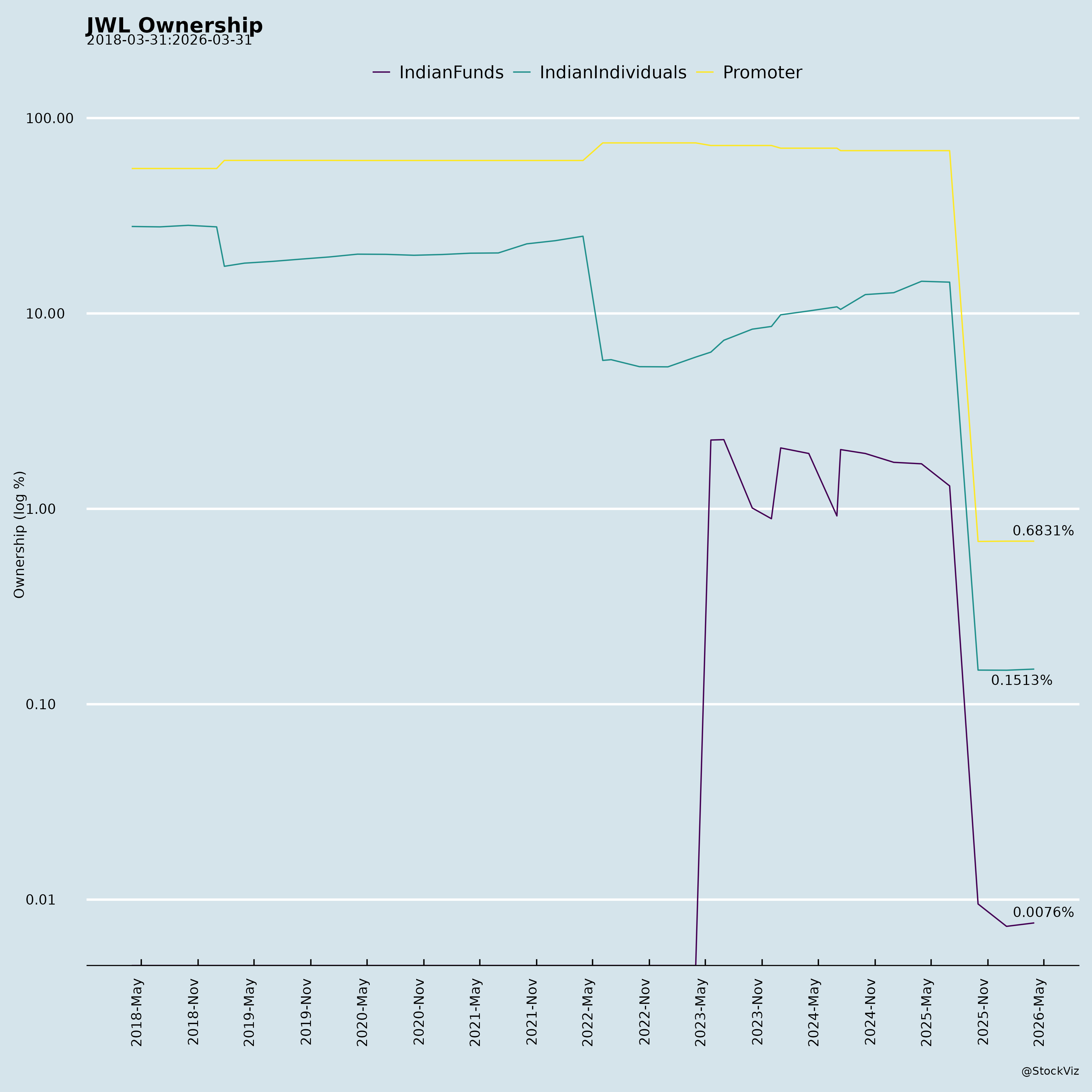

Ownership

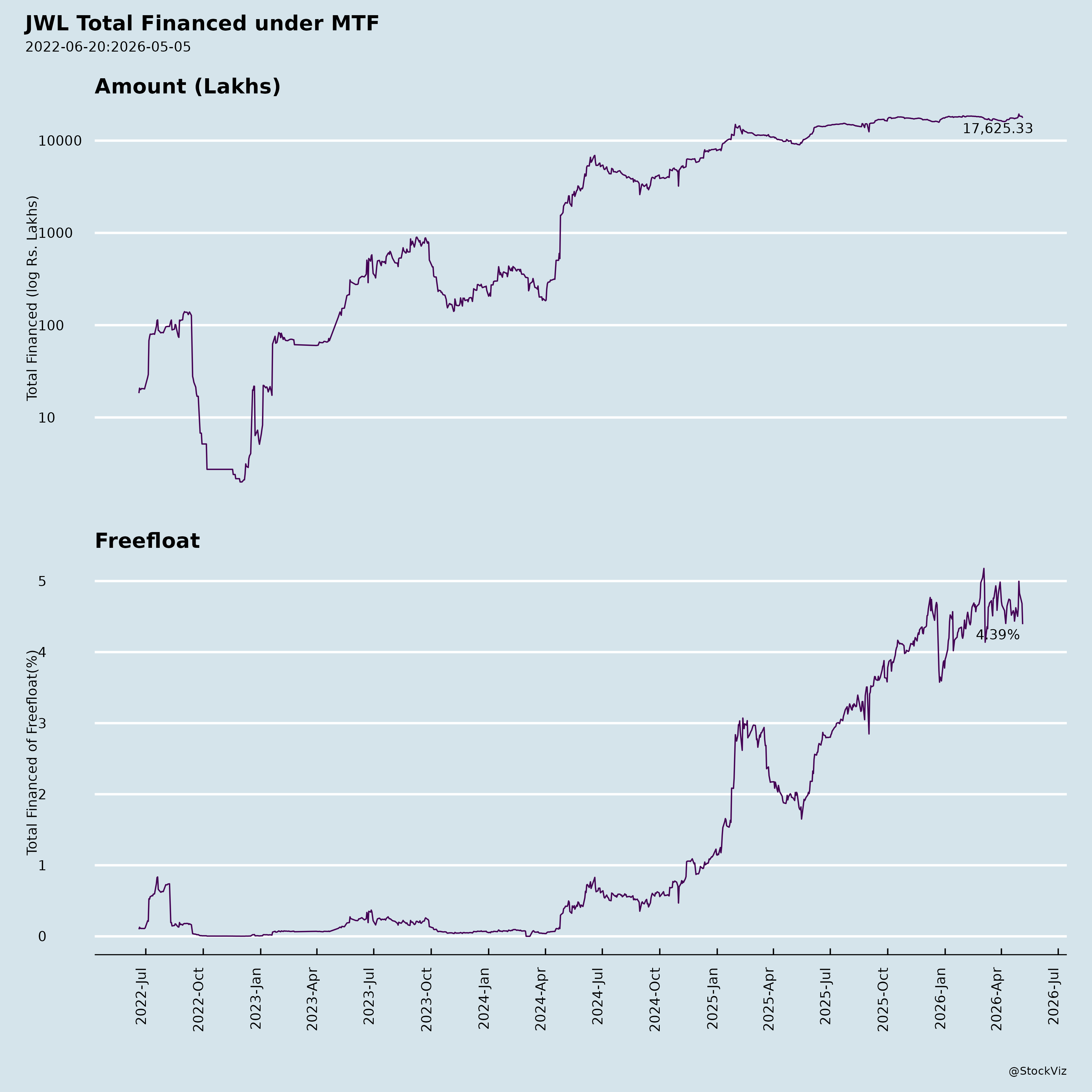

Margined

AI Summary

asof: 2025-12-03

Jupiter Wagons Limited (JWL) Analysis: Headwinds, Tailwinds, Growth Prospects, and Key Risks

Jupiter Wagons Limited (JWL), a diversified rail and mobility solutions provider (wagons, components, containers, BESS, eLCVs), reported Q2/H1 FY26 results impacted by early-year wheelset supply disruptions but showed strong sequential recovery. Consolidated H1 FY26 revenue was ₹1,245 Cr (-34% YoY), EBITDA ₹163 Cr (13.1% margin), PAT ₹76 Cr (6.1% margin). Order book stands at ₹5,538 Cr (Sep 2025), providing ~2-3 years visibility. Wagon business (~60-70% revenue) is stabilizing, with diversification into high-margin segments (wheels, containers, BESS, EV). Below is a structured summary based on earnings call, financials, investor presentation, and disclosures.

Headwinds (Challenges Impacting Near-Term Performance)

- Supply Chain Disruptions: Wheelset shortages (Q1 FY26 and July) led to 71% QoQ Q2 revenue growth but 34% YoY H1 decline; missed FY26 revenue guidance of ₹5,000 Cr.

- YoY Declines & High Base: Q2 revenue -22% YoY, PAT -49% YoY due to strong prior-year execution; EBITDA margins dipped 150 bps YoY to 13.1%.

