IT Enabled Services

Industry Metrics

May 8, 2026

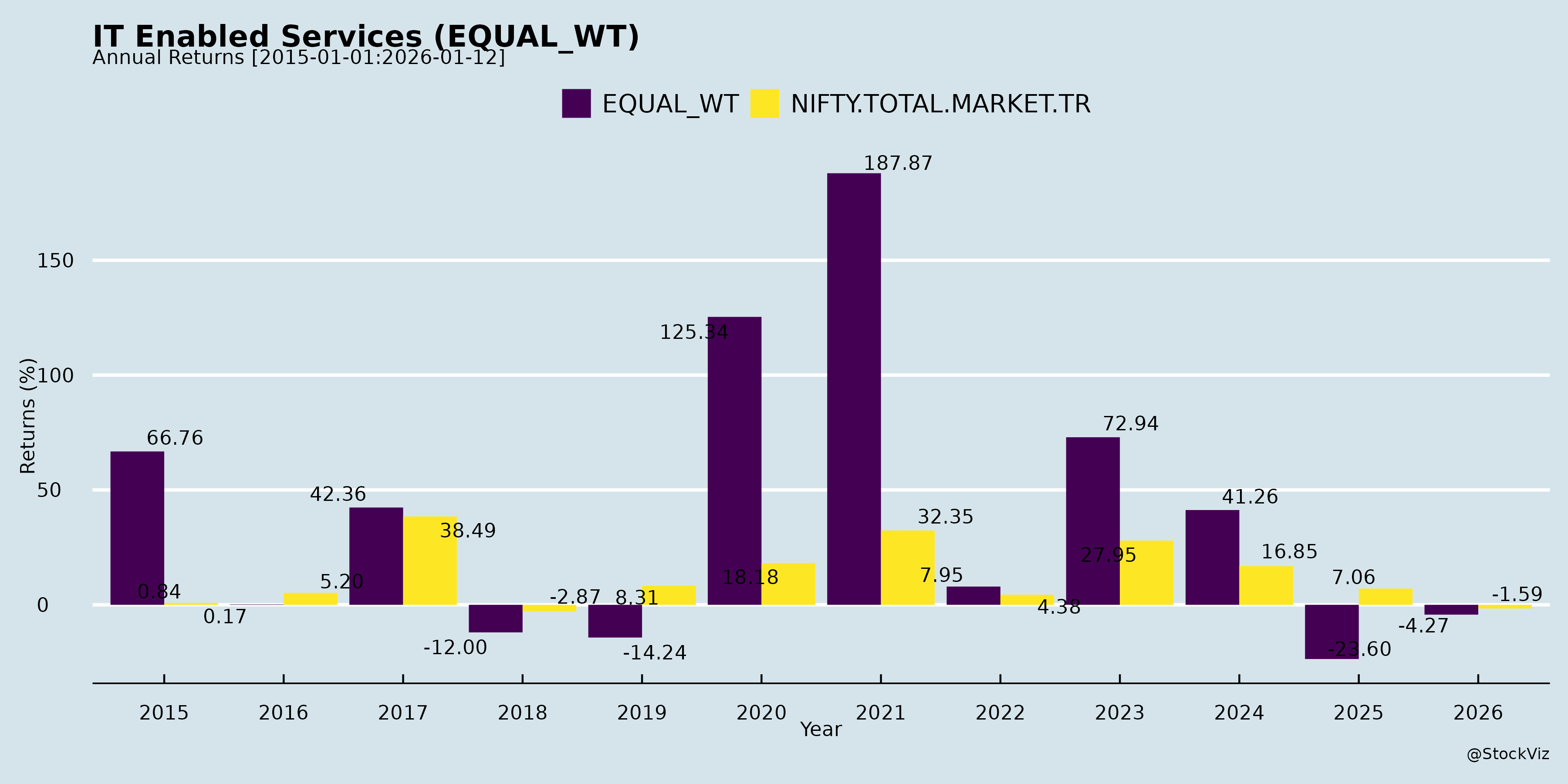

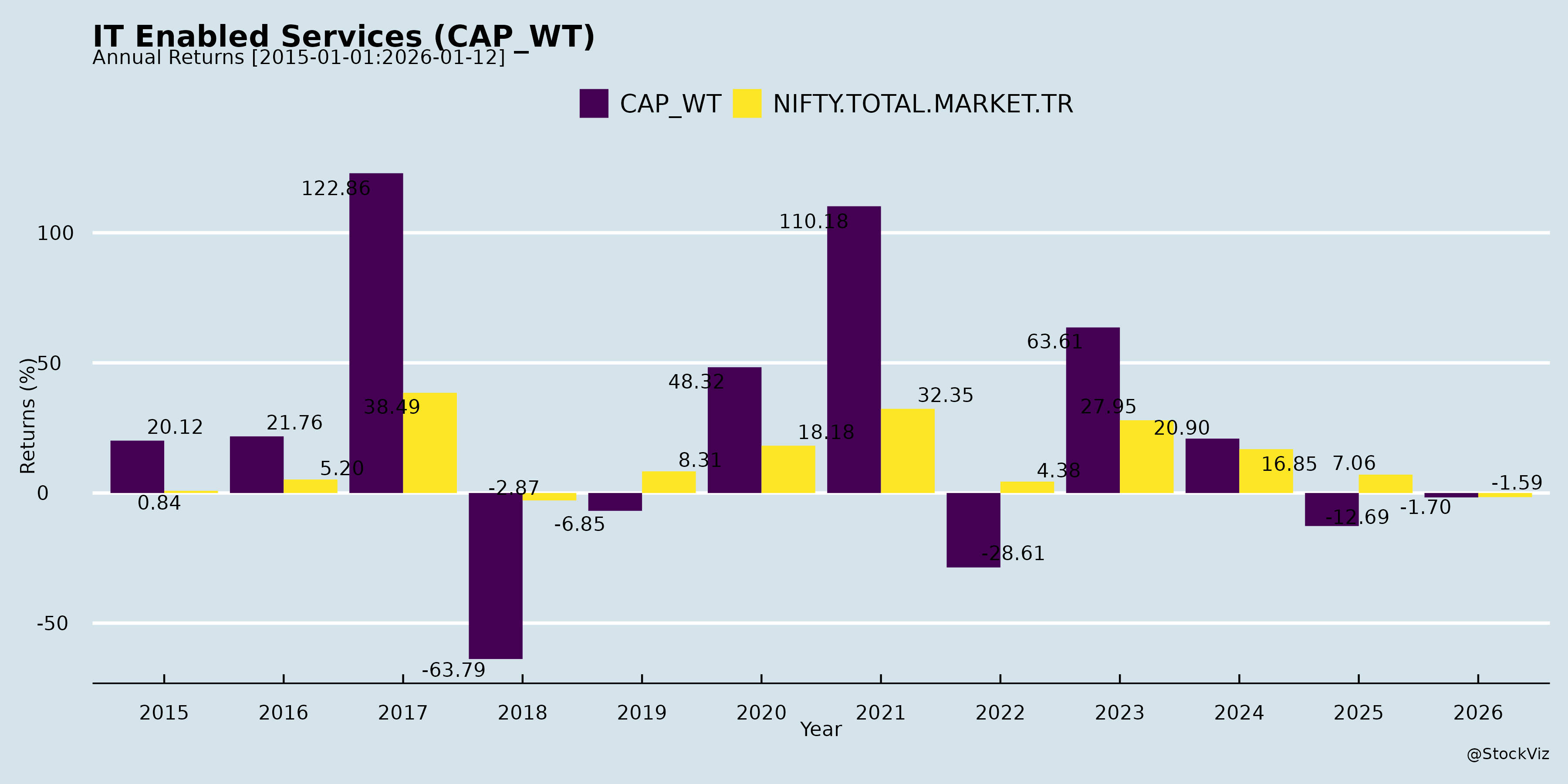

Annual Returns

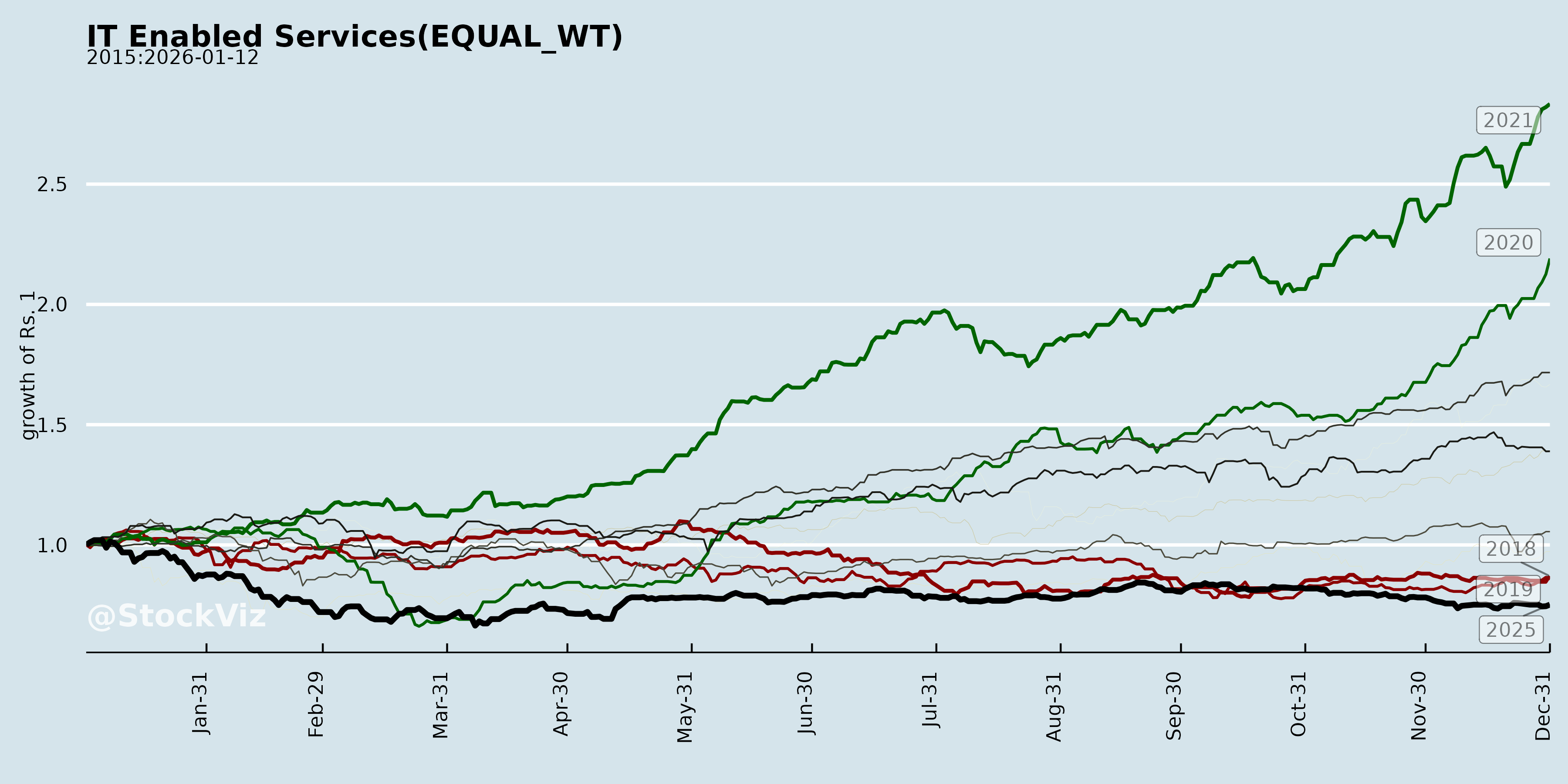

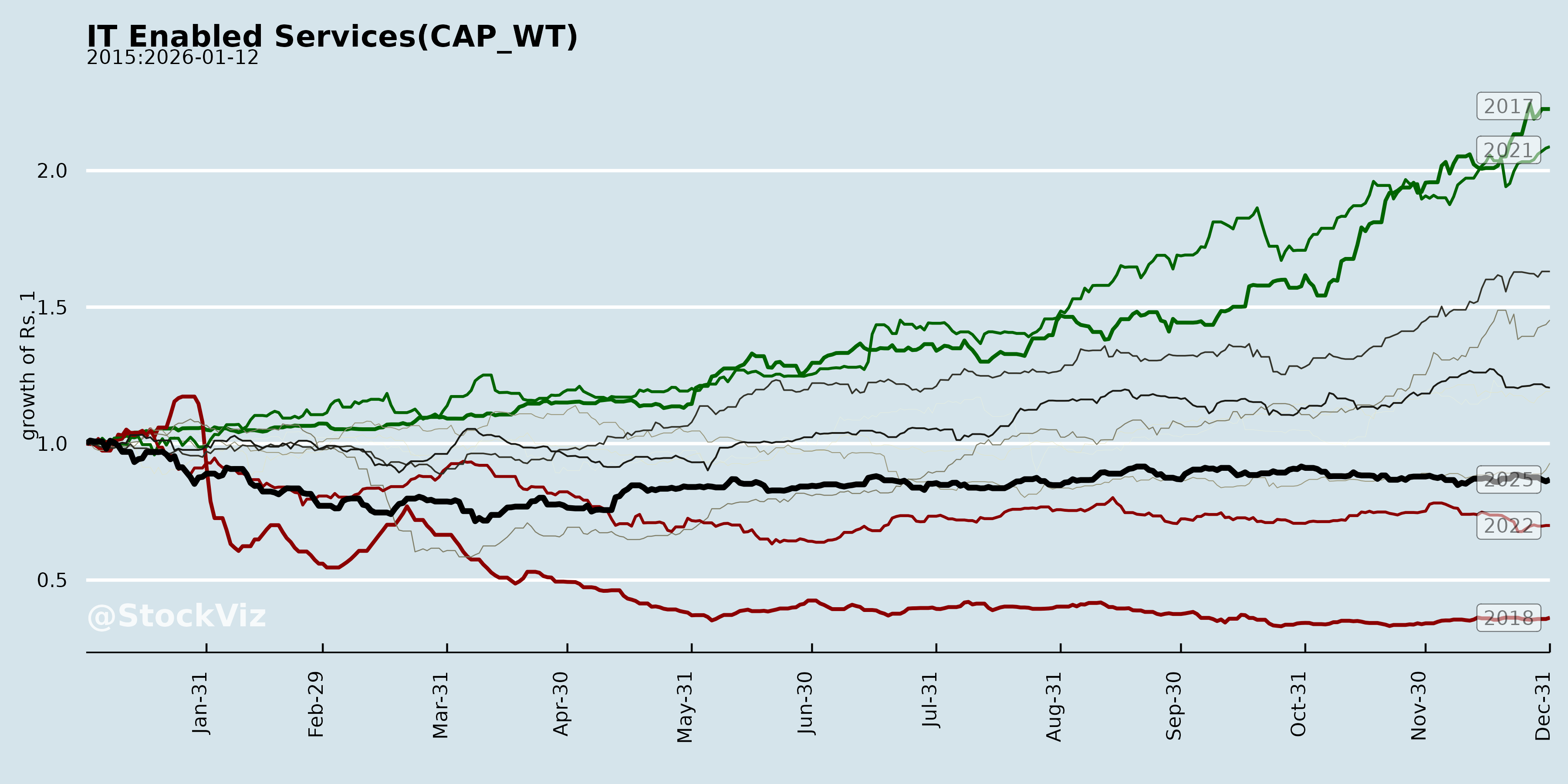

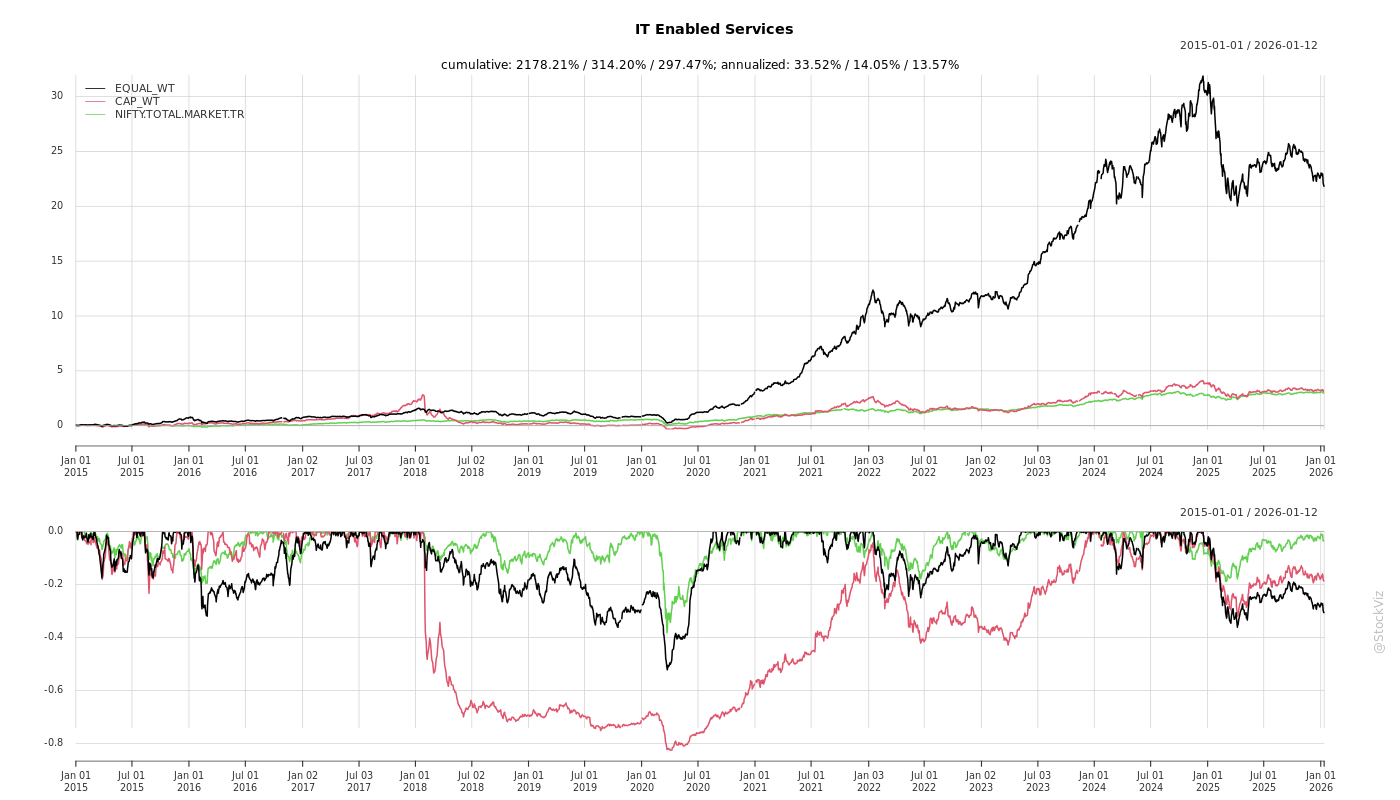

Cumulative Returns and Drawdowns

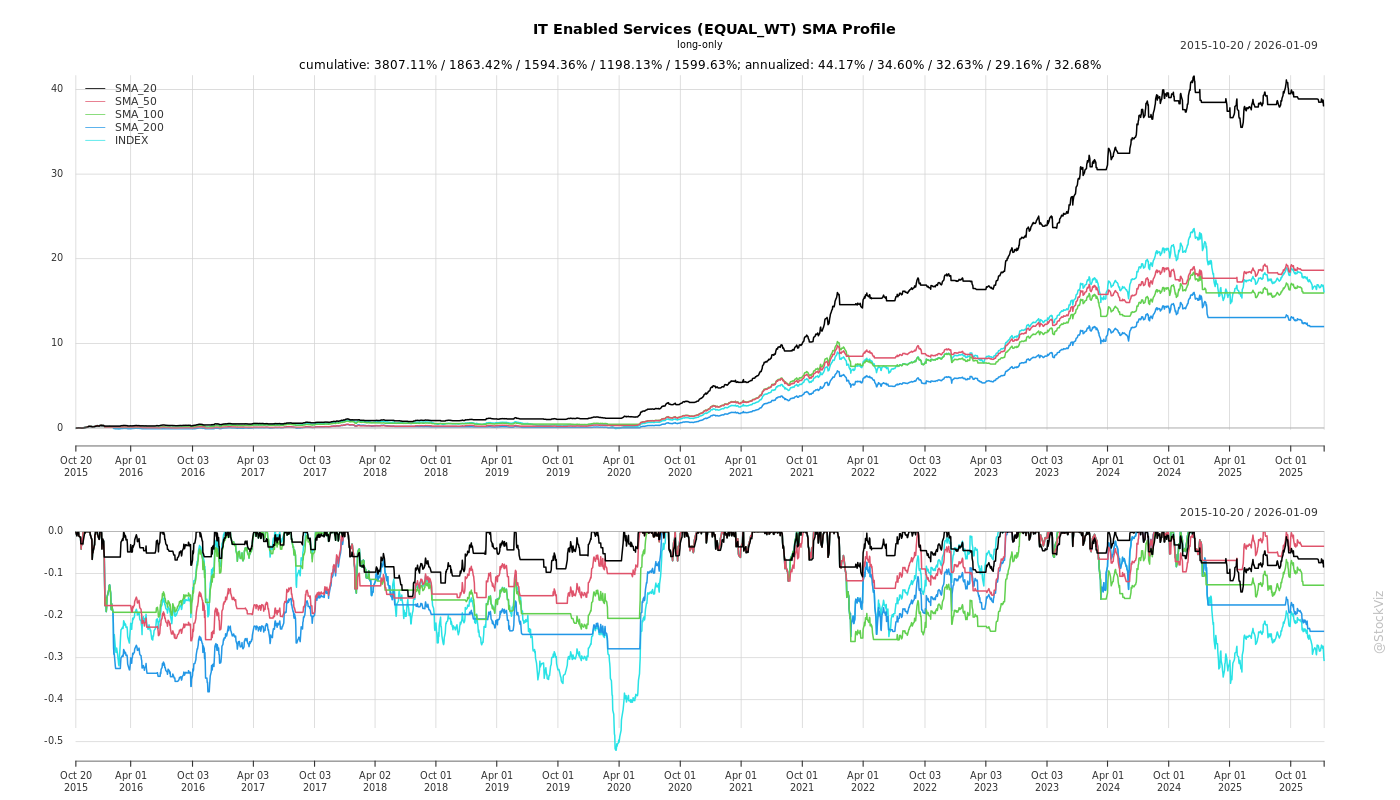

