Pharmaceuticals

Industry Metrics

May 8, 2026

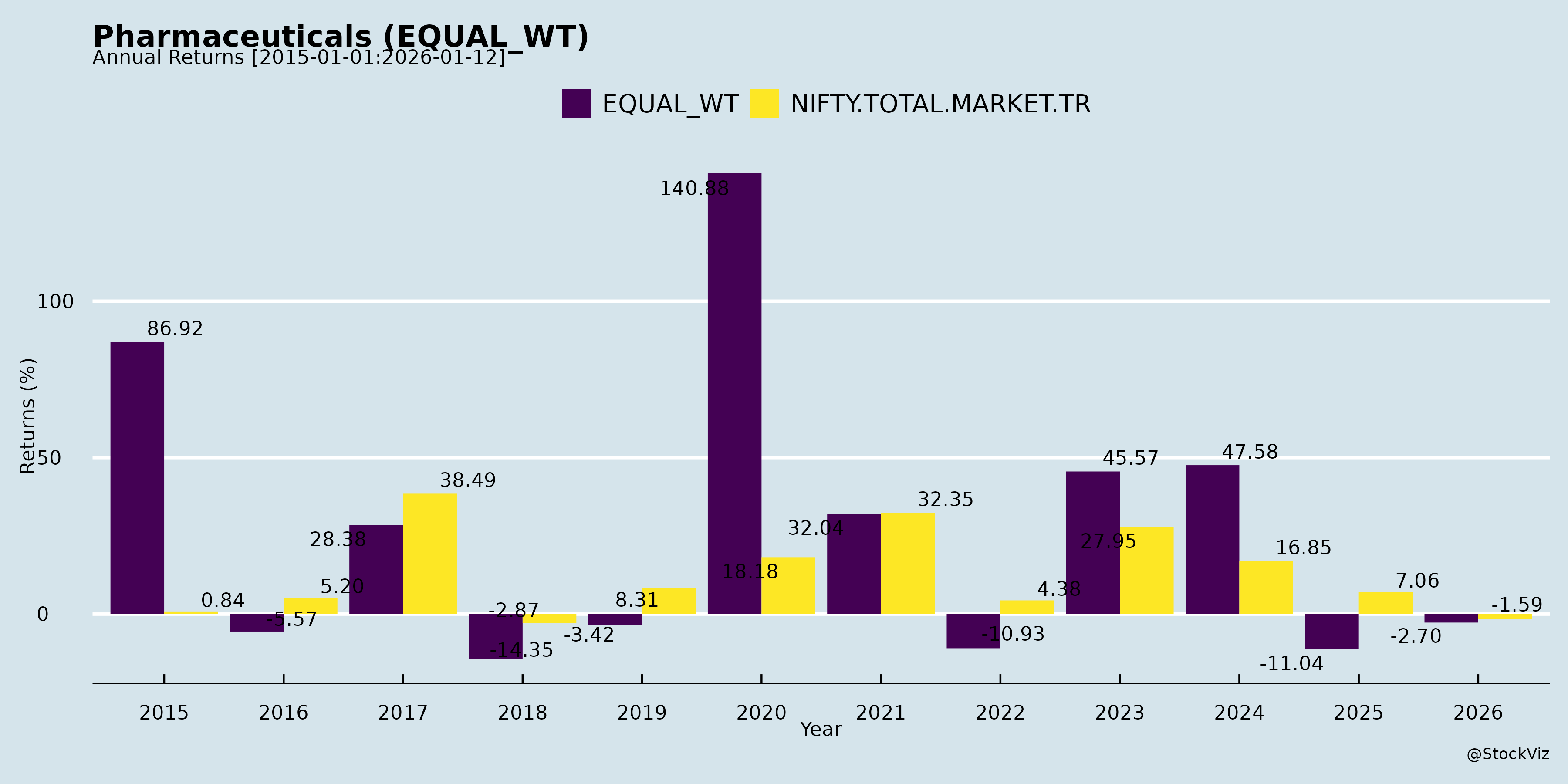

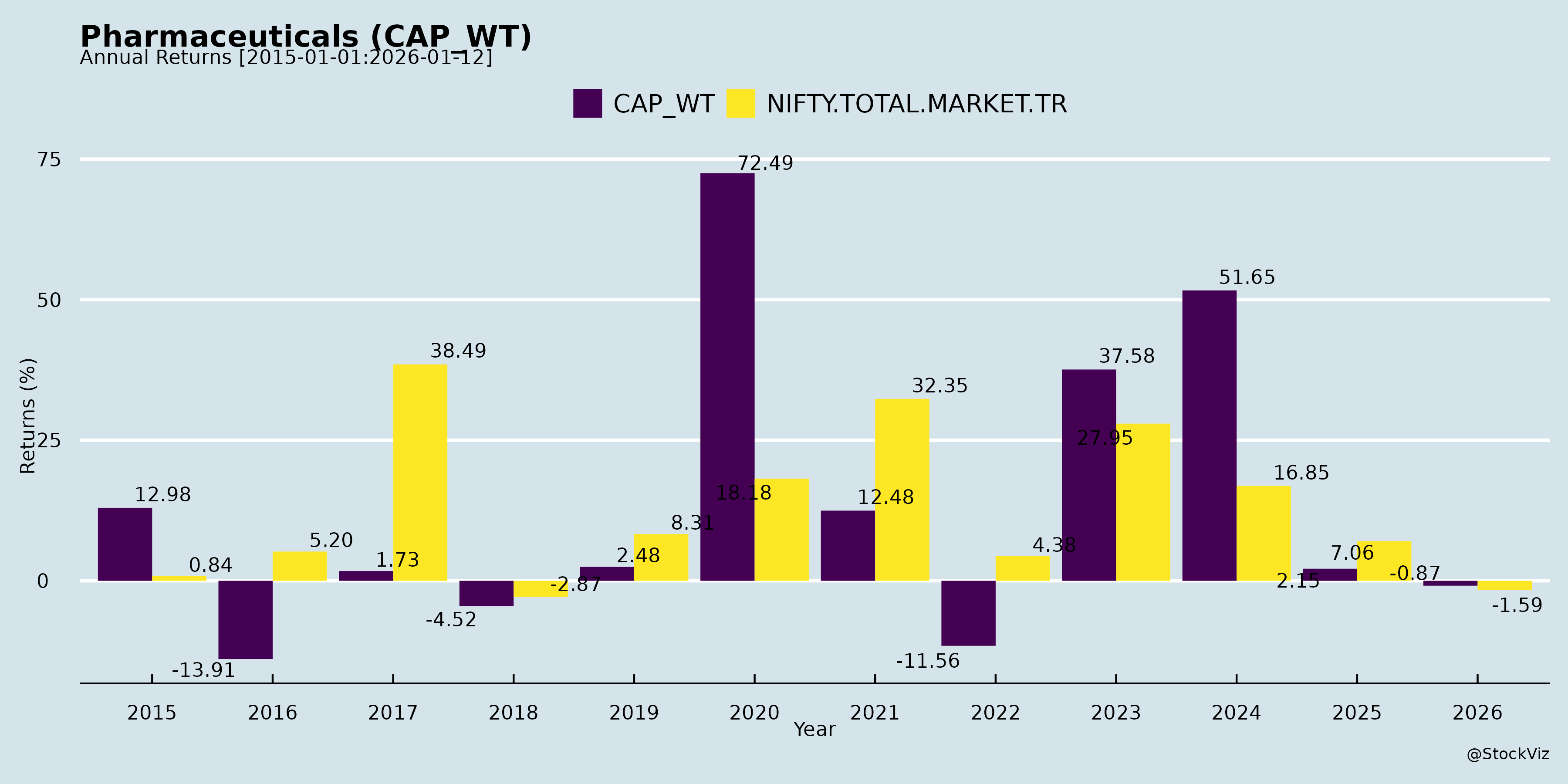

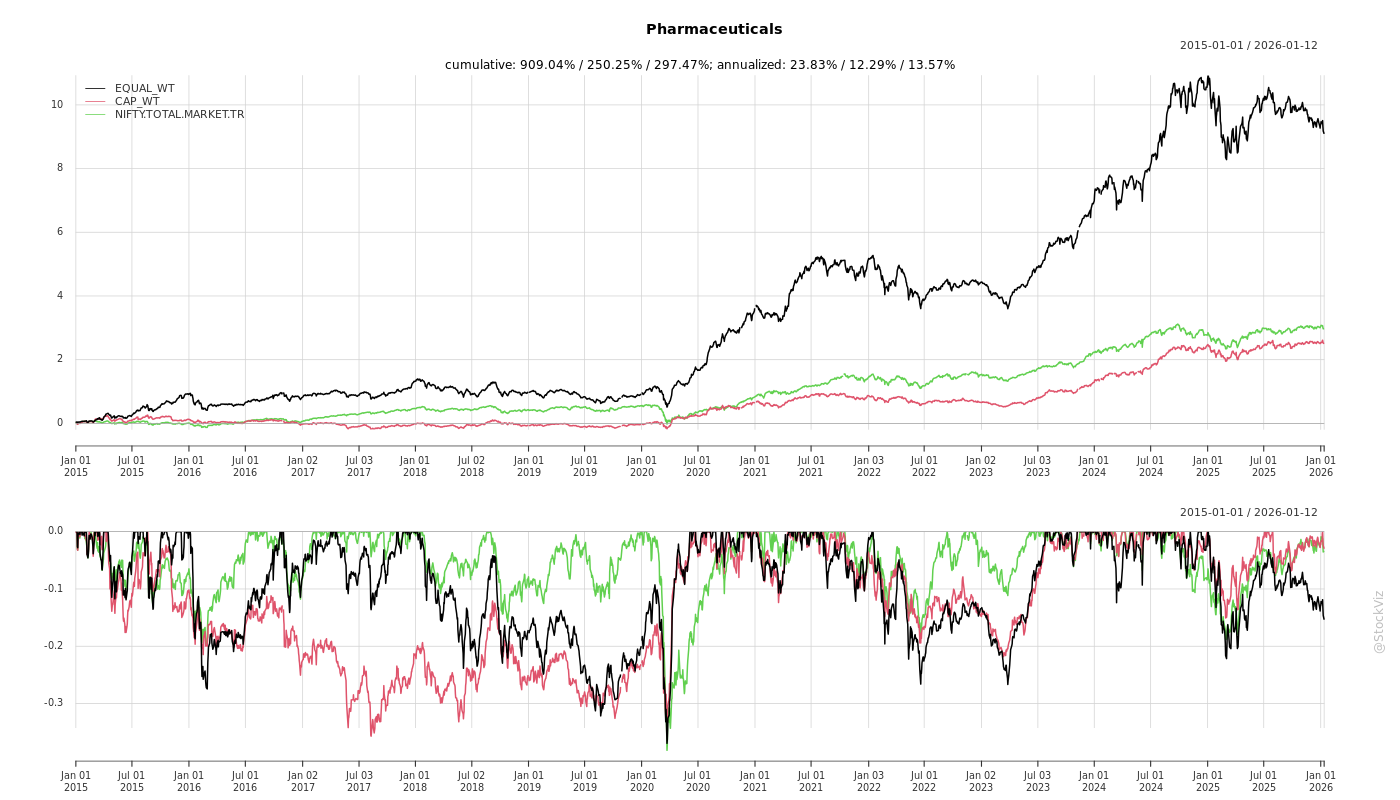

Annual Returns

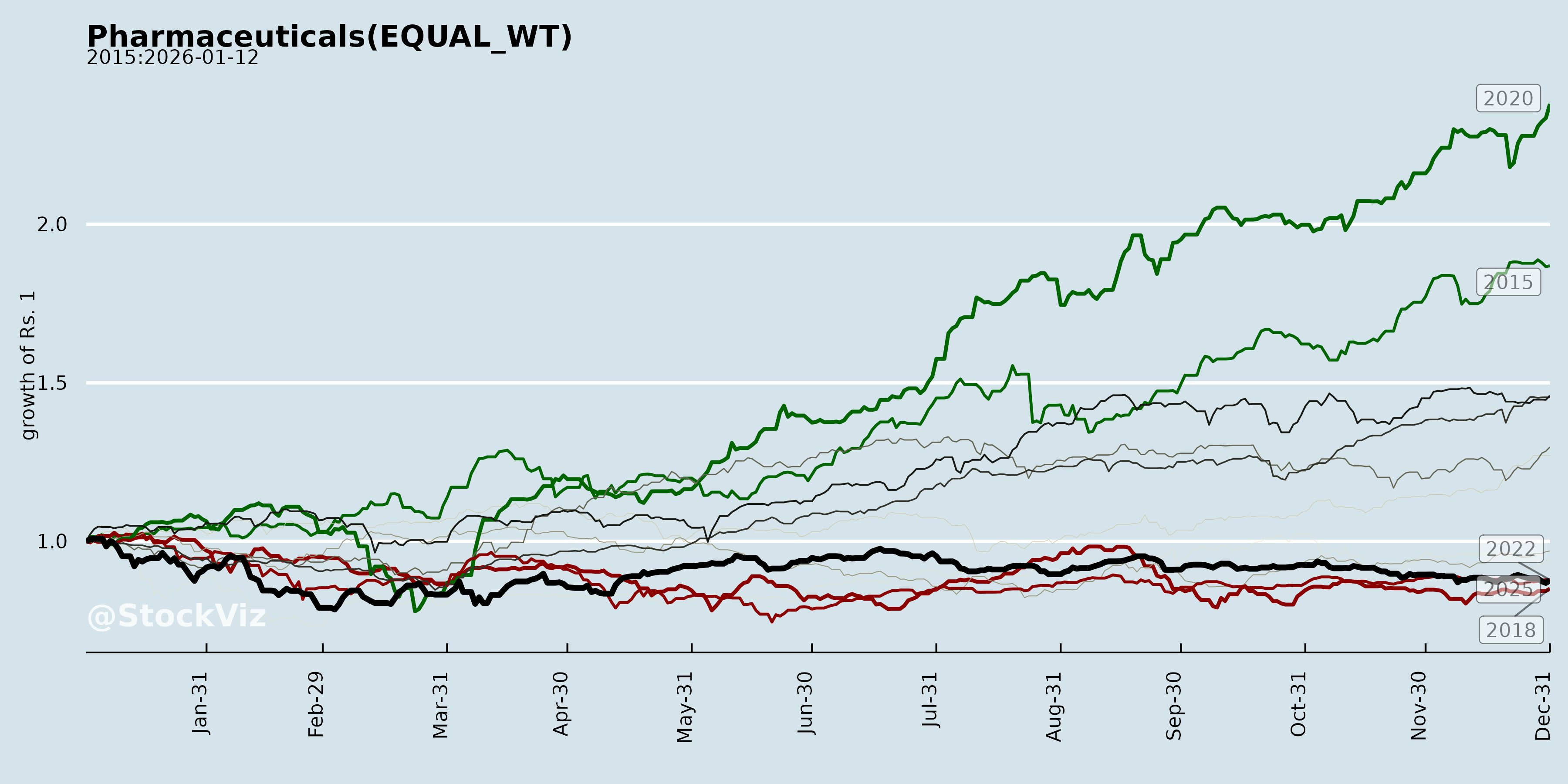

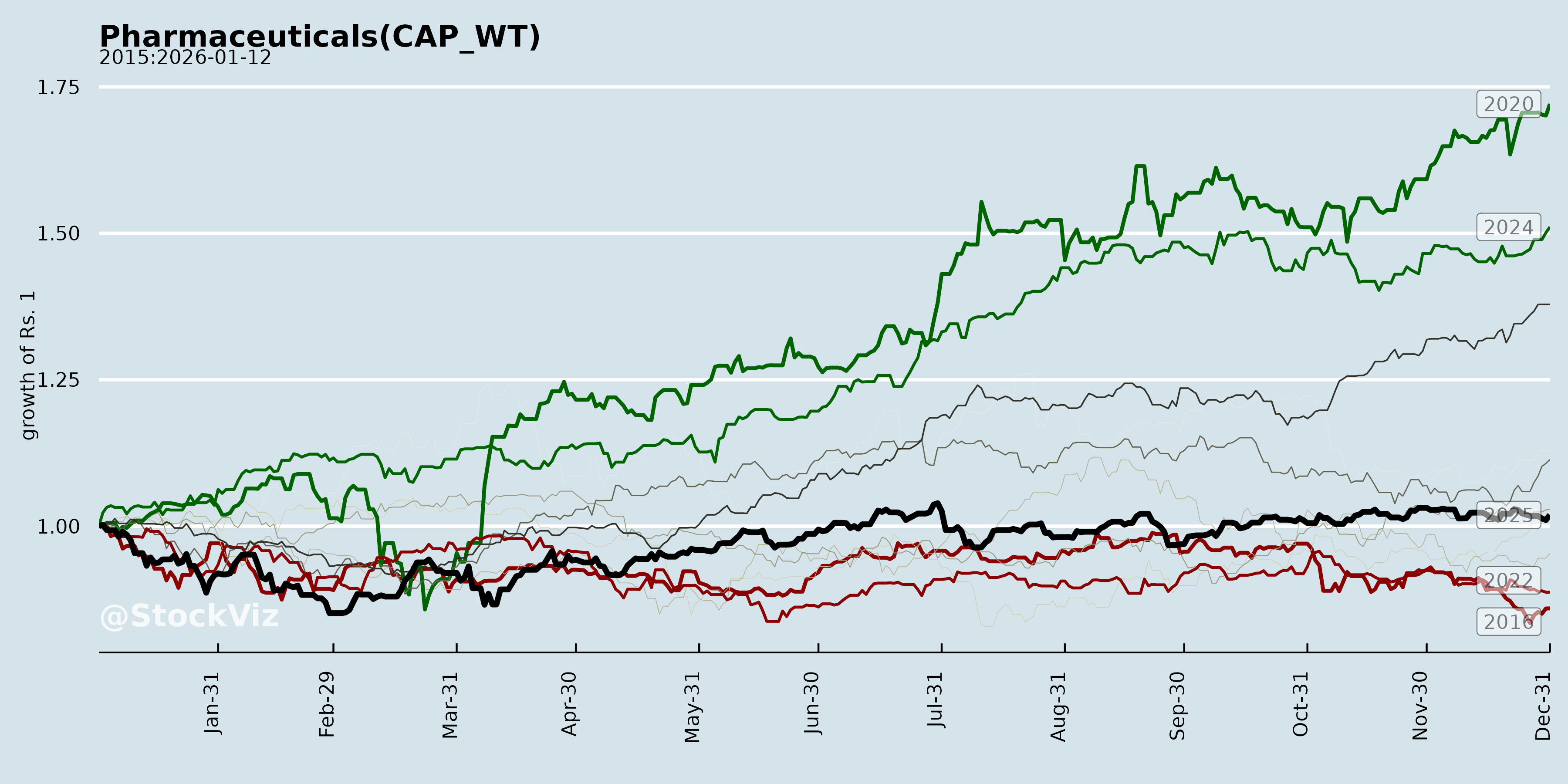

Cumulative Returns and Drawdowns

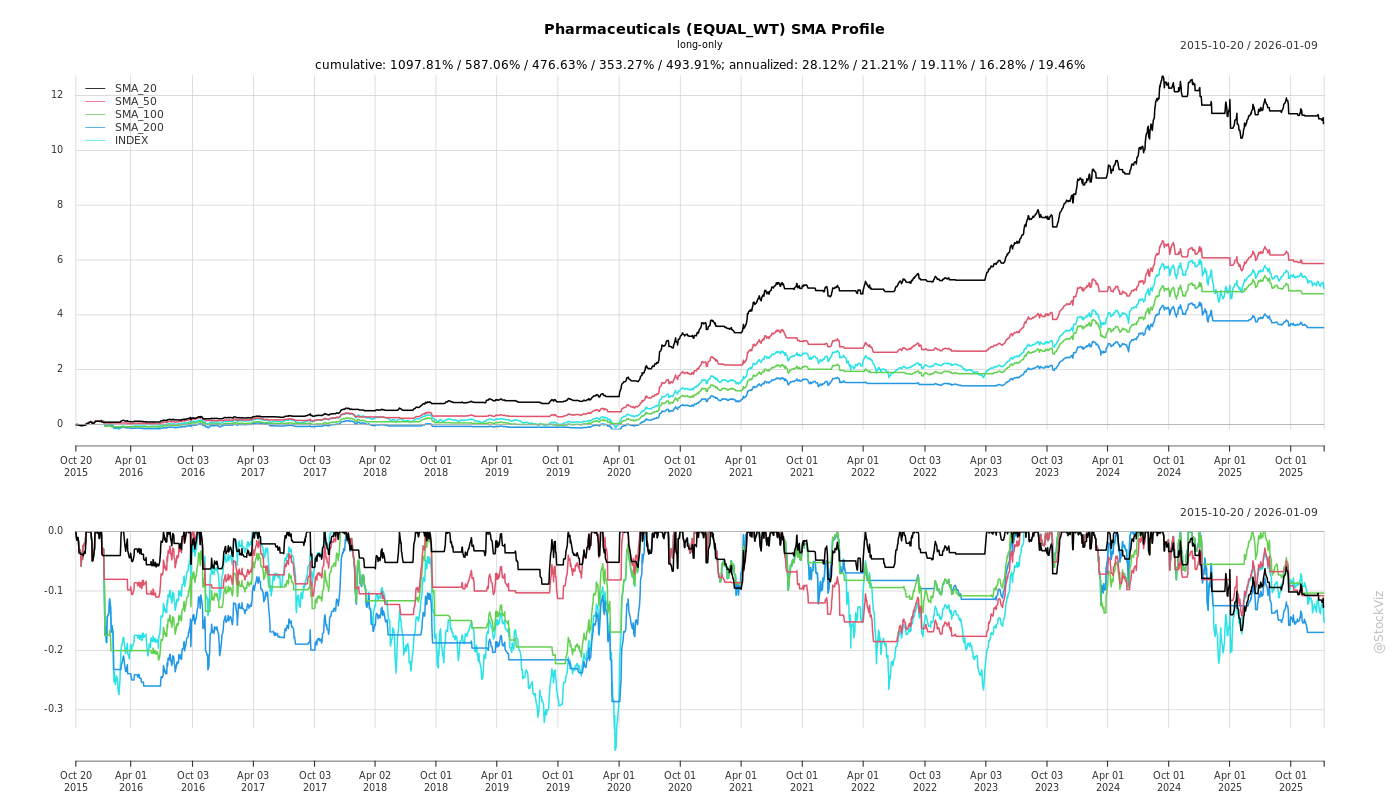

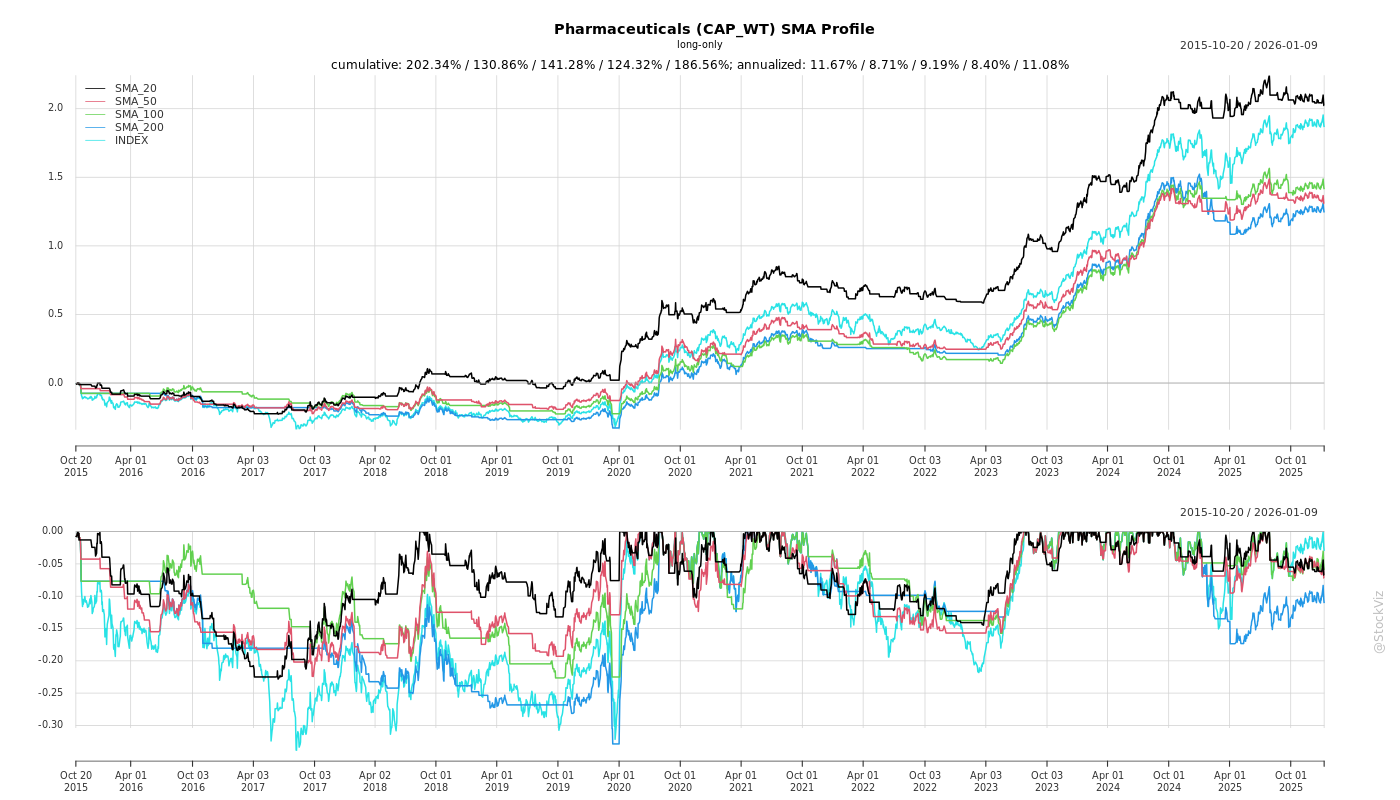

SMA Scenarios

Current Distance from SMA

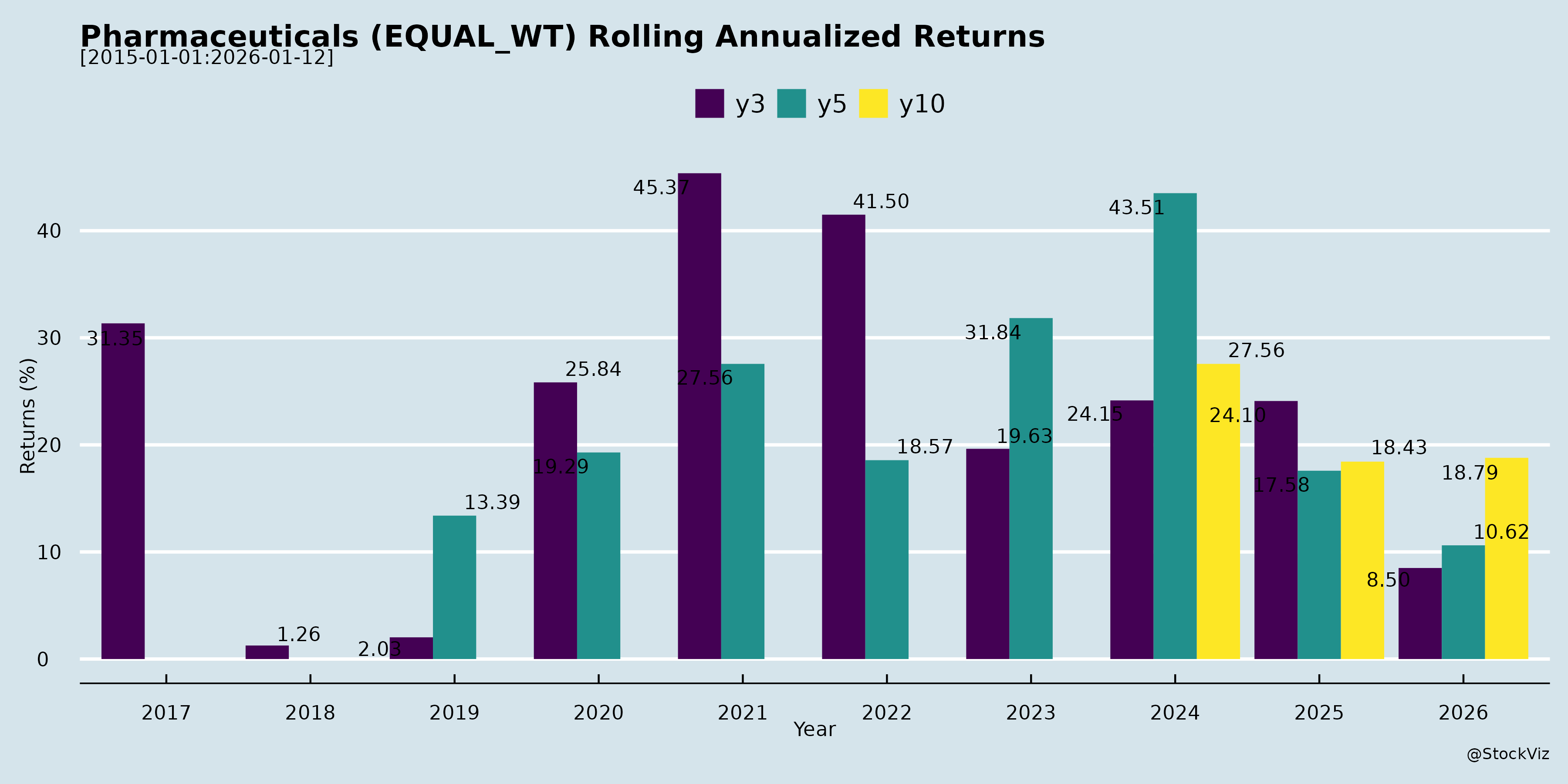

