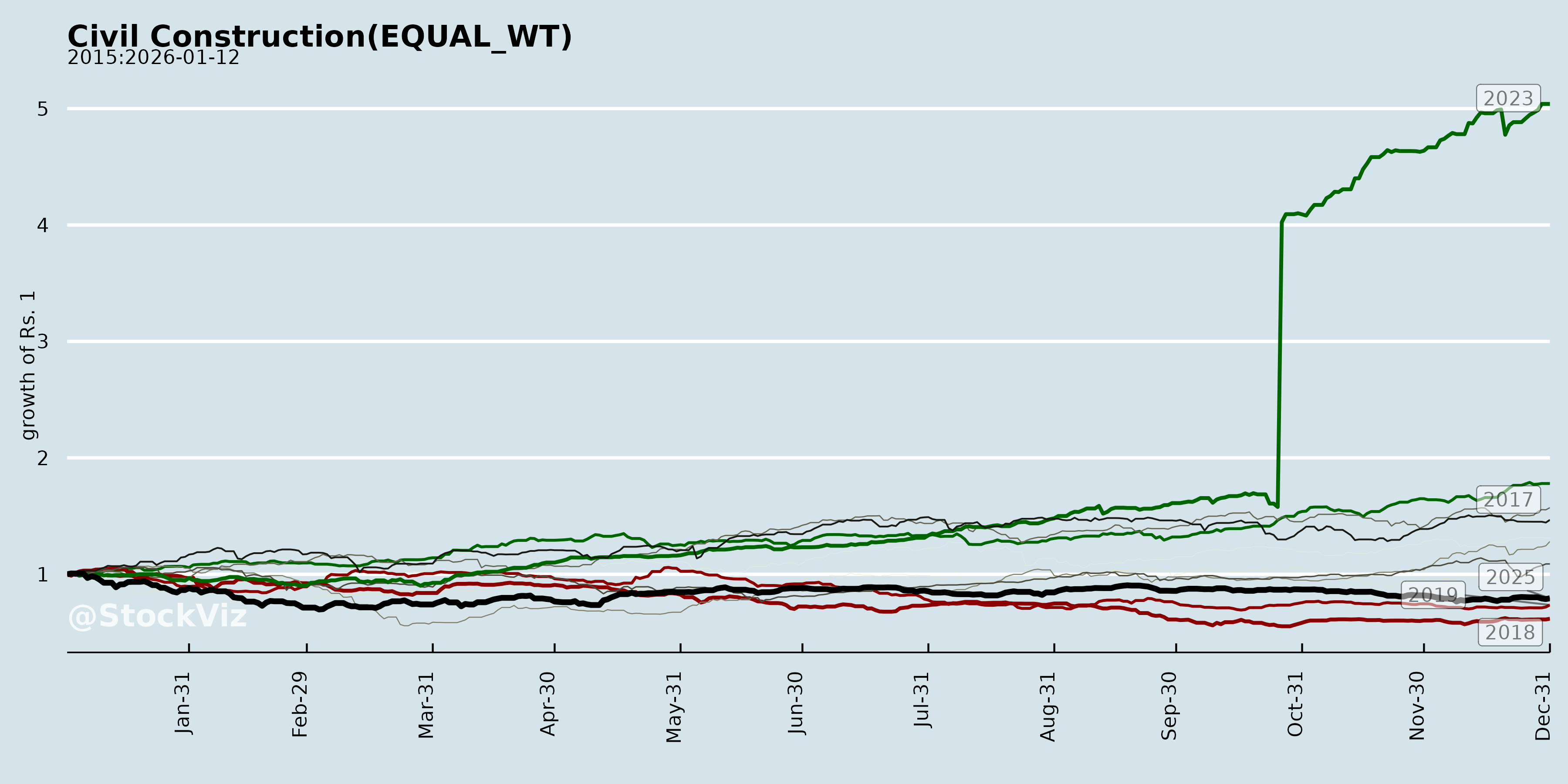

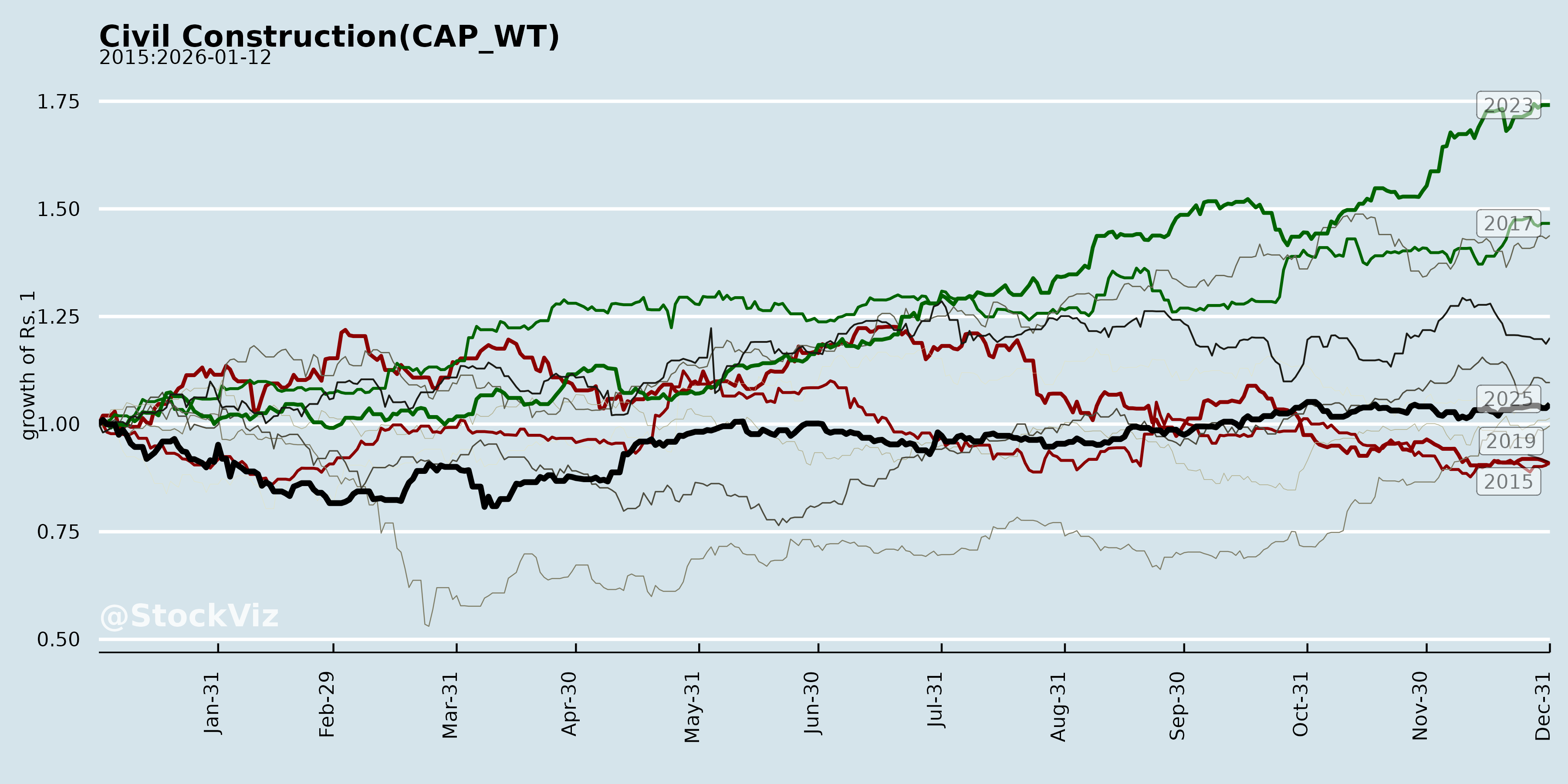

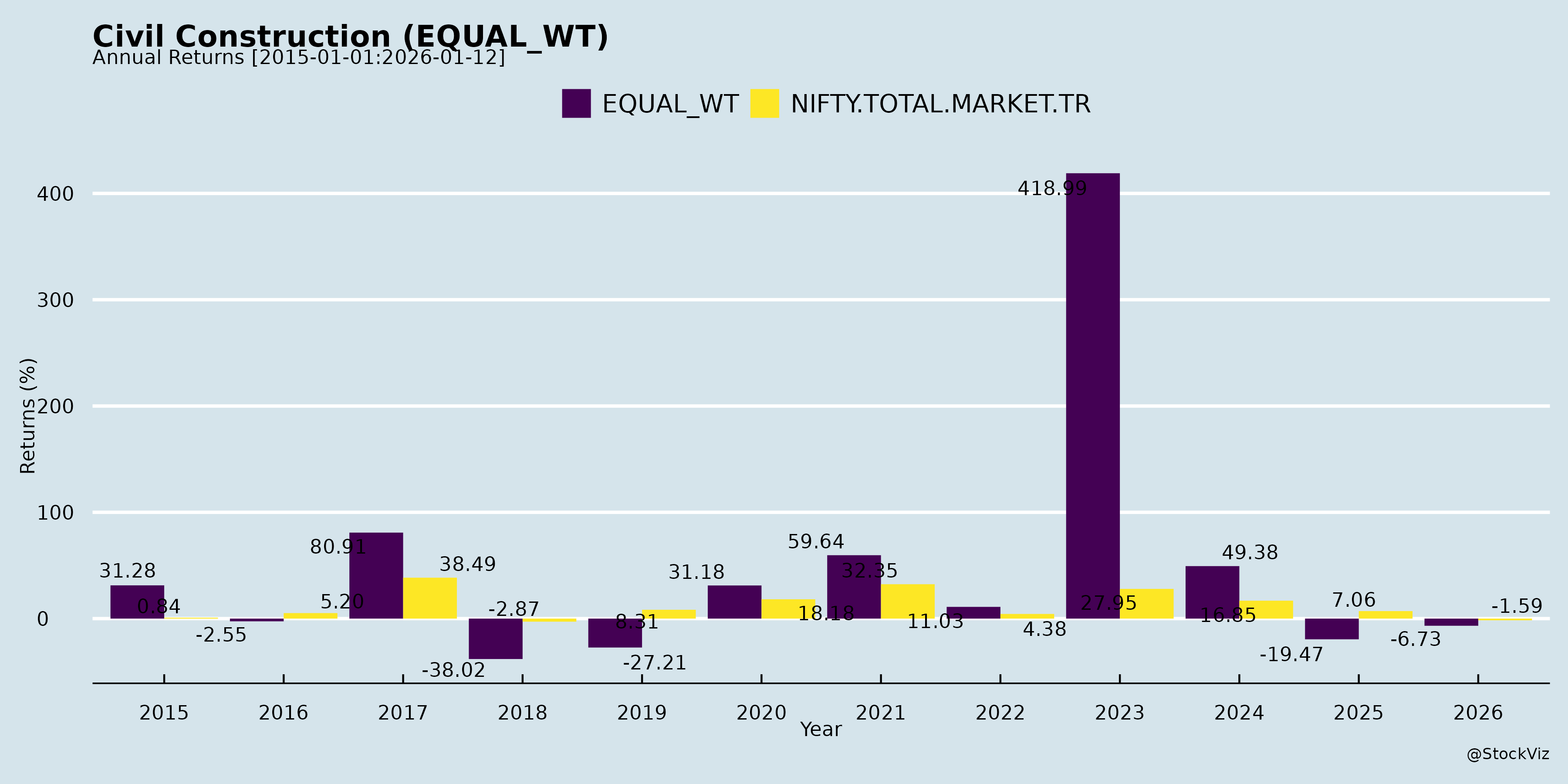

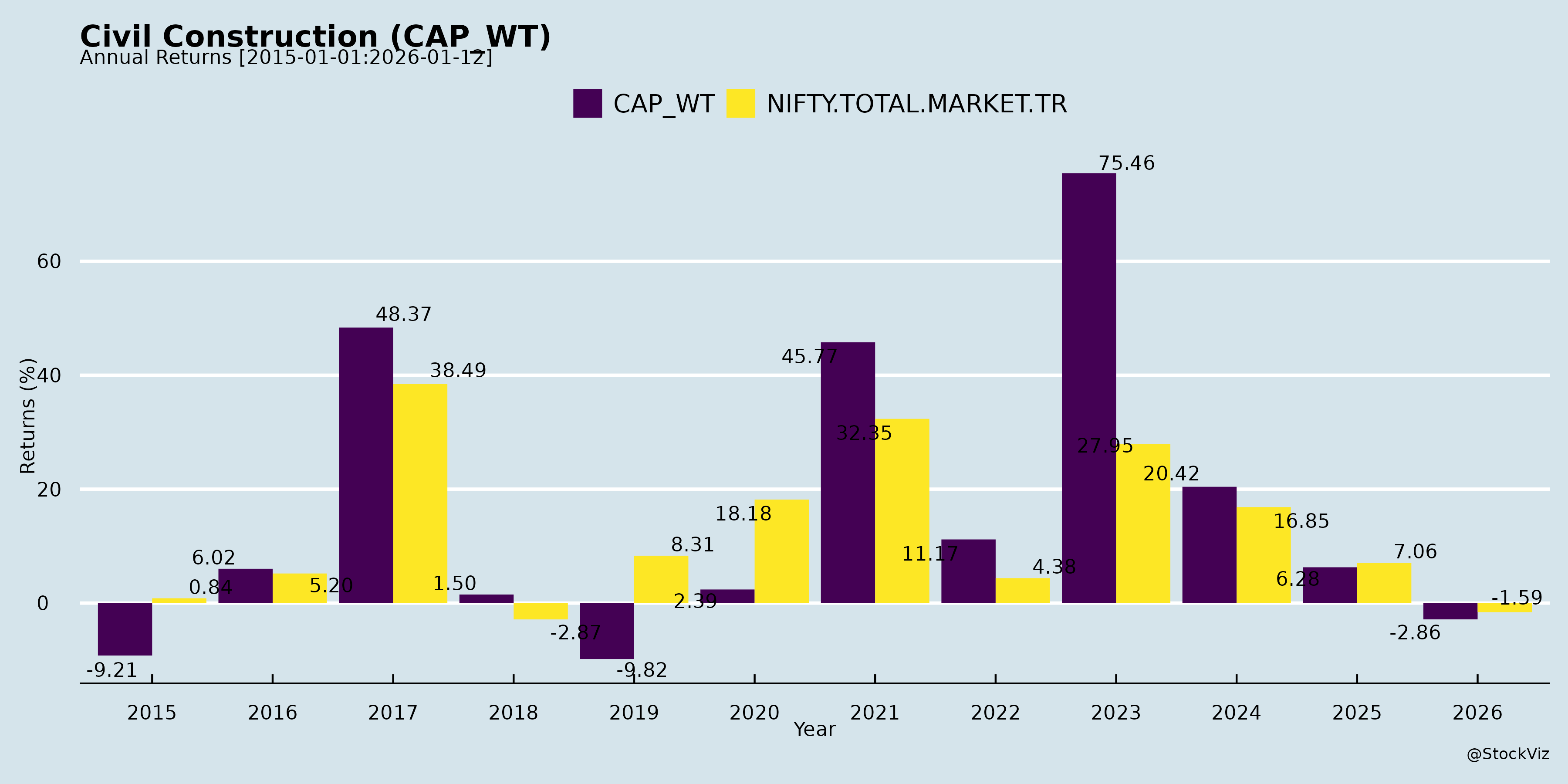

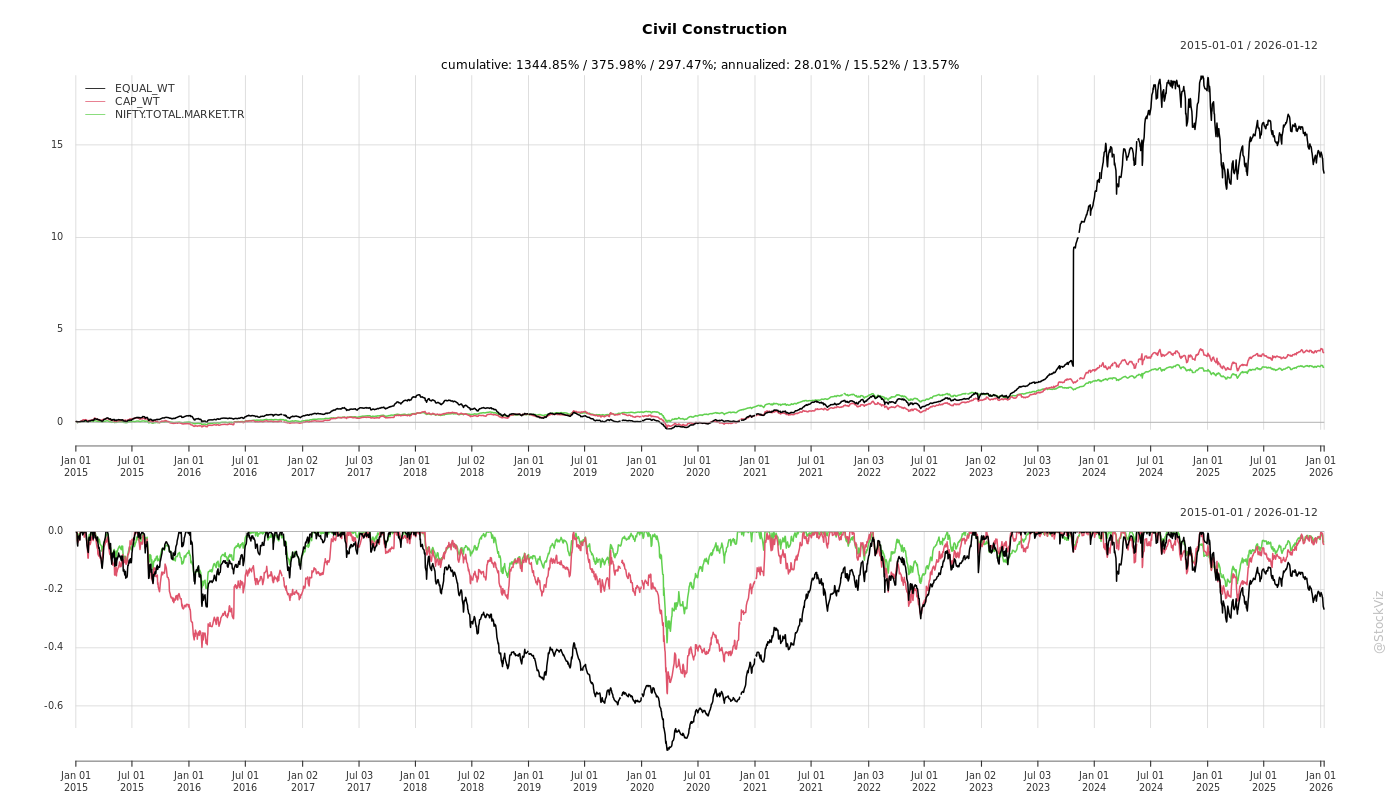

Civil Construction

Industry Metrics

May 8, 2026

