TV Broadcasting & Software Production

Industry Metrics

May 8, 2026

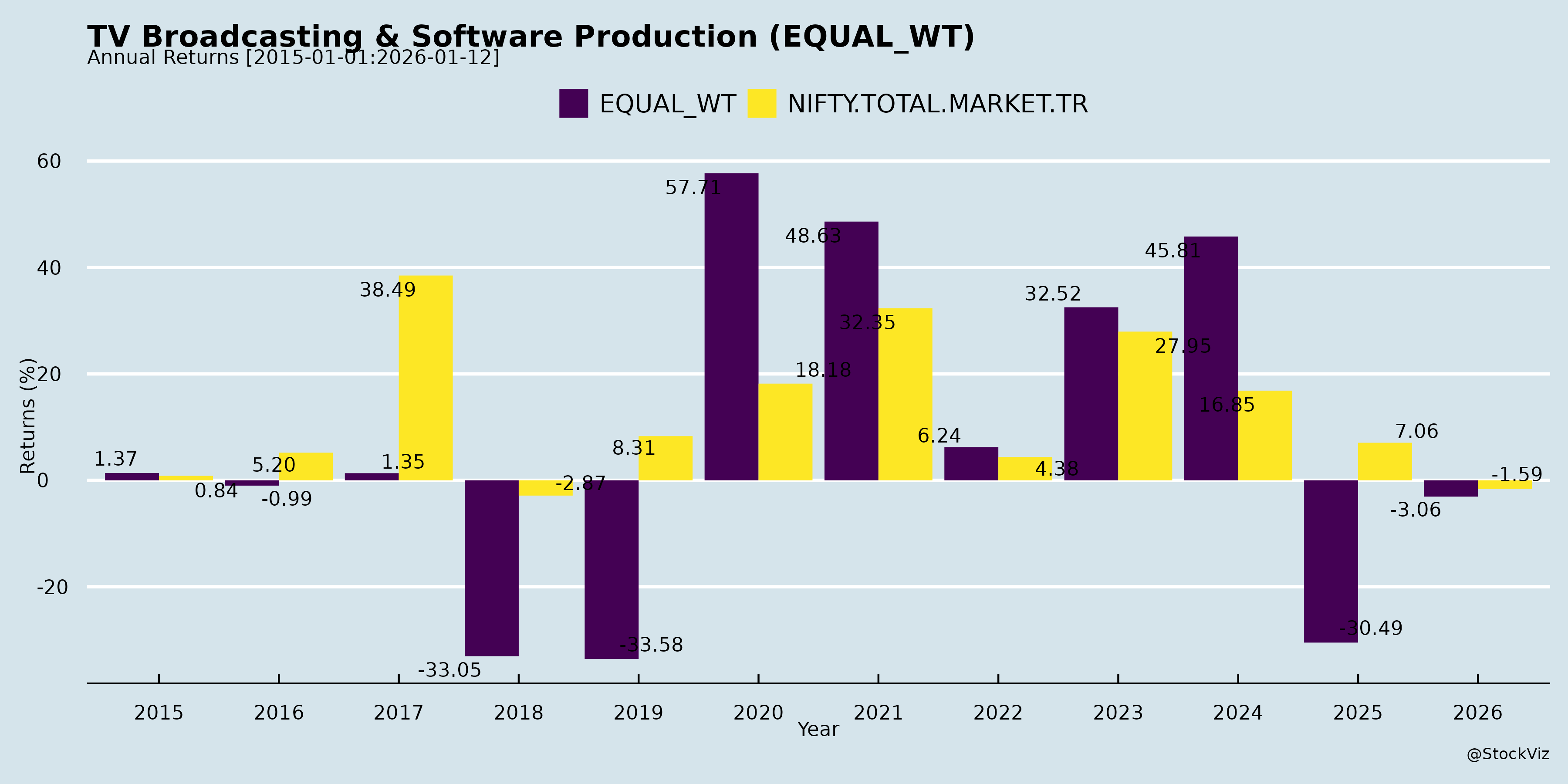

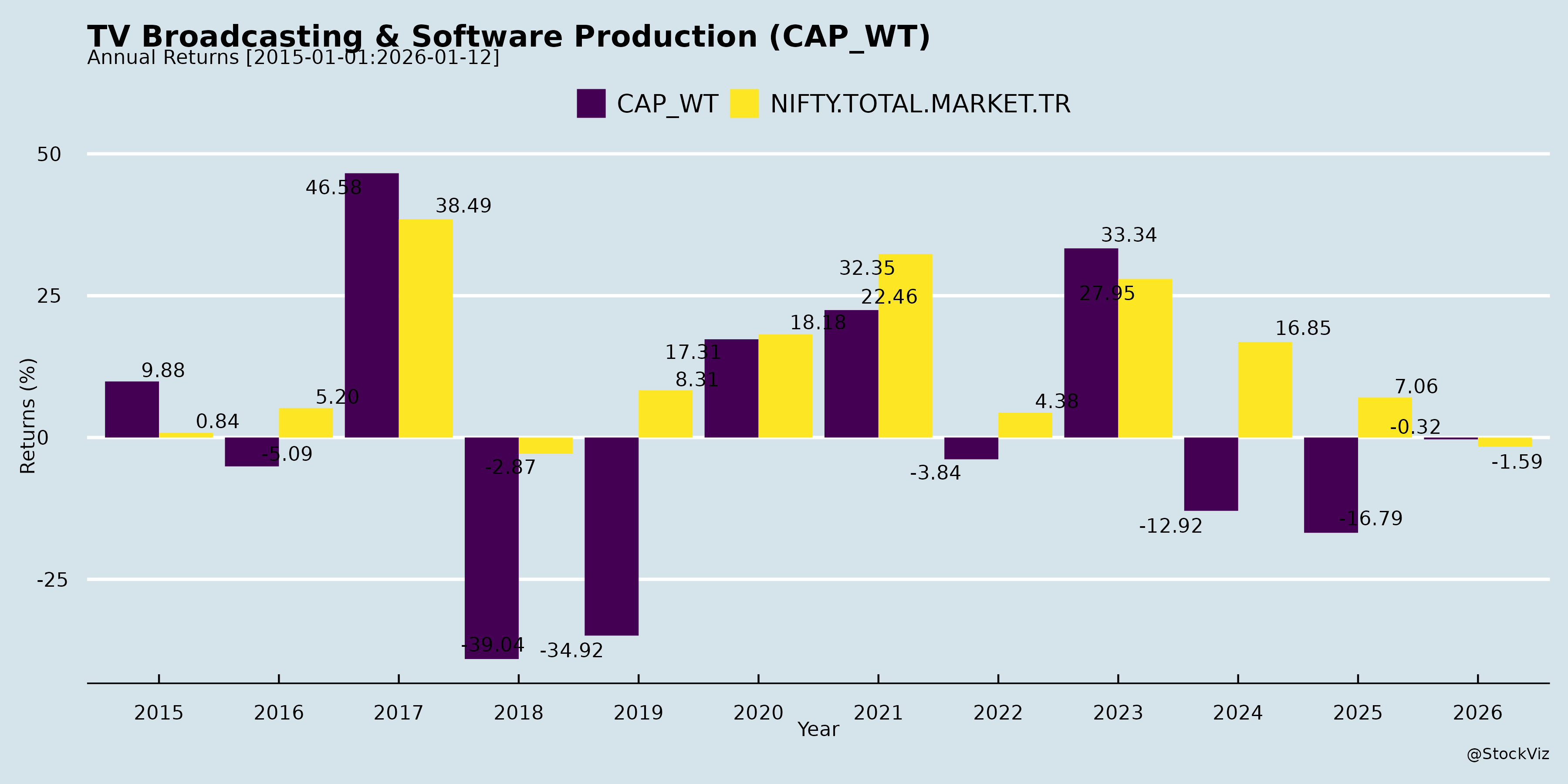

Annual Returns

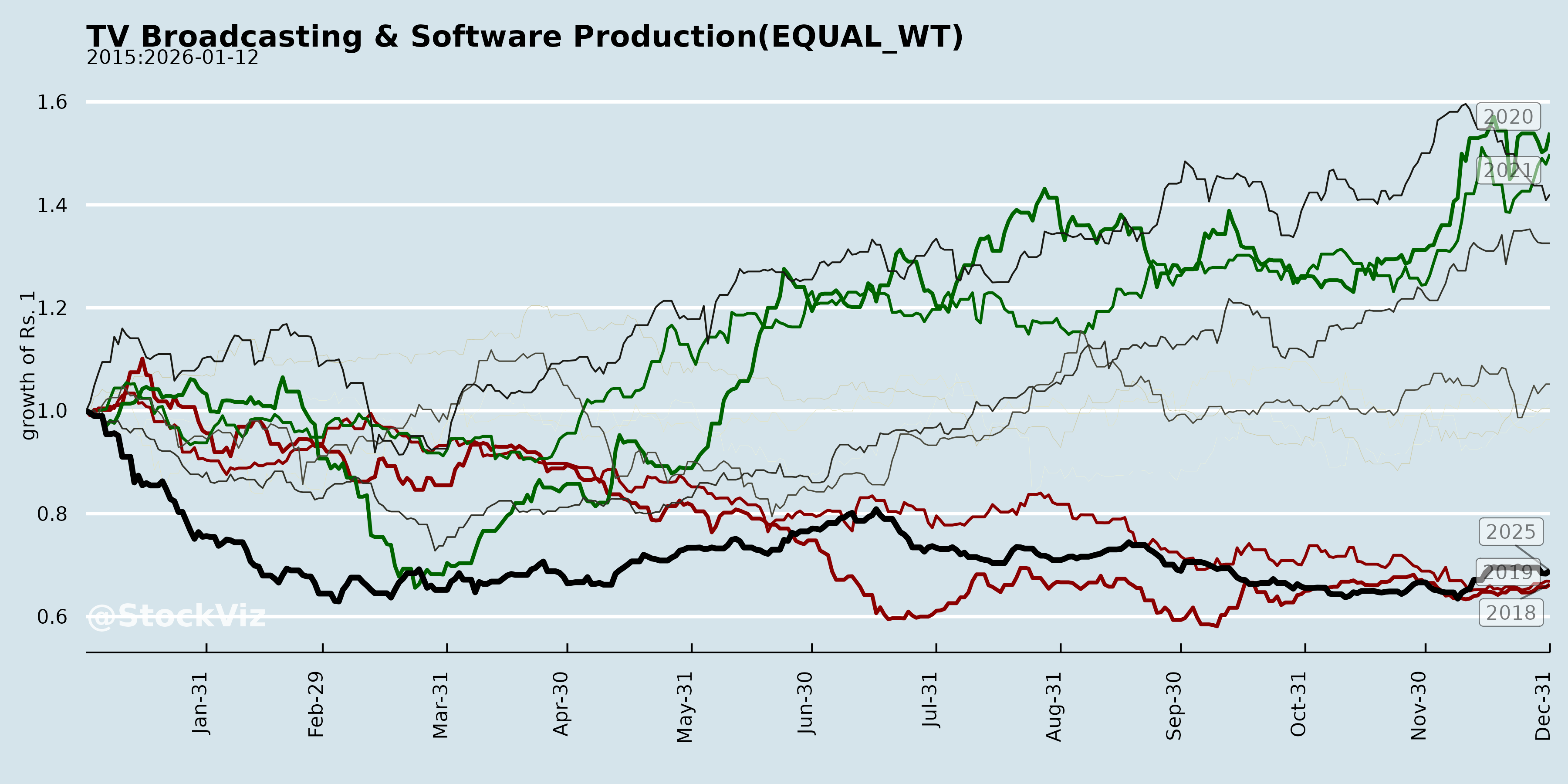

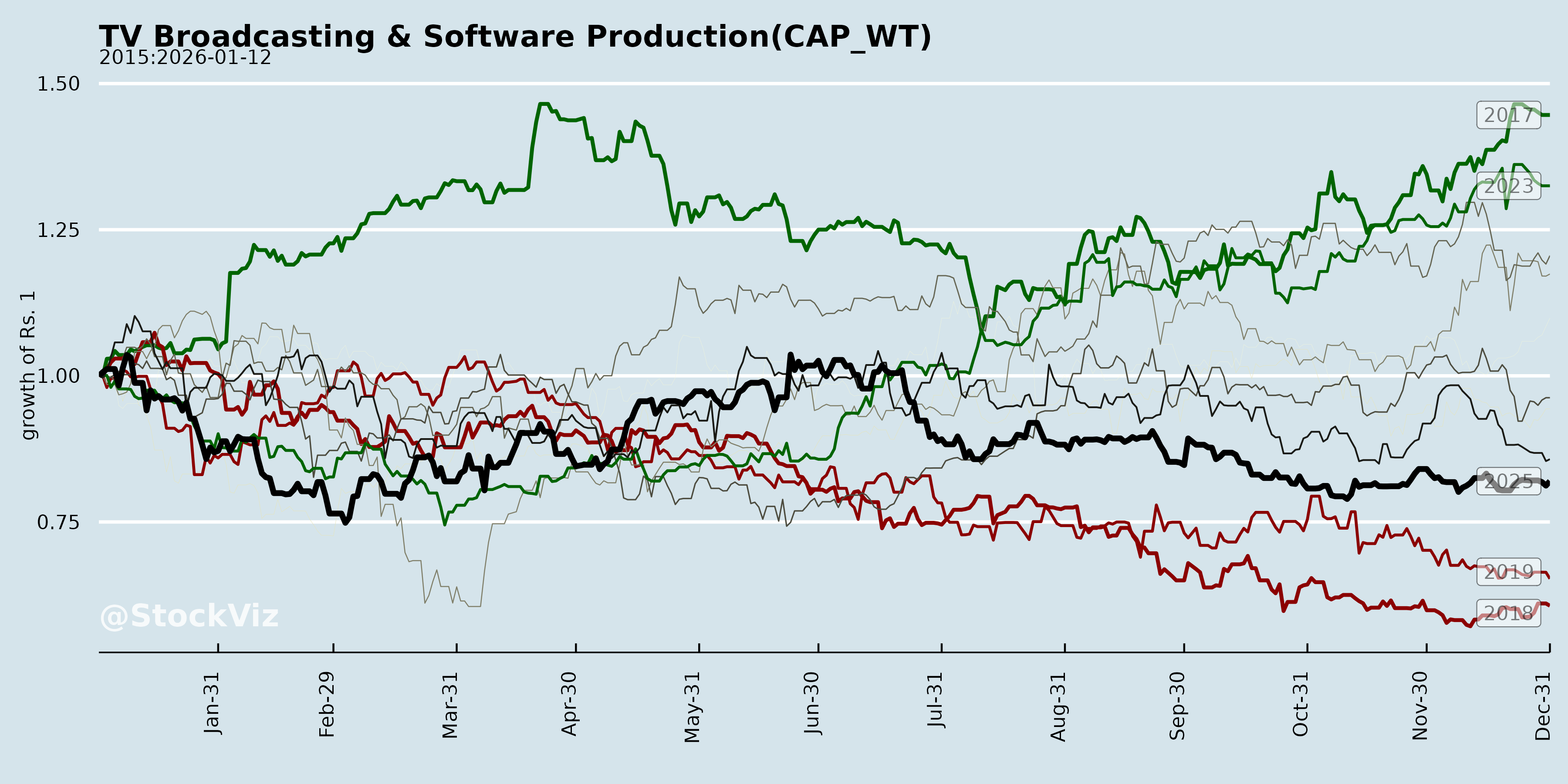

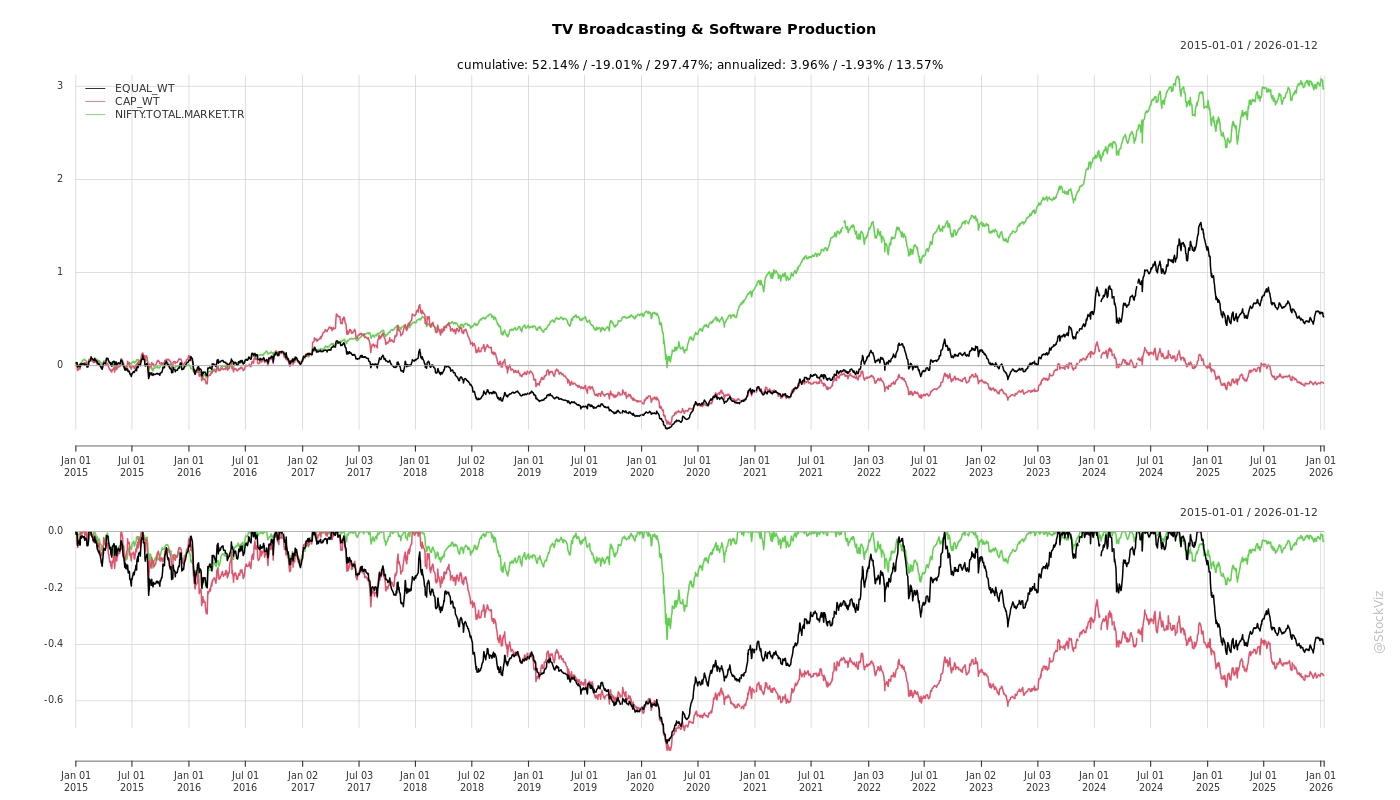

Cumulative Returns and Drawdowns

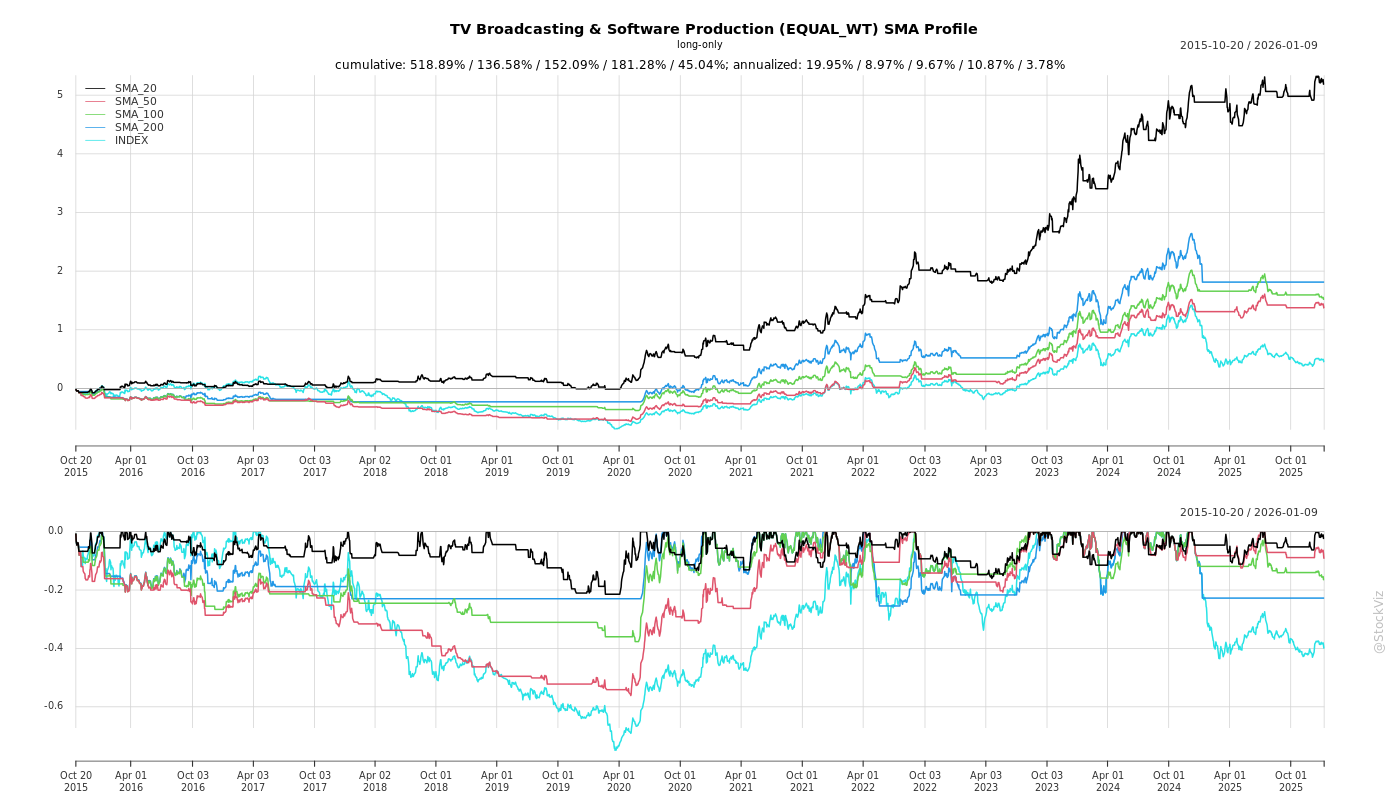

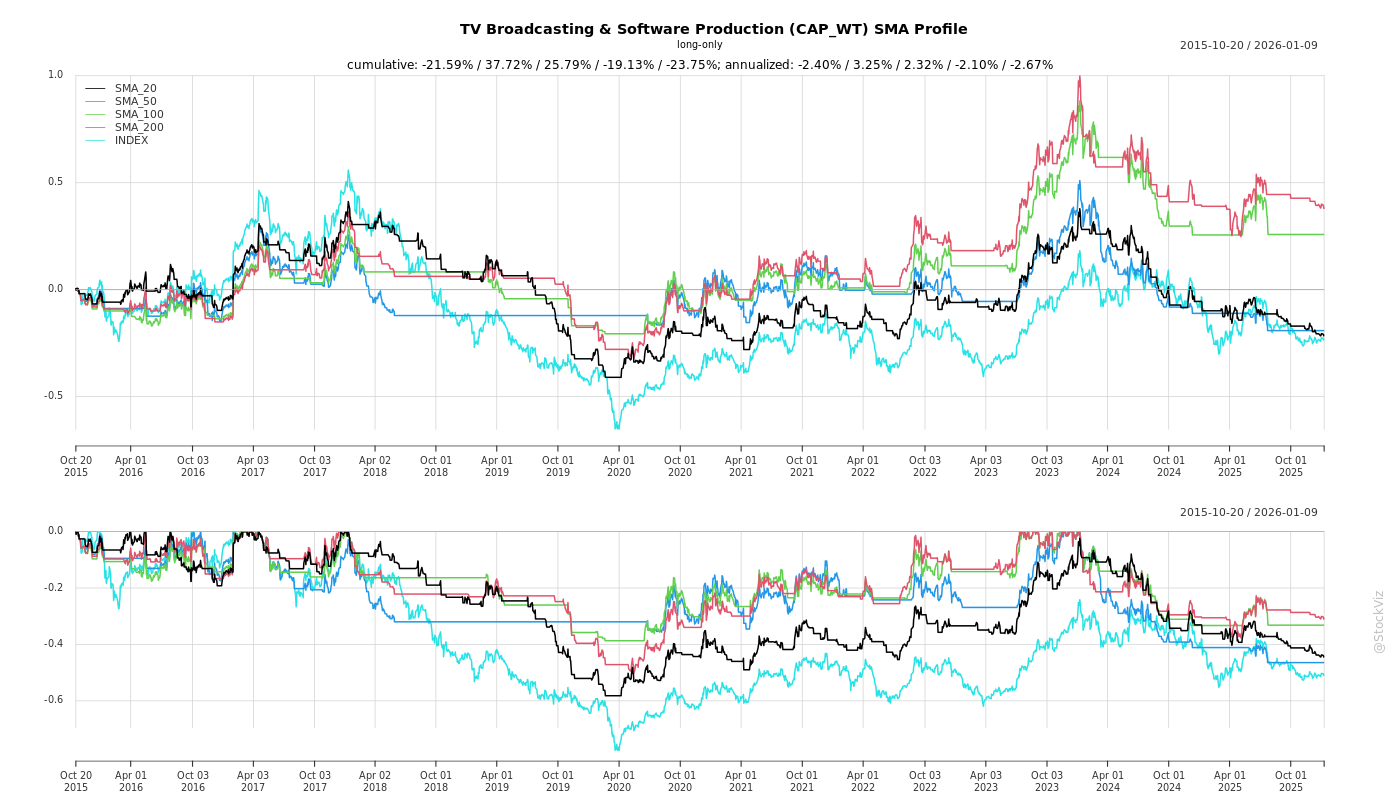

SMA Scenarios

Current Distance from SMA

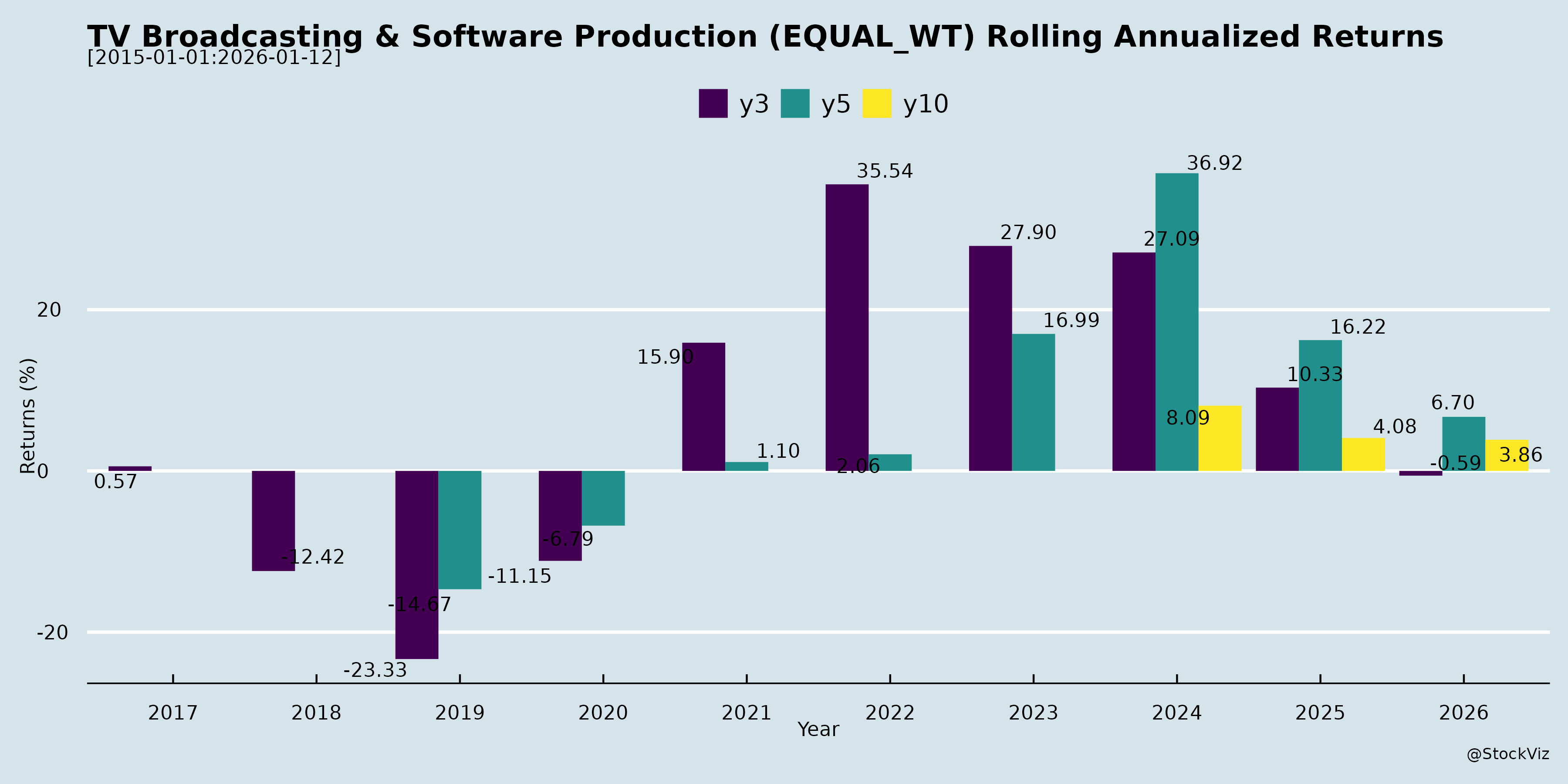

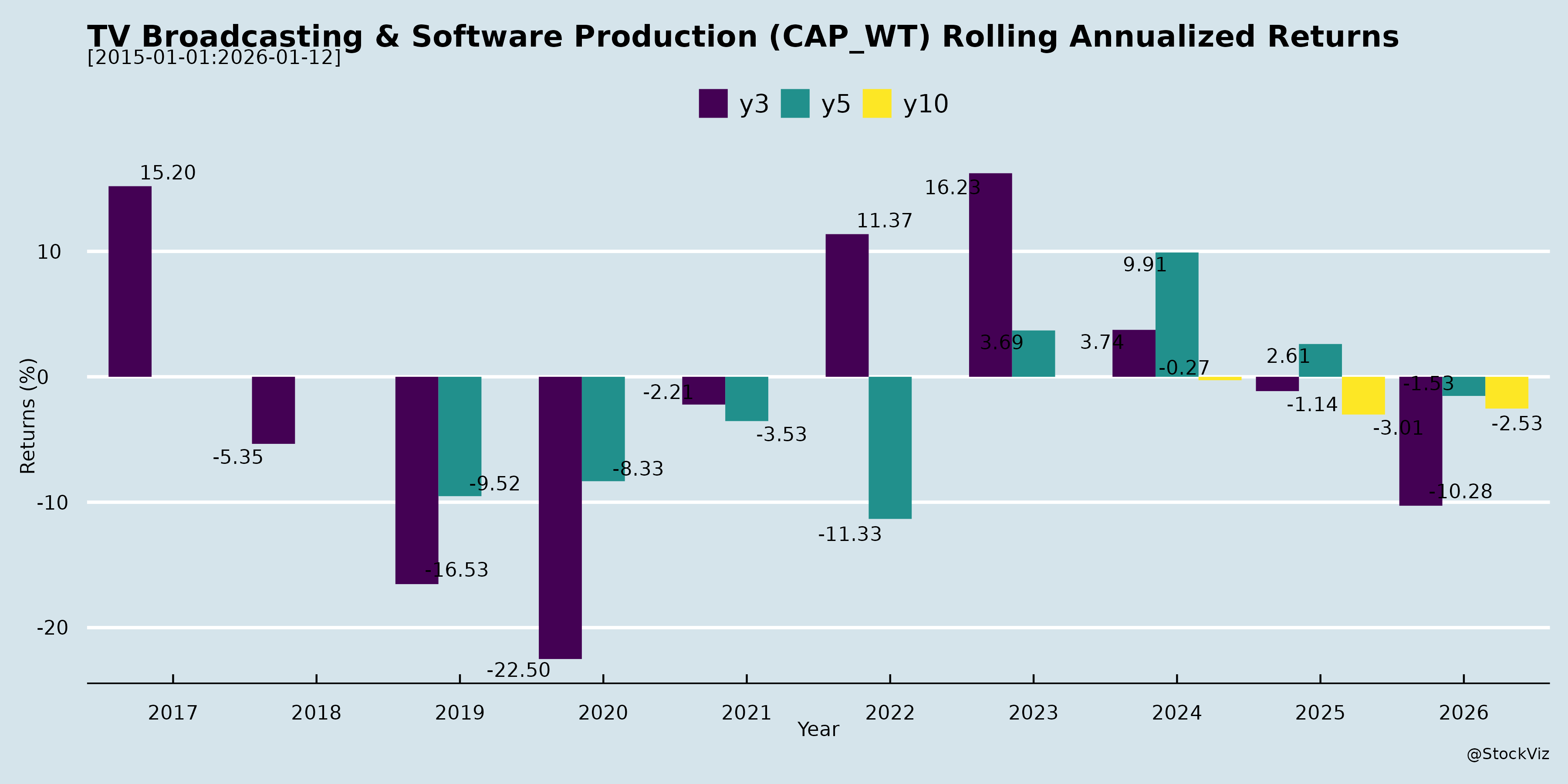

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-16

Based on the provided sources, the landscape for Indian media, entertainment, and telecommunications companies has evolved significantly, marked by emerging technological opportunities and demographic shifts, alongside persistent financial, regulatory, and legal challenges.