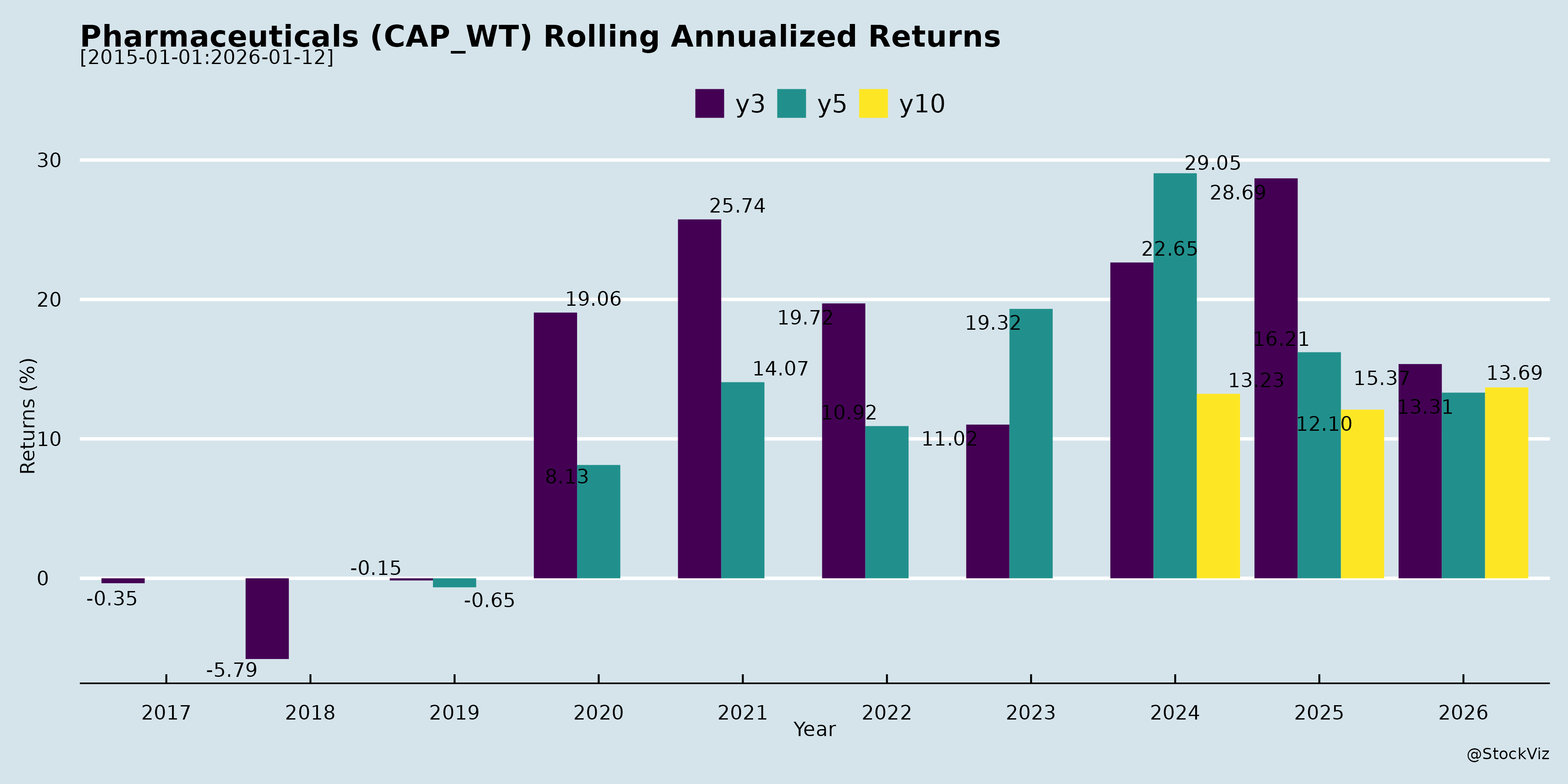

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-14

Over time, the pharmaceutical and healthcare industry has undergone a significant transformation, marked by a dynamic interplay of evolving operational challenges and emerging strategic opportunities. Companies are actively shifting their business models from traditional generic manufacturing to high-value, research-driven, and specialized segments to navigate a complex global landscape.

Here is a detailed breakdown of how challenges and opportunities have evolved:

The Evolution of Industry Challenges

1. Severe Pricing Pressures and Chinese Overcapacity A dominant challenge over recent years has been the intense pricing pressure across global markets, primarily driven by structural overcapacity and aggressive pricing from China [1-4]. For instance, the global market for base Active Pharmaceutical Ingredients (APIs) like ibuprofen and generic antibiotics has seen severe margin depression due to excess capacity and newer technologies driving down realizations [5-9]. Indian manufacturers have found themselves struggling to compete on cost with massive Chinese facilities (e.g., 200 KL fermenters compared to 60 KL in India), which have significantly lowered their production costs and market prices [10-12].

2. Supply Chain Vulnerabilities and Geopolitical Tariffs Evolving trade policies and geopolitical uncertainties have introduced high volatility into supply chains and procurement decisions [1, 3, 13]. For example, earlier U.S. trade tariffs on items like HPMC capsules created significant short-term headwinds and deferred customer procurement decisions [14-18]. Furthermore, the industry’s historical reliance on China for basic chemicals and intermediates has exposed companies to supply chain risks, prompting an urgent need for self-sufficiency and backward integration [19-23].

