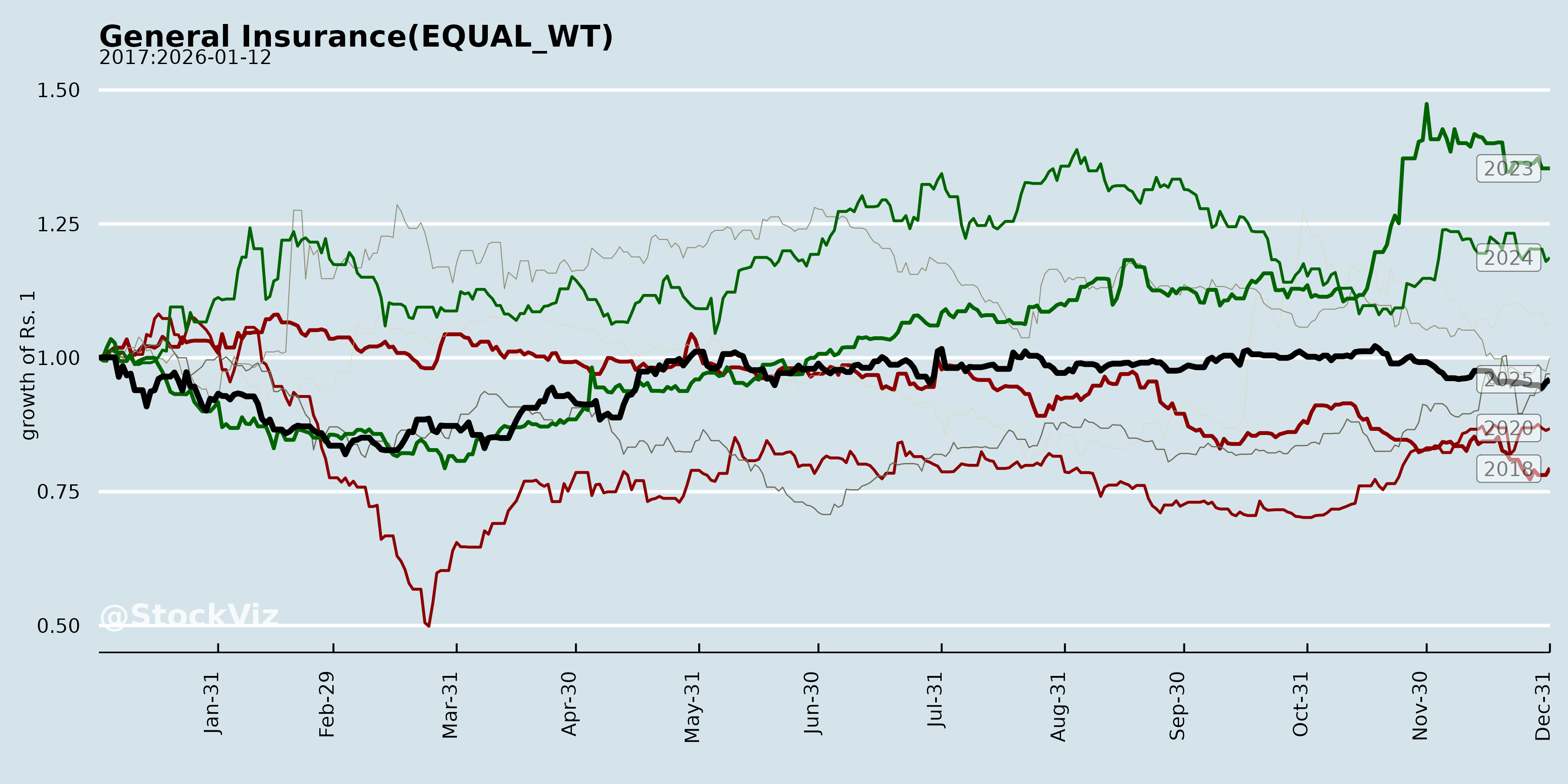

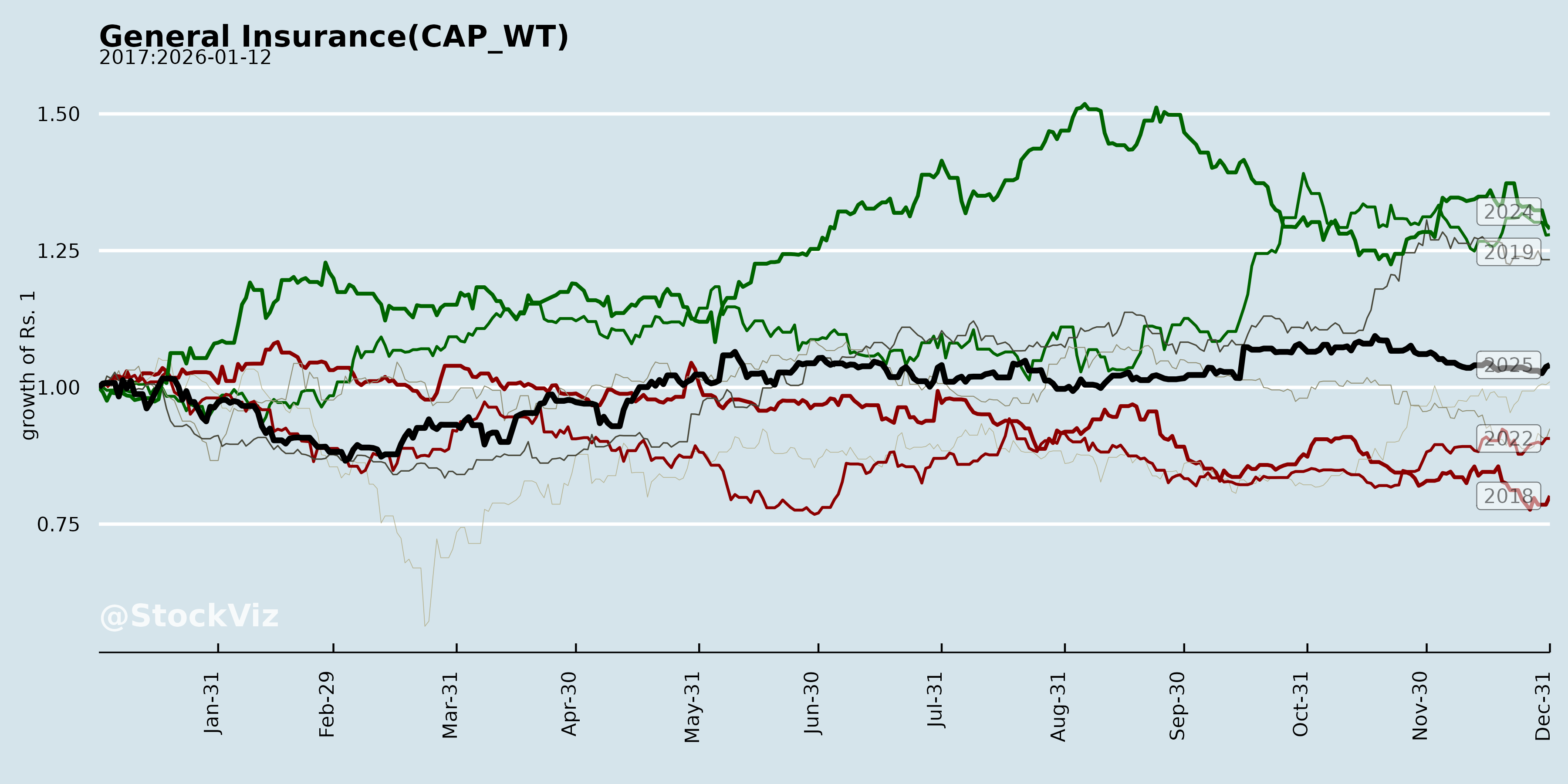

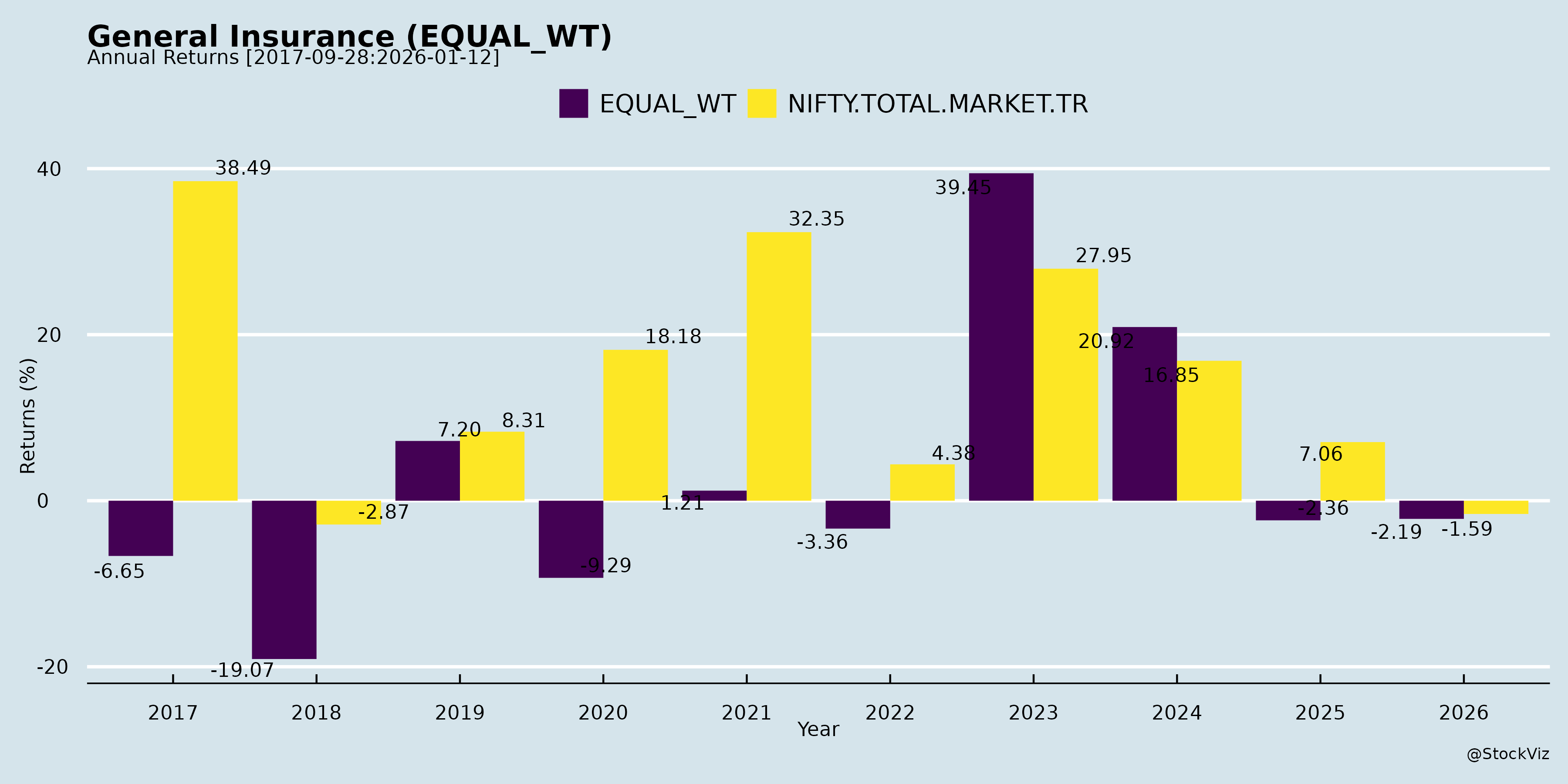

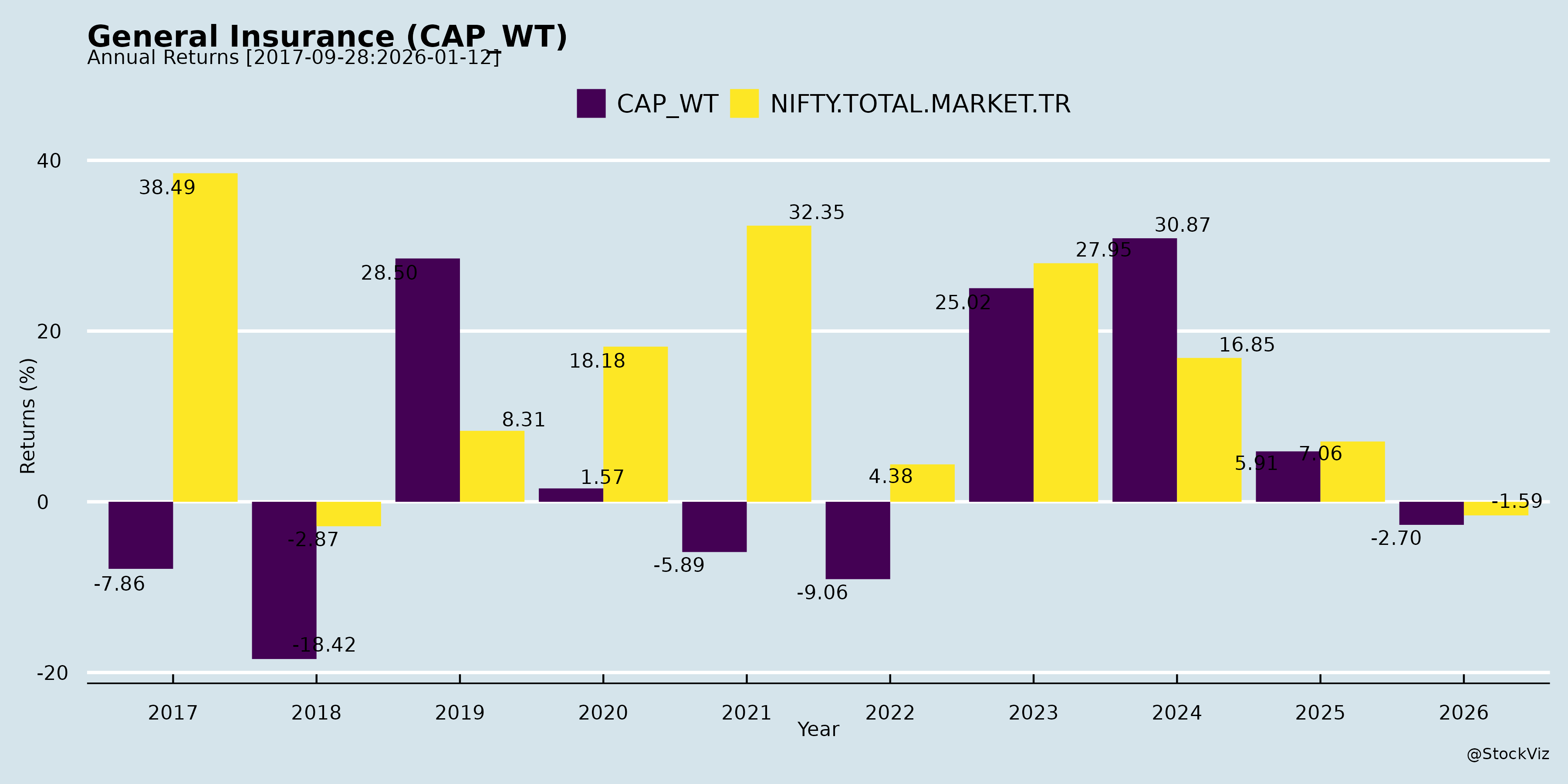

General Insurance

Industry Metrics

May 8, 2026

Annual Returns

Cumulative Returns and Drawdowns

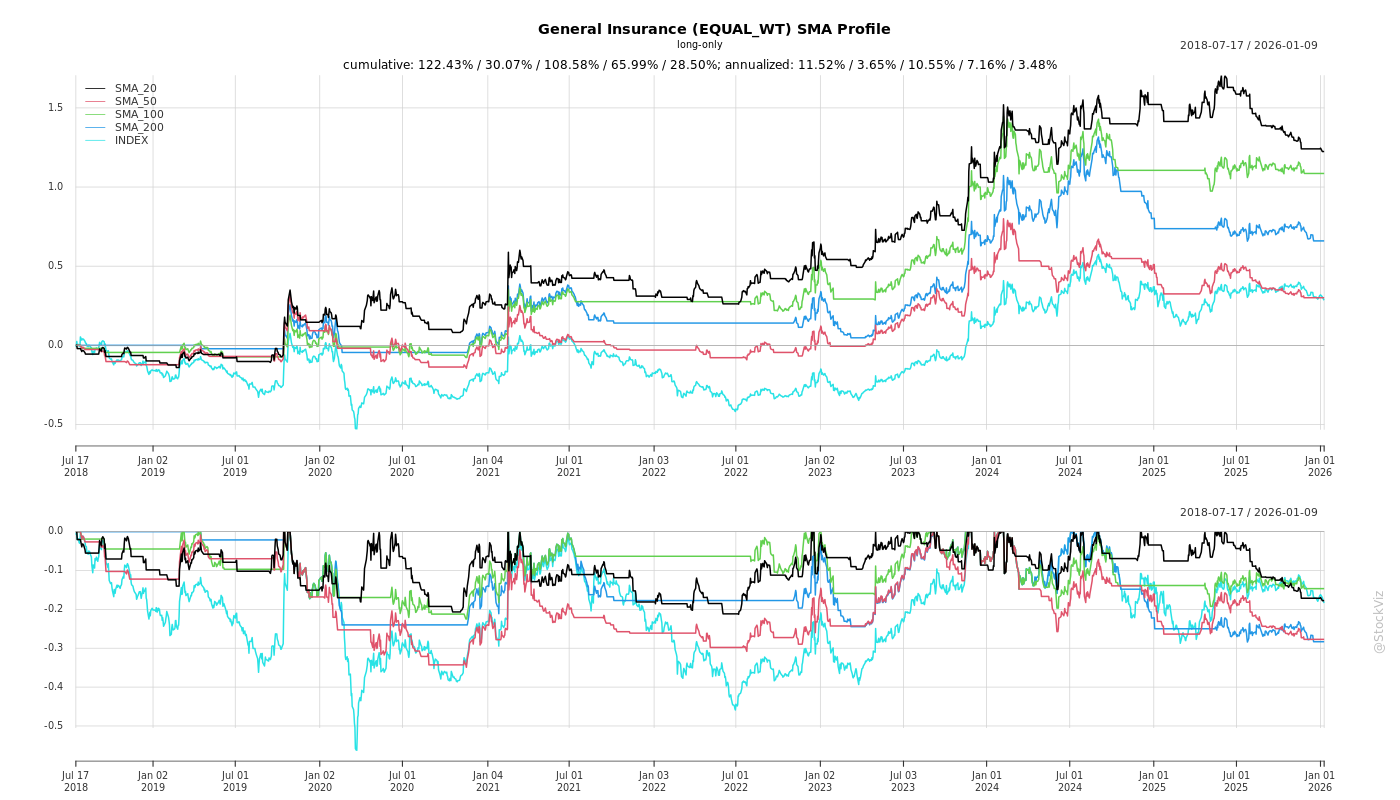

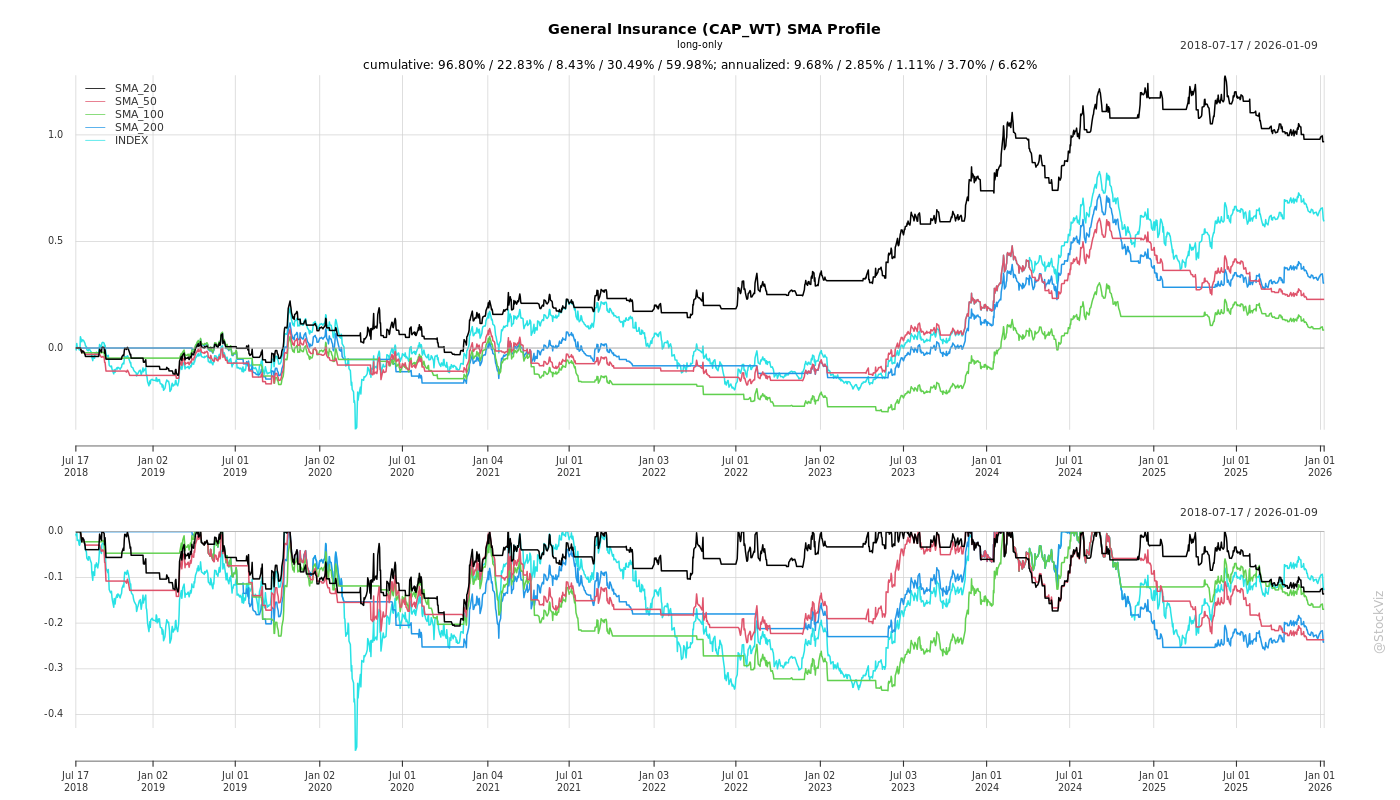

SMA Scenarios

Current Distance from SMA

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-16