Here is a detailed breakdown of how these opportunities and challenges have evolved over time:

Evolving Opportunities

1. Demographic Growth and Market Expansion * Rising TV and Broadband Penetration: The industry is benefiting from India’s population growth and increasing per capita income, which is expanding the middle class and is expected to drive the number of television households to 200 million by 2028 [1-3]. Additionally, India has historically had one of the lowest fixed broadband penetration levels globally, presenting a massive runway for growth. The push for digital connectivity by the government and higher data usage for consumer and enterprise needs are accelerating this expansion [4, 5]. * Targeting Underserved Markets: Companies like GTPL Hathway have launched satellite-based Headend-In-The-Sky (HITS) platforms, such as “GTPL Infinity.” This technology allows them to bypass high infrastructure and delivery costs to seamlessly expand into rural, “cable-dark” areas, and hilly terrains where traditional cable expansion was previously unviable [6-8].

2. Technological Innovation and Bundling * Integrated Bundles: To combat cord-cutting, operators are successfully shifting toward converged services. Bundling Digital Cable TV with High-Speed Broadband, OTT platforms, and Cloud Gaming (e.g., GTPL Genie and GTPL Buzz) is enhancing customer retention and monetization [2, 9, 10]. * AI and International Expansion: Companies are leveraging technological trends for global growth. For example, Aqylon Nexus Limited (formerly Sri Adhikari Brothers Television Network) is expanding into the United Arab Emirates (UAE) to capitalize on the overwhelming market demand for its AI Technology Products and Services [11-13].