- Delayed Railway Tenders: Major ~50,000 wagon tenders postponed (due to industry backlog); recent small tenders (5-6k wagons) floated, but large ones expected early FY27.

- Margin Pressures: PAT margins at 5.8-6.1% (vs. 9.6% H1 FY25); exceptional loss of ₹10.4 Cr in Q2 (lease rent settlement); JVs/subsidiaries still marginally negative.

- Inventory Build-Up: H1 inventories up ~45% YoY to ₹1,119 Cr, tying up working capital amid execution ramp-up.

Tailwinds (Positive Momentum Drivers)

- Supply Normalization: Wheelsets now available (no issues for next 6-12 months); Q2 revenue +71% QoQ, EBITDA +73% QoQ.

- Robust Order Book: ₹5,538 Cr (~Sep 2025), with 60% private orders (higher margins); recent wins: ₹242 Cr from GATX (583 wagons), ₹113 Cr (9k LHB axles), ₹215 Cr LoI (Vande Bharat wheelsets).

- Diversification Gains: Non-wagon volumes up (e.g., containers doubled YoY, wheels +300% YoY); private orders resilient amid railway delays.

- Backward Integration: Odisha forged wheel/axle plant (₹2,500 Cr capex) on track (axles CY2026, wheels CY2027; 100k wheelsets/year capacity).

- Strong Balance Sheet: Net cash position (cash ₹526 Cr vs. borrowings ₹723 Cr); ROE 17.2% (FY25), low D/E 0.13; ESG rating 46.

- Leadership Stability: New CFO (Vinod Agarwal); AGM resolutions passed overwhelmingly (e.g., 99.95% for financials/auditors).

Growth Prospects (Medium-to-Long Term Opportunities)

- Railway Infra Boom: National Rail Plan targets massive capex (₹70-80k Cr announced); FY27 wagon volumes to surge post-tender execution; exploring aluminum/specialized wagons, passenger (Vande Bharat/Metro) entry by FY27.

- Diversification to 50% Non-Wagon by FY28: | Segment | H1 FY26 Volumes | Outlook | |———|—————–|———| | Containers | 839 (+100% YoY) | Data centers/solar; clients: GE, Toshiba, Reliance; capacity expansion. | | Wheels/Wheelsets | 769/10k (+300% YoY) | Export potential; Odisha plant self-reliance. | | BESS (JEM) | First 10ft/20ft units delivered | C&I focus; own BMS/EMS soon; multifold volume growth. | | eLCVs (JEM) | ~50 units; ₹100 Cr FY26 target | 10+ dealerships; double FY27; EBITDA+ FY27 (20-30% MoM growth). |

- Clean Energy/Mobility: BESS leadership (few proven players); EV partnerships (Porter, Pickkup); 1-2 tonne variants FY27.

- Capex/Expansion: JVs (Dako, Kovis, Talegria) maturing; Stone India PAT+ FY27; total revenue/margin expansion FY27-28.

- FY26-28 Outlook: H2 FY26 revenues/margins improve; FY27: Railway volumes + EV/BESS scale; aim pre-disruption peaks + diversification.

Key Risks (Potential Vulnerabilities)

| Risk Category | Description | Mitigation |

|---|---|---|

| Execution/Supply | Wagon delivery delays if wheelsets recur; capex overruns (Odisha). | Supply normalized; integrated facilities. |

| Revenue Concentration | 40% railways, 60% private; tender dependency. | Diversification; private resilience. |

| Competition | Wheels (Titagarh), EV/BESS (Reliance/Adani/Tata entry). | Tech JVs, first-mover in BESS delivery. |

| Macro/Regulatory | Infra slowdown, raw material volatility (steel), policy shifts (rail tenders). | Strong order book; govt. push (Make in India). |

| New Ventures | BESS/EV scaling (infancy stage); JVs/subsidiaries EBITDA timeline slips. | Proven pilots; on-track milestones. |

| Financial | Working capital strain (inventory/receivables up); forex (imports). | Cash-rich; margins improving vs. peers. |

Overall Summary: JWL faces short-term headwinds from supply hiccups and tender delays (H1 impacted), but tailwinds from order visibility, diversification, and rail infra boom position it for H2 FY26 recovery and FY27 acceleration. Growth prospects are strong in high-margin non-wagon segments (BESS/EV to potentially surpass wagons), targeting margin expansion to FY25 peaks. Risks are manageable via integration/JVs, but execution in new areas is key. Recommendation: Positive outlook; monitor Q3 execution and tenders. (Valuation context: FY25 PAT ₹373 Cr; current multiples attractive vs. peers on order book strength.)

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.