The insurance sector has navigated a complex and evolving landscape of challenges and opportunities over time. As market dynamics, technological advancements, and regulatory environments have shifted, insurers have been forced to adapt their strategies to maintain profitability and capitalize on new growth avenues.

Evolving Challenges

1. Competitive Pricing and Claims Inflation Over time, the general insurance industry has operated in a highly competitive environment characterized by intense pricing pressures and elevated claims experiences in certain segments [1, 2]. Claims inflation and intense competitive intensity have persisted as near-term hurdles [3, 4]. Historically, insurers have struggled with large corporate accounts where the pricing did not adequately compensate for the risk or capital consumption, forcing them to reconsider their underwriting strategies [5, 6]. Additionally, some insurers have historically relied heavily on investment income for their profits, requiring a strategic shift away from this reliance toward core underwriting profitability [7].

2. Catastrophic and Segment-Specific Losses The frequency and financial impact of natural catastrophes (CAT losses) have presented significant challenges. Elevated catastrophic losses have periodically spiked the incurred claim ratios [8]. To handle future claim volatility and reduce financial vulnerability, companies like GIC Re have had to begin actively providing for Catastrophe Reserves on a quarterly basis rather than annually [9-11]. Insurers have also faced sudden segment-specific shocks, such as severe marine cargo claims resulting from sunken ships, or regulatory and seeding issues leading to major premium declines in crop insurance [12-15]. In the health segment, there are recurring seasonal challenges, with higher claims typically witnessed during the monsoon period due to water-borne diseases [16].