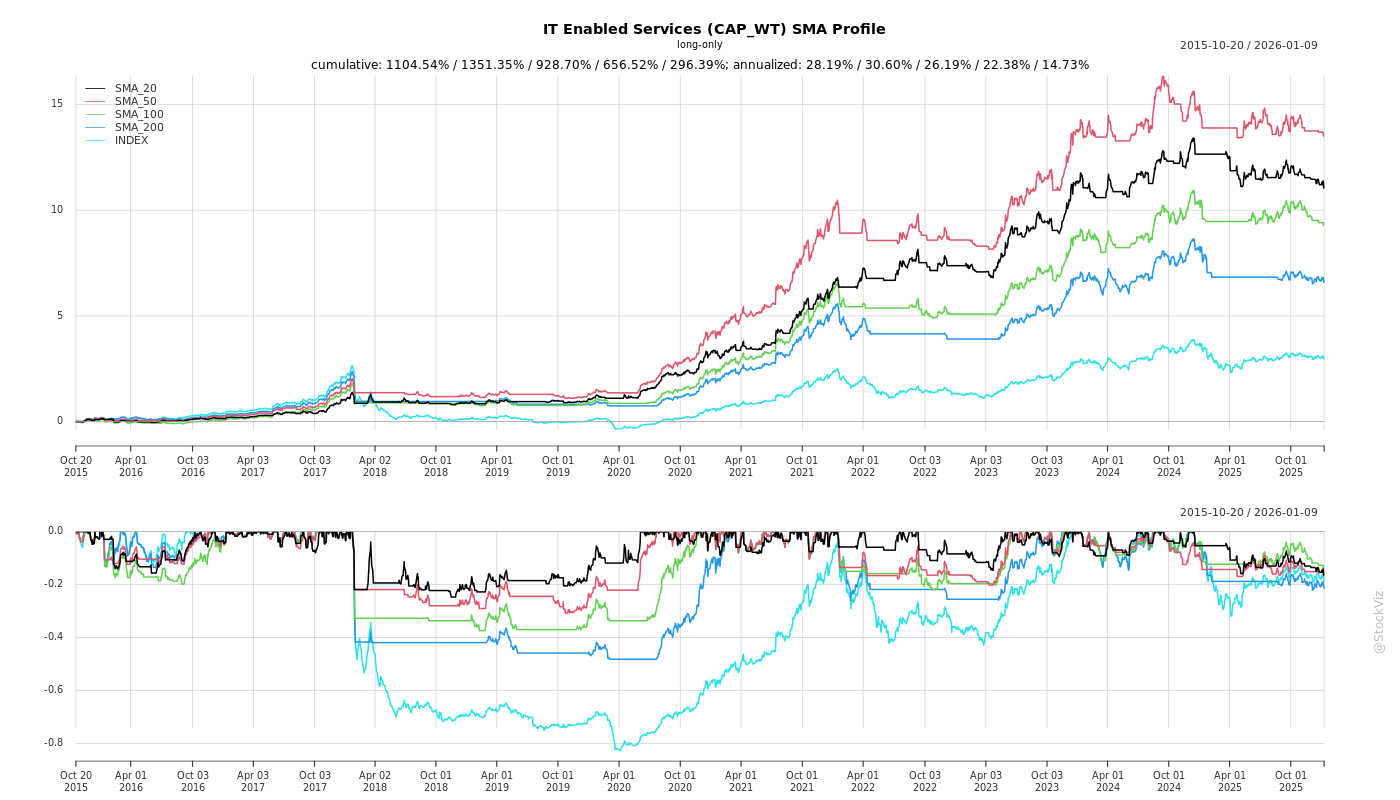

SMA Scenarios

Current Distance from SMA

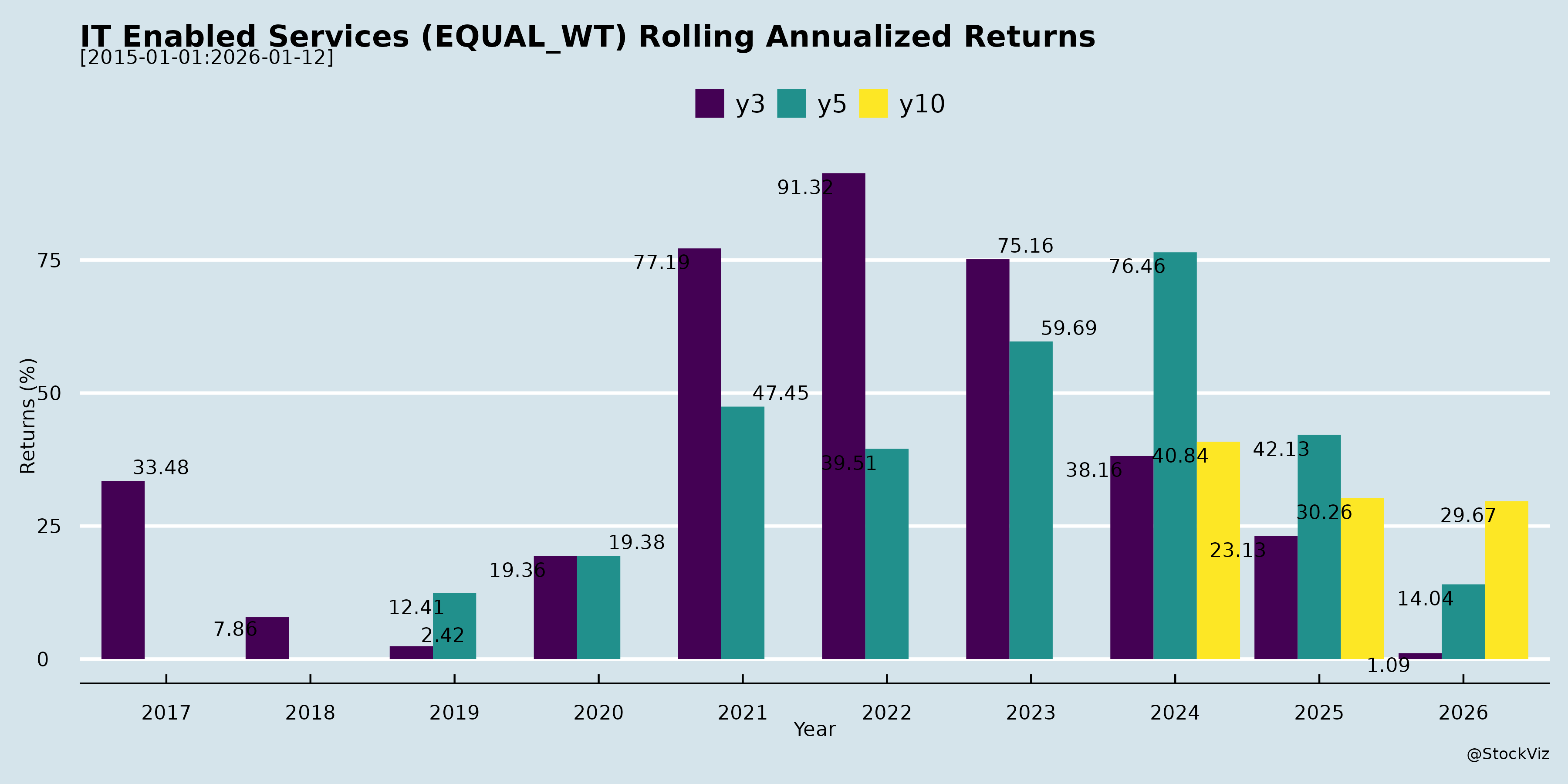

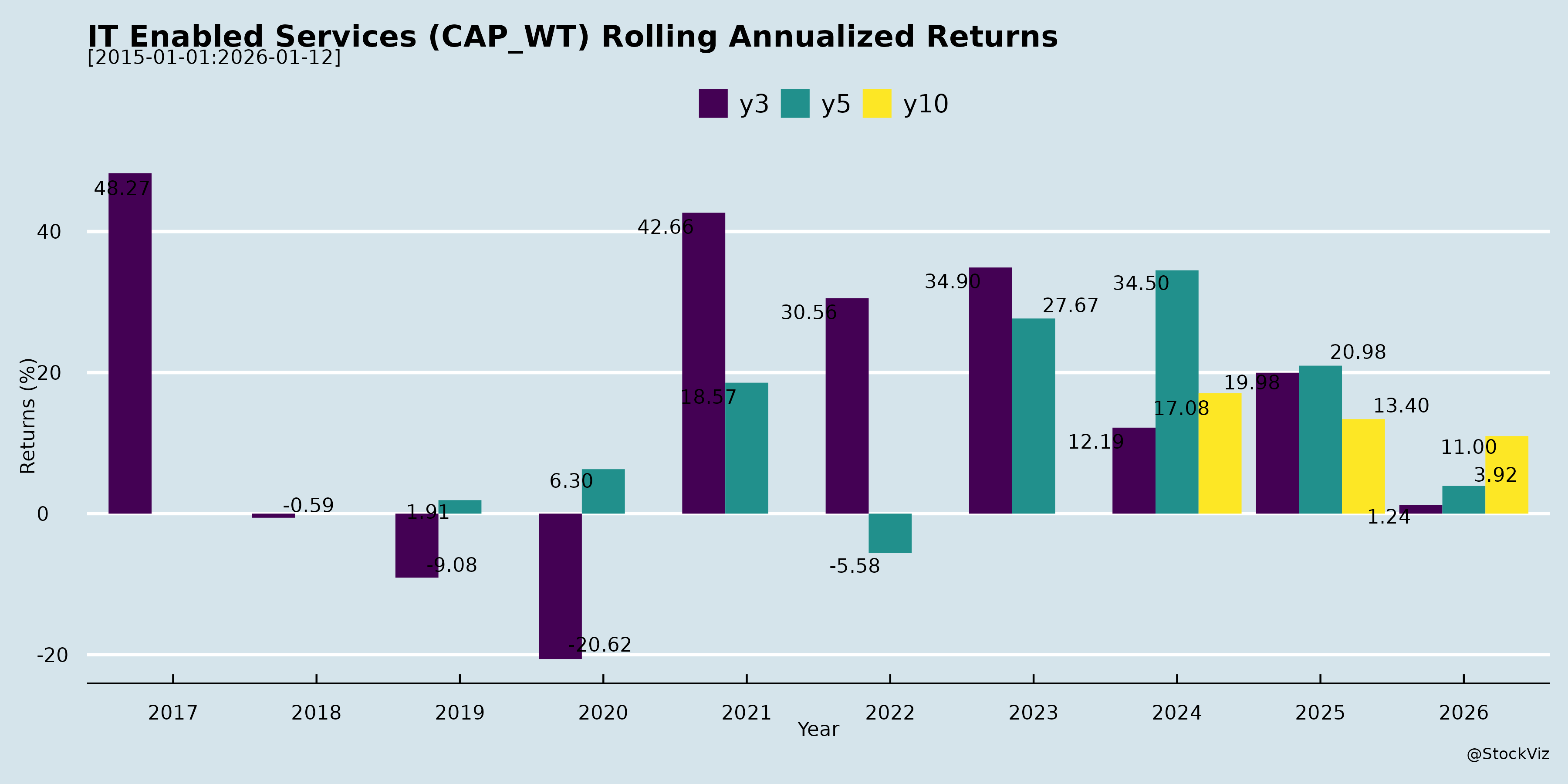

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-16

The evolution of challenges and opportunities over time reflects a massive shift from basic cost arbitrage and manual interventions to highly complex, AI-driven, and outcome-based technological ecosystems. Across various industries such as healthcare operations, IT services, and digital infrastructure, the landscape has transformed significantly over the last few decades.

The Evolution of Challenges

1. From Basic Process Inefficiencies to Complex Margin Pressures Historically, the primary challenges for businesses were rooted in manual, repetitive tasks, outdated infrastructure, and siloed operations [1-3]. Over time, these operational hurdles have evolved into severe macroeconomic and structural challenges. Today, companies face intense margin compressions, pricing and payment pressures (with clients extending payment cycles from 30 to 60 days), and funding winters [4-7]. In sectors like healthcare, challenges have deepened to include complex stakeholder relationships, fragmented data across legacy silos, intricate regulatory compliance, and the critical need for human-in-the-loop clinical judgment [8-10].