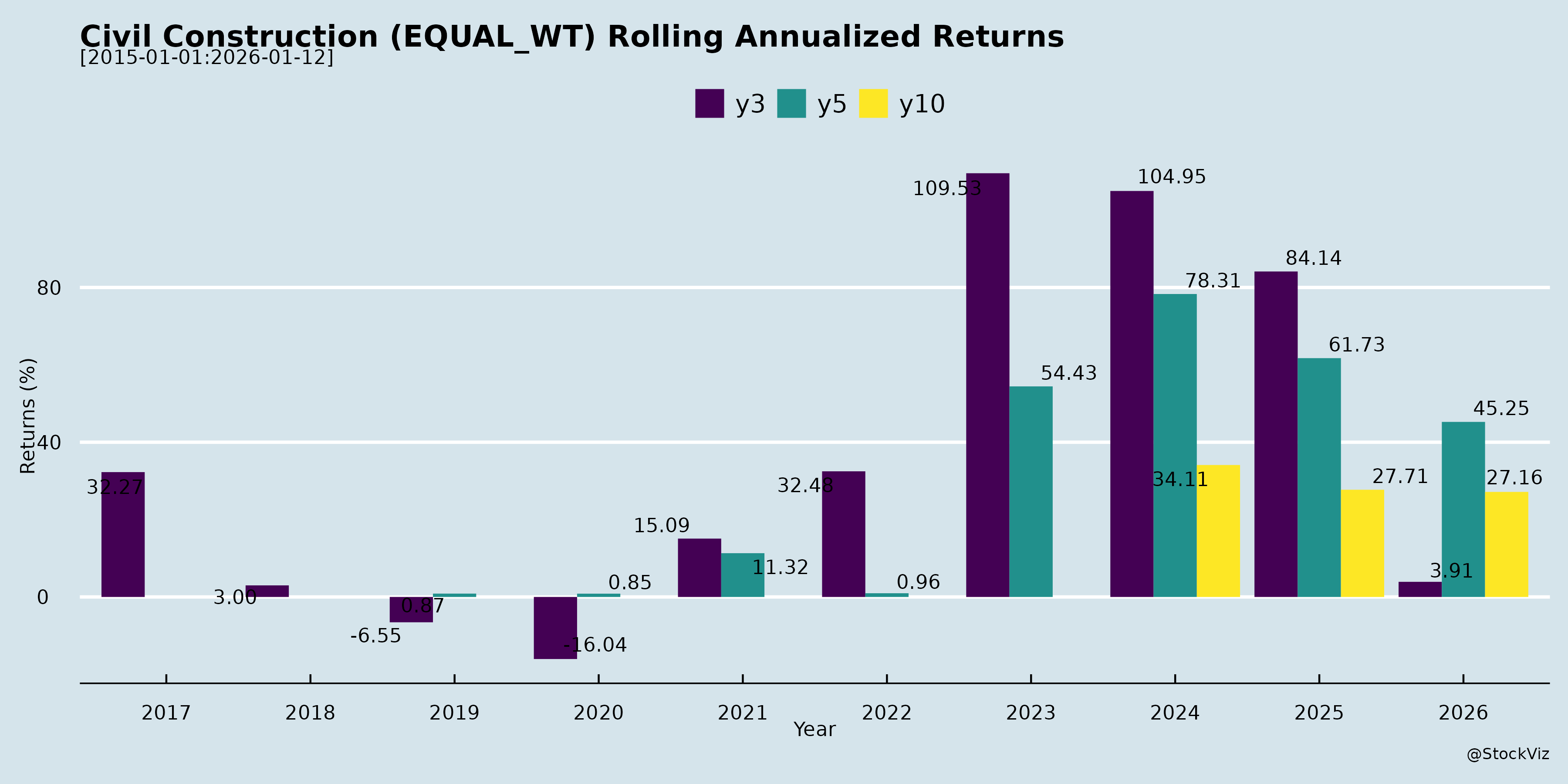

Annual Returns

Cumulative Returns and Drawdowns

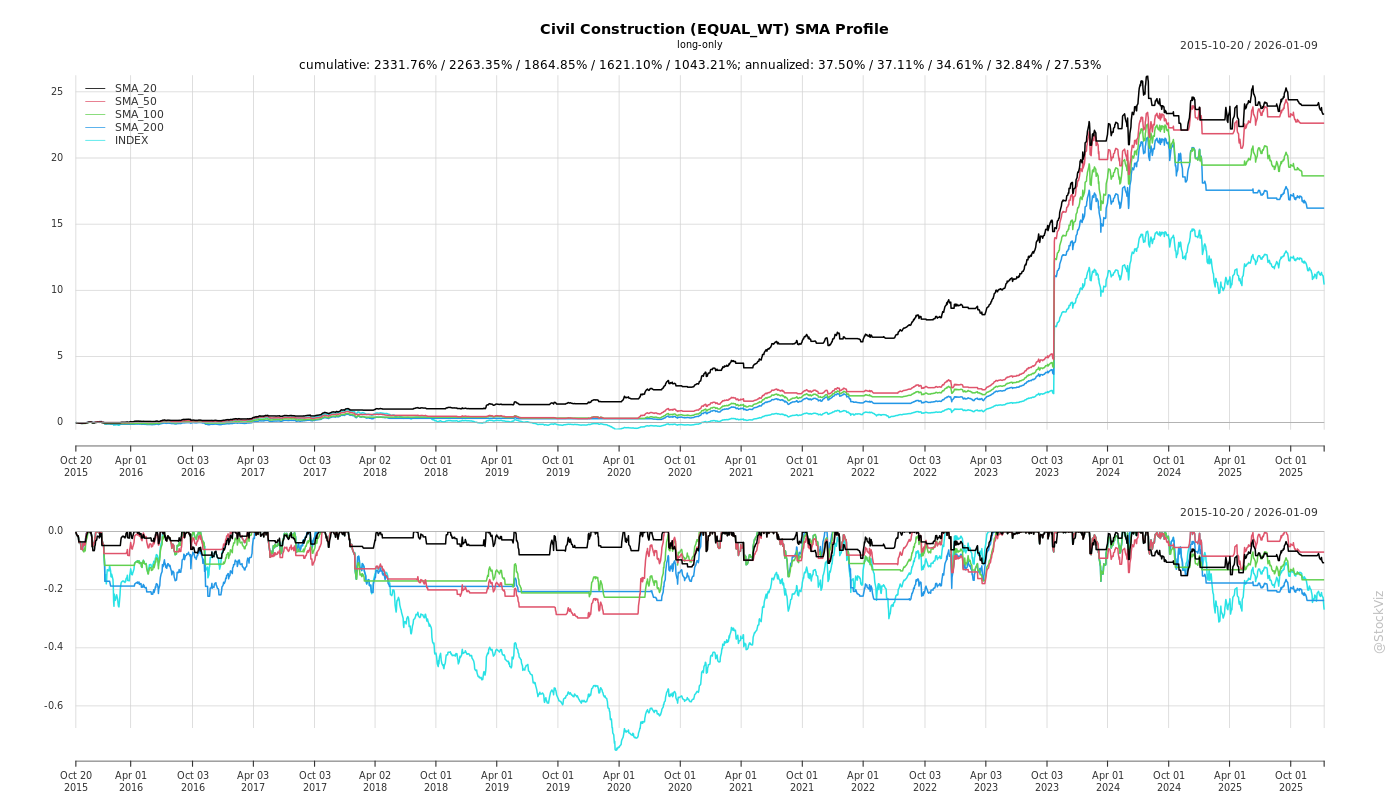

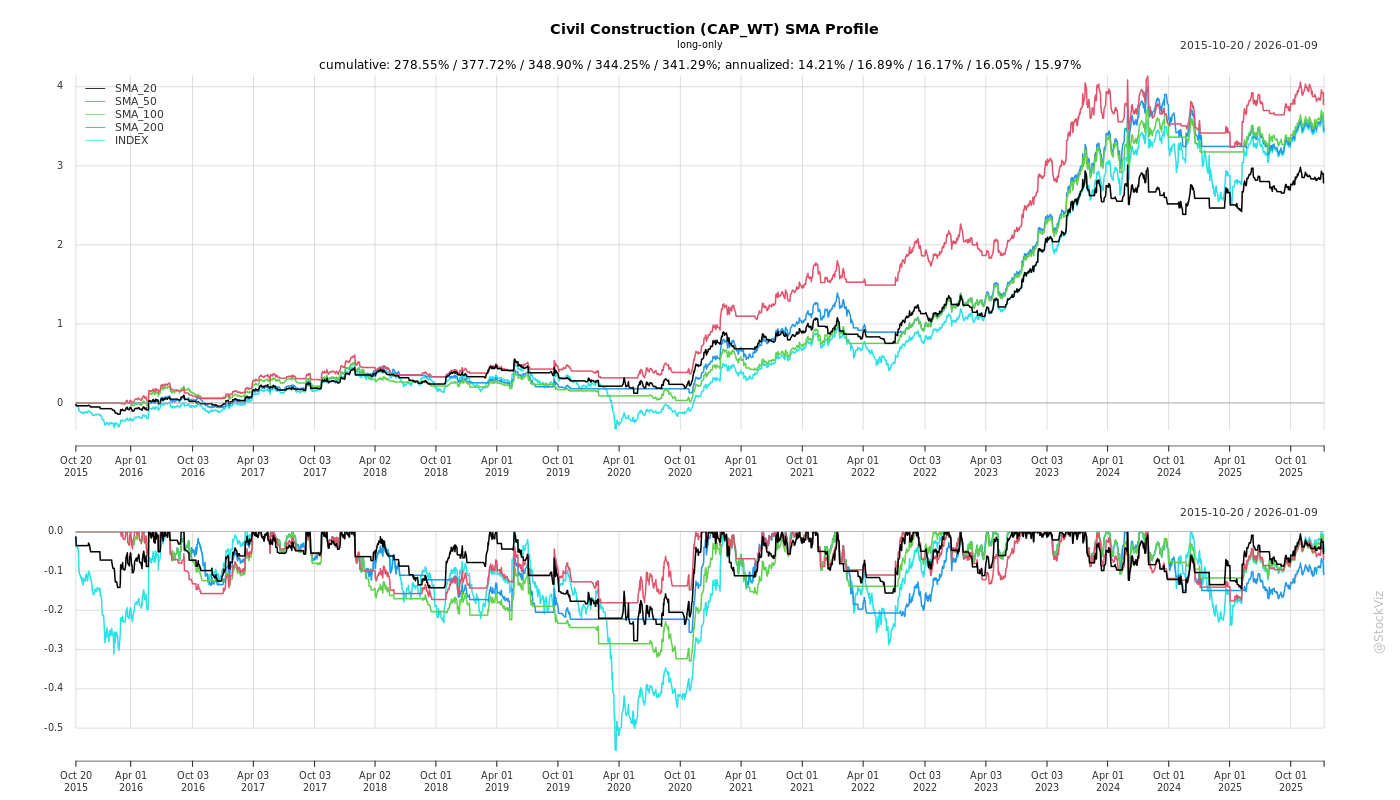

SMA Scenarios

Current Distance from SMA

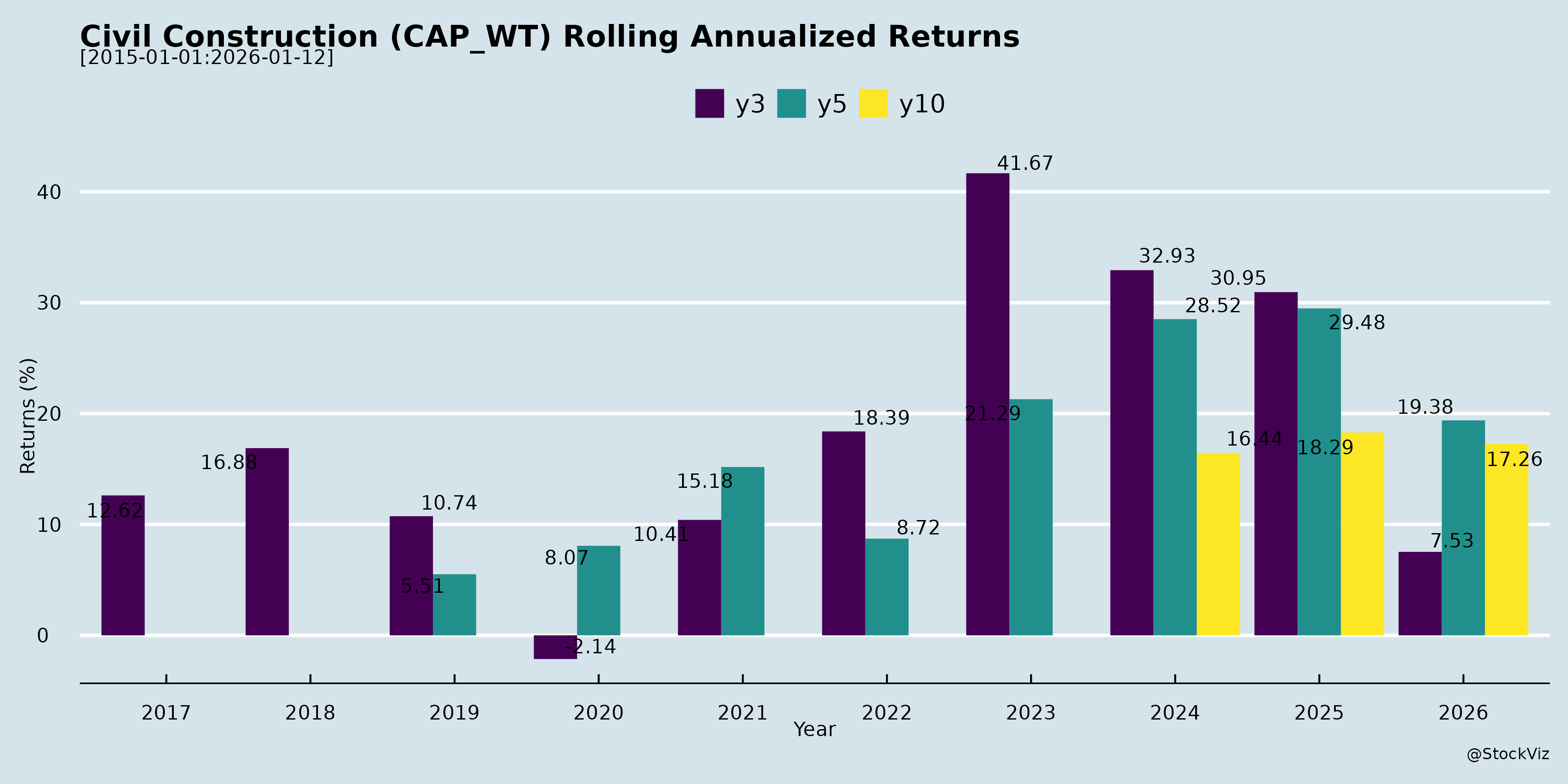

Rolling Returns

Fundamental Ratios

AI Summaries

How have the challenges and oppurtunities evolved over time?

asof: 2026-04-14

The Evolution of Challenges over Time

- Environmental Regulations and Seasonal Disruptions: Pollution and National Green Tribunal (NGT) construction bans have evolved into a recurring annual challenge, particularly in the NCR region, severely disrupting operations from the festive season (October/Diwali) through the end of January [1-4]. For example, in an 18-month project, 6 to 8 months can be lost solely due to pollution-related work stoppages [5, 6]. To mitigate this, companies are being forced to evolve their methods by adopting dust-free technologies like Mivan shuttering, pre-cast technology, and water sprinklers [7-10].