3. Operational, Regulatory, and Cyber Risks Operational costs and regulatory compliance present ongoing hurdles. Major wage revisions for public sector general insurance employees have required provisions of thousands of crores, substantially inflating expense ratios and combined operating ratios in the short term [8, 17, 18]. Some insurers have even seen their expenses of management exceed the regulatory limits set by the IRDAI [19]. Furthermore, insurers have faced scrutiny from tax authorities, resulting in multiple disputed demands regarding GST and Service Tax [20, 21]. In the modern digital era, cyber risk has materialized as a direct challenge; for instance, a cybersecurity incident involving unauthorized data access in August 2024 resulted in an IRDAI penalty and necessitated significant overhauls to an insurer’s information security systems [22].

Evolving Opportunities

1. Vast Untapped Market and Favorable Macro Policies Despite the challenges, the structural opportunity in the Indian market remains massive. The general insurance penetration level in India is under 1%, indicating immense room for growth [7]. The macro and policy environment is highly supportive, driven by the national ambition of achieving ‘Insurance for All’ by 2047 [23]. Government budgets have introduced numerous enablements for the MSME (Micro, Small, and Medium Enterprises) sector, which opens up vast opportunities for credit and overall business protection insurance [24, 25]. Insurers are actively targeting this by expanding their physical and digital footprints into Tier 2 and Tier 3 cities [26, 27].

2. Strategic Portfolio Recalibration and Niche Products To combat unviable pricing, insurers have aggressively recalibrated their portfolios to exit loss-making corporate lines and refocus on Retail, SME, and better-quality risks [5, 6, 28, 29]. This strategic shift has allowed companies to stabilize their portfolios and improve market share [5, 6, 30, 31]. The market has also seen the evolution of highly specialized, tailor-made products, including specific health coverage for cancer, diabetes, cardiac illnesses, senior citizens, and women [32].

A major evolutionary leap is the introduction of Parametric Insurance, a product based on weather-related thresholds rather than traditional loss assessment [33, 34]. Because payouts are triggered automatically when a threshold is breached (e.g., severe weather events), policies can be issued digitally en masse, and claims can be settled in a matter of minutes or hours, dramatically easing the burden of claim processing and accelerating insurance penetration [35, 36].

3. Digital and Technological Transformation Technology has become a cornerstone of operational efficiency and customer acquisition. The industry has moved toward a “Digital First” approach, which is building operating leverage across the value chain [37]. Key technological evolutions include: * Customer Self-Service: Customer applications have scaled massively—with some seeing over 13 million downloads and facilitating hundreds of thousands of digital renewals and claim submissions [38]. * AI and Automation: The deployment of AI-enabled claims engines has allowed insurers to migrate significant portions of claims traffic (up to 57%) to automated systems, enhancing productivity and customer satisfaction [38]. Predictive underwriting models and advanced tech platforms are also being leveraged to improve risk selection [39]. * Accessibility: Insurers have revamped websites and introduced AI/ML-enabled chatbots, alongside WhatsApp services and call centers offering policy and claim-related support in multiple regional languages [40-43].

Ultimately, while the industry has grappled with aggressive pricing, catastrophic losses, and rising operational and cyber risks, the shift towards digital transformation, tailored retail products, and vast underpenetrated markets continues to drive long-term value creation.

What are the headwinds affecting this industry?

asof: 2026-04-16

Claims Inflation and Catastrophic Losses The industry is currently grappling with persistent claims inflation and elevated claims experiences across certain segments [1-4]. For example, the marine sector has faced exceptionally large claims due to ship sinkings resulting in General Average (GA) and marine cargo claims, while the aviation sector has been impacted by major individual incidents like the Air India claim [5-8]. Furthermore, multiple catastrophic (CAT) losses—especially concentrated in the first half of the year—have elevated the incurred claim ratios for insurers, prompting them to start provisioning specific Catastrophe Reserves on a quarterly basis to handle future volatility and reduce financial vulnerability [9, 10]. The industry also routinely battles seasonal headwinds, such as spikes in health insurance claims during the monsoon period due to rainy season-related diseases [11, 12].

Competitive Intensity and Pricing Pressures Insurers are operating in a highly competitive environment characterized by selective pricing pressures [1, 3]. This intense competition has forced companies to take deliberate, strategic steps to weed out non-viable product lines and exit or restructure select large corporate accounts [13-16]. In segments like Motor and Group Mediclaim (GMC), companies have suffered from exceptionally harsh losses where the pricing did not adequately compensate for the underlying risk or capital consumption, forcing them to walk away from accounts that do not offer fair and adequate pricing [17-20].