2. Supply Chain Disruptions and Hardware Shortages As the demand for advanced technology has surged, physical infrastructure challenges have emerged. Global semiconductor shortages and acute supply-chain disruptions have severely impacted end-user computing and data-center hardware availability [11, 12]. The massive global investments in AI factories and advanced chipsets (like Nvidia) have absorbed a disproportionate share of capacity, leading to extended lead times and significant input cost inflation across mainstream enterprise infrastructure [13-16].

3. The “Threat” of AI and Technological Disruption While AI is largely an enabler, it has introduced novel existential and operational challenges for IT and software businesses: * Fears of Commoditization: There are growing concerns that AI will negatively affect software and IP-led businesses by reducing the cost of coding, accelerating the replication of features by competitors, and weakening product differentiation [17, 18]. * The “SaaS Apocalypse” and Revenue Erosion: Some industry segments fear that advanced AI (like Claude) could replace traditional SaaS platforms or erode traditional “per-seat” and headcount-based billing models, as fewer humans are needed to complete the same amount of work [19-24]. Additionally, Generative AI has emerged as a direct competitor to traditional low-code platforms [25, 26]. * Tool Fatigue: Many clients have purchased multiple AI tools expecting instant results, only to realize that the tools alone do not deliver outcomes without expert integration, leading to widespread “tools fatigue” [27-30].

The Evolution of Opportunities

1. From Labor Arbitrage to Advanced Automation * 25 Years Ago: The original premise of outsourcing and offshoring was simply delivering services from a lower-cost geography to achieve a basic cost differential [31]. * 10 Years Ago: The focus shifted toward process improvement methodologies (like Six Sigma) and early digital tools such as Robotic Process Automation (RPA) and process mining, which successfully targeted simple, rule-based processes to generate 15% to 20% efficiency gains [1, 32, 33]. * Present & Future: The opportunity has evolved far beyond “table stakes” cost reduction. Service providers are now expected to fundamentally transform businesses by orchestrating Agentic AI and Generative AI to automate complex workflows and make autonomous decisions [31, 34-37]. Instead of just executing tasks, AI is used as a “force multiplier” to modernize highly complex legacy systems—such as converting monolithic ERP environments into hyper-scalable microservices [38-40].

2. Shift in Business and Delivery Models Because of the efficiencies driven by modern technology, the way companies sell and capture value has drastically changed: * Rise of Outcome-Based and Managed Services: There is a distinct shift away from traditional Time & Materials (T&M), EPC (Engineering, Procurement, and Construction), and headcount-based billing [20, 23, 41-43]. Clients now demand end-to-end Managed Services and “As-a-Service” models (like Device-as-a-Service, SD-WAN-as-a-Service, and Core Banking-as-a-Service) where vendors take on upfront CapEx risks in exchange for long-term, sticky, annuity-based revenues [44-48]. * Capitalizing on Margin Compression: Ironically, the margin compression and high Medical Loss Ratios (MLR) hurting end-clients have become massive growth opportunities for service providers. Because clients are desperate to reduce operational costs, they are opening up previously restricted “onshore” or core-business operations to end-to-end outsourcing [49-52].

3. Expansion into New Ecosystems and Infrastructure The convergence of different technologies has created entirely new addressable markets: * Digital Public Infrastructure (DPI): There is immense opportunity in building population-scale digital registries and open digital ecosystems across identity, taxation, health, agriculture, and education [53-56]. * Data Centers and Cloud: Driven by AI workloads and data localization requirements, there is a booming opportunity in designing, building, and managing AI-ready data centers, hybrid cloud infrastructure, and sovereign GPU capacities [57-61]. * Next-Gen Engineering: The evolution of technology has opened up vast opportunities in software-defined vehicles (SDVs), digital twins for smart cities, embedded mobility electronics, and the convergence of 5G with satellite communications (Non-Terrestrial Networks) [62-65].

Ultimately, companies that successfully adapt to this evolution are moving away from being mere vendors of commoditized labor or software. Instead, they are integrating deep domain expertise, proprietary intellectual property, and full-stack AI orchestration to deliver guaranteed business outcomes and become highly embedded strategic partners [66-68].

What are the headwinds affecting this industry?

asof: 2026-04-16

Semiconductor Shortages and Supply Chain Disruptions One of the most severe headwinds affecting the technology and infrastructure space is the global semiconductor shortage and supply-chain disruption, which has specifically impacted the availability of end-user computing (EUC) and data-center hardware [1, 2]. The explosive global demand for AI-led data-center infrastructure has absorbed a disproportionate amount of advanced chip and GPU capacity (such as Nvidia hardware) [2-4]. This massive consumption has resulted in extended lead times and significant input cost inflation across mainstream servers, storage, and enterprise devices [1, 2, 4, 5].

Because IT service providers often operate on pre-signed, fixed-price rate contracts to maintain long-term customer relationships, they are forced to absorb these OEM price hikes, resulting in acute, temporary margin pressures [4, 6]. Management in the sources anticipates that these semiconductor and supply-chain challenges will persist throughout the upcoming fiscal year [7].

Macroeconomic and Geopolitical Pressures The broader IT and tech services industry is facing a difficult macroeconomic environment characterized by a “funding winter,” slow procurement cycles, and delayed decision-making by clients [8]. Certain regions, specifically Europe and the Middle East and Africa (MEA), are experiencing notable macro headwinds and challenging market conditions [8, 9].

Additionally, geopolitical turbulence and trade uncertainties are acting as significant obstacles [10]. Service providers are navigating uncertainties in the North American market regarding potential tariff implications on IT service exports, as well as shifts caused by strained political relations between Canada and the USA [11, 12]. Companies are also facing tightened pricing and payment pressures, with North American clients increasingly negotiating extended payment cycles—moving from 30 days to 45 or 60 days [13]. Furthermore, the introduction of new labor codes is anticipated to necessitate the revisiting of pricing structures, posing a potential risk to operational costs [14].

AI Disruption, “Tool Fatigue,” and Margin Pressures While Artificial Intelligence presents opportunities, it also acts as a headwind by threatening traditional business models. * Commoditization of Software Engineering: Investors and analysts fear that AI will negatively impact software and IP-led businesses by drastically reducing the cost of coding and accelerating feature replication [15, 16]. This threatens to compress differentiation windows and commoditize standard development work, especially for companies relying on shallow AI layers built on top of third-party models [15, 16]. * The “SaaS Apocalypse” and Tool Fatigue: The market has experienced fears of a “SaaS apocalypse,” marked by significant drops in the share prices of major software companies due to fears that AI agents (like Anthropic’s Claude) could replace traditional SaaS platforms [17-19]. Meanwhile, enterprise clients are experiencing “tools fatigue”—they have purchased and experimented with multiple AI tools but are struggling to realize actual business outcomes, forcing service providers to pivot toward outcome-based consulting rather than simple tool deployment [20, 21]. * Customer Resistance and Margin Demands: Service providers are caught in a tug-of-war over AI efficiency. Clients are aggressively demanding that IT vendors pass on the cost-saving margins gained through AI automation [22, 23]. Conversely, many other enterprise customers are actively resisting AI entirely due to a lack of internal readiness or strict data confidentiality concerns, forcing vendors to continue executing projects using less-efficient, “old school” programming methods [24-26].