3. Complex Technical and Scale-Up Hurdles As companies attempt to modernize and scale their manufacturing, they face steep technical hurdles. Scaling up complex processes—such as moving from 10 KL pilot fermenters to 60 KL commercial fermenters—has frequently resulted in unexpected drops in conversion ratios and yields [24-26]. Furthermore, moving into novel areas like Antibody-Drug Conjugates (ADCs) and Radiopharmaceuticals requires massive upfront capital expenditures, highly specialized containment systems (e.g., OEB 5 certification), complex isotope handling, and long gestation periods of 2-3 years [27-30].

4. Stringent Regulatory and Compliance Frameworks The regulatory landscape has become increasingly rigorous. Companies have had to pivot from simple manufacturing to maintaining a steady state of global compliance to overcome regulatory delays and U.S. FDA remediation shocks [14, 31-34]. Navigating these stringent regulations involves long tech-transfer timelines (up to 24 months), high switching costs, and complex care coordination requirements, establishing massive entry barriers for new players [28, 35-37].

The Evolution of Strategic Opportunities

1. Pivot to Specialty, Novel, and Complex Therapeutics To escape the commoditization of basic generics, companies are aggressively pivoting towards high-value, complex therapeutic areas such as Oncology, CNS, Anti-diabetics (GLP-1s), and Radiopharmaceuticals [32, 34, 38-41]. The U.S. radiopharmaceutical market alone is growing at a 20% CAGR [27]. There is also a major shift toward developing novel, proprietary drugs. For instance, massive R&D investments are yielding breakthroughs like ZAYNICH and Miqnaf—novel antibiotics designed to combat multi-drug-resistant infections, representing multi-billion dollar addressable markets [42-47].

2. The CDMO Boom and “China Plus One” Strategy The Contract Development and Manufacturing Organization (CDMO) landscape is experiencing a structural shift. Driven by the U.S. Biosecure Act and a desire for supply chain resiliency, global innovators are actively diversifying their outsourcing away from China and looking towards quality-focused Indian and on-shore manufacturers [48-52]. This has led to a sharp uptick in early-stage Requests for Proposals (RFPs) for high-value small molecules, advanced intermediates, oligonucleotides, and customized payloads [51-55].

3. Explosive Growth in Animal Health & Consumer Healthcare (OTC) Companies are unlocking entirely new growth engines outside of traditional human prescriptions: * Animal Health: The companion animal market is emerging as one of the most attractive long-term opportunities. With rising pet ownership and generic penetration currently sitting at a mere 15% (compared to 85-90% in human health), there is massive headroom for growth and CDMO partnerships [56-63]. * Consumer Healthcare: There is a significant behavioural shift towards self-care, preventive health, and wellness. Increased disposable income and digital awareness are driving massive demand for Over-The-Counter (OTC) products, medical devices (like glucometers and BP monitors), and Vitamin, Mineral, and Supplement (VMS) portfolios [64-69].

4. Backward Integration and Operational Excellence To protect margins and ensure supply reliability, the industry is heavily focused on end-to-end backward integration [70-74]. By manufacturing their own intermediates and APIs for finished dosages, companies are structurally insulating themselves from external price shocks. Concurrently, businesses are adopting green chemistry, continuous flow chemistry, and robotic automation (like automated visual inspection and pre-filled syringe lines) to drastically improve yields, safety, and cost-efficiency [75-81].

5. Geographic Expansion into Emerging Markets Instead of relying solely on the highly competitive U.S. generics market, there is a renewed focus on deep penetration into emerging, semi-regulated, and non-English speaking markets (e.g., Latin America, Africa, Southeast Asia, and CIS countries) [70, 82-86]. These regions value affordability and long-term commitment, offering companies an end-to-end business model with highly favorable returns on capital [83, 84, 87].

What are the headwinds affecting this industry?

asof: 2026-04-14

The pharmaceutical and chemical manufacturing industries are currently navigating a highly dynamic and challenging environment. The key headwinds affecting the industry span across structural overcapacities, severe pricing pressures, geopolitical instability, and regulatory hurdles:

1. Structural Overcapacity and Chinese Dumping A significant drag on the industry is global oversupply and structural overcapacity. This is particularly evident in the Global Crop Protection segment and in specific commodity APIs like ibuprofen, where capacities built out of India and China far exceed current market demand [1], [2], [3], [4]. Furthermore, a weak domestic economy in China has led Chinese manufacturers to aggressively dump huge accumulated inventories into international markets at very low prices [5], [6], [7]. This oversupply significantly depresses profitability and makes it difficult for other global players to recover costs [4], [8].

2. Severe Pricing Pressures and Margin Erosion The influx of cheap generic alternatives and intense competition has triggered a race to the bottom for pricing across multiple product lines and geographies: * Antibiotics and APIs: The global antibiotics market is experiencing severe stress, with one company reporting a 12% price erosion and a 10% quantity erosion over a 9-month period, reflecting broad industry pressure rather than product-specific issues [9], [10]. In the API space, average selling prices for some companies have plummeted by as much as 24% over the last two years [11]. * Generic Prescription (Rx) Markets: Competitive intensity is exceptionally high in regulated markets like the UK and the US [12], [13]. In the UK market, for example, massive inventory liquidations led to a “blood bath on pricing,” forcing many generic products to be sold at a loss [14], [15].

3. Geopolitical Instability and Macroeconomic Volatility Ongoing geopolitical conflicts and sanctions have created deep uncertainties in significant export markets. For instance, the war and resulting sanctions have severely disrupted sales into large, historically reliable markets like Russia, the CIS region, Iran, Egypt, and Bangladesh [16], [17], [18].

4. Evolving Trade Policies and Tariffs Volatile trade policies are causing distributors and customers to delay procurement and investment decisions [2], [19]. * US Tariffs: The looming threat or implementation of US tariffs on pharmaceutical and nutraceutical imports has caused geopolitical uncertainty, leading US distributors to hold off on new orders or rely on existing inventories while waiting for clarity [20], [21], [22]. * Chinese Export Rebate Withdrawals: China’s decision to withdraw export tax rebates on certain basic chemicals and raw materials (such as fluorspar and caffeine salts) is expected to increase procurement costs and introduce selective pricing pressures on the input side for Indian pharmaceutical and agrochemical manufacturers [23], [24], [25], [26].

5. Regulatory Hurdles and Compliance Costs The industry remains highly sensitive to regulatory actions. Shifting customer offtake patterns and sales deferments have occurred in the wake of stringent US FDA audits, Official Action Indicated (OAI) statuses, and warning letters [27], [28], [29]. The time and resources required to execute remediation measures and regain regulatory compliance stall growth and delay supply resumptions [30], [31], [29].

6. Operational Constraints and Input Cost Fluctuations * Fuel and Energy Costs: Companies are facing unexpected spikes in fuel costs. For example, as more manufacturers shift toward sustainable fuels like husk to reduce their carbon footprint, the increased demand—coupled with weather disruptions—has caused significant fluctuations and spikes in energy costs, directly impacting EBITDA margins [32], [33], [34]. * Scale-up and Manufacturing Challenges: Firms expanding into complex manufacturing, such as large-scale fermentation for APIs, are encountering severe technical hurdles. Scaling up production (e.g., from 10 KL to 60 KL batches) has resulted in unexpected drops in conversion ratios and yields, delaying commercialization and dragging down profitability [35], [36]. Additionally, structural supply shortages in specific areas like SPECT products have temporarily constrained revenues for some players [37].