3. Strategic Consolidation and New Revenue Streams * Industry Consolidation: Increased compliance requirements and the cancellation of licenses for non-compliant Multi-System Operators (MSOs) have driven industry consolidation. This allows larger, organized players to acquire smaller regional operators, improving their scale, negotiation power, and cost efficiency [1, 4, 14]. * Content Monetization and Restructuring: Media companies are actively developing new sustainable revenue streams. Zee Entertainment, for instance, has generated significant revenue (over Rs. 8,019 lakhs in the Dec 2025 quarter) by licensing and monetizing its extensive content archives [15, 16]. NDTV has undertaken structural consolidation by merging four entities into one to simplify operations and has broadened its footprint into live entertainment with mega-concerts and the proposed acquisition of the “GoodTimes” channel [17-20]. * ESG Leadership: Emphasizing Environmental, Social, and Governance (ESG) practices is becoming a competitive advantage. Zee Entertainment recently ranked in the top 5% globally in the media and entertainment sector for its ESG performance, enhancing stakeholder trust [21-23].

Evolving Challenges

1. Severe Financial Distress and Solvency Risks * Negative Working Capital and NPAs: Several companies have faced severe financial instability. TV Vision Limited has suffered substantial continuous losses leading to a negative net worth, and defaults on bank loans have resulted in their accounts being classified as Non-Performing Assets (NPAs) by lenders [24-29]. Similarly, Zee Entertainment has reported significant accumulated losses and negative working capital, requiring aggressive cost rationalization and credit period extensions to survive [30, 31]. * Asset Impairment: Companies are struggling with assets that no longer generate returns. TV Vision Limited, for example, faces a strong indication of impairment on business and commercial rights valued at Rs. 2,719.61 Lakhs, as these assets have generated zero revenue [32-35]. * Investment Costs vs. Immediate Profits: The pressure to transform business models requires heavy capital expenditure. NDTV noted that while their revenue grew robustly, their bottom line was heavily impacted by the significant investments required to support their ongoing transformation and growth initiatives [36].