- Labor Shortages and Escalating Costs: The nonavailability of workers has escalated from a lurking issue to a “full-blown issue,” particularly worsening post-elections [11, 12]. Because of labor scarcity and diminishing skills, unit rates for labor are increasing every quarter, often far beyond what government contracts recognize [13, 14]. This challenge is driving the industry toward greater standardization, offsite work, and heavy mechanization to reduce dependency on manual labor [15, 16].

- Administrative Bottlenecks and Payment Delays: The execution of complex projects continues to be hindered by challenges in securing Right of Way (ROW), land acquisition, and timely design approvals [17-19]. Flawed original tender designs have led to massive delays requiring complete redesigns on the ground [20-23]. Additionally, delayed payments from state and central government entities—sometimes caused by impending elections or funding dry-ups—have strained working capital and impacted company turnover and margins [24-27].

- Intense Competition and Margin Pressures: The market has experienced intense competition, with many projects being aggressively bid below estimated costs, causing severe margin compression [28, 29]. However, as the overall volume of awarded projects increases, the industry expects this challenge to stabilize, as bidders with limited net worth will deplete their capacity to take on new projects [30, 31].

The Evolution of Opportunities over Time

- Unprecedented Government Capital Expenditure: The sector is benefiting from massive, sustained government push. For example, the Union Budget for FY27 raised capital expenditure for core infrastructure by 9% to ₹12.2 lakh crore, which includes a record ₹3.09 lakh crore allocation specifically for the Ministry of Road Transport & Highways [32]. This has created a robust pipeline of multi-trillion rupee opportunities across roads, railways, and defense [32-35].

- Emergence of New Technological Sectors: Companies are shifting their focus to capitalize on the technology and energy transition. The boom in data centers in the U.S. and India has spurred massive mechanical engineering opportunities for transmission lines, substations, and towers [36-39]. Furthermore, India’s target of 500 GW of non-fossil capacity by 2030 has opened a massive market for Solar Park Development, Battery Energy Storage Systems (BESS), and Green Hydrogen infrastructure [40-45].

- Expansion in Water and Urban Infrastructure: Driven by government initiatives like the Jal Jeevan Mission and AMRUT, there is a booming, long-term opportunity in rural water distribution, sewage treatment, and bulk water supply projects [46-48]. In tandem, rapid urbanization is driving vast opportunities in metro rail networks, institutional buildings, and international-standard sports infrastructure [49-51].

- Innovative Funding and Monetization Models: The financial ecosystem has evolved favorably with structural reforms by SEBI regarding REITs and InvITs, allowing infrastructure developers to monetize operational assets and recycle capital more efficiently [52-55]. New “self-funding” urban redevelopment models are also emerging as superior alternatives to traditional PPP models, offering developers vast land parcels for development without requiring upfront monetary investments [56, 57].

- Global Expansion and Value Engineering: Because the Indian public sector heavily relies on highly competitive, lowest-bidder (L1) models, domestic engineering and construction firms are finding lucrative opportunities by expanding into international markets (such as the Middle East, Africa, and South America). In these global markets, a company’s past experience with complex projects, modernization, and quality carries more weight than just pricing, offering higher-margin opportunities [58-63].

What are the headwinds affecting this industry?

asof: 2026-04-14

The infrastructure, engineering, and construction industry is currently navigating a complex array of headwinds, ranging from environmental disruptions and severe financial constraints to administrative bottlenecks and global economic uncertainties.

Environmental and Weather Disruptions Prolonged and erratic monsoon seasons have severely disrupted operations, causing work stoppages across various regions and delaying the achievement of billing milestones [1-6]. Additionally, pollution-related construction bans, such as the enforcement of the Graded Response Action Plan (GRAP) in the Delhi NCR region, have forced complete halts to construction activities for months at a time [7-12]. This has become a recurring annual issue that significantly impacts top-line revenue growth and project timelines [7, 9].

Financial, Liquidity, and Margin Pressures Delayed payments from clients, particularly in government-funded projects like the Jal Jeevan Mission, have placed immense pressure on working capital and forced companies to slow down execution [13-18]. For several players, high working capital requirements and longer collection periods in PSU/government contracts result in large amounts of retention money getting stuck [19-21]. Some companies in the sector are facing severe liquidity constraints, negative net worth, and insolvency proceedings (including NCLT applications) due to continuous cash losses, delayed debt servicing, and Non-Performing Asset (NPA) classifications by lenders [22-26]. Furthermore, intense competitive bidding is squeezing profitability, with many contractors quoting below project estimates just to secure orders, which severely compresses EBITDA margins [27-32].

Administrative, Land, and Policy Bottlenecks There has been a marked slowdown in new project awarding by authorities like the Ministry of Road Transport and Highways (MoRTH) and NHAI over the past two years, which was further exacerbated by state and national elections [28, 33-36]. Execution is frequently hindered by delays in securing Right of Way (ROW), land acquisition, and necessary environmental or administrative clearances from clients [37-42]. A strategic policy shift by the government from the Hybrid Annuity Model (HAM) to Build-Operate-Transfer (BOT) toll models has also stalled bidding pipelines, as developers wait for Model Concession Agreements (MCA) to undergo modifications [43-47]. Furthermore, design changes and the implementation of new earthquake codes have led to mandatory rework and extended project timelines [48, 49].

Labor and Supply Chain Constraints The industry faces significant labor availability shortages, especially during festival seasons (like Holi) or election periods when migrant workers return to their hometowns [4, 9, 50, 51]. Consequently, the unit rates for scarce skilled labor are rising faster than government estimates recognize, putting additional pressure on project costs [52, 53]. Compliance with newly implemented Labour Codes has also introduced one-time financial impacts and increased administrative costs for contractors [54-56]. Commodity price volatility—specifically for raw materials like steel, cement, aluminum, copper, and crude oil—remains a persistent threat to margins [57-61]. Geopolitical tensions and global wars have driven up crude prices, directly impacting fuel and bitumen costs [62, 63].

Global Market and Sector-Specific Uncertainties Companies providing international engineering services are battling a slowdown in the global automobile and EV industries, which has forced some to downsize their mechanical engineering teams [64-66]. Finally, policy and tariff uncertainties in the US market, alongside election-year apprehension, have caused builders to hold back on capital spending, delaying major high-rise and industrial projects [67-72].

What are the key things to understand about this industry?

asof: 2026-04-14

India’s construction and infrastructure industry is a massive, multi-faceted sector that serves as a primary engine for the country’s economic growth. Understanding this industry requires looking at its economic scale, government drivers, the operational models of its key players, and the unique challenges it currently faces.

Here are the key things to understand about this industry:

1. Massive Economic Scale and Growth Projections

The construction sector is a cornerstone of India’s development, acting as the second-largest contributor to the national economy after agriculture [1]. * Economic Contribution: It accounts for 8.4% of the national Gross Value Added (GVA) at constant prices [1]. * Market Size & Trajectory: The market size was valued at USD 1.04 trillion in 2024 and is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.1%, reaching USD 2.13 trillion by 2030 [2]. * Global Standing: With sustained investment momentum, India is projected to become the world’s third-largest construction market, with the sector expected to contribute a massive 15% to the country’s GDP by 2030 [1, 3].