What are the key things to understand about this industry?

asof: 2026-04-14

The pharmaceutical industry is structurally complex and operates across several distinct verticals, primarily divided into Active Pharmaceutical Ingredients (APIs), which are the core active drugs or raw materials, and Formulations, which are the finished dosage forms such as tablets, capsules, injectables, and sprays [1-4]. Many companies also operate dedicated Contract Development and Manufacturing Organizations (CDMOs) or Contract Research and Development Manufacturing Organizations (CRDMOs) to provide specialized, outsourced services to global innovators [3, 5, 6].

To understand the key dynamics shaping this industry, several critical factors must be considered:

1. Market Classification and Regulatory Moats The global market is broadly bifurcated into Regulated Markets (such as the US, UK, Canada, and the EU) and Semi-regulated or Emerging Markets (such as parts of Asia, Africa, and Latin America) [7-9]. Operating in regulated markets requires rigorous adherence to safety, efficacy, and Good Manufacturing Practices (GMP) enforced by agencies like the USFDA, UK MHRA, EDQM, and ANVISA [10, 11]. These stringent regulatory frameworks, combined with the need for high-quality infrastructure (like sterile isolator technologies and complex handling requirements), act as massive entry barriers for new players [12, 13]. Furthermore, switching costs for customers are exceptionally high, as technology transfers and regulatory re-approvals for new suppliers can take 18 to 24 months [13].

2. Supply Chain Restructuring and the “China Plus One” Strategy The industry is actively redesigning its supply chains to mitigate risks, heavily driven by the goal of reducing dependence on China for APIs, intermediates, and key starting materials (KSMs) [14-16]. Geopolitical tensions, new U.S. tariffs, and legislation like the Biosecure Act are accelerating this shift [5, 17, 18]. Large multinational innovators are increasingly seeking high-quality, reliable alternate manufacturing partners in India or onshore in North America to ensure supply chain resilience and avoid disruption [13, 16, 18, 19].

3. Intense Pricing Pressures and the Commodity Trap The generic drug market is characterized by intense competition and continuous pricing erosion, particularly for large-volume, mature commodity products (such as ibuprofen or paracetamol) [20-22]. When raw material prices drop or market competition intensifies, gross margins on these mature generics can fall significantly, leading to under-recovery of manufacturing costs [22, 23]. To survive, pharmaceutical companies are deliberately decoupling from commodity reliance and pivoting toward high-value, low-volume niche molecules where they can exercise better pricing power [24, 25].

4. Transition Towards R&D, Complex Molecules, and Innovation To protect margins and secure future growth, the industry is transitioning from being a generic “pharmacy of the world” to a research-driven powerhouse [26, 27]. Companies are aggressively scaling their Research & Development (R&D) investments to focus on high-barrier, complex therapeutic areas [28-30]. Key areas of scientific focus include: * Specialty and Oncology: Advanced treatments such as targeted oncology, Antibody-Drug Conjugates (ADCs), radioligand therapies, and high-potency APIs [30-32]. * Complex Modalities: Expanding into peptides, oligonucleotides, and biosimilars to treat chronic and rare diseases [33-35]. * Process Innovation: Utilizing green chemistry, automated high-throughput experimentation, and process optimization to improve product yields and reduce costs [36, 37].

5. The Booming CDMO Landscape There is a structural shift toward increased outsourcing, with global innovators and emerging biotech firms heavily utilizing CDMOs to conserve capital and de-risk early-stage development [6, 38, 39]. Indian manufacturers with strong R&D, reliable execution, and excellent Environmental, Health, and Safety (EHS) track records are capturing a significant share of this early-stage and commercial manufacturing demand [33, 38]. Once an innovator partners with a CDMO for a product, they are typically “locked in” due to the complexities of technology transfer and regulatory filing, providing the CDMO with highly stable, recurring revenue [40, 41].

6. Shift Toward Chronic Therapies and OTC Self-Care Demographic changes are driving a shift in disease profiles, leading to surging demand for chronic therapies (such as cardiovascular, anti-diabetic, CNS, and dermatology treatments) [42, 43]. Simultaneously, the industry is witnessing a major transformation in consumer behavior with the rise of the Over-The-Counter (OTC) and direct-to-consumer (B2C) segments [44, 45]. Empowered by the internet, consumers are increasingly engaging in self-care and self-medication for common ailments, leading to explosive growth in lifestyle products, nutritional supplements, proteins, and weight-management brands [45-47].

7. Emerging Opportunities in Animal Health The Animal Health segment is emerging as a highly lucrative adjacent market. Similar to human health, innovator companies in this space are increasingly outsourcing production to quality-focused manufacturers [48, 49]. However, the generic penetration rate in companion animal health is currently only around 15%, offering massive headroom for growth as these markets mature and begin to genericize over the next few years [50, 51].

What are the tailwinds affecting this industry?

asof: 2026-04-14

Supply Chain Diversification and Geopolitical Shifts Global innovators are actively prioritizing supply chain resilience and capital efficiency, driving a structural shift to de-risk their supply chains away from single geographies like China [1-3]. This “China Plus One” strategy creates a highly favorable environment for quality-focused Indian manufacturers to capture global market share, deepen relationships, and expand their product portfolios [2, 4]. Additionally, the enactment of the Biosecure Act in the U.S. is providing a distinct advantage to non-Chinese CDMOs (Contract Development and Manufacturing Organizations) [5-7].

Tariff Dynamics and Policy Changes Geopolitical tensions and trade policies are directly benefiting manufacturers outside of China. U.S. tariffs on Chinese goods have created a massive competitive advantage for Indian players, with tariff differentials on Chinese goods reaching as high as 60% to 70%, allowing Indian manufacturers to aggressively capture market share in the U.S. [8, 9]. Furthermore, large innovator pharmaceutical companies are exploring onshore U.S. manufacturing to mitigate the risk of impending tariffs [10, 11]. In parallel, China has announced the withdrawal of export tax rebates on certain products (such as caffeine and its salts), removing a roughly 13% benefit previously enjoyed by Chinese manufacturers [12, 13]. This policy change is expected to push global prices up by 8% to 10% and reduce the intense pricing pressure and oversupply originating from China, thereby improving the margin profile for Indian API manufacturers [12, 14, 15].

Booming CDMO Outsourcing and Capacity Shortages The global biotech and biopharma CDMO market is experiencing robust growth driven by rising demand, complex biomanufacturing requirements, and an increasing trend of innovators outsourcing development to conserve capital [16-18]. In the specific niche of CDMO Sterile Injectables, the market is witnessing a severe supply-demand mismatch. It is projected that by 2027, there will be a global shortfall of approximately 700 million sterile vials [6, 10]. This gap is widening due to industry consolidation—such as Novo Holding’s acquisition of Catalent—and a rapidly growing pipeline of biologic drugs [6, 10].