2. Regulatory and Legal Hurdles * Government Levies and AGR Dues: Telecommunication and broadband providers are locked in massive, ongoing legal battles with the Department of Telecommunications (DoT). The DoT has issued multi-billion rupee demands against companies like GTPL Hathway for license fees, arguing that revenue from pure internet services should be included in their Adjusted Gross Revenue (AGR). Though companies are actively defending against these demands in the Supreme Court and TDSAT, these contingent liabilities remain a major financial overhang [37-42]. * Investigations and Contractual Disputes: Zee Entertainment has faced intense scrutiny, including show-cause notices from SEBI and ongoing inspections by the Ministry of Corporate Affairs regarding alleged material irregularities and inter-corporate deposits [43, 44]. Additionally, Zee is entangled in a major arbitration dispute in the London Court of International Arbitration with Jiostar over the broadcasting rights for ICC global events, involving damage claims exceeding USD 1 billion [44]. * Changing Labor Laws: The government’s introduction of new unified Labour Codes requires companies across the board to re-evaluate their employee benefit liabilities and financial compliance, presenting a transitional administrative and financial burden [45-47].

In summary, while the industry features immense opportunities driven by digital transformation, rural expansion, and demographic shifts, companies must simultaneously navigate a minefield of massive legacy debts, regulatory disputes with the government, and the high costs associated with upgrading their business models.

What are the headwinds affecting this industry?

asof: 2026-04-16

The media, broadcasting, and cable television industry faces a multitude of headwinds, ranging from severe financial distress and shifting consumer behavior to complex regulatory and legal hurdles.

Regulatory and Legal Challenges A major headwind involves ongoing disputes with the Department of Telecommunications (DoT) regarding Adjusted Gross Revenue (AGR) and license fees [1-3]. The DoT has issued substantial demands to companies—sometimes amounting to billions of rupees—by attempting to include revenue generated from pure internet services and non-licensed cable television businesses in the calculation of license fees [1, 2, 4, 5]. Although operators and the All India Digital Cable Federation (AIDCF) have challenged these demands before the Telecom Disputes Settlement and Appellate Tribunal (TDSAT) and the Supreme Court, the litigation creates significant contingent liabilities and financial uncertainty [4-7].

Additionally, the industry is grappling with increased compliance burdens and regulatory scrutiny. The Ministry of Information & Broadcasting (MIB) has actively cancelled the registrations of non-compliant Multi System Operators (MSOs), forcing smaller players to consolidate [8]. Furthermore, the Government of India’s introduction of four unified Labour Codes—covering wages, social security, industrial relations, and occupational safety—has forced companies to reassess their employee benefit measurements, resulting in incremental financial liabilities [9-12]. Companies are also vulnerable to various legal litigations, including pre-institution mediation proceedings involving substantial claims for damages and penalties over alleged infringements [13].

Financial Distress and Debt Burdens Several players in the sector are experiencing severe financial instability and liquidity crises [14, 15]. Key financial headwinds include: * High Debt and Defaults: Companies have defaulted on bank loans, leading to their accounts being classified as Non-Performing Assets (NPAs) by lenders [16, 17]. * Coercive Recovery Actions: Secured lenders have recalled loans and initiated recovery proceedings through debt recovery tribunals [14, 18]. This has resulted in lenders taking symbolic possession of mortgaged properties used as collateral, invoking corporate guarantees, and seizing pledged shares [14, 18, 19]. * Insolvency Pressures: Some businesses have been pushed into the Corporate Insolvency Resolution Process (CIRP) [20]. To adhere to approved resolution plans and reduce massive financial debts, these companies are being forced to liquidate and sell off non-core assets, such as commercial real estate [21-23]. * Negative Net Worth: Mounting liabilities that substantially exceed current assets have resulted in massive accumulated losses and negative net worth for certain subsidiaries and parent companies [14, 19, 24, 25].

Operational and Market Pressures On the consumer and operational front, the industry faces the ongoing threat of “cord-cutting” as audiences increasingly shift toward digital and OTT (Over-The-Top) platforms [26]. To combat this trend and retain their subscriber base, Distribution Platform Operators (DPOs) are being forced to adapt by offering integrated bundles that combine Pay TV, broadband, and OTT services [26].

Furthermore, some media entities are suffering from an inability to successfully monetize their business and commercial rights [27, 28]. The failure to generate revenue from these content and broadcasting assets has led to strong indications of impairment, forcing auditors to recommend massive impairment losses that further overstate assets and understate net losses [27-30]. Companies are also struggling to manage daily operational costs, evidenced by outstanding, unpaid balances for carriage fees and other vendor expenses [31-33].

Macroeconomic and Extrinsic Risks Finally, forward-looking industry assessments highlight broad macroeconomic risks [34]. The sector remains highly sensitive to global and domestic industry downtrends, fluctuations in exchange rates, and rapid technological changes [34, 35]. Changes in tax laws, shifting political and economic environments, and labor relations continue to threaten cash flow projections, investment income, and overall business stability [34].

What are the key things to understand about this industry?

asof: 2026-04-16

Here are the key things to understand about the digital cable TV and broadband industry, characterized by strong growth, market consolidation, and an expanding consumer base:

1. Reaching Global Scale and Massive Market Expansion India’s television market is rapidly expanding to a global scale, positioned to surpass the UK in 2025 and Japan in 2028, which will make it the fourth-largest traditional TV market in the world [1]. Indian households are projected to grow from 332 million in 2025 to 345 million by 2028, and the number of television households is expected to cross 200 million by 2028 [2, 3]. This surge is largely fueled by an expanding middle class, which is anticipated to reach 715 million people by 2030-31, allowing many more families to afford television sets [1, 3]. Additionally, there is a huge runway for natural growth, as over 120 million of India’s 320+ million households currently do not own a television [4]. In total, the targetable market encompasses approximately 200 million households for Cable TV and 150 million households for Broadband [1].

2. Strong Viewership and Changing Consumer Habits Traditional TV retains a powerful mass appeal, with the industry projected to see 5.3% per annum growth from 2024 to 2029 [2]. Viewership trends are highly robust, featuring an average weekly TV reach of 745 million and an average daily watch time of 3 hours and 45 minutes [3]. Notably, the 15 to 50 age demographic drives 58% of the total viewership [3].

To combat cord-cutting, operators are capitalizing on convergence; integrated bundles that combine Pay TV, IPTV, broadband, and OTT services are gaining significant momentum [3]. Furthermore, the industry is witnessing a shift of Direct-to-Home (DTH) viewers back to cable TV, as post-digitization broadcast quality and the number of channels offered are now on par across both platforms [4].

3. Industry Consolidation Favoring Organized Players The market is undergoing significant consolidation, which is driving scale, negotiation power, and cost efficiencies for larger operators [2]. The number of Multi System Operators (MSOs) operating in India plummeted from 1,702 in December 2020 to just 818 by September 2025 [2]. This dynamic heavily favors organized players, as stricter compliance requirements and the cancellation of licenses for non-compliant MSOs by the Ministry of Information and Broadcasting force unorganized and smaller players out of the market [4, 5].