Healthcare-Specific Headwinds For IT service providers operating in the U.S. healthcare operations space (such as payers and providers), the industry faces highly specific systemic challenges: * Margin Compression and Medical Loss Ratios (MLR): Healthcare payers are experiencing severe margin compression due to increasing Medical Loss Ratios (MLRs), which have risen into the high 80s and 90s [27, 28]. This means payers are spending over 90% of their collected premiums solely on paying out claims, leaving very little capital to run administrative operations or generate profit [28]. * Policy and Enrollment Shifts: Funding cuts impacting Medicaid-heavy plans, combined with ACA subsidy changes, have led to a decline in new consumers and significant membership volatility [27, 29, 30]. * Technological and Regulatory Bottlenecks: Healthcare IT modernization is uniquely hindered by heavily fragmented data, siloed legacy systems, and restricted access protocols requiring complex patient consents [31, 32]. Furthermore, deploying AI in this space is constrained by complex stakeholder relationships and strict regulatory concerns regarding behavioral health bias and benefit parity rules [31, 33].

Client Consolidation and Loss Some organizations in the sources also noted the loss of specific large-scale clients—such as the conclusion or loss of hyperscaler cloud services clients and large telecom contracts—which had immediate negative impacts on quarterly revenue and necessitated the absorption of associated OEM savings-plan costs [1, 4, 34, 35].

What are the key things to understand about this industry?

asof: 2026-04-16

The IT services, digital transformation, and e-governance industry is currently undergoing a massive evolution driven by the integration of artificial intelligence, shifts in business models, and the need for specialized domain expertise. Based on the sources, here are the key things to understand about the current state and trajectory of this industry:

1. The Integration of AI and the Modernization of Legacy Systems A central theme across the industry is the shift toward AI-powered platforms and the reduction of technical debt. IT companies are no longer just providing basic software; they are actively helping clients modernize monolithic, legacy environments into hyper-scalable, microservices-based applications [1]. * AI as a Catalyst: Artificial Intelligence, including Generative AI and Agentic AI, is being embedded into enterprise workflows to boost productivity, automate complex customer interactions, and generate hyper-personalized content [2-4]. For example, AI-driven orchestration systems are being deployed in manufacturing for Industry 4.0 [5], and AI tools are being utilized within IT companies themselves to compress development time, improve engineering quality, and reduce the overall code and database footprint [6, 7]. * Opening New Markets: The advent of AI has created a level playing field, allowing IT service providers to tap into large enterprises that previously relied solely on legacy “systems of record.” By using AI to unlock locked data and integrate it with ERPs like SAP and Salesforce, IT firms are accessing entirely new total addressable markets (TAM) [8, 9].

2. The Strategic Shift Toward “As-a-Service” and Recurring Revenue Models To stabilize income and foster long-term client stickiness, the industry is aggressively moving away from traditional one-off projects toward recurring, annuity-based revenue streams [10, 11]. * Diversified “As-a-Service” Offerings: IT firms are increasingly offering specialized models such as Core Banking-as-a-Service (supporting state and cooperative banks), Device-as-a-Service (DaaS), and Software-Defined Wide Area Network (SD-WAN)-as-a-Service [10, 12, 13]. * Managed Services: There is a heavy focus on comprehensive, end-to-end managed services where IT providers handle everything from infrastructure and cloud setups to ongoing security and application support over multi-year contracts [14-16]. * SaaS Transition: Companies are purposefully transitioning their clients from traditional licensing models to Software-as-a-Service (SaaS) models, which provide better financial predictability and align with the recurring engagement preferences of modern enterprises [17, 18].

3. The Boom in E-Governance and Digital Public Infrastructure (DPI) The digitalization of government services and public infrastructure is a massive growth engine, particularly in emerging markets like India. * Population-Scale Digitalization: IT firms are securing high-value mandates to design and maintain national digital platforms, such as the National Pharmacists Registration Tracking System, the UMANG app, and DigiLocker [16, 19, 20]. * Financial Inclusion and Rural Reach: Through Business Correspondent (BC) networks and Assisted E-services, companies are bridging the digital divide by delivering core banking, biometric payments (AEPS), and citizen-centric services (like Aadhaar registrations and birth certificates) directly to rural and semi-urban populations [21-24]. * Global DPI Expansion: The expertise gained in building domestic digital registries is being exported globally, with Indian IT firms winning turnkey projects to build agricultural and identity DPIs in countries like Ethiopia [25, 26].

4. Deep Domain Expertise is Becoming a Crucial Differentiator Clients are increasingly rejecting “black box” outsourcing models and instead demanding partners who possess deep, specialized knowledge of their specific industry [27, 28]. * Complex Industry Ecosystems: In highly regulated sectors like U.S. healthcare, IT providers must understand intricate payer-provider dynamics, clinical judgments, and strict privacy laws (like HIPAA) to effectively deploy AI and optimize administrative costs [29-32]. Domain expertise allows these providers to proactively find revenue leakages—such as overpayments on complex contracts—and deliver targeted point solutions that clients cannot build themselves [33-35]. * Governance and Trust: In sectors like education and e-assessments, deploying AI cannot be done casually. A strong emphasis on responsible AI, fairness, explainability, and data privacy serves as a major commercial differentiator, as clients prioritize trusted governance over mere technological novelty [36, 37].

5. Expansion of Cloud, Data Centers, and Cybersecurity The backbone of this digital and AI expansion requires robust infrastructure. * Data Center Investments: Driven by data localization requirements, AI workloads, and government incentives, there is a surge in data center modernization and expansions [38-40]. IT integrators are heavily involved in providing the disaster recovery, storage capabilities, and infrastructure required by massive hyperscalers and utility companies [13, 41]. * Cybersecurity Imperative: As digital footprints grow—especially with the convergence of satellite, terrestrial, and cloud networks—cybersecurity, Zero Trust architectures, and Security Operations Centers (SOC) have become integral to nearly all IT modernization contracts [38, 42-44].

6. Navigating Margin Pressures and Shifting Pricing Constructs While the industry is growing, it is not immune to macroeconomic headwinds. * Pricing and Payment Pressures: Service providers face aggressive pricing demands and elongated payment cycles from clients across global markets [45-47]. Furthermore, clients themselves are facing severe margin compressions, forcing them to seek IT partners who can take costs out of their operations with minimal upfront capital expenditure (CapEx) [48-51]. * Outcome-Based vs. Time and Materials (T&M): To adapt, the industry is seeing a transition in billing models. While T&M contracts still exist, there is a distinct push toward “outcome-based” pricing. In these models, the IT firm takes on the upfront investment and operational risks, but shares in the financial benefits (e.g., increased cash collections or medical cost savings) generated by their technological efficiencies [52, 53]

What are the tailwinds affecting this industry?

asof: 2026-04-16

Artificial Intelligence and Automation The explosive growth of Artificial Intelligence is acting as a massive force multiplier across industries. Increasing AI workloads and the need for AI-ready infrastructure are accelerating enterprise investments in modern IT [1]. Companies are moving beyond experimenting with AI to embedding Generative and Agentic AI into productive business use cases, creating new demands for AI integration, orchestration, and autonomous modernization [2, 3]. Furthermore, AI and data-center growth is driving a surge in the semiconductor space, particularly creating demand for high-bandwidth, low-power optical interconnects and silicon photonics packaging [4].