2. Strong Government Push and Policy Support

The sector’s growth is heavily reliant on and driven by government capital expenditure [1]. * Budgetary Focus: The Government of India (GoI) intends to reach a $5 trillion economy heavily through infrastructure development because of its high multiplier effect [2]. To achieve this, the budget raised the capex target by 11.1% to INR 11.1 trillion [4]. * National Infrastructure Pipeline (NIP): The government has expanded the NIP to encompass 7,400 projects, representing a massive ₹11,10,000 crores investment in both rural and urban infrastructure [3]. * Funding and Investment: To attract capital, the sector allows 100% Foreign Direct Investment (FDI) through the automatic route [4]. Furthermore, new funding models like Toll-Operate-Transfer (ToT) and Infrastructure Investment Trusts (InvITs) have been introduced to increase interest from international equity and debt funds [3]. * Policy Reforms: Initiatives like the Real Estate Act (RERA), GST, and REITs have been implemented to reduce approval delays and strengthen the industry framework [3].

3. Diverse Operational Segments

Construction spending flows primarily into three distinct segments: infrastructure, real estate, and industrial construction [1]. * Infrastructure (69% share): This encompasses roads and highways, railways, airports, ports, telecom, power, and oil and gas [1, 5]. For instance, the government has set ambitious targets like building 10,000 kilometers of national highways in a single year [6]. There is also a massive push for water infrastructure through the Jal Jeevan Mission and AMRUT schemes [7, 8]. * Building Construction (25% share): This involves the development of residential townships, commercial complexes, healthcare facilities, and institutional buildings [5, 9-11]. * Industrial/Manufacturing (6% share): This covers the construction of large-scale industrial clusters, data centers, and specialized facilities [5, 9, 12].

4. Prevalent Industry Challenges and Headwinds

Despite the massive growth potential, companies in this sector face several systemic and environmental hurdles: * Pollution-Related Halts: Environmental regulations pose a major challenge, particularly in the Delhi NCR region [13]. When pollution levels rise and the Graded Response Action Plan (GRAP) 3 or 4 is initiated, the government entirely bans construction [14]. These bans cause significant spillover delays; for example, an 18-month project can easily stretch to 26 or 28 months due to these winter stoppages [13]. * Labor Scarcity and Rising Costs: The industry is grappling with scarce labor availability and diminishing worker skills [15]. Consequently, unit rates for labor are increasing every 3 to 4 months, often outpacing the cost escalations recognized by government clients [15]. * Administrative and Election Delays: Awarding of new projects can be highly cyclical. Recently, awarding activities by the National Highways Authority of India (NHAI) and other bodies remained subdued due to administrative delays and various state elections [16, 17]. * Payment Delays: While central government projects are relatively stable, contractors frequently experience sluggish payment cycles and stuck final payments when dealing with certain state governments (like Himachal Pradesh and Assam) [18, 19]. * Intense Competition: Bidding can be fiercely competitive, with many players quoting below estimates just to win jobs, which severely compresses profit margins [6, 20, 21].

5. Strategic Business Models

To navigate these challenges and protect profitability, leading companies employ strategic operational models: * Asset-Light Models: To avoid heavy capital investments in machinery and improve margins, many players rely on third-party subcontractors for equipment, materials, and labor [22-26]. This approach ensures cost efficiency and geographical scalability [23]. * Selective Bidding for High Margins: To combat fierce competition, disciplined companies are shifting toward selective bidding. They prioritize fully-funded, short-to-medium tenure projects (6-12 months) that offer higher Internal Rates of Return (IRR) and margins typically above 10% [27-31]. * Tech-Based Integrated EPC: Companies are moving beyond basic civil construction to offer end-to-end Engineering, Procurement, and Construction (EPC) services [32, 33]. This includes integrating advanced technologies like the Internet of Things (IoT) into Building Management Systems (BMS) for energy efficiency and constructing “Net Zero” buildings [33, 34]. * Diversification: To mitigate concentration risks, contractors continuously diversify their portfolios across different geographies and sub-sectors, blending traditional road and building projects with high-growth areas like renewable energy, water distribution, and complex mechanical/electrical engineering tasks [23, 35-39].

What are the tailwinds affecting this industry?

asof: 2026-04-14

Government Capital Expenditure and Favorable Policies The infrastructure, engineering, and construction sectors are experiencing massive tailwinds driven by the Indian government’s commitment to infrastructure-led economic growth and its vision to become a $5 trillion economy [1-3]. The Union Budget for FY ’27 raised public capital expenditure on core infrastructure by 9% to 11.1%, reaching approximately ₹12.21 trillion [1, 2, 4, 5]. This is anchored by the National Infrastructure Pipeline (NIP), which plans an investment of ~₹111 lakh crore across multiple sectors over a five-year period [6-8].

Additionally, the government is introducing an Infrastructure Risk Guarantee Fund to reduce financing risks during the construction phase, encouraging lenders to actively fund projects [9, 10]. Policy reforms, such as 100% Foreign Direct Investment (FDI) via the automatic route, faster bill clearances, lower bank guarantee requirements, and SEBI’s enhanced regulations for REITs and InvITs, are deeply strengthening long-term institutional participation and capital recycling [11-14].

Roads, Highways, and Logistics Expansion The Ministry of Road Transport & Highways (MoRTH) and the National Highways Authority of India (NHAI) continue to be major growth drivers. MoRTH received a record budget allocation of ₹3.09 lakh crore for FY ’27 (an 8% year-on-year increase), while NHAI was allocated ₹1.87 lakh crore (a 10% increase) [5, 15-17]. NHAI’s debt-to-equity ratio has significantly improved from roughly 50% in FY ’22 to around 20% in FY ’25, creating the fiscal headroom needed to support an ₹8 lakh crore project pipeline from FY ’26 to FY ’28 [18, 19].

National highway toll collections are projected to cross ₹1 lakh crore by FY ’27, driven by higher traffic volumes and expansions of high-speed corridors [18, 19]. To facilitate this, the government is shifting focus toward large Build-Operate-Transfer (BOT) and Toll-Operate-Transfer (TOT) models to enhance public-private partnerships (PPP) [18, 20, 21]. Furthermore, India’s logistics sector is set to grow at a CAGR of 8% over the next five years, with the Grade A and B warehousing segment growing at 12% to 12.5% [22, 23].

Renewable Energy and Battery Energy Storage Systems (BESS) India’s ambitious target to achieve 500 GW of non-fossil energy capacity by 2030 is unlocking extensive EPC opportunities [24-26]. Renewable energy has reached permanent grid parity without subsidies, accelerating widespread industrial adoption [27]. Because surging renewable integration requires grid stability, Battery Energy Storage Systems (BESS) have emerged as a high-growth, margin-accretive vertical [27-29]. The government is preparing policies to make BESS mandatory for solar and wind developers, driving a projected BESS capacity of 236 GW by FY ’32—translating into a $57 billion market [25, 26, 30]. The FY ’26 budget reinforces this transition with ₹1,09,000 crore allocated for energy infrastructure [25, 26].