4. The Broadband Boom and Low Penetration Opportunity India currently has one of the lowest fixed broadband penetration levels globally. As of February 2026, there were 46.02 million wired subscribers, representing only a ~14.5% penetration rate across the country’s households [5]. However, this represents a massive growth opportunity. The India Wired Broadband Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.43% between FY23 and FY2028, with the Fiber to the Home (FTTH) segment specifically expected to grow at a 17.62% CAGR [6].

This rapid broadband growth is being driven by several key factors [6]: * Increasing internet usage for both enterprise and consumer needs. * Higher data consumption due to the increased adoption of Social Media and OTT platforms. * A strong push for digital connectivity by the Government of India. * The growing necessity of uninterrupted broadband services in residential homes.

What are the tailwinds affecting this industry?

asof: 2026-04-16

Favorable Demographic and Economic Shifts * Growing Middle Class and Rising Incomes: India’s per capita income is expected to increase from US$2,820 in 2025 to US$3,640 by 2028, driving the middle class to an estimated 715 million people by 2030-31 [1]. This expanding middle class acts as a major catalyst for TV penetration, enabling more households to purchase television sets [1, 2]. * Household Growth: The total number of Indian households is projected to rise from 332 million in 2025 to 345 million by 2028, naturally expanding the addressable market [1].

Vast Untapped Market for Traditional TV * Large “TV-Dark” Population: Out of over 320 million Indian households, more than 120 million currently do not own a television set, presenting a massive runway for natural market growth [3]. Total television households are expected to cross 200 million by 2028 [1]. * Global Scaling: This rapid expansion positions India to surpass the UK in 2025 and Japan in 2028, making it the fourth-largest traditional television market in the world [2]. * Consumer Shift from DTH to Cable: There is a notable migration of Direct-to-Home (DTH) viewers back to cable TV, as post-digitization cable services now match DTH in terms of broadcast quality and the number of channels offered [3]. * Bundling Strategies: Operators are successfully combating cord-cutting by offering integrated bundles that combine Digital Cable TV, Broadband, and OTT services [1]. New technologies like Headend-In-The-Sky (HITS) are also opening up previously unviable, cable-dark, and rural areas by lowering signal delivery costs [4, 5].

Massive Broadband Expansion Opportunities * Low Current Penetration: India suffers from one of the lowest fixed broadband penetration levels globally, with only 46.02 million wired subscribers as of February 2026, representing just ~14.5% penetration across ~320 million households [6]. This leaves a targetable market of approximately 150 million households [2]. * Surging Data Demand: Growth is being accelerated by the increasing necessity of uninterrupted home internet for both consumer and enterprise needs, fueled by higher data usage from OTT and social media adoption [7]. * Government Initiatives: State and central government pushes for digital connectivity across India are directly driving broadband expansion, particularly in rural markets [7, 8]. * Strong Projected Growth Rates: The Indian Wired Broadband Market is expected to register a Compound Annual Growth Rate (CAGR) of 15.43% from FY2023 to FY2028, with the Fiber to the Home (FTTH) segment expected to grow even faster at a 17.62% CAGR [7].

Industry Consolidation and Regulatory Environment * Market Consolidation: The industry is heavily shifting in favor of organized players [3]. Increased regulatory compliances and the cancellation of licenses by the Ministry of Information and Broadcasting (MIB) for non-compliant Multi System Operators (MSOs) are forcing unorganized players out of the market [3, 6]. * Inorganic Growth: This consolidation provides large, organized operators with significant opportunities to acquire and absorb smaller regional players, ultimately driving scale, better negotiation power, and cost efficiencies [6, 9].

What is the general outlook of this industry?

asof: 2026-04-16

The general outlook for the cable television and broadband industry is highly positive, characterized by strong growth projections, an expanding target market, and strategic industry consolidation.

Television and Cable TV (CATV) Market: * Strong Mass Appeal: Traditional TV retains a strong mass appeal, with the industry expected to grow at a rate of 5.3% per annum between 2024 and 2029 [1]. Furthermore, India’s television households are projected to cross 200 million by 2028 [2]. * Global Scale: This rapid expansion positions India to surpass the UK in 2025 and Japan in 2028, making it the fourth-largest traditional TV market globally [3]. * Expanding Middle Class and “TV Dark” Households: Growth is largely catalyzed by India’s expanding middle class, which is expected to reach 715 million people by 2030-31 alongside rising per capita incomes, enabling more households to afford televisions [1, 2]. There is a massive runway for natural growth, as over 120 million of India’s 320+ million households still do not own a television set [4]. * Stable Viewership: The average weekly TV reach remains stable at approximately 745 million viewers, with audiences spending an average of 3 hours and 45 minutes per day watching TV [2]. * Shift from DTH to Cable: Cable TV is benefiting from a shift of Direct-to-Home (DTH) viewers, as the quality of broadcasts and the number of channels offered have become equally competitive following digitization [4].

Broadband Market: * Low Penetration Creating Opportunity: India currently has one of the lowest fixed broadband penetration levels globally, sitting at around 14.5% (approx. 46.02 million wired subscribers across 320 million households) as of February 2026 [5]. This leaves a massive targetable market of approximately 150 million households [4]. * High CAGR Projections: The Indian wired broadband market, which stood at USD 605.37 million in FY2023, is expected to register a Compound Annual Growth Rate (CAGR) of 15.43% from FY2023 to FY2028 [6]. The Fiber to the Home (FTTH) segment is projected to grow even faster at a CAGR of 17.62% during the same period [6]. * Key Growth Drivers: Broadband growth is being fueled by increasing internet usage for both consumer and enterprise needs, higher data consumption driven by OTT and social media adoption, the necessity of uninterrupted home broadband, and the Indian government’s heavy push for digital connectivity [6].

Emerging Industry Trends: * Service Bundling: To combat “cord-cutting,” Distribution Platform Operators (DPOs) are successfully gaining momentum by offering integrated bundles that combine traditional Pay TV, IPTV, broadband, and OTT services [2]. * Market Consolidation: The industry is experiencing consolidation in favor of organized, larger players, which helps drive scale, negotiation power, and cost efficiency [1, 4]. This consolidation is partly triggered by increased compliance requirements and the cancellation of licenses for non-compliant Multi-System Operators (MSOs) [7].

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.