Cloud Adoption and Data Center Expansion There is strong demand momentum for data center modernization, cloud adoption, and data localization [1, 5]. Regulators and government bodies are becoming highly open to hybrid and cloud-hosted infrastructure for large-scale public initiatives, further propelling cloud expansion [6]. Simultaneously, governments are actively incentivizing domestic data center build-outs to support the global surge in AI and cloud computing needs [7, 8].

Digital Public Infrastructure (DPI) and E-Governance Government policies are increasingly focused on interoperable, population-scale digital registries and open digital ecosystems (such as ONDC and account aggregators) across sectors like health, agriculture, and education [9-11]. The deployment of DPI is expanding not only domestically but across emerging and developed markets to support financial inclusion and cross-border digital services [12]. Additionally, growing internet penetration and digital literacy are driving the assisted e-commerce and e-governance service markets [13, 14].

Cybersecurity and Resilience As digital infrastructure and cloud-native environments expand, there is a heightened focus on enterprise-grade cybersecurity, compliance, and operational resilience [15, 16]. Businesses are recognizing the need to secure AI deployments and protect digital documents, electronic signatures, and transaction validations across vast ecosystems [12].

Legacy Modernization and Tech Debt Reduction Enterprises are aggressively looking to reduce technical debt, accelerate engineering velocity, and modernize legacy monolithic platforms [3, 17]. AI tools are facilitating faster legacy modernization, allowing companies to tap into data previously locked inside older systems of record [18, 19].

Sector-Specific Tailwinds * Healthcare Operations: U.S. healthcare payers are facing severe margin compression and rising Medical Loss Ratios (MLRs) driven by high utilization and an aging population [20-22]. This financial pressure is forcing health plans to rely on outsourcing partners to drive down administrative costs and deploy tech-led operational efficiencies [23-25]. * Automotive and Telecom: The automotive industry is undergoing a massive transformation toward Software-Defined Vehicles (SDVs), high-performance computing, 5G, and V2X (Vehicle-to-Everything) technologies [26]. In telecommunications, momentum is building around the convergence of satellite and terrestrial networks and the rapid adoption of Non-Terrestrial Network (NTN) services [27]. * Financials and Pensions: The pension sector is entering a phase of structured growth fueled by regulatory reforms aimed at expanding penetration in the non-government sector. Initiatives like multi-scheme frameworks, withdrawal flexibility, and a shift toward AUM-linked (Assets Under Management) charge structures are designed to incentivize long-term asset growth [28, 29].

What is the general outlook of this industry?

asof: 2026-04-16

The fundamental growth drivers across the industry are firmly anchored in artificial intelligence (AI) adoption, digital transformation, enterprise system modernization, and cybersecurity [1, 2]. Overall, the general outlook for the IT and technology services industry is exceptionally optimistic and characterized by robust long-term demand, even as companies navigate near-term macroeconomic and supply chain headwinds [1, 3].

The Transition from AI Experimentation to AI Implementation A major theme shaping the industry’s outlook is the maturation of AI technologies. While the previous year was largely defined by experimentation, the current focus is shifting heavily toward actual, productive implementations of AI and Agentic AI into enterprise workflows [4, 5]. IT service providers see AI not as a disruptive threat to their business models, but as a “boon” and a massive force multiplier that creates extensive new business opportunities [6, 7].

Furthermore, many client companies are experiencing “tools fatigue”—having purchased multiple AI software tools without seeing the promised efficiencies, they are now increasingly turning to IT service providers to deliver concrete, outcome-based solutions [8, 9]. As the market matures, clients are moving past the novelty of AI and are prioritizing trusted, explainable, and well-governed AI integrations, which heavily favors established tech companies with deep domain expertise [10].

Core Technology Growth Vectors Beyond AI, the demand environment remains highly resilient across several core technology pillars: * Data Centers and Cloud Infrastructure: There is accelerating enterprise investment in modern, AI-ready data centers, cloud adoption, and data localization [11]. In rapidly growing digital economies like India, there is strong government and regulatory support for hybrid and cloud-hosted digital public infrastructure (DPI), as well as sovereign cloud initiatives for sensitive data [12, 13]. * Cybersecurity and Tech Debt Reduction: Heightened focus on compliance, systemic resilience, and the modernization of legacy tech debt continues to drive enterprise spending [8, 14]. Companies are also actively seeking partners to help accelerate their overall engineering velocity [8, 15]. * Global Capability Centers (GCCs): GCCs are actively expanding and attempting to position themselves as AI Centers of Excellence for their parent enterprises, requiring significant expertise and enablement from IT partners [15, 16].

Massive Sector-Specific Tailwinds The outlook is further strengthened by sweeping, sector-specific digital shifts: * Healthcare: US healthcare payers are facing severe margin compression and rising medical loss ratios (MLR), forcing them to drastically reduce administrative expenses to maintain profitability [17, 18]. Because current outsourcing penetration in the payer market is only in the low 20s, IT and managed service providers have a massive ~70% untapped market to generate efficiencies through process automation and offshoring [19]. * Automotive and Telecommunications: The global automotive industry is undergoing a software-led transformation toward Software-Defined Vehicles (SDVs), centralized architectures, and 5G/V2X technologies [20]. In the telecom space, the rollout of 3GPP Release 19 is integrating AI/ML into cellular networks and driving the convergence of terrestrial and satellite communications [21, 22]. * Digital Public Infrastructure (DPI) & Education: Emerging markets are witnessing a massive expansion in population-scale digital infrastructure across identity, taxation, health, and agriculture [23, 24]. Additionally, the education sector is seeing accelerated, long-term adoption of digital learning platforms, high-stakes testing, and enterprise skilling [25].

Macroeconomic and Supply Chain Headwinds Despite the strong underlying demand environment, the industry does face several tangible, near-term challenges: * Geopolitical and Pricing Pressures: Service providers are dealing with geopolitical turbulence, uncertainties around US tariff implications, and shifting global trade relations [26, 27]. This has led to pricing and payment pressures globally; for instance, North American clients are increasingly negotiating extended payment terms, moving from standard 30-day cycles to 45 or 60 days [28]. * Hardware and Supply Chain Disruptions: The massive global investment in AI factories and data centers has absorbed a disproportionate share of advanced chip (GPU) capacity [29]. This dynamic has caused severe global supply chain bottlenecks, hardware component shortages, extended lead times, and increased input prices, which are temporarily pressuring margins for companies heavily involved in IT infrastructure and hardware deployment [29-31].

In summary, while hardware supply chain constraints, pricing pressures, and geopolitical uncertainties pose short-term hurdles, the industry’s long-term outlook remains exceptionally strong. Enterprises worldwide are continuously redefining their core operations and increasingly relying heavily on IT service partners to navigate complex digital transformations, deploy enterprise-grade AI, and securely manage mission-critical infrastructure [1, 32-34].

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.