Grid Modernization and Conventional Power There is a massive push for transmission and distribution (T&D) upgrades, smart-grid rollouts, and a target to install 250 million smart meters under schemes like the Revamped Distribution Sector Scheme (RDSS) [31, 32]. Simultaneously, rising per-capita power consumption is driving a robust pipeline of ~53 GW in thermal capacity expansion over the next 5-7 years, creating significant opportunities for integrated Balance of Plant (BOP) and Engineering, Procurement, and Construction (EPC) players [33].

Water, Urban, and Railway Infrastructure Heavy investments are flowing into water sanitation, reuse, and distribution projects. The Jal Jeevan Mission received an allocation of ₹67,670 crore for FY ’27, which will support municipal and rural water supply networks across the country [9, 34-36].

In urban development, the Smart Cities Mission and Pradhan Mantri Awas Yojana (PMAY) are receiving increased funding to modernize public services and accelerate affordable housing [8]. The aviation sector aims to expand operational airports to 220 by 2025 under regional connectivity schemes [8]. Meanwhile, the railway and metro sectors are prioritizing decongestion on high-density routes through dedicated freight corridors and economic rail corridors under the PM GatiShakti framework [37, 38].

International Markets and Niche Sectors * United States: The U.S. construction sector is entering a strong recovery phase with improved capital spending from Tier-1 clients [39]. Significant investments in data centers, electrification, and EV infrastructure are spurring high demand for civil engineering, structural design, and T&D services (substations, lines, poles, and towers) [40-43]. * Middle East (GCC): The GCC region is experiencing strong growth underpinned by massive investments in Artificial Intelligence (AI) infrastructure, hyperscale data centers, and large-scale urban development projects in Saudi Arabia and the UAE [44, 45]. * Sports Infrastructure: With India preparing to host the 2030 Commonwealth Games and the 2036 Olympics, sports infrastructure (such as Olympic-standard swimming pools and stadiums) is expected to grow meaningfully over the next 5 to 7 years [46-48]. * Mining & Minerals: There is a rising demand for critical and transition minerals to support the global energy supply chain. Regulatory reforms, such as the auctioning of mining blocks and private sector entry, are boosting domestic mineral production and creating tailwinds for Mining Development and Operations (MDO) players [7].

What is the general outlook of this industry?

asof: 2026-04-14

The general outlook for the infrastructure, engineering, and construction (EPC) industry in India is highly positive and robust, underpinned by strong macroeconomic momentum, massive government-led capital expenditure, and diverse sectoral opportunities [1-4].

Market Size and Growth Projections The Indian construction market is positioned for exponential growth. It was valued at USD 1.04 trillion in 2024 and is projected to reach USD 2.13 trillion by 2030, growing at a Compound Annual Growth Rate (CAGR) of 12.1% from 2025 to 2030 [5]. Consequently, India is on track to become the world’s third-largest construction market, with the sector expected to contribute around 15% to the country’s GDP by 2030 [6, 7].

Government Initiatives and Capex Push The government’s ambition to create a $5 trillion economy relies heavily on infrastructure development due to its high economic multiplier effect [5]. To fuel this, the Union Budget for FY26/FY27 has seen a capital outlay increase of 9% to 12%, dedicating roughly INR 11.1 trillion to INR 12.21 trillion toward core infrastructure [8-11]. Specific allocations include: * Road Transport & Highways: A record allocation of INR 3.09 lakh crore in the FY27 budget, representing an 8% year-on-year increase [11, 12]. * Urban & Water Infrastructure: Substantial allocations of INR 85,222 crore for urban development and INR 67,670 crore for the Jal Jeevan Mission, ensuring a long-term pipeline for water and civic infrastructure projects [13-16].

Key Sectoral Drivers * Roads and Highways: While project awarding by the NHAI was subdued recently due to state elections, administrative delays, and modifications to the Model Concession Agreement (MCA) [17-21], the sector is entering a strong recovery phase. There is a robust bid pipeline of over INR 1.5 lakh crore, and the government is prioritizing large-ticket Build-Operate-Transfer (BOT) toll projects to enhance public-private participation [21-25]. * Railways and Metro: Massive investments are being directed toward easing high-density route congestion, improving freight movement, and building multimodal integration via dedicated freight corridors under the PM GatiShakti framework [22, 24]. Significant capex is also targeting high-speed rail corridors, station redevelopments, and new metro lines [26-28]. * Energy Transition, Renewables, and BESS: India’s target of 500 GW of non-fossil capacity by 2030 is generating massive opportunities in utility-scale solar, wind, and transmission and distribution (T&D) [29]. A major emerging segment is Battery Energy Storage Systems (BESS), which is projected to reach 236 GW by FY32, translating into a $57 billion market [30, 31]. Concurrently, rising per-capita power demand is driving a ~53 GW thermal power pipeline over the next 5-7 years [32]. * Logistics and Warehousing: The logistics sector is set for a massive transformation, expected to grow at a CAGR of ~8% over the next 5 years. Grade A and B warehousing is projected to grow even faster at a 12% to 12.5% CAGR, aiming to reach 800 million square feet by FY29 [33, 34].

Short-term Challenges and Industry Mitigation Despite the highly optimistic outlook, the industry has faced some short-term headwinds. These include delays in government project awards, prolonged payments from certain state authorities, and disruptions caused by severe pollution bans (like the NGT work stoppages in the Delhi NCR region during winter months) [17, 21, 35-39].

To mitigate these risks, companies are focusing heavily on selective bidding for fully-funded, high-margin projects, pivoting toward institutional and private sector works, and employing increased mechanization and off-site pre-casting to reduce dependency on site labor and bypass pollution-related work halts [40-43].

Regulatory and Technological Advancements From a regulatory standpoint, recent SEBI reforms for REITs and InvITs are viewed as a positive structural development. These reforms enhance capital deployment flexibility and encourage long-term institutional participation, allowing EPC companies to recycle capital and strengthen their balance sheets [44-47].

Operationally, the industry is witnessing an accelerated adoption of digital technologies. Companies are integrating Building Information Modeling (BIM), AI/ML, digital twins, drones, and IoT-enabled wireless Building Management Systems (BMS) to drive execution efficiency, improve safety, and control costs [29, 48, 49].

International and Export Opportunities Beyond the domestic market, the global outlook is supporting industry growth. There is strong demand in regions like the Middle East (GCC) and Africa, driven by massive investments in AI infrastructure, mega data centers, urban projects, and oil and gas expansions [4, 50, 51]. Export inquiries for capital goods and specialized engineering services have seen a notable uptick, prompting many Indian firms to aggressively expand their overseas footprint [52-55].

Copyright © 2023 SAS Data Analytics Pvt. Ltd. All rights reserved.