Increased Operational and Employee Costs Surging employee benefit expenses have been a major headwind, significantly denting underwriting results and Combined Operating Ratios [9, 21, 22]. This is driven by two primary factors: * Public Sector Wage Revisions: The Central Government recently approved wage revisions for Public Sector General Insurance Companies, forcing insurers to recognize massive one-time provisions—amounting to thousands of crores—toward wage arrears (dating back to August 2022) and retirement benefits for active employees [9, 23-26]. * New Labour Codes: The implementation of the government’s four New Labour Codes (the Code on Wages, Industrial Relations Code, Code on Social Security, and Occupational Safety, Health and Working Conditions Code) has expanded eligibility criteria and revised the definition of wages [27-29]. This has required companies to recognize incremental gratuity expenses and increased employee benefit provisions [27].

Extensive Taxation Disputes and Litigation Insurance companies are currently fighting severe legal and financial battles with both direct and indirect tax authorities: * Indirect Tax Demands: Insurers have received massive orders from GST and Service Tax authorities alleging non-payment of taxes [30-32]. These multi-crore disputed demands specifically target co-insurance premiums accepted, reinsurance commissions earned on ceded policies, group mediclaim policies issued to Special Economic Zones (SEZs), and claims settled on a net salvage basis [30, 31]. * Direct Tax Demands: Companies are also facing major disputed income tax demands regarding the treatment of profits on the sale of investments, Unexpired Risk Reserves, Reinsurance Premiums Ceded outside India, and reserves for Claims Incurred But Not Reported/Enough Reported (IBNR/IBNER) [33, 34]. These demands have forced companies to file writ petitions and appeals before appellate authorities and High Courts [30, 31, 33, 34].

Regulatory Scrutiny and Cybersecurity Risks The regulatory landscape continues to present challenges that disrupt standard operations. Regulatory issues have specifically hindered the Crop insurance segment, where insurers faced significant de-growth because the Agriculture Insurance Corporation could not seed business on a reinsurance basis [35, 36]. Insurers have also struggled to keep their operating expenses within regulatory limits, with some exceeding the maximums stipulated by the IRDAI Expenses of Management regulations and having to formally seek forbearance from the authority [37].

Additionally, the industry is battling modern technological risks. At least one major insurer suffered a cybersecurity incident involving unauthorized data access, which led to a show-cause notice from the IRDAI for non-compliance with Information & Cyber Security guidelines and resulted in a monetary penalty [38]. Companies are also facing regulatory letters of advice highlighting violations of Master Circulars related to Health Insurance Business, Corporate Governance, and the Protection of Policyholders’ Interests [39].

Market Volatility Finally, broader macroeconomic headwinds and volatile market conditions have actively impacted the asset side of the business, causing noticeable reductions in fair value change accounts and putting pressure on insurers to heavily rely on realizing equity capital gains to offset their underwriting losses [40-43].

What are the key things to understand about this industry?

asof: 2026-04-16

Based on the provided sources, here are the key things to understand about the general, health, and reinsurance industry in India:

1. Massive Growth Potential and Seasonality * Low Penetration: The general insurance penetration level in India is currently under 1%, which indicates immense growth potential for the industry [1]. The sector is working alongside the government’s national ambition to achieve “Insurance for All” by 2047 [2]. * Seasonality: The industry, particularly the health insurance segment, is highly seasonal. Claims typically spike during the monsoon season due to an increase in rainy season-related diseases [3, 4]. Conversely, premium income historically peaks towards the end of the financial year as policyholders purchase insurance to avail of tax benefits [3, 4].

2. Core Business Segments General insurers maintain diversified risk portfolios that span across multiple lines of business. The primary segments include: * Motor Insurance: Split into Own Damage (OD) and Third Party (TP) [5, 6]. * Health and Personal Accident (PA): Includes retail, group/corporate, and government health schemes [6, 7]. * Commercial and Property Lines: Includes Fire, Marine (Cargo and Hull), Engineering, Aviation, Liability, and Crop/Agriculture insurance [6, 8, 9].

3. Key Performance Indicators (KPIs) and Profitability Understanding an insurance company’s financial health requires looking at specific industry metrics: * Incurred Claim Ratio (ICR): The ratio of net claims incurred to the net earned premium [10]. * Expense Ratio: Calculated by dividing net commissions and operating expenses by the net written premium [10]. * Combined Ratio: The sum of the claim ratio and the expense ratio [10]. A combined ratio below 100% generally indicates that a company is making an underwriting profit, while a ratio above 100% means it is paying out more in claims and expenses than it collects in premiums. * Solvency Ratio: A crucial measure of financial stability, with the regulatory minimum requirement set at 1.50x [11, 12]. * Reliance on Investment Income: Because of claims inflation and high competitive intensity (especially in Motor and Health), underwriting profitability can be challenging [13, 14]. Consequently, insurers often rely heavily on the income generated from investing the premiums they collect to drive their overall Profit After Tax (PAT) and Return on Equity (ROE) [1, 15].

4. Reserving and Reinsurance * Mandatory Reserves: Insurers must carefully estimate and set aside technical reserves to ensure they can meet future obligations. Key reserves include IBNR (Claims Incurred But Not Reported), IBNER (Claims Incurred But Not Enough Reported), and the Premium Deficiency Reserve (PDR) [16, 17]. * Catastrophe Reserves: Companies are increasingly focused on creating catastrophe reserves to handle future volatility from large natural catastrophes (NAT CAT) and to reduce financial vulnerability [18, 19]. * The Role of Reinsurance: Reinsurers provide critical capacity and support to primary domestic insurers. They help manage large exposure pools, mitigate risks, and support social financial schemes [1, 20].