A Wave of Patent Expiries Over the next few years, numerous blockbuster products are coming off-patent, providing massive lifecycle management and generic manufacturing opportunities [19, 20]. This genericization runway is not limited to human health; the companion animal health sector is emerging as one of the most attractive long-term opportunities [21]. Currently, only about 15% of the animal health market is genericized (compared to 85-90% in human health), leaving massive headroom for volume growth and cost-efficient generic penetration as pet ownership increases globally [21, 22].

Favorable Macro-Demographics and Government Initiatives The rapid expansion of chronic and sub-chronic therapeutic segments (such as cardiovascular, diabetes, CNS, and dermatology) is being fueled by shifting lifestyle habits, dietary changes, and rising medicine consumption [23, 24]. In India, the domestic market is receiving a major boost with the healthcare budget crossing Rs 1 lakh crore, signaling stronger support for health infrastructure [24]. Additionally, government catalysts like the BioE3 Policy and the RDI initiative are accelerating innovation and scaling up India’s biomanufacturing ecosystem [18].

Shift Toward Complex and Innovative Therapeutics The pharmaceutical industry is evolving from standard generic medicines to complex, high-value specialty therapies and biopharmaceuticals [25, 26]. There is rapid momentum and a growing pipeline for specialized technologies such as Antibody-Drug Conjugates (ADCs), oligonucleotides, peptides, and targeted oncology treatments [5, 27, 28]. Market segments like GLP-1 receptor agonists (for diabetes and weight loss) and novel biopharmaceuticals are serving as massive growth drivers for the industry [29-31].

Rise in Consumer Healthcare and Self-Medication The landscape of consumer behavior is shifting rapidly, serving as a major tailwind for the Over-The-Counter (OTC) and Vitamin/Mineral/Supplements (VMS) markets. Consumers are increasingly taking health into their own hands, with around 53 million people searching for health information online and 1 in 4 consumers practicing self-medication for simple ailments and allergies to avoid expensive doctor visits [32, 33]. This dynamic is largely influenced by social media and internet accessibility, opening up vast opportunities for pharmaceutical companies to scale consumer engagement and drive direct pharmacy sales [34, 35].

What is the general outlook of this industry?

asof: 2026-04-14

The global pharmaceutical, chemical, and life sciences industries are currently navigating a dynamic transition phase, showing signs of a steady recovery while simultaneously dealing with structural realignments and macroeconomic challenges [1]. While traditional base segments face near-term cyclical pressures, the long-term outlook is robust, driven by a strategic pivot toward research, complex specialty therapies, supply chain diversification, and evolving consumer behaviors.

Here is a detailed breakdown of the general outlook across various segments of the industry:

1. Pricing Pressures and Cyclical Challenges in Base APIs and Generics The foundational Active Pharmaceutical Ingredient (API) and generic medication markets are currently experiencing significant headwinds. There is widespread price and quantity erosion across broad geographies, particularly in markets like oral antibiotics, which have seen a 12% price erosion and 10% volume erosion recently [2]. In the last two years, some generic API average selling prices have dropped by as much as 24% [3, 4]. This depression is heavily driven by structural global overcapacity and intense pricing pressure from Chinese manufacturers, who tend to dump products into international markets when their domestic demand slows down [5, 6]. Highly commoditized products, such as Ibuprofen, are facing immense margin pressures due to excess manufacturing capacities that far outpace global demand [7]. However, industry management teams note that the API business is inherently cyclical; as prices fall to levels where suppliers can no longer cover expenses, inventory corrections take place, and the market eventually bottoms out to reach a new equilibrium [8-10]. There are already “green shoots” of recovery appearing, and some fiercely competitive markets, such as the UK and Europe, have recently witnessed a sharp 30% to 40% rebound in prices [11, 12].

2. Growth in Domestic Formulations and the Indian Pharmaceutical Market (IPM) The Indian domestic market remains a strong anchor for the industry, expected to grow in excess of 8% [13]. Recent data indicates the IPM is growing at roughly 8% to 8.9%, largely driven by a 5% to 5.5% increase in pricing and new product introductions, while volume growth has remained relatively muted at around 1% to 2% [14, 15]. The market is observing two notable shifts: high government healthcare spending is facilitating government purchases that eat into the private practice market, and generic drugs are growing equally as fast as branded pharmaceuticals [16]. Furthermore, a rising prevalence of chronic diseases—such as cardiovascular, diabetes, CNS, and dermatology conditions—continues to support excellent long-term demand visibility and a shift toward branded and specialty therapies [17].

3. The Rise of CDMOs and Global Supply Chain Diversification The Contract Development and Manufacturing Organization (CDMO) sector is experiencing accelerated growth as global innovators look to outsource manufacturing to improve capital efficiency and maintain supply chain resilience [18]. Geopolitical tensions and new legislative measures, such as the Biosecure Act in the US, are forcing large multinational pharmaceutical companies to proactively “on-shore” or diversify their supply chains away from China [19]. Innovators are seeking partnerships with reliable suppliers that prioritize environmental, health, and safety (EHS) performance, compliance readiness, and integrated manufacturing capabilities [20-22]. Consequently, specialized CDMO sectors are booming; for example, the global CDMO sterile fill-and-finish market is projected to grow at an 11% CAGR, from $13 billion in 2023 to $20 billion by 2027, driven by a massive pipeline of biologics and an increase in expiring exclusivities [23].

4. A Strategic Pivot to Specialty and Biopharmaceuticals There is a clearly stated, industry-wide intent to transition from merely being the “pharmacy of the world”—focused on established generic medicines—to becoming a “research powerhouse” [24]. Companies are actively decoupling from high-volume, low-margin commodities and pivoting toward complex, high-barrier therapeutic areas that offer superior profitability and lower competitive intensity [25, 26]. Future growth is heavily anchored in new chemical entities (NCEs), complex drug-device combinations, targeted oncology treatments, anti-diabetics (such as GLP-1s for weight management), and peptide chemistry [27-30]. Because these specialized fields target specific unmet patient needs and require smaller, highly focused sales forces, they significantly improve overall operating leverage and profit margins [31, 32].

5. Massive Untapped Potential in Animal Health The animal health sector, specifically regarding companion animals (pets), is emerging as one of the most attractive long-term opportunities in the life sciences space [33]. Supported by a rapidly growing middle class and increasing pet ownership globally, this market is seeing steady demand [34, 35]. Crucially, the generic penetration in the companion animal market is currently very low—around 15%, compared to 85-90% in human health [33, 36]. As blockbuster animal health patents expire over the coming years, manufacturers anticipate a massive runway for genericization, making it a primary focus area for future expansion [35-37].

6. Changing Consumer Behaviors in OTC and Self-Care The Over-The-Counter (OTC) and consumer healthcare landscape is shifting dramatically due to digital empowerment. Approximately 1 in 4 consumers are now self-medicating for simple ailments like pain or allergies to avoid the high costs of doctor visits [38, 39]. With millions of people turning to online search engines and AI tools like ChatGPT for health information, the consumer healthcare segment—particularly Vitamins, Minerals, and Supplements (VMS)—is poised for robust growth. This shift requires the industry to heavily invest in direct-to-consumer education, e-commerce, and pharmacy-level retail execution [40-42].

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.