5. Technological Transformation and New Products * Digitalization and AI: Insurers are adopting a “digital first” approach to improve customer experience and operating leverage. This includes AI and Machine Learning (ML) enabled claim engines that automate claim processing for faster settlements, as well as multi-lingual chatbots and mobile apps for policy renewals and self-service [14, 21, 22]. * Parametric Insurance: A new and emerging product line that differs from traditional insurance. Instead of indemnifying the actual loss, parametric insurance pays out automatically when a predefined weather-related peril threshold is breached [23]. Because it relies on digital interfaces, it allows for claims to be paid in minutes or hours rather than going through lengthy traditional claim processing, aiding faster market penetration [24, 25].

6. Regulatory Environment The industry is tightly governed by the Insurance Regulatory and Development Authority of India (IRDAI), which sets guidelines on everything from solvency and cyber security to the limits on expenses of management [26-28]. Additionally, the industry is actively preparing to transition to IFRS (the global standard for financial reporting) by 2027 to enhance transparency and international comparability [2].

What are the tailwinds affecting this industry?

asof: 2026-04-16

Government Reforms and Supportive Policy Environment: Ongoing government reforms and a growth-supportive macroeconomic policy environment are creating highly optimistic prospects for the general insurance industry [1, 2]. This includes the national ambition and initiatives aimed at achieving “Insurance for All” by 2047 [1].

Low Insurance Penetration: The general insurance business in India currently has a penetration level of under 1%, which indicates immense untapped potential and long-term room for growth [3].

MSME Sector Growth and Budgetary Support: Government intentions and recent budgetary enablements to financially include and support the MSME (Micro, Small, and Medium Enterprises) sector are opening up substantial insurance opportunities [4, 5]. This provides new avenues for credit insurance and overall business protection products tailored to a massive population of SMEs [4, 5].

Geographic Expansion: There are growing opportunities to expand insurance books and increase awareness beyond major metropolitan areas into Tier 2 and Tier 3 cities [6, 7].

Market Consolidation and Pricing Discipline: As more insurers become publicly listed and the broader market consolidates, pricing discipline within the industry is expected to structurally strengthen over the medium to long term [3].

GST Rationalization: Specifically within the motor insurance side, GST rationalization has acted as a tailwind, providing visible benefits and driving premium growth in the private car segment [8, 9].

Digitalization and New Product Innovation: The government’s agenda to achieve insurance penetration faster and quicker is driving the adoption of innovative, tech-enabled products like Parametric Insurance [10, 11]. These products leverage digital interfaces to issue policies to large populations at once and can automatically settle claims in a matter of minutes or hours, drastically easing the operational burden of traditional claim processing [12, 13].

Primary Market Expansion: The expected broader growth of both primary insurance and reinsurance markets in India, alongside other large and fast-growing global markets, provides a strong foundational tailwind for insurers and reinsurers alike [14].

What is the general outlook of this industry?

asof: 2026-04-16

The general outlook for the insurance industry is highly optimistic, largely driven by ongoing government reforms and a growth-supportive macroeconomic and policy environment [1, 2].

Massive Untapped Potential and Government Initiatives A major factor driving this positive outlook is the current low penetration of general insurance in India, which stands at under 1% [3]. This low baseline indicates immense potential for expansion [3]. To capture this market, the industry is aligning itself with the government’s national ambition to achieve ‘Insurance for All’ by the year 2047 [2]. Because the government wants to drive penetration faster and more efficiently, there is a growing demand for innovative and easily accessible products like parametric insurance, which can be issued digitally to large groups of people at once and settle claims in a matter of minutes [4, 5].

Expansion into the MSME Sector and Tier 2/3 Cities Recent government budgets have introduced significant enablements for the Micro, Small, and Medium Enterprises (MSME) sector [6, 7]. This shifting policy environment opens up substantial new insurance opportunities, particularly concerning credit and overall financial protection for these businesses [6-9]. Insurers are actively leveraging these policies to expand their portfolios, with a strategic focus on expanding operations and awareness programs deep into Tier 2 and Tier 3 cities [8, 9].

Market Consolidation and Pricing Discipline Structurally, the industry is benefiting from strong domestic market growth momentum [10]. As more insurance companies become publicly listed and the market undergoes consolidation, pricing discipline is expected to strengthen over the medium to long term [3]. This evolving landscape enables industry players to capitalize on the expected growth of both the primary insurance and reinsurance markets in India, alongside other large and fast-growing international markets [11].

Overall, the industry expects to maintain its current momentum, leaning on digital initiatives, prudent risk selection, and favorable policy reforms to deliver improved performance in the future [1, 